Missed targets by marginally , let us see what management had to say

3 Likes

I think this is surprising result (Lower than expected). In Q1 they had shown so much of promise but Q2 FY22 over Q2FY21 is flat in terms of revenue. I agree that we will get more details in the Investor call

Key Takeaways

- Domestic Sales are Flat mainly due to impact of less rain fall

- Animal Nutrition and Export sales are very strong

- No constraints on raw material availability until December 2022

- 5 New Product Launches (100 crore capex)

- 1 New product coming this year and rest five will be launched in FY23 (All of these are parent molecules and shipped to customers of parent )

- Pricing increase is passed on to products that are being exported

- Domestic price increase is little challenging due to high availability of the stock in the market (Failure of Kharif season - less rain fall contributed to the less uptake of the stock in the market )

- Agro Delivery Systems (Delivery of pesticides - drones ) , unique application systems (Acquisition could be in those areas , We would like to look at the entire Agro system and look for opportunities )

- Three out of 6 new product launches are bio stimulants

- Margins on the products that are sold to sumitomo parent (pricing is at arms length )

- For example, pricing to a parent affiliates in brazil, parent didn’t interfere at all , so we decide on the pricing

- In excess of 700 crores on books will use it on need basis and further expansions

Very Interesting observation is they are saying their next acquistion could be in agro chemical delivery systems .

Future looks promising, this is one of those boring slow and consistent compounders for long term investing.

7 Likes

I had listened to this with amusement, even a bit of skepticism frankly. But came across this today:

b4713847-3f7d-4889-b95f-ba2907788152.pdf (bseindia.com)

Dhanuka has already made this type of acquisition.

2 Likes

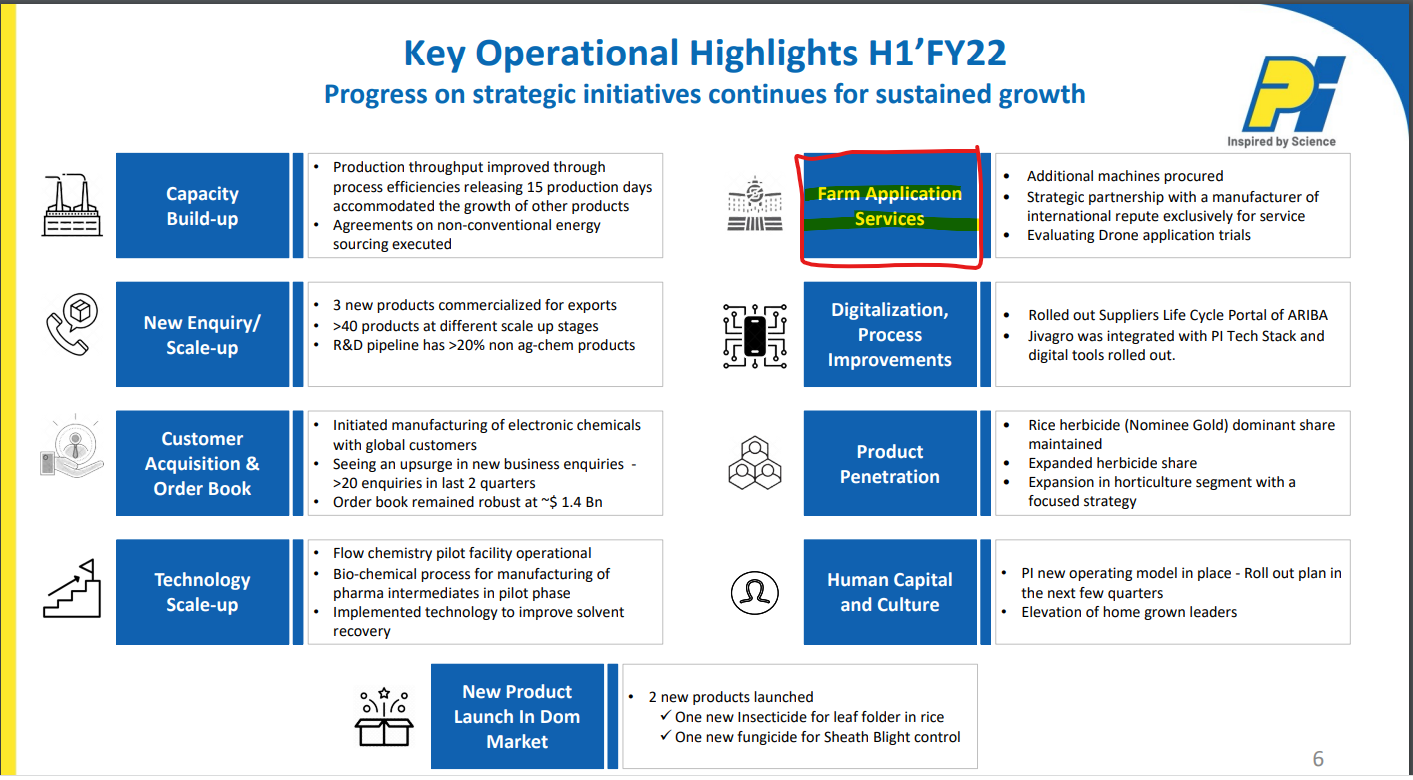

@Chandragupta thanks for spotting that . Here is another development by PI as well from Q2FY22 Investor Presentation Page 7

3 Likes

Yes indeed. This seems to be the new trend in the industry. I had heard that a lot of start-ups are working in this field, and their efforts now seem to be coming to fruition. What’s notable is that drones here are conceptualized much more than just a mode of transport to move materials. Recently field trials to spray nano urea using drones were successfully carried out in Bhavnagar and widely reported in the press. ( click here)

Even PI uses the term Farm Application Services in the above slide. If the idea scales up successfully, this could add a completely new dimension to the existing business model of Ag Chem companies in the long term.

4 Likes

CCFI defends 17 of the 27 molecules proposed to be banned. Glyphosate is not in this list. Does this mean it will be banned? Dr. Rajendran Committee to take a final call “by early December”, says this report:

3 Likes

@Chandragupta here is the response

Question 1 : If this ban is implemented, how much percentage of domestic sales will be impacted ?

- There is no proposal from the Indian authorities to ban Glyphosate; Accordingly, this molecule is not in the list of products to be defended by CCFI as referred to by you.

- The proposal under consideration with the Indian authorities is regarding use of Glyphosate only through ‘pest control operators’.

- We and various other stakeholders who would be impacted by this proposal have submitted their objections to the Indian authorities with data and scientific studies and implementation possibility in view of lack of PCO infrastructure in rural India.

- We continue to be hopeful that the Indian authorities will take a considerate and logical decision in this matter based on scientific information.

Question 2 : From the banned list of 27 molecules, what is the % sale of each of the molecules of our company ?

- As we have mentioned in the past, even if such proposal was to be implemented, it should not have material adverse impact on the Company.

- We are selling only 3 of the products in the Indian market from the aforesaid draft list of 27 products.

- We have submitted our objections to the Indian authorities and provided detailed scientific explanation and data to defend these products.

- Various other stakeholders having impact from this proposal have also submitted objections to the Indian authorities for various products.

- We continue to be hopeful that the Indian authorities will take a considerate and logical decision in this matter based on scientific information.

Question 3 : What is the total % of dependency on China for Raw Materials and Finished products (traded products) ?

- As we have mentioned in the past, currently roughly about one third of total purchases of all input materials is sourced from China.

6 Likes

Thanks for the clarification!

China dependency seems to be on the higher side, not sure if there is any roadmap to reduce it or they plan to continue as it is.

Hi, Can someone help with - How many technical grade/formulation of Sumitomo comes under Red-triangle

Here is the response from them

Currently, roughly about one third of total purchase of all input materials is sourced from China. We believe this is not an alarming level and is lower as compared to the overall industry level in India.

While we are working on several initiatives to source higher proportion locally in India or undertake backward integration, it may be difficult to significantly reduce proportion of procurement from China in the short-term, keeping in mind various factors.

2 Likes

4 Likes

Tracking the valuations consistently and apparently premium valuation is provided by the market. Do you believe it’s far stretched or it’s relying on the hope that parent company might provide some future growth triggers which makes it reasonable?

Also, can anyone please explain various growth triggers for SCIL as there’s not much coverage available on the internet recently?

Also, which are the direct competitors of SCIL in India?

1 Like

Q4FY22

Results

Investor Presentation

Concall Transcript

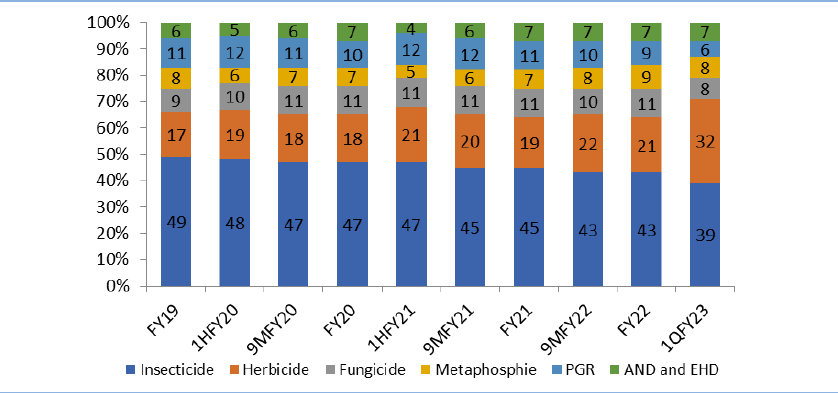

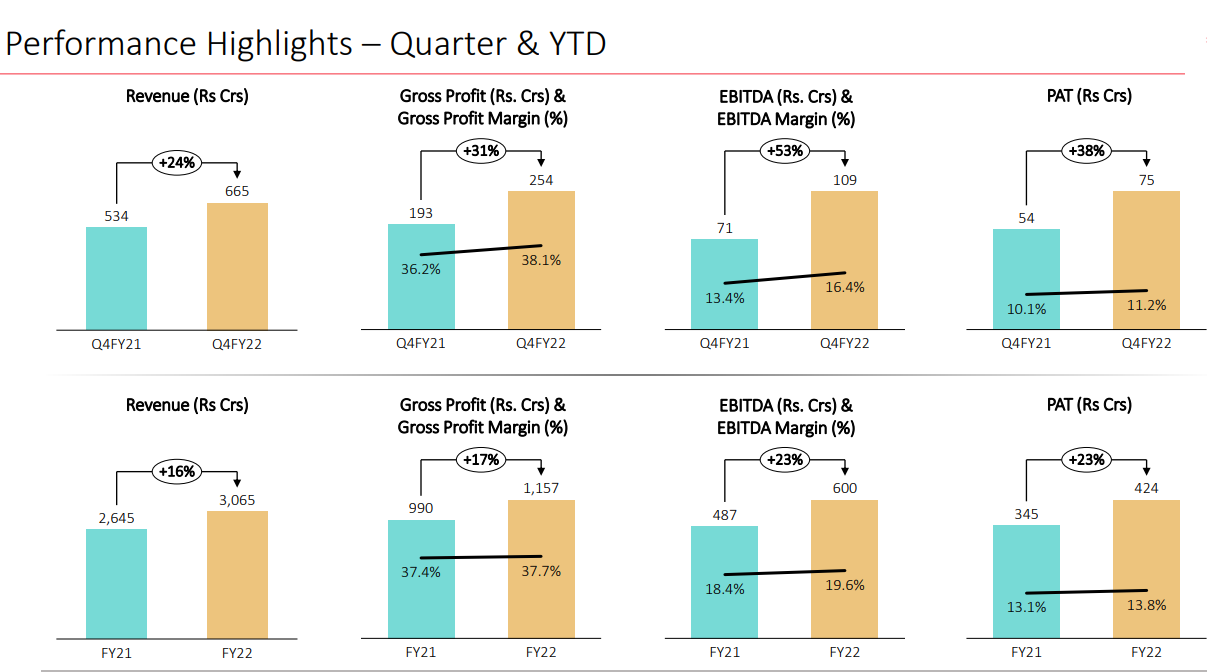

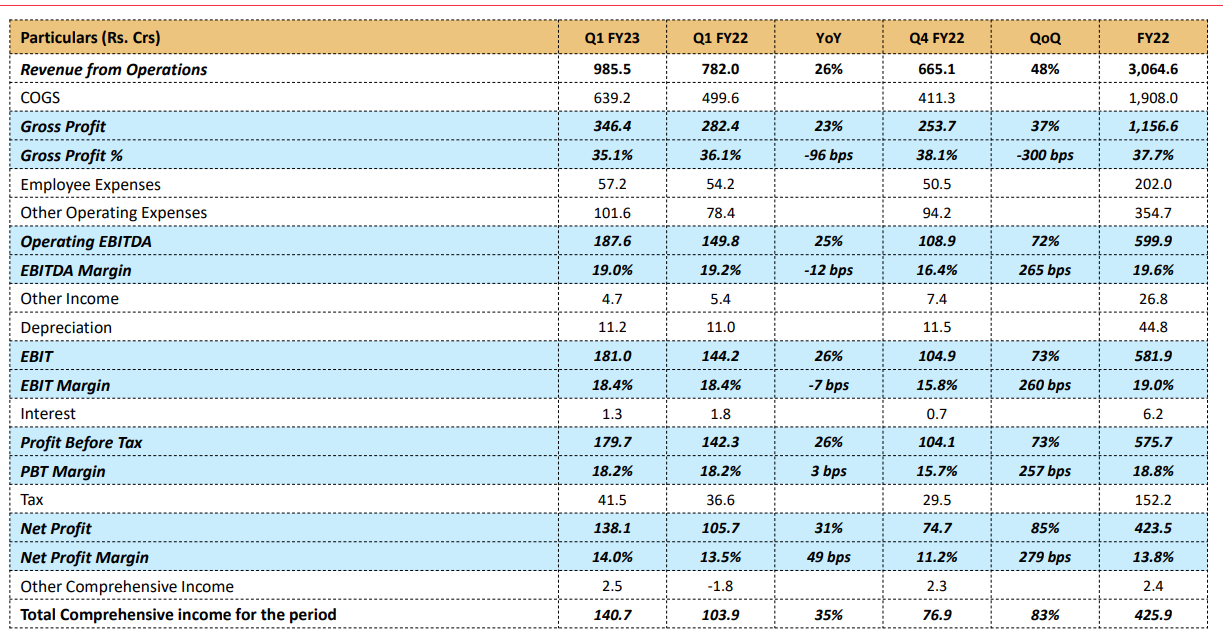

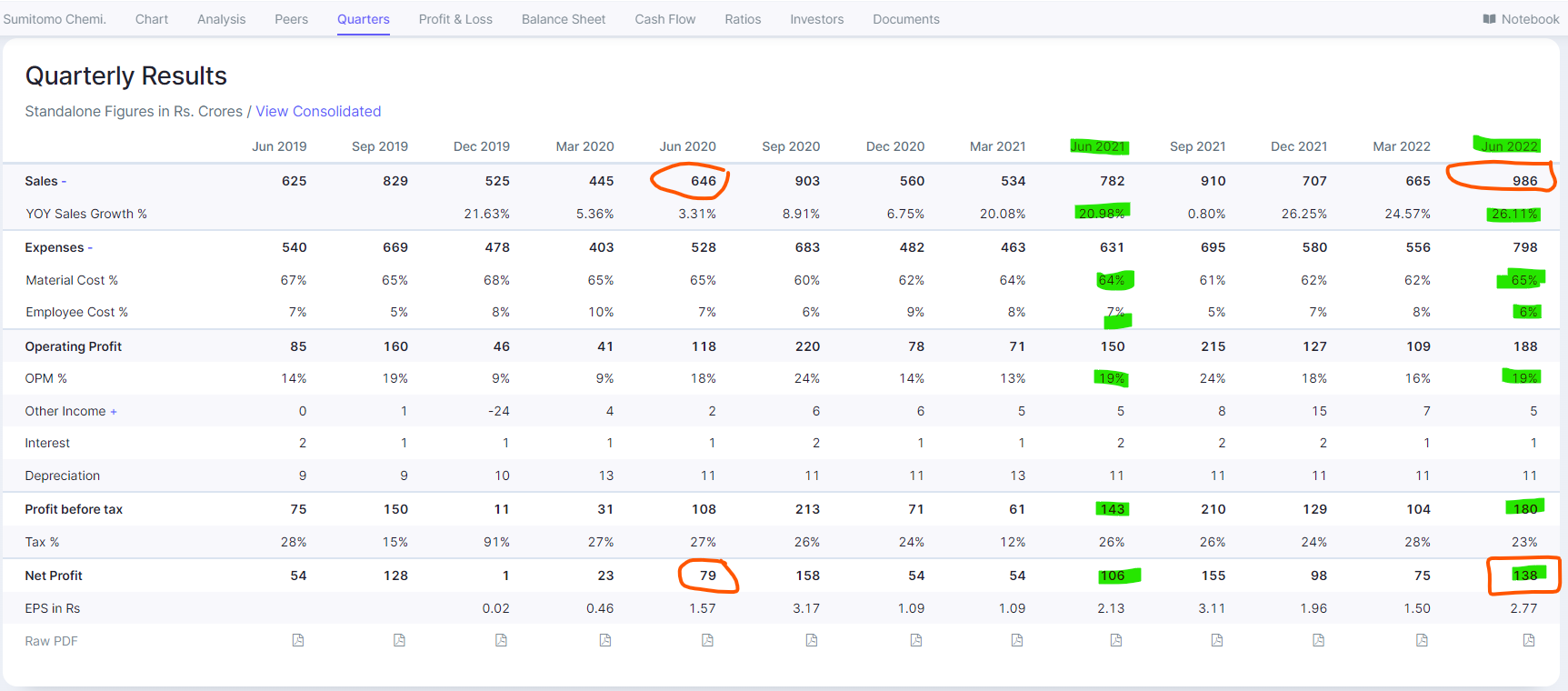

- Revenues grown by 16% , EBIDTA gown by 23% (Margins at 19.6% vs 18.4%) , PAT gown by 23%

- Touched landmark revenue of 3,000 crores (3064 cr)

- Increase in inventory days due to more stocking to offset price increase in RM

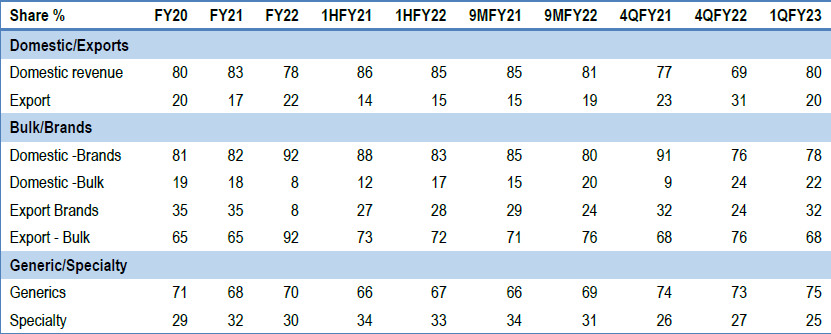

- Exports increased by 5% YOY (17% to 22 % - This was on account of increased shipments to our affiliate companies, especially in Latin America )

- 200 brands across complete agrochemical value chain with more than 20 mega brands with high brand recall value.

- Domestic and export margins are same

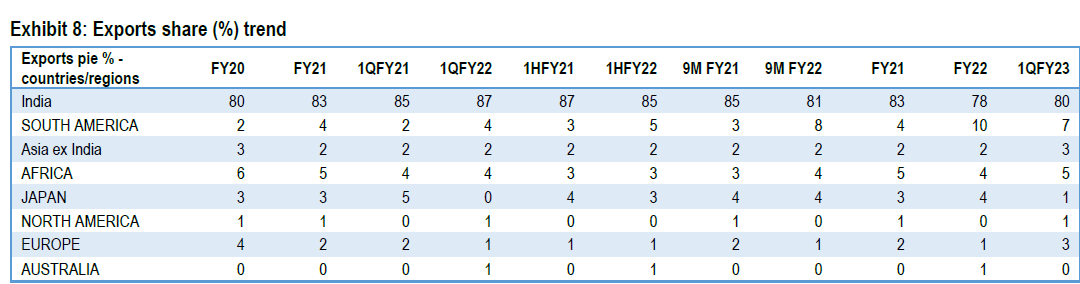

- LATM markets very competitive and price sensitive , registrations take anywhere between 3-5 years in LATM (this can be reduced based on the data package we have to submit)

- More focus on high growth profitable segments like PGR (Plant Growth Regulators), Bio Rational Products

- Recently added segments showing growth - Animal Nutrition and Household Insecticides

- When the opportunity comes then we might carve into other segments (that of parent ) IT Chemicals and Pharma chemicals

- Even in such challenging conditions they are managed to pass on the RM costs that helped them to improve their gross margins (this FY prices are increased twice both in domestic and exports, strong brand pull helped to pass on these increases )

- Improvement in Receivable days (to offset high inventory days - this increase in inventory days is by design )

- In U.S. market, we have got registration for aluminum phosphide (due to technical error we have asked for correction, this is 100 tonnes a year opportunity)

- Chlorpyriphos registration in Latin America came through (new capacity at Dahej will full fill this requirement)

- Aluminum phosphide registration in Latin America came through and started the shipments

- Doubled Tebuconazole capacity - demand is robust domestic and export market

- China + 1 is not as big as one thinks, we can expect max of 5% shift that in itself is a big size

- No herbicides in European market but only fungicides

- Formed a task force to explore Europe markets for existing biological product registration in Europe - Registrations take two to three years

- Parent has given free hand to explore and take new opportunities elsewhere but the primary focus will be to capitalise on parent molecules

- Herbicide contributing roughly 21% , herbicide growth was roughly 28% for this fiscal, that is mainly because of the higher glyphosate prices

- The fungicide grew by 16-odd percent

Forward Looking Statement / Key Takeaway

Glyphosate is likely to grow. Bayer is expected to register the GMO cotton.(We don’t know the time frame, it may take two years, three years), this is likely to increase the overall volume. Once cotton comes probably, corn would also come, corn would also follow cotton probably a couple of years down the road.

Disc: Invested

10 Likes

1 Like

Q1FY22 Results

Investor Presentation

Few points from Investor Presentation

- 1 insecticide, 1 metal phosphide and 2 PGR products launched during Q1FY23

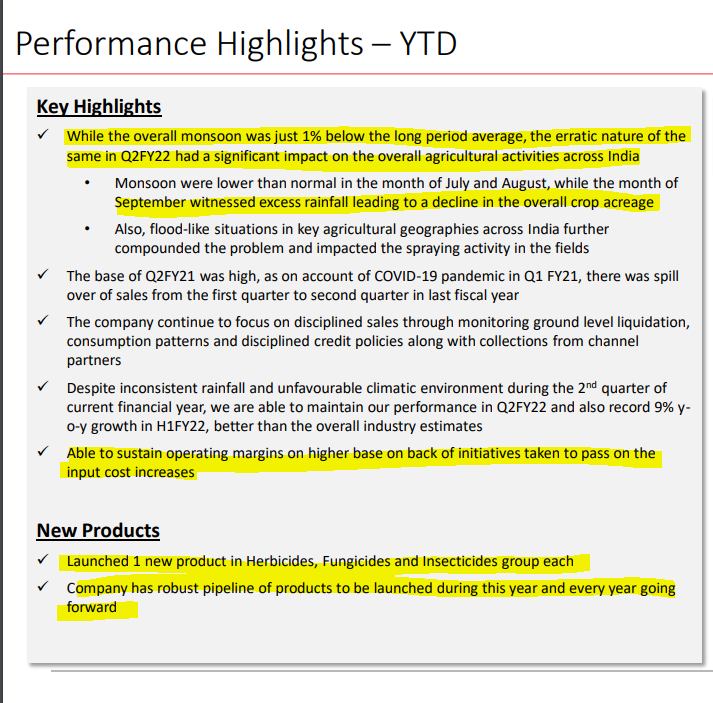

- The slow start of the monsoon delayed sowing by 15 to 20 days. Monsoons have accelerated,

with cumulative rainfall 20% above normal till July 31, ‘22 - While East and Northeast regions received 21% surplus rainfall, North-West India, Central India,

Southern peninsula received deficient rainfall till the week ending July 1, ‘22 (June rainfall in rice-growing states was scant, though it picked up later) - Lower-than-expected rainfall in June’22 slowed placements and caused sales to spill over from

Q1FY23 to Q2FY23 - Delayed monsoon led to lower acreage across states, down 5% y-o-y as of July 1, ‘22 with higher

negative impact for some of the crops

As the monsoons intensified in July, sowing activity increased, significantly narrowing the

acreage deficit - As a precaution against missing out on potential liquidation opportunities in Q2, we have

stocked up our inventory -

There has been an uptick in exports, and recent capacity expansion investments should help

sustain this encouraging trend

@Chandragupta please share your views.

3 Likes

Results look quite strong, which is what the market has come to expect from the company. I guess exports to US / LATAM and Europe must be growing neatly, a lot of growth is coming from there. In domestic, company has been able to pass on RM cost increases well, so there is no major compression in overall margins. Need to watch the working capital however. Also progress in animal nutrition and environment health business – how they are growing. I don’t find the presentation and concall details on the website however, waiting for it.

5 Likes

Buy Sumitomo Chemicals; target of Rs 565: ICICI Direct Aug 14 2022

Sumitomo.pdf (538.9 KB)