Sundaram Finance Holding Ltd (SFHL) is a very interesting company. I used to hold Wheels India and it popped up as promoter share holder. Digging deeper I realized that this was an entity which was demerged from Sundaram Finance. Now TVS family has split and Sundaram group has gone to TSF group. They have their holding in all the auto ancillary companies directly and through SFHL. It is similar to Tata investments. SFHL also has mandate to invest upto 10% in other opportunistic bets.

Looking further at its holdings led to to realization that it was holding 23.57% in a gem called Brakes India Pvt Ltd. This is a high growth high ROCE business. A close comparison would be Wabco India. As these companies make complete braking system including actuation and not a single component, they command a high PE ratio.

Another positive is that none of its companies face EV disruption except for Turbo Energy which is 10-15% of valuation. Turbo chargers are still in growth phase in India. Non of Maruti engines use turbo chargers yet. Turbo charges in commercial vehicles are not going away.

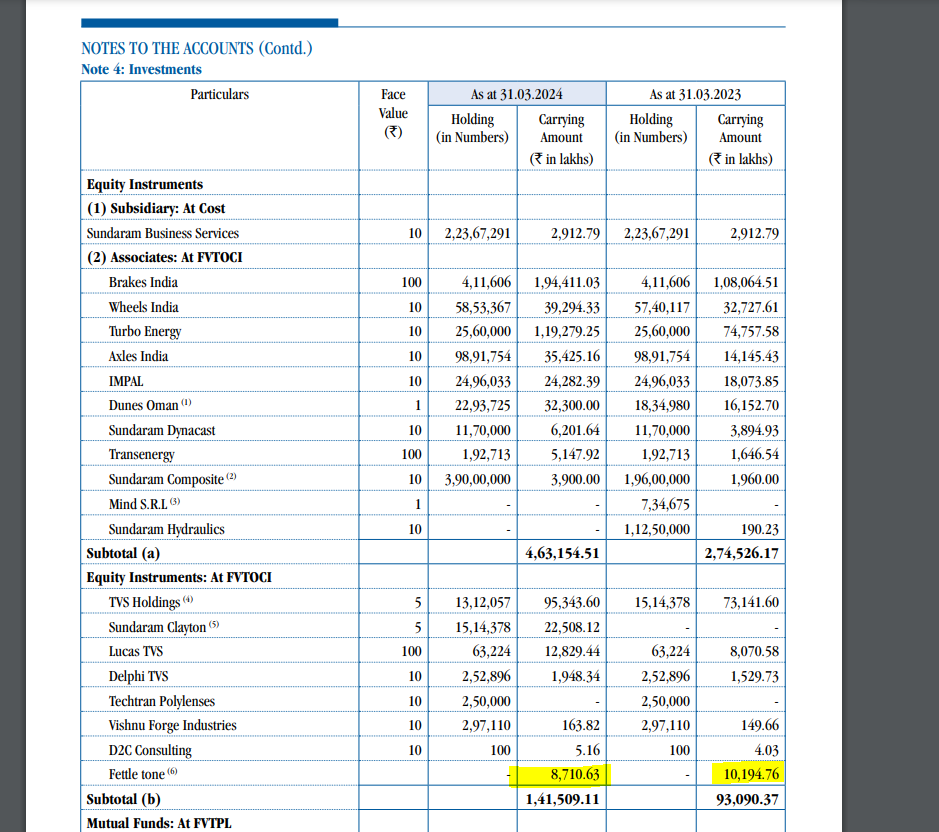

Below table lists holdings and I have tried to do a valuation exercise.

Companies

% Holding

Mcap (in crore)

Profit (in crore)

Assumed PE

Implied value

Brakes India

23.57%

716.00

50

8438

Turbo Energy

32.00%

265.00

15

1272

Axles India Limited

38.81%

86.00

20

668

The Dunes Oman FZC (LLC)

43.69%

56.00

15

367

Sundaram Dynacast

26.00%

20.00

20

104

Transenergy

42.41%

9.00

15

57

SBSL

100.00%

17.00

15

255

IMPAL

20.00%

1650

330

Wheels India Limited

23.96%

2000

479

TVS Holding

6.49%

30000

1947

Sundaram Clayton

7.49%

3540

265

Sundaram Composite

39.00%

Annual report

15

Lucas-TVS

5.32%

Annual report

65

Delphi TVS Technologies

3.19%

Annual report

20

Fettle Tone

2.71%

Annual report

87

Cash and equivalent

Annual report

720

15089

Fettle Tone is one of promoter of Max health insurance. It is part of opportunistic bet which I have mentioned earlier.

SBSL - Sundaram Biz Services Ltd is into IT/BPO

Current market cap even after a sharp run-up is 9000 crore.

Below link summarizes performance of SFHL and its major holdings.

Disc: Invested around Rs 200. Not a buyer at this level.

But I am very bullish on Brakes India. This can command much better valuations with getting into advanced braking solution. They are catching up with Wabco. Infact Brakes India was JV with ZF and when ZF acquired Wabco they had to divest their stake in Brakes India to meet Competition Commission requirements as both companies were in similar biz

Latest move from Brakes India is about getting into electronics and software side of braking - controls and systems. Required for advanced systems like ECS (Electronic Stablity Control). They have partnered with Japanese leader ADVICS (Advanced Intelligent Chassis Systems). They are Toyota subsidiary. This will immediately open up Toyota and High end Maruti market for them. As safety norms become stricter all cars will eventually need to have advanced braking.

They are also developing new products and setting up north america presences (required for tax efficient exports to US)

Thank you very much for creating this thread. I always looked for SFHL thread in value picker. I am also a shareholder of it.

I am also on the firm believer of Brakes India doing well in future also, however real value unlocking will only happen if Brakes India gets listed in Bourses. Don’t see any articles regarding this to happen by management. The other significant investment is in Turbo Energy Company, which is also unlisted. Its listing also not sure. Turbo Energy is currently testing what opportunities they can have in the EV landscape.

The major listed companies include Wheels India Limited, IMPAL which dont have significant market cap and also in terms growth and profitability these 2 companies dont score high.

Other small investments in listed companies are in TVS Holdings(Parent Company of TVS motors) and Sundaram Clayton are good in future growth and profitability margin.

I believe the company has good fundamentals and can create wealth for investors. And listing of Brakes India, Turbo Energy or Axles India ltd can make the real difference.

They will slowly sell TVS Holdings and Sundaram Clayton and invest in current holdings or new biz. It is more like cash sitting on books. As those companies have gone to Srinivasan.

TSF group key businesses are

Sundaram FInance

Auto ancillaries -

Held partially through SFHL and partially directly. SFHL remains the driver holding company for this biz. They issued right share to increase holding in Brakes India when ZF had to exit. This gives me confidence that this is best auto ancillary play in India.

Brakes India is huge with billion dollar revenue.

Turbo energy is a JV with BorgWarner @babu44b Where did you get info about their EV plans. My understanding is that BorgWarner is pursuing that on their own. But this business is still in growth mode in India.

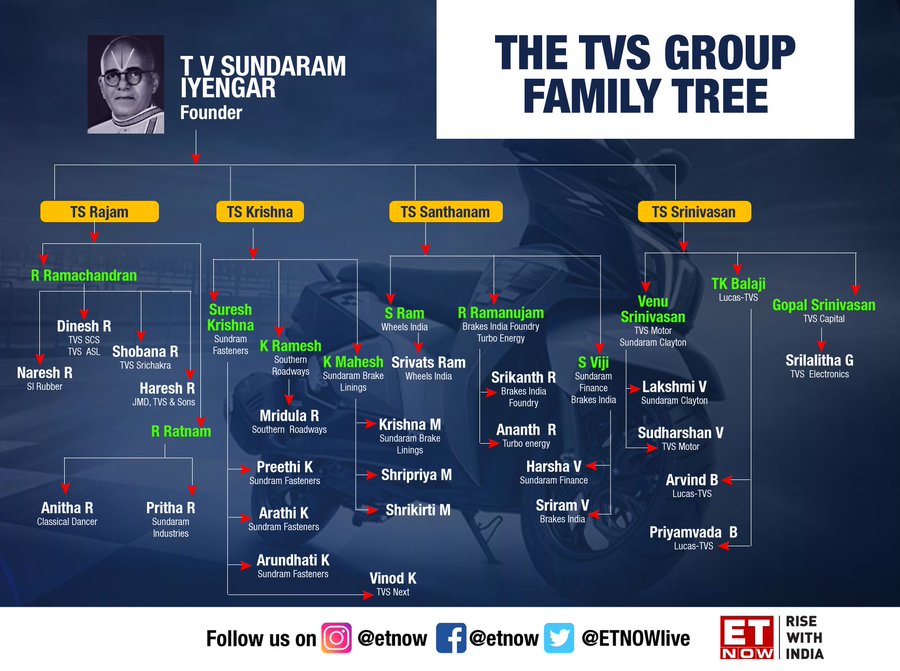

This pic gives out which family group controls what. Some amount of cross holding still exists.

It is mentioned in the rating report by Crisil. Quoting the same.

“TEPL is in the primitive stages of researching E-compressors and Electronic Braking which will be used in EVs. The amount spent on the R&D are expenses as revenue expenditure as technical feasibility has not been achieved. Evolution of EVs, and ability to introduce new products, including for EVs will be a key monitorable for TEPL.”

Please refer the below link for the Report.it is of Jul 2023.

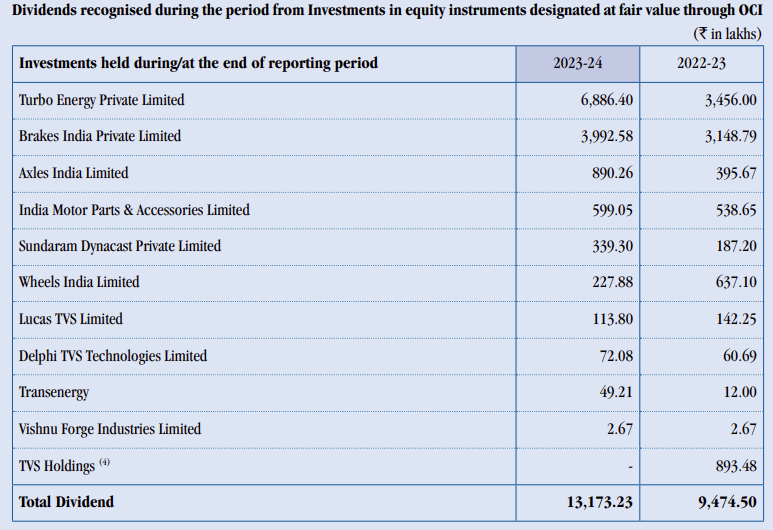

Niva Buppa IPO is coming. SFHL is invested in promoter investor Fettle Tone LLP to tune of 87 cr. Found following note “Investment is made for the specific purpose of reinvesting in Nivabupa Health Insurance Company Limited as per the agreement

entered into with Fettle Tone LLP”

This should see some value unlocking depending on agreement.

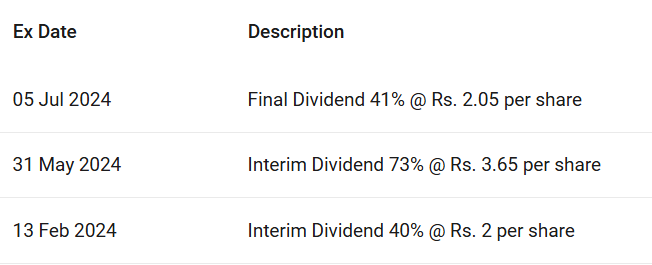

Being a holding company it is bit complex as dividends will fluctuate a lot depending on biz needs and performance of each company.

Best is to value each company based on its profit/revenue as provided in Annual report. I had adopted same in first message of the thread. That gave me idea of tremendous undervaluation.

As dividend was minuscule after covid as profits were down for each company and they were conserving cash to get back on feet.

Thank you for pointing this information. I have couple of points to add here.

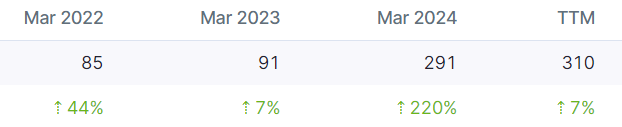

The below screenshot is from the Annual report and I can see that the valuation of investments in last year was 102 crore but it has decreased to 87 crore this year. not sure whether the investment amount was sold or valuation of investment decreased.

Agree amount is small for any meaningful value unlocking.

But as mentioned earlier. This is not a core holding. This is part of strategy that they can make opportunistic bets outside core holding upto 10%. So they are likely to rotate this amount. More like venture funding.

The Board of Directors have, at their meeting held today, declared an Interim Dividend of ₹3.70/- per share (74%) for the financial year 2024-25 on the paid-up capital of ₹111.05 cr, for Feb 2025.

If we see last year trend total dividend declared was 7.7 and in For Feb 2024 it was ₹ 2 /- Per share. Which is increased to ₹3.70/- per share for Feb 2025. So we can expect the dividend pay out per share this year will be more compared to last year.

If Associate companies keep up the good performance, so SFHL can get the dividend (Even if no listing for Brakes India, Turbo Energy or Axles India ltd ) the company can be a good dividend play for its investors.

Disclaimer : Investor in SFHL , views can be biased. Not a buy, sell recommendation

Best part is the fact that largest company in group Brakes India has no presence in USA. So there is nothing to loose for them from tariff tantrum. Infact, it may provide them an opportunity due to supply chain rejig.