Manishji: Yes…sugar is a cyclical sector…but the upcycle in sugar sector lasts for around two years…the full impact of the impending fall in sugar production will be felt in the next summer season…with increasing global demand and a La Nina condition (which causes drought I brazil) it will be difficult even too import sugar in next summer…that’s the time of maximum investor frenzy in sugar stocks …that’s the time to look out for technical signs of topping out formation in sugar stocks…BOTH AT THE BOTTOM AND AT THE TOP…SUGAR INVESTING IS A GAME OF TECHNICALS

9 Likes

Mehnazji:

You can’t expect the market to absorb fifty thousand shares of stock as easily as it does one hundred.

- Jesse Livermore

I am quoting these words of Jesse Livermore, just to give reason behind 4% drop is prices of Balrampur Chini on result. I wrote in the morning on MMB that irrespective of good or bad results, it is likely to see profit booking and it happened. Those who buy in bulk need to take out some cash from time to time. Chart of most of sugar companies have turned bullish in line with firming of sugar prices within country and at international level ICE Future No.11 has closed above 17 C/lb.

Fresh bull run is sugar sector is just in infancy stage. It has long way to go. With major shift from deficit to surplus, ICE future has bottomed out and coming out of consolidation phase. Looking to history, I would consider 16 to 18 C/lb is range where it can spend more time and break out from this range means take off from runway, journey full of excitement for any sugar stock you pick up.

Balrampur Chini is following classical higher top higher bottom pattern. And now around 108-109, it is at higher bottom, very safe entry point in a jet flight.

1 Like

As can be seen from the monthly chart of Balrampur chini, the stock is in a congestion zone…caught between strong resistance and a strong support. I do not think that it may come out of congestion zone in May…but in june it may break free with a lot of momentum. Investors may expect a long price bar for the month of June / July

1 Like

Today food minister has made a contradictory statement… firstly he said that govt may reduce the import duty on sugar if price rises and secondly he has said that cost of production for mills is 32-33 rupees and mills too should have some profit and that sugar price should be market determined.

Just a few days ago, the prime minister has assured his own party MPs from Maharashtra that import duty on sugar will not be reduced. When maharashtra is suffering from unprecedented back to back drought and farmers are in huge losses, any attempt to depress the price of sugar will be taken as downright anti farmer.

And then there is the elections in UP and a huge votebank of sugar farmers - who have voted for BJP in the parliamentary elections. If the actions of central govt cause distress to sugarcane farmers who were suffering since last five years…then BJP looses the UP elections.

Even the central govt knows that 80% of the sugar is bought by bulk / industrial buyers… and an individual family buys just 1-2 kgs of sugar in a month… so a 5-10 rupee rise in sugar prices does not pinch the consumers that much.

Its in our interest to try and disregard these kind of statements and focus solely on the price action…sugar prices are about to embark on next leg of the rally… in june huge ramazan demand coupled with existing summer demand for sugar will hit the sugar market…after ramazan comes the marriage season and then comes the festival season… very good demant till August end…

3 Likes

Venezuela is running out of sugar… Coke issued a red flag on potential shortage of sugar

A lot of African countries too are facing rising sugar prices…there is a huge demand for sugar from china, where due to abolition of subsidy farmers have shifted to other crops… the 1.5 milion tons of sugar that was exported from india is suspected to have been smuggled to china… there is less sugar in the second largest exporter - Thailand… sugar profuction has fallen in Indonesia and Phillipines…

2 Likes

All sugar stocks are trading down this week. Impact appears to be from the combination of excise subsidy withdrawl and import duty reduction but I’m still not convinced on the numbers. The retail price is still 33.5 - 34 as confirmed by Balrampur MD in con-call yesterday.

The crushing season is over so excise duty withdrawl will not factor in until Q3 and import duty reduction will still not match domestic prices on retail level. How do either of these news impact industry dynamics at the moment?

Even if they do impact it slightly, sugar companies like Balrampur are sitting on a produced cost of Rs. 27 per kg including depreciation. The guidance is pretty straightforward from here, or I am missing something?

Aashish: you have got the fundamentals of Balrampur chini correctly…but that does not mean that the stock will go up in a straight line…

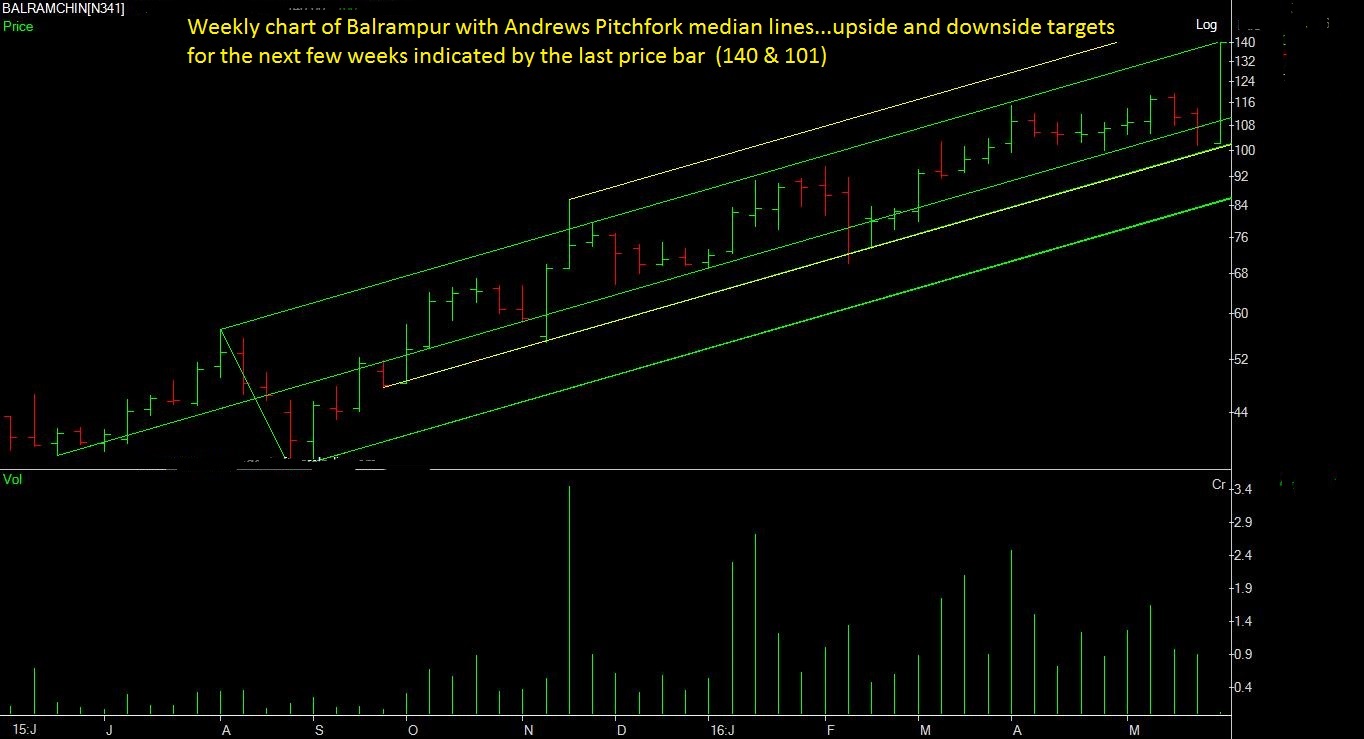

one of the rules of the median lines as per Andrews Pitchfork technique is that after touching a median line the stock will move towards the opposite median line. Balrampur chini is a textbook case of the movement of stock between median lines…I am posting the weekly chart of the Andrews pitchfork with the relevant median lines…the buying and selling points are quite obvious …

3 Likes

Hi Niraj,

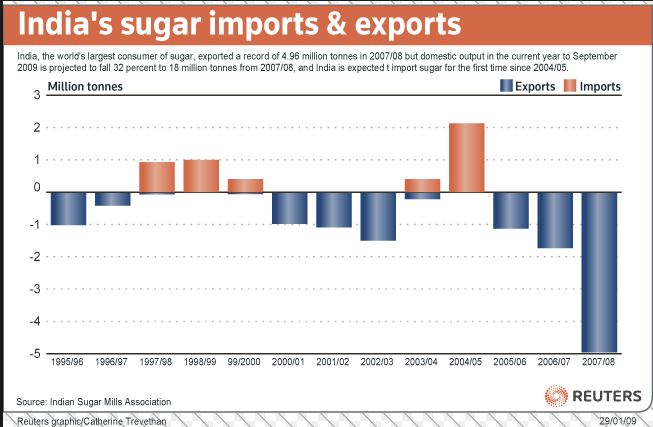

Banning of sugar exports will be counter productive because it is more remunerative for the mills to sell sugar locally than abroad. This is because the local realizations are much better than in international markets during an upturn. Btw, the government has now removed the export incentive which was in play since late last year. But this will not dent the sugar rally.

As mentioned by you, we will be net importers of sugar in the coming year. And that is the reason we are seeing this rally in sugar prices. Just have a look the following chart.

It clearly shows that sugar cycle turns when the possibility of imports looms.

Regards,

Roberto el S

1 Like

The Commodities Market Has A Sweet Tooth : By Wall Street Daily

Despite appearances that the entire commodities sector is continuing on a major downslide, one resource remains steadfast –sugar.

Sugar has been one of the best-performing commodities so far this year – largely driven by a global supply shortage, after wallowing in a five-year surplus.

Supply woes are pushing futures prices higher, while demand continues to increase on a global basis. In fact, the International Sugar Organization – along with most analysts – forecast global deficits through 2017.

According to the latest bi-annual report, issued May 19, 2016 by the United States Department of Agriculture (USDA), the world production for 2016-17 will be approximately 169 million metric tons (mmt), a figure revised down by 7.2 mmt.

Global sugar consumption is forecast at a record 174 mmt (raw value), exceeding production, and drawing stocks down to the lowest level since 2010-11.

While the rising pace of global consumption has been sustained by drawing down stock levels in recent years, inventories are now approaching historic lows.

World raw sugar prices, after falling for over a year and then bottoming at less than $0.11 per pound in August 2015, are finally trending higher.

From Sweet and Low to Sugar Highs

Sugar FuturesSugar Futures

Sugar’s price history, these past few years, has been an intriguing drama with an ever-thickening plot.

Since 2011, No. 1 sugar producer, Brazil – along with Australia, Thailand, Mexico, and India – has created an international sugar glut that resulted in a steep drop in world sugar prices from $0.32 per pound to $0.11 per pound.

But the surplus has finally come to an end.

Adding to the effects of the worldwide production shortfall are dry growing conditions in major producer nations, as El Nino weather patterns cause parched fields from Thailand to India – the world’s No. 2 producer of sugar.

Brazil Drives Volatility

Political upheaval in Brazil, the world’s largest sugar-producing country and the largest exporter, has been the key driver of price volatility this year.

Brazilian farmers have become reluctant to sell sugar on the international markets because the Brazilian real has been especially volatile. Farmers have been quick to hold off on sales when it appreciated, and were just as eager to liquidate their supplies when it depreciated.

Fifty-seven percent of Brazil’s sugar cane crop is now converted to ethanol, further contributing to the sugar deficit.

As a result of all this, Coca-Cola Co. (NYSE:KO) reported that it is halting production of its namesake soft drink for the foreseeable future due to sugar shortages.

The US Company, which manufactures out of economically-troubled Venezuela, claims it has run out of the raw material in the country, amidst an economy teetering on the edge of collapse with widespread food shortages and inflation forecast to surpass 700%.

India’s Drought

Insufficient rainfall in India has also affected this sugar shortage, forcing over 100 sugar mills to halt production in February, according to the Indian Sugar Mills Association.

Sugar consumption in India, however, is expected to rise to a record 27.2 mmt while the country’s production is forecast to drop to 25.5 mmt due to smaller areas being cultivated, as well as lower yields.

Drought conditions have encouraged farmers to keep existing cane in production longer rather than planting new cane. Stocks are thus expected to fall 18%.

Furthermore, according to government sources, the country may revoke compulsory sugar export orders after two consecutive droughts have potentially turned the country into a net importer – rather than exporter – next season.

Farmers will no longer receive payment after an order is revoked; thus, without subsidies, Indian mills will struggle to export profitably.

Additionally, production in the European Union is expected to decrease by 650,000 metric tons, to 16.1 mmt — nearly 10% of global production.

China Loves Sugar

China’s production is also down 400,000 metric tons to 10.6 mmt — which is about 6% of global production. But China’s consumption is more important here.

Sugar consumption in China, projected at a record 17.8 mmt, continues to trend higher, bringing stocks down to 3.2 mmt, while production is forecast to decline to 8.2 mmt.

Over recent years, higher land and labor costs, and the cancellation of minimum purchase prices in the Yunnan, Guangdong, and Hainan provinces have resulted in growers opting to grow other, more profitable, crops such as tobacco and bananas. Imports are forecast at a record 7.9 mmt.

A report, China Sugar Blues from April 20, revealed that the sugar industry in China – already having suffered for four consecutive years – continues to struggle with high production costs, the elimination of government support prices, and import competition.

As of early March 2016, approximately 90% of China’s sugar manufacturers were operating at a loss according to industry reports, and a number of mills were already closed.

The United States Shifts Gears

Of course, China is not the only nation that loves its sugar.

The U.S. consumes 10 million short tons (mst) of sugar each year, 20% of which comes from imports. What is important to note, however, is that absolutely none of the sugar grown on U.S. soil is exported.

Production in the U.S. is forecast to be down 200,000 short tons from last year to 7.9 mst, which is based on projected lower cane yields. Meanwhile, imports are expected to rebound 8% to 3.2 mst, and stocks are projected to dip 5% to 1.5 mst.

Until recently, the global price of sugar was not of much concern to U.S. farmers. Even while the international price remains barely half of what it costs to produce the commodity, farmers still have an incentive to grow sugar beets because the USDA actually regulates the amount of sugar produced nationally to protect the industry from outside influences.

By adhering to the World Trade Organization (WTO) rules, the USDA ensures a stable domestic sugar industry, while continuing to bolster relationships with its trade partners.

Both the WTO and the USDA classify sugar as an “essential” food, meaning it’s too important a crop to rely heavily on imports. Members of these organizations control their supply by producing only what they consume.

And while cane was once the dominant sugar in U.S. markets, beet sugar has taken the lead in the past few years.

This is because beets can be grown in colder climates and is, therefore, a more versatile sugar source. Furthermore, cane has to be processed twice, making it more expensive to produce than beet sugar. So, cane producers, like those in Brazil, are moving into the ethanol market.

Anti-GMO Influences

One of the biggest health trends in the U.S. is currently non-GMO.

Food production companies are jumping on the bandwagon in an effort to stay ahead of the curve, causing a major shift in the sugar industry.

In 2008, many farmers switched their crops from regular sugar beets to genetically modified beets, which were engineered to tolerate a weed killer called glyphosate.

GMO beets require the application of weed killer only a few times each season, rather than every 10 days like non-GMO beets, according to an NPR report. Practically all of the U.S. production of sugar beets comes from genetically modified seed.

As a result, there has been a major backlash from the anti-GMO crowd. Slowly but surely the larger players in the food industry, such as Hershey (NYSE:HSY), are buying into the movement. Hershey is shifting its entire candy portfolio out of GMO, thus using a lot more sugar from sugarcane rather than beet sugar.

This poses an additional problem: with so many farms focused on cost-effective beet sugar, the beets of which are GMO-based, there is a sudden shortage of sugarcane.

On May 5, 2016, just days ago, 45 U.S. Representatives signed a letter asking Department of Agriculture Secretary Tom Vilsack to increase the tariff quota for raw sugar, in order to address insufficient domestic supply. The tight supply has sent futures prices even higher.

Sugar Prices – Oh… How Sweet It Is!

Speculators are now taking a more active role in going long sugar, according to recent CFTC reports. And for now sugar looks like it will hold its upward trend. Technically, the charts point to a price of $0.20 per pound.

If you have taken a position in sugar, make sure to keep an eye on the forward curve, and hedge or stop-out your position, because, after all, a sugar high can always turn into a sugar crash.

Good investing,

by Shelley Goldberg

6 Likes

Balrampur Chini seems to be taking good support at 50 DMA & risk reward looks favorable. Attaching the chart for reference

2 Likes

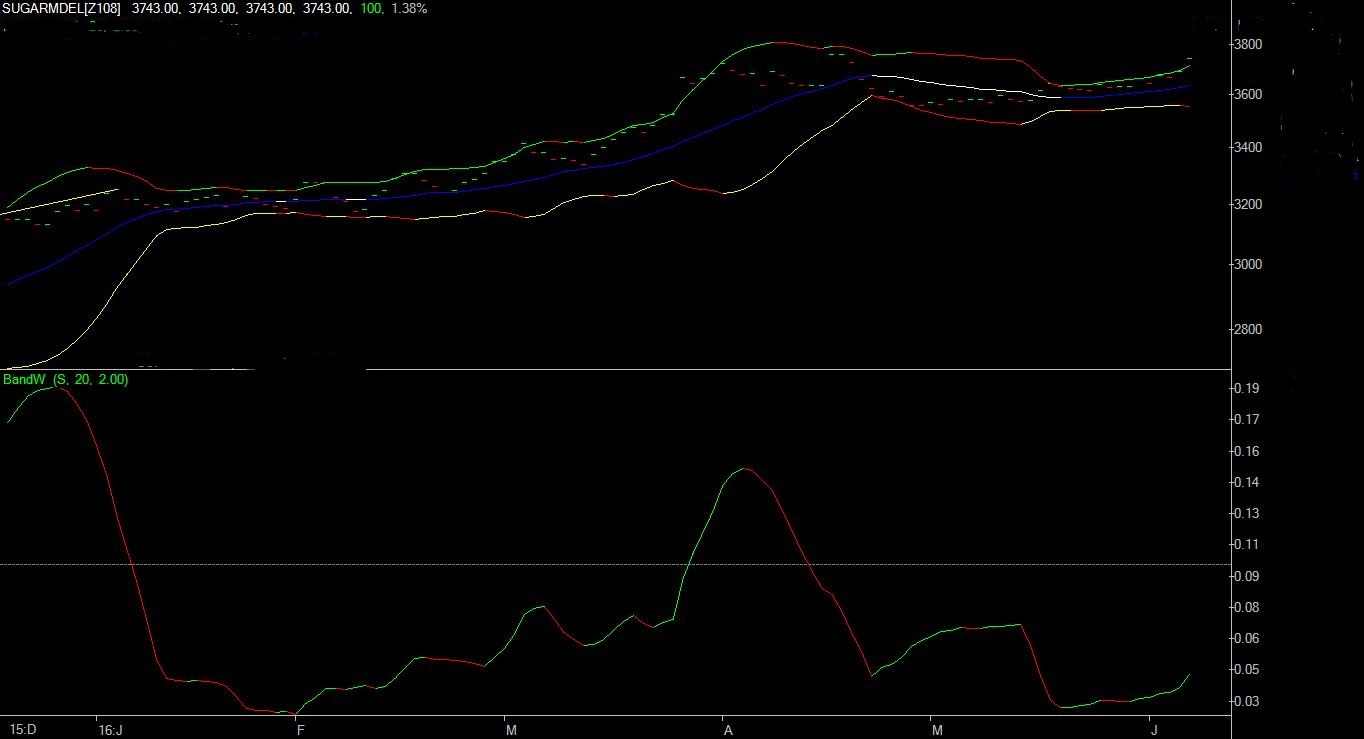

Pl refer to my two posts in May on the prospects of resumption of rally in domestic sugar prices. Today the spot sugar price in Delhi has closed at 3745 rupees per quintal. it appears that the next leg of the rally in sugar price is on…The global sugar prices too are at a two year high @19 cents…partly in anticipation of shortage of sugar in india…therefore it is natural that domestic sugar prices too are in uptrend…

As can be seen in the daily chart above, the bollinger bands are in expansion… indicating the beginning of rally.

It is just a matter of time before sugar stocks too join the party…

2 Likes

I am posting the weekly chart of international raw sugar price (ICE SUGAR 11) with Bollinger bands to show how the said price is in a big uptrend…its going to be a party time for sugar stocks

6 Likes

Thanks for knowledge sharing Fatima Jee. Which stocks in your opinion are in best position to take advantage of this situation from an investment perspective…

Balrampur Chini looks the best to ride the wave. It has good management and good capacity pus it has the second largest store of sugar inventory. To add to all this, it has not fired recently.

DISC: Invested recently

5 Likes