There are about three pointers which I sort of wanted to mention on why I am bullish on Sundrop Brands apart from the usual management, undervaluation and underperformance as compared to other FMCG companies.

1. Growth and Margin Expansion Theory for FMCG Multibaggers:

I stumbled onto a very interesting podcast off-late by SOIC, it featured the CIO of Persistence Capital, Siddhant Bhandari. I really like to listen to Siddhant and invariably end up learning something. I’ll attach the link of the podcast here: https://www.youtube.com/watch?v=p1J-J5CDwYI

He specially spent a long period of time talking about consumption led stocks. And he pointed to how getting the consumption story right is all about getting growth elevation and margin expansion right.

Let me explain both of these elements and which factors affect them in detail.

1. Growth: Double digit growth in core portfolio, introduction of new fast growing product, increase in distribution

2. Margins: Low starting margins- ability of margins to go up

Growth is the most important piece of the FMCG puzzle. To figure out growth, a company needs to grow its core business in double digits, it is fine if this is 10-12% growth. Primarily, the penetration and distribution expansion has been the factor driving core business growth for these companies. Secondly, they need to introduce a fast growing new product.

You can see that this has been the path followed by consumption led multi-baggers in the past. It also describes my thesis for how it can play out similarly in Sundrop Brands

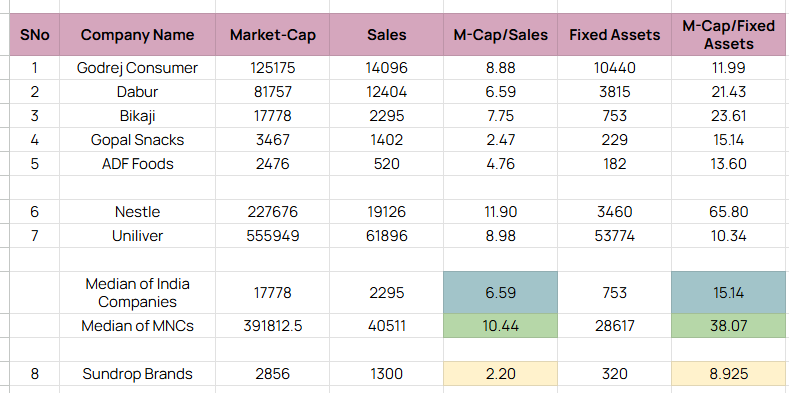

Similarly on the margin front, the company’s margins are the most depressed they have ever been in any cycle. And to me, I think the reason is not some problems with the product portfolio, I sensed that the previous promoter wasn’t as interested in running this India business.

I have two pieces of evidence here: One, the fact that fixed assets increased but the revenues remained constant over the past 12 years.

Fixed assets went up 4X in the 12 years since March 2013

However revenues remained constant

Second, look at the quality of the investor presentation these guys made. It seemed as if there was no value creation happening in the core listed entity and the entire investor relations department was coasting at their job

This one above seems like some internal document which they just took and pasted onto the deck. Does this happen when a promoter genuinely wants to make money through a listed entity?

SME stock presentations are much better than this. I think there was some sort of incentive misalignment in terms of private entities being present or some other thing which we are not privy to.

2. Promoter Buying in the Stock

Again, one thing which people haven’t mentioned here is the very recent promoter buying which the stock saw:

The price here was higher than the price the company currently trades at

3. Interesting hiring patterns:

When I saw that Ashish Kumar Sharma has been appointed the CEO and ED of Agro Tech line of the business, I tried to find out who took his place in the team as the Marketing Head and it turns out, he is somebody who has returned to the company’s fold after 5-6 years.

He was part of the company when Sundrop was in the hyper growth phase and led the West India Marketing efforts

All in all, these three things make me feel like a lot is changing in the business. We’ll know the full impact of it in a few quarters, but the interesting bit is that financials are a lagging indicator to company performance, things like the ones I’ve mentioned above invariably tend to be forward looking indicators. Where will these changes take us, I really don’t know- but what provides me a lot of comfort is ironically, how badly this business has been run till now.