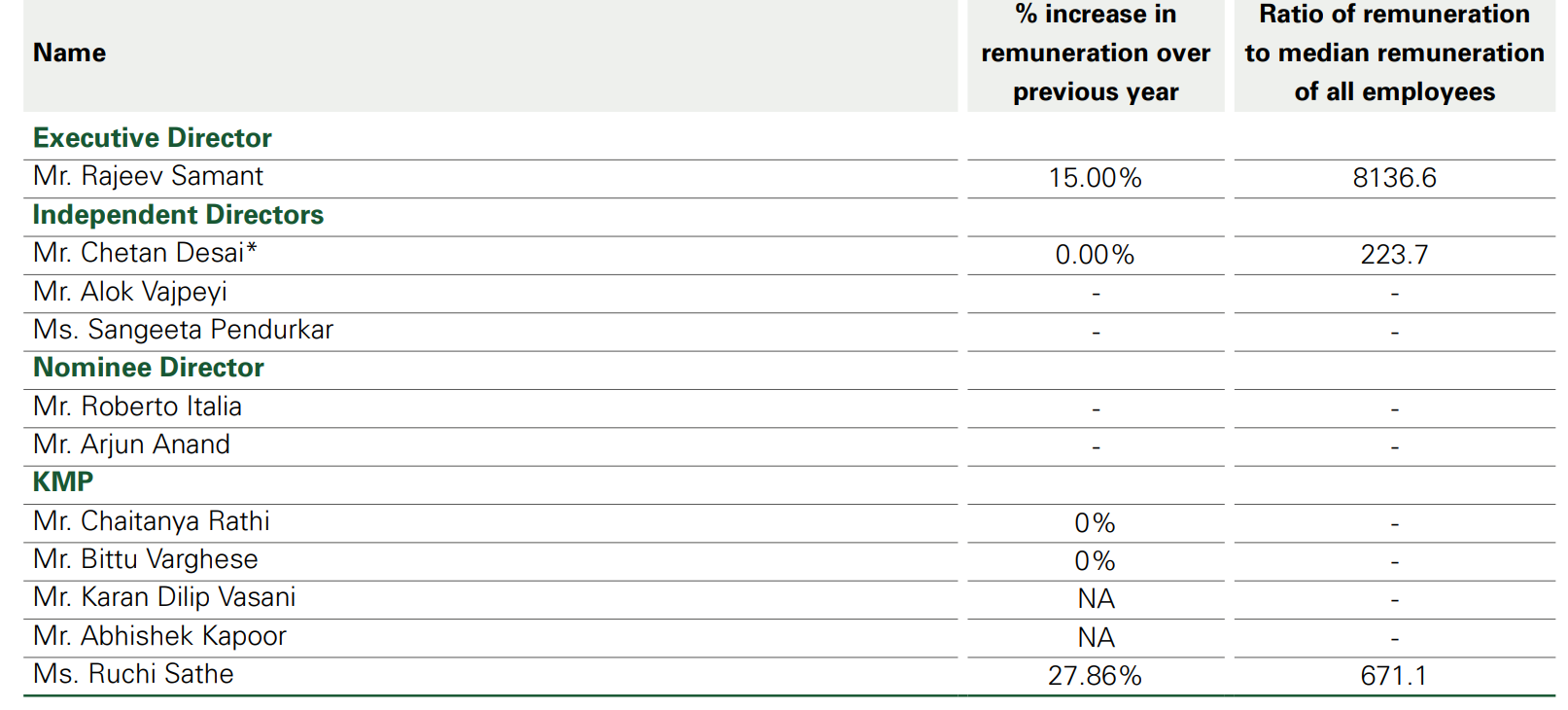

Is a median remuneration of Sanjeev considered normal or high

Why is the Sanjeev Receiving such a high median remuneration of 8136.6 time to median remuneration of all employees

Is a median remuneration of Sanjeev considered normal or high

8Cr+ you mean above ? if yes it is very high

IMO It doesn’t look like 8Cr. It’s a ratio which means it could be 8100 times median salary.

It literally states “Ratio of …” in the vertical column, it means the Executive Director is getting paid the salary of 8136 workers

Rajeev Samant has been continuously diluting his stake in the company, though in small instalments, but it really makes me a little nervous about the skin in the game. Is he indicating that the price has already reached the valuation which will not improve anytime soon and hence he is smartly diluting his stake? The Q4 results were a little soft as well and the company being the hyped “new drink category creator”, “pioneer of wine” “premiumisation of Indian drinking community” etc, how do you see the below 25% stake of the show runner?

Anubhav,

The promoter’s dilution is Institution’s accumulation which perhaps testifies the faith in the company and the category. I’m worried of the increase in number of shareholders (2,10,000). If some point in time stock starts appreciating in non linear manner, it may increase to 400,000 or may be more. In such case the future return may suppress since Public sharholding is still more than Promoter and the Institutions.

Disc- Not invested but closely watching.

I am ultimately saying a similar thing as Institutions may not absorb the promoter selling beyond a point and retail are obviously following the herd mentality if the company is hyped in the media. Verlinvest has already sold out. DIIs are putting in money fueled by burgeoning monthly SIPs which makes them put in money where they can and hence I am not reading much into DIIs increased holding. If and when, the monthly SIPs decline, it will be an interesting scenario for me to see how DIIs cut stake in the narrative driven stocks.

Verlinvest was a Private Equity which needs exit and IPO is exactly done for that. Moreover Sula is selling an aspiration, dream and experience and this will always command a premium.

Apart from Verlinvest, as in the image others have only increased while the share price was falling.

It depends on how you look at it, a alcoholic beveraage or a hospitality company. Moreover their business is all about strong value chain and distribution.

IMO, it may not give returns in the near term and consolidate longer but it has margin of safety much like Sona BLW.

Good luck and Happy Investing

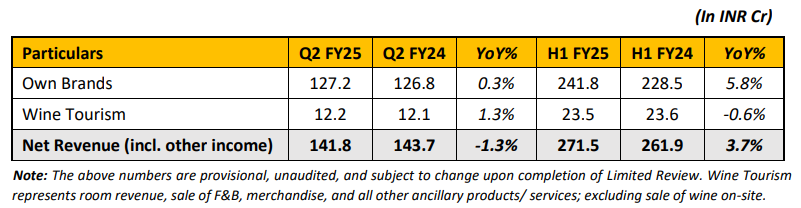

Net revenue: 10% ![]() YoY (Rs. 129.7 Cr)

YoY (Rs. 129.7 Cr)

EBITDA: 10.3% ![]() YoY (Rs. 35.2 Cr)

YoY (Rs. 35.2 Cr)

EBITDA margin: steady at 27.2%

Elite & Premium: 8.6% QoQ ![]() (Rs. 81.36 Cr)

(Rs. 81.36 Cr)

Economy & Popular: 24% QoQ ![]() (Rs. 33.2 Cr)

(Rs. 33.2 Cr)

Revenue: 2.3% ![]() YoY (Rs. 11.3 Cr)

YoY (Rs. 11.3 Cr)

Milestone cellars - New tasting room and restaurant near Nasik airport.

Have planned expansion of wine tourism facilities at Domaine Sula near Bangalore

New resort coming up next year next to the York winery in Nashik - this will expand room capacity by 30% and also add conference facilities.

The wine tourism business had declined because of some headwinds and that in turn impacted the sale of elite & premium wines. Majority of elite wines has a much higher proportion of sale (D2C) at wine tourism than any other category.

The headwinds include the following:

This was a pause on the premiumization phase. But regardless, the focus on the premiumization shall continue as mentioned by the management.

Have decided to shift to a third-party sales model for the economy and popular brands in Maharashtra. This would enable the internal sales team to focus on the elite and premium categories. This strategy has has shown promising early results in Maharashtra. In fact, this strategy was earlier adopted in Karnataka and Telangana, and had yielded good results, hence confident of the strategy.

Why the promoter share holding is very low in this company. Even though they are makeing huge capex and good branding

This is also my concern as an existing shareholder. Why is the promoter regularly selling. A stake at around 25% does not inspire confidence.

I checked few restaurants in Pune and found that they don’t serve Sula wines at all. Most of them serve Fratelli wines. Has anyone of you did some check on the restaurants in your vicinity? Is Fratelli more popular than Sula?

If someone has any insights into this kindly share. Much appreciated!

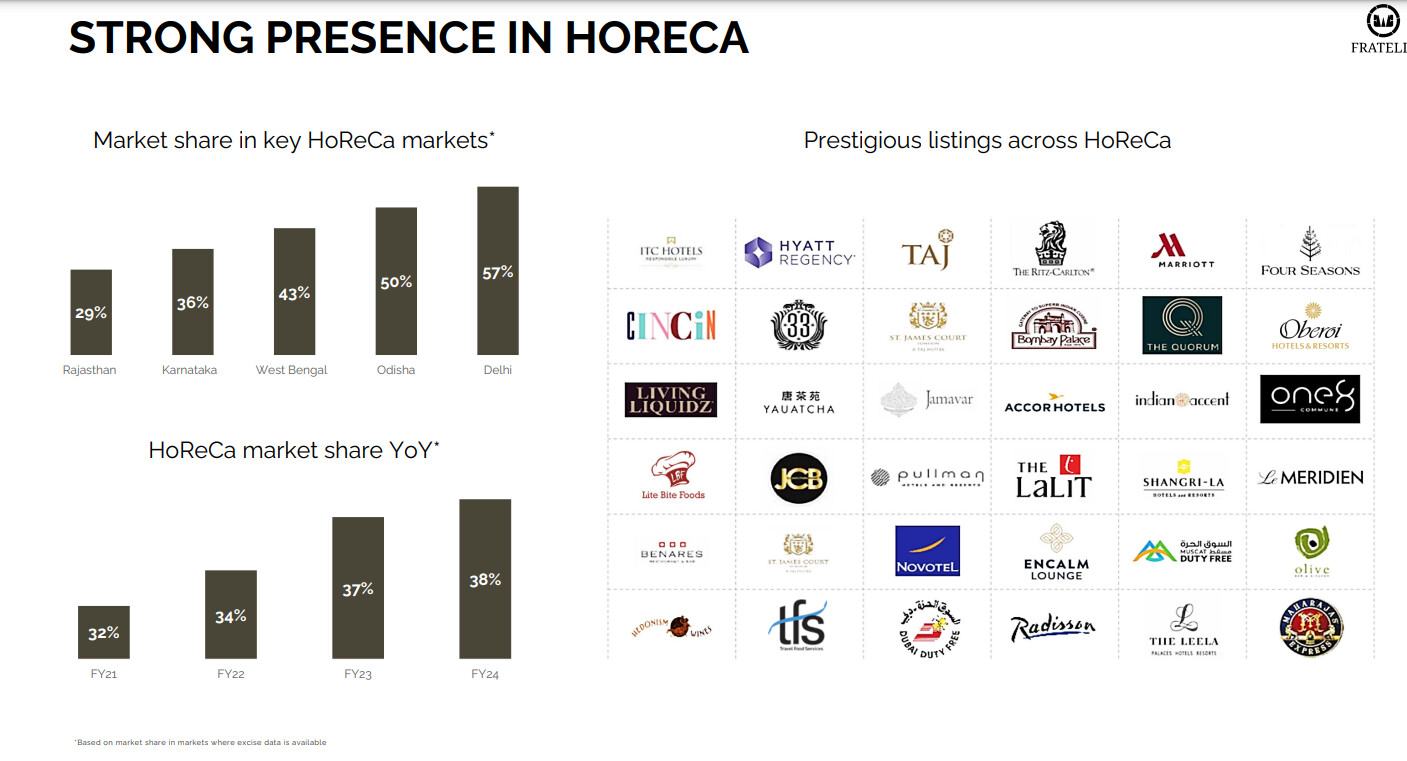

This is absolutely correct. Fratelli holds a very significant market share in HORECA business. Sula wines seems to be the market leader only in B2C and wine tourism.

There is a dedicated topic for Fratelli Vineyards, think this would be more relevant there.

Why Sula has less HORECA market share compared to Fratelli?

As far as I understand this is because of the original business of trading was run in the name “Tinna Trades”. Tinna trades later acquired Fratelli wines. Their trading business gave them an edge over other wine brands because of already established distribution network.

Personally I have seen Sula wine being displayed in Goan restaurants.