Notes on Sun Pharma based on latest investor ppt -

No 1 pharma company in India

No 9 in US generics mkt

World ranking in generic pharma- 4th ( behind Mylan, Teva and Novartis. Aurobindo,Lupin and Cipla are ranked -7,8,9 )

43 mfg plants across the world

Present in 100 countries across generic and branded mkts

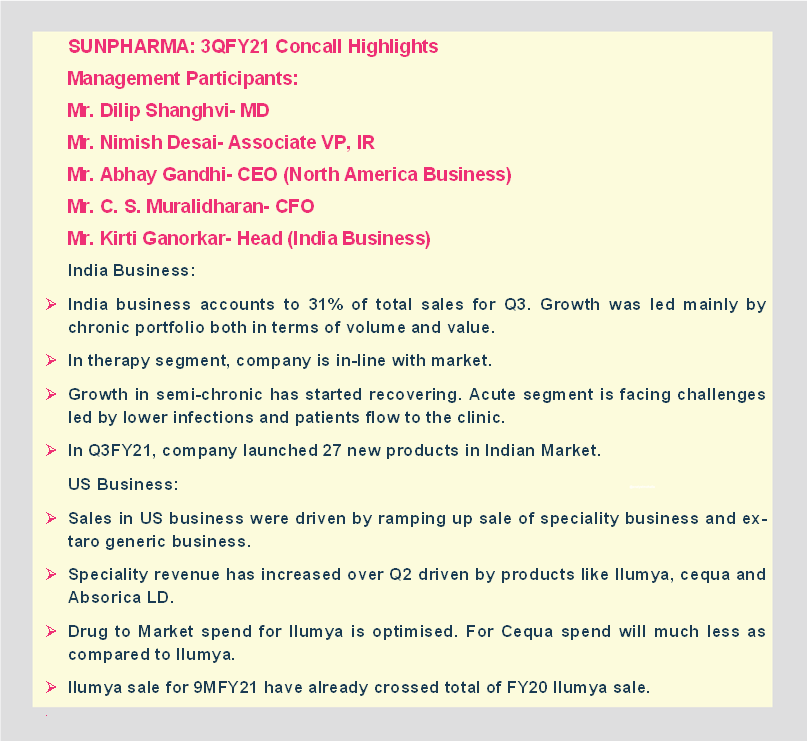

US business ( 33 pc of sales ) -

9th in US generics mkt, 2nd in dermatology

Present in generics, branded and OTC

US sales for FY 19-20- Rs 10500 cr

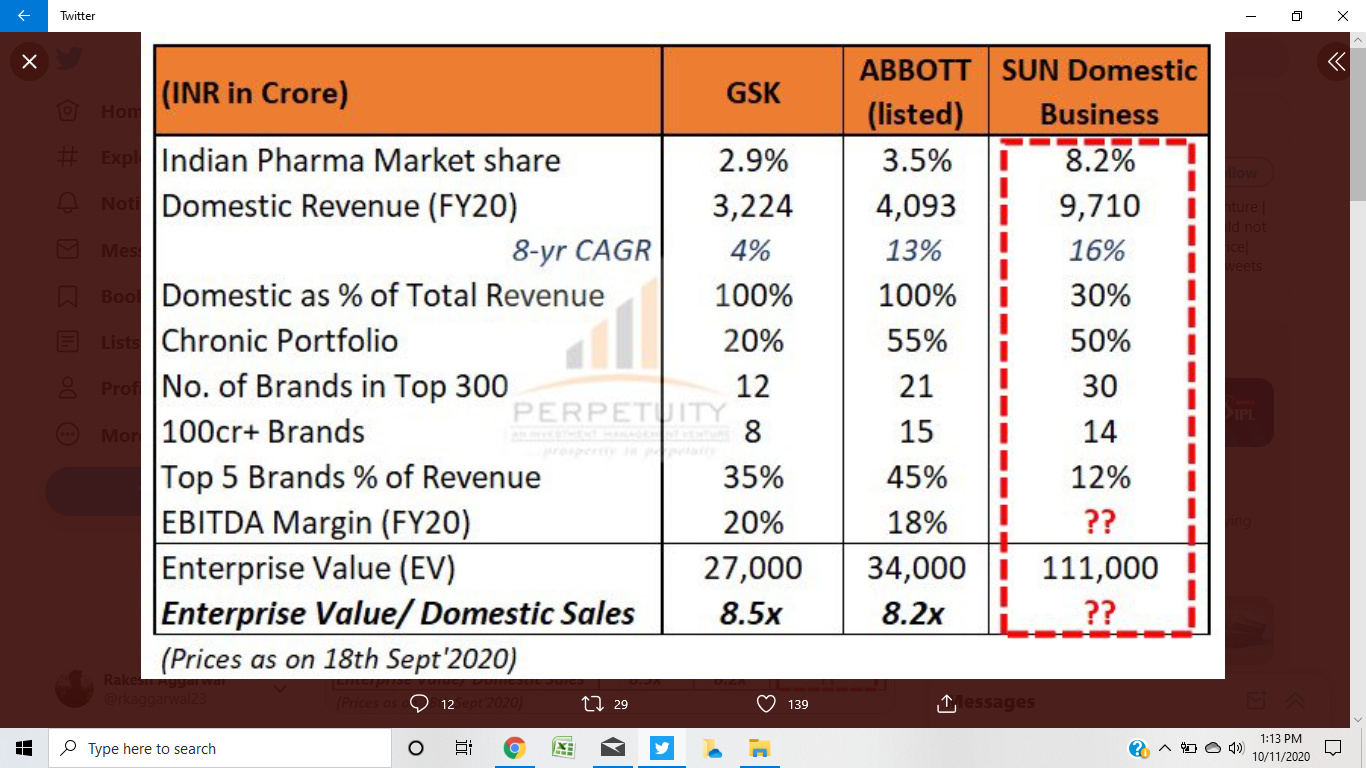

India business ( 30 pc of sales ) -

Overall rank- 1 ( mkt share at 8.2 pc ), Cipla and Lupin are ranked 3 and 5

Mkt leader in Chronic segment, strong postn in acute segment

31 brands among top 300 brands

FY 19-20 sales at Rs 9700 cr

Leadership postn among the following Doctor Categories - Psychiatrists, Neurologists, Cardiologists, Orthopaedics, Gastroenterologists, Nephrologists, Diabetologists, Dermatologists,Urologists, ENT and Consulting Physicians

MR field force- 9700

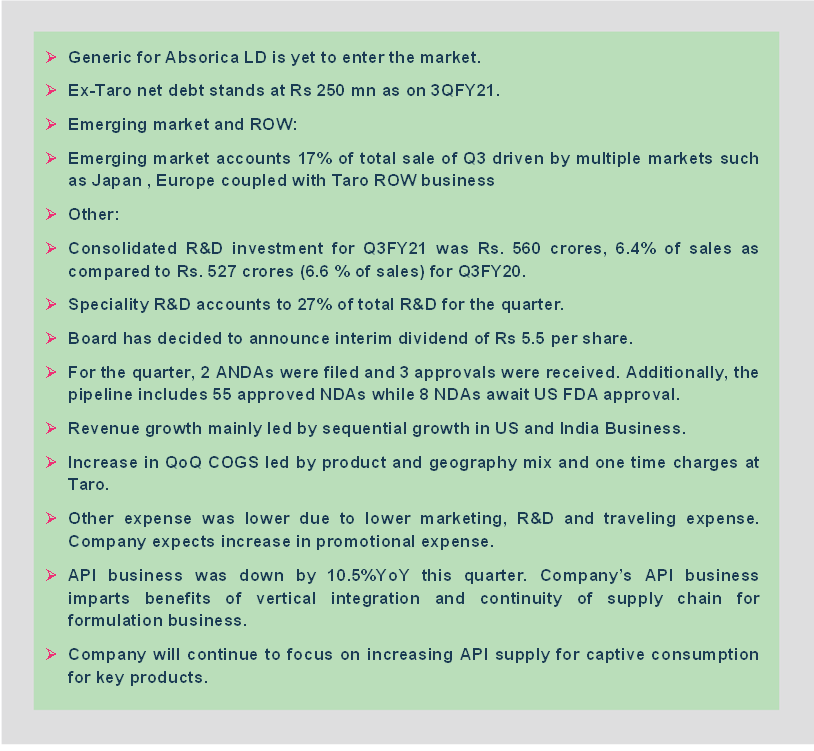

Emerging Mkts ( 17 pc of sales ) -

Present in 80 countries

Focus mkts- Romania, Russia, SA, Brazil, Mexico

Local manufacturing across 07 EM countries

MRs - 2300

Other Developed Mkts ( 14 pc of sales ) -

Include- Aus, NZL, Canada, Japan, Western Europe

Focusing on development of complex generics and other differentiated products

Local mfg at- Canada, Japan, Aus, Israel and Hungary

India and Intl Consumer healthcare -

Brands like- Volini, Revital, Pepfiz, Abzorb etc in India

Also present in - Romania,Russia, SA,Ukraine, Nigeria,Myanmar, Poland, Thailand,Morroco,UAE,Oman - wrt consumer heathcare products

Enjoy strong brand equity in 4 countries ( India, Myanmar, Nigeria and Romania )

Dedicated field force in each Mkt

APIs ( 6 pc of sales ) -

Make 300 APIs

Provide backward integration

Aprox 20 APIs scaled up annually

14 API manufacturing facilities

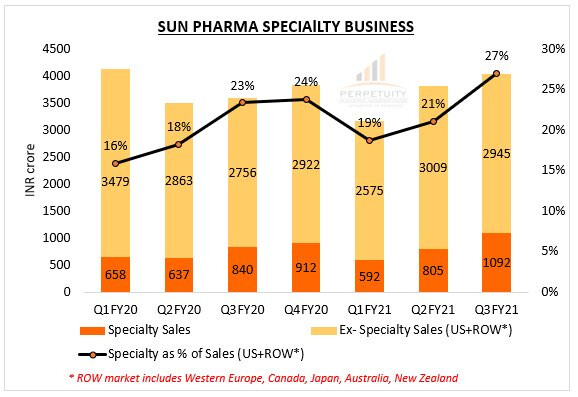

SPECIALTY PORTFOLIO -

ILumya - for plaque psoriasis , launced in US in 2018, Europe and Aus - Dec 18, Outlicensed for Greater China, Japan approval in Jun 2020

Cequa - for dry eye disease, US launch in Oct 19, Outlicensed for greater China Mkt

Absorica- for severe recalcitrant nodular acne, currently being sold in US

Levulan - for actinic keratosis, currently being sold in US

Odomzo - for LABCC, being sold in US,Germany, France, Switzerland, Denmark, Aus, Israel

Yonsa - used in prostate cancer, sold in US

Bromsite - used after catract surgery to relieve pain and inflammation, sold in US

Xelpros - used in ocular hypertension, sold in US

Infugem - a chemotherapy product, being sold in us and Europe

Key deals -

Acquired POLA Pharma in Japan in 2018 , access to Japanese derma mkt

Acquired Global rights for Cequa and Odomzo in 2016

Acquired Biosintez in Russia for local mfg footprint in 2016

Acquired 14 brand from Novartis in Japan in 2016

Acquired Insite Vision in US in 2015, strengthens opthal portfolio

2015 - merged Ranbaxy with itself

2012 - acquired Dusa pharma in US in 2012, got sterile injectable mfg capability in US

2010 - Acquired Taro Pharma ( Israel ) , access to US derma mkt

1997- Acquired Caraco entry in US mkt

Disc: invested drom Rs 480 levels

.The journey over the years and the organisation as a whole.

.The journey over the years and the organisation as a whole.