5 reasons the bull run in sugar is not over

I buy when things are low and no one wants them. I keep them until they go up, and people are crazy to get them.

Hetty Green

the primary reason for the sugar price rise in global markets the deficit forecast by global majors for the crushing season 2015-16 as against surplus of 2014-15. Leading global research firms like Kinsman has forecast global sugar deficit of 3.2 million tonnes in the current crushing season as compared to 3.4 million tonnes of surplus last year.

With downward revision in sugar output in India at 27 million tonnes for 2015-16 season, 2% decline from the previous year, production surpasses consumption by 3.5 million tonnes.

Even i have been avoiding commodity stocks most of my life; because have been hurt badly in past. But i feel if you have done your homework well they reward you handsomely.

I have not invested yet in any sugar stock. But price action seem to be showing right signals. Frankly scared and don’t have any idea of sugar companies there capacities, location advantage, etc.

Sugar is once in a decade rally from last two weeks. According to some international report for 2016 global sugar deficit is likely to be around 2 million Tonne and for 2017 it is around 5-6 million tonne, which likely to support higher sugar prices in near to medium term. If next year some weather related adverse things happen in Brazil, India etc than deficit and correspondingly sugar prices even higher. Personally for me this was very rewarding and helped me increase my overall portfolio by about 20%. This is among the best gain i had in so short duration in my investing experience of 5 years.

As I said earlier, apart from global sugar deficit and improvement in sugar prices, there is structural change happening in the sector - one is export incentives, progressive ethanol blending program and most important is cane price linkages (hopeful to get through over 2yrs timeframe)…Another news doing rounds after UP Govt assisted millers last sugar season, this time Central Govt is planning to pay farmers to reduce cane arrears situation in the country.

Didnt like the subsidised route Govt (like in petrol and diesel) is taking addressing the issue but I am hopeful that over next 2-3 years they will get back to linkage – just rough calculation on this year estimated production of 26-27mt - subsidy burden will work out to around Rs 140-150cr (Rs 55/ton subsidy) against a huge arrears of over peak of the season last year - wont help address the actual situation

Govt may pay sugarcane growers directly to help mills: Srcs

Read more at: http://www.moneycontrol.com/news/economy/govt-may-pay-sugarcane-growers-directly-to-help-mills-srcs_3707881.html?utm_source=ref_article

http://www.moneycontrol.com/news/economy/govt-may-pay-sugarcane-growers-directly-to-help-mills-srcs_3707881.html

Companies with high sugar inventories will see improvement in their balance sheet.

http://m.agrimoney.com/news/china-sugar-woes-to-drag-it-behind-thailand-in-output-league--8850.html

Abandoning sugar cane’

The bureau’s downgraded forecast for Chinese sugar production reflected too ideas of a drop in cane area, driving production down 8m tonnes to 90m tonnes.

"Since 2011-12, the [state guaranteed] floor price for sugar cane has dropped by more than a quarter, while production costs are estimated to have nearly doubled, largely due to higher labour costs.

“Farmers have increasingly been abandoning sugar cane and switching to specialty crops to increase farm income.”

This has led to China sugar imports increase by 50%.

Drought in Cuba too contributes to sugar deficit predictions.

Interesting interview by Mawana Sugar mgmt

Even after the partial decontrol of sugar about two years ago, mills continue to be under pressure. Mills are forced to pay a high price for sugarcane to farmers and a series of measures taken by the government is not helping. Mawana Sugars promoter Siddharth Shriram tells Dilip Kumar Jha that till the Rangarajan committee formula, which proposes linking cane pricing with final product prices, is implemented, the industry’s woes will persist. Edited excerpts from the interview.

Sugar mills in Uttar Pradesh are badly affected. How do you view sugarcane pricing in the state?

The Rangarajan committee formula which ensures 75 per cent of sugar revenues to farmers and 25 per cent to millers is a welcome design. However, the UP government, which has traditionally announced cane prices as state advised price (SAP), has not accepted this formula. It prefers to have a situation where it can decide cane prices, for whatever reason, without reference to sugar prices.

The Centre has taken measures to improve the situation. Will these measures help turn around the sugar industry?

The Centre is trying to increase the prices of sugar by organising exports. While the intention is good, it might not be possible within the confines of the World Trade Organization. If it is possible, will the mills be asked to make up the losses on the export price? Why should this be, especially since cane prices have been artificially determined by the state government?

Many mills, such as ours, are unable to access the central government’s excise loan which was to be interest-free for a number of years or for participating in the Rs 6,000 crore loan that the government has given only to pay farmers (this loan will have to be serviced in future years, after the first year). This leaves us in a pretty poor state. The government comes out with relief measures too little, too late.

What is the way out for companies?

Having announced a high price, the state government is reluctant to reduce these for obvious electoral purposes; it cannot reduce the price farmers will get. In this case, who will bear the burden of the difference between cane prices and sugar prices, which until a month ago was a negative 30 per cent (about Rs 6,000 a tonne)? If the government wishes to give subsidy, so be it. That is their political business. However, the industry should only be responsible for 75 per cent of sugar prices to farmers. Most of the balance sheets of sugar companies are in poor shape. Some that have more power or ethanol for sale are in a better shape. Others which run old plants, and have a higher cost of production, are in a pretty serious shape.

What is the solution?

The Rangarajan Committee formula with a proviso to make payment for sugarcane in three tranches would work. The miller would pay the first tranche of about 25 per cent within 14 days of purchase of cane to the farmer. Forty per cent would be paid about three months later when some of that sugar is sold, and the balance would be paid by the end of the sugar year.

This has the benefit of reducing interest costs for millers as we will not have to take loans from the banks who in any case are reluctant to give loans under the circumstances.

High sugar price is really a price signal for the farmers to grow more cane. A lower price will balance the economics between sugarcane and other crops and the farmers can decide which way they should go.

What about the mills? Can there be a win-win solution for both farmers and mills?

It will take at least two-three years of high sugar prices to repair the balance sheets of companies, so the government should implement the Rangarajan Committee after two years from this season. The farmer will get two years to decide whether he wishes to grow sugarcane or any other crop. In the next two years, the central and state governments could make up for the losses that are likely to accrue. Thereafter, with the linkage of sugarcane prices and sugar prices, we will not need any further government intervention.

Return ranking of sugar stocks in last 1 month:

(1) Dalmia Bharat Sugar - 191 %

(2) Dwarikesh Sugar - 175%

(3) Dhampur Sugar - 81%

(4) Triveni - 68%

(5) Rajshree sugar - 59%

Some other sugar stocks return : Sakthi sugar (58%), Balrampur (38%), Oudh sugar (36%). So generally UP based sugar stocks with lighter balance sheet and smaller MCAP seem to be outperforming. Still 3-4 times return in next 2 years cannot be rules out from these levels if things play out as expected. Govt is also talking about some rational sugarcane policy in next 1-2 months which augur well in near term. Proposed conditions imposed by govt can weed out marginal and weaker players from the sector.

2 Likes

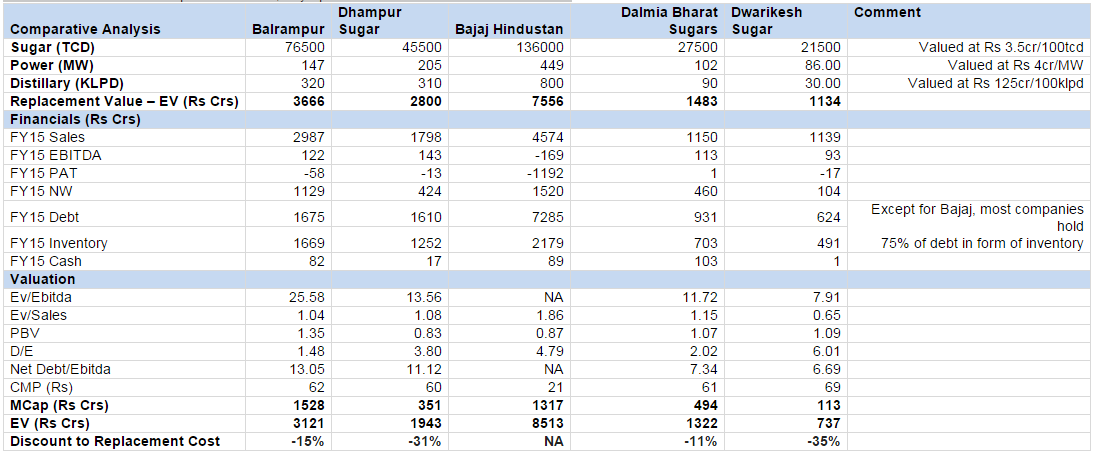

I have Reworked SOTP of key sugar companies post recent rally - Balrampur and Dalmia Sugar discount has come down significantly but Dwarikesh and Dhampur still provides some headroom there. Just to highlight, Replacement cost might also go up as market will start paying premium to earlier price given the attractiveness of the sector. I have not revised replacement cost, any upside revision will increase the discount.

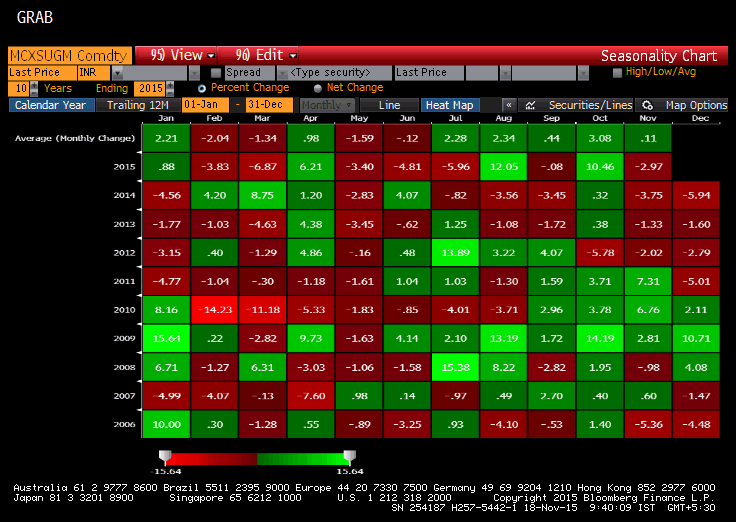

But few days back i was checking 10 year seasonality chart of global sugar prices which suggests that any 3-4 month of rally in sugar price is followed by prolonged correction…will try to update that chart…so i feel the recent rally in sugar price will wane off in 1-2 months time…once that correction starts reflecting in sugar prices then we will see some correction in these stocks which ran up too fast too soon…i might be wrong but such a rally in short span is irrational…

2 Likes

Chintan, you are right being a cyclical industry usually once uptrends start it continue till march of next year then because of weather related uncertainties correction happens between march and july and depending upon monsoon conditions it moves up and down. However during poor monsoon years (like 2015) usually uptrends continue for 2 years because major effect of poor monsoon is felt in next year crop and cause larger sugar deficit. Poor monsoon has three prolonged effect reduction in acrage, reduced production of sugarcane and lower recovery which magnify its effect. Because sugarcane takes between 10 to 15 months for full development there is no much scope for supply improvements in between times. Same stories was repeated during previous monsoon drought of 2002 and 2008. Also usually south based sugar companies are better managed like EID Parry, Parry Sugar, Bannari Aman etc and they tend to outperform in latter part of cycle from UP based companies.

1 Like

Just a query, should we be taking the working capital debt (that is covered by Inventory) in the EV calculations. i beleive we should take only the long term debt for calculating the EV. The LTD should be much lower than reported here for all companies.

Balrampur Concall – Guided for firm sugar prices, accommodative SAP policy, 5% lower industry-wide output. At Balrampur, Some volumes at Cogen and distillery will get spilled over to next year on a/c of ongoing capex

· Policy measures taken so far:

o Govt provided soft loan of Rs 6000cr to industry to clear cane arrears

o New Ethanol tender for 266cr ltrs is for 10% blending of which 110cr ltrs has been contracted so far (Company has contracted 7cr lts to be supplied between Dec’15-Dec’16 period)

o Govt exempted excise on ethanol produced from new molasses which will add Rs 5/ltr to ethanol realization

o Govt mandates 4mt of sugar exports proportionately across all sugar units (Balrampur’s share would be around 115 lakh quintals)

o As per media, Central Govt to pay cane farmers Rs 5/quintal directly which will reduce cane cost by the same amount for the millers

· Sugar production lower than last year: For next season, management expects 26.5mt vs 28mt output in SS14. Early estimates suggests UP to produce 7.3-7.5mt, Maharashta production will come down from 10.5mt to 8.5mt and Karnataka output will be 4.6mt vs 4.9-5mt last season.

· Cane Prices: For UP SAP, mgmt. indicated that it will get notified over next fortnight (key for next season). Mgmt expects that there will be similar linkages which was there in the last season but it will be more accommodative than what it has provided last year.

· Sugar Prices: On sugar prices, due to global climatic conditions and expected lower sugar output, global sugar prices inched up from 10 cents to 15 cents in recent month. Following the global cues, indian sugar prices also inched up from low of Rs 22.5/kg to Rs 27.5/kg currently. Management is positive on sugar price trend and expects prices to remain firm. However, at current prices, industry making loss of over Rs 3.5-4/kg. On export front also, industry making loss of Rs 4-4.5/kg on raw sugar.

· Key policy announcement made this qtr: One is Rs 6000cr soft loan to industry with 1yr interest subvention, two on export incentive on raw sugar export, three on duty waiver on ethanol – will lead to 12.5% improvement in realization for the company and four on consent to increase ethanol blending, however, these needs huge investment to cater to the OMC demand at 10% blending

· Capex: Company plans to shift its distillery to 100% ethanol focus units. For this, Company plans to spend Rs 200cr over next 2 years towards its distilleries to become zero discharge and complaint to pollution norms. Expansion will be phased out from current 7cr ltrs to 9cr lts by next year and further 10.5cr ltr capacity in FY17 will be available.

· Current Debt at Rs 1050cr (LT Debt Rs 651cr and ST debt of Rs 400cr) vs Rs 1233cr in Q1, D/E at 1x vs 1.18x in Jun’15. Of the LT debt, only Rs 150cr is interest bearing to the tune of 10%, Rs 50cr of 2% and balance is interest free. Against this, Company holds sugar inventory of Rs 736cr. Current cane dues at only Rs 119cr vs Rs 600cr as of last qtr.

· Lowers guidance for distillery and cogen due to ongoing capex: Due to distillery expansion, some volumes of this year will get spilled over to next year during the construction phase at the respective units. So for full year FY16, mgmt. guided power sales will be around 55cr units vs 62cr units they reported in FY15. While distillery sales will be around 70000kl vs 74202kl last year.

Enjoy the great sugar rally till it last. Some smart money is also started entering into the sector. Mr Vallabh Bhanshali of Emam fame has invested in Balrampur for his family account.

Akash Bhanshali disclosure

1 Like

Please refer to my post dated Sept 3, where I had pointed out the turnaround in Sugar cycle …when Balrampur was @ 40, Dhampur was @ 30 and Bajaj Hind was @ 12… That time the boarders were quite sceptical about the turnaround…Now when the stocks have almost doubled, everybody appears to be turning bullish…That’s the way market works…

3 Likes

I hope you bought into the turnaround story!

I had some positions which were squared off last month and here we are today.

Looking at aluminium for a turnaround. Will be like 2 quarters though.

MCX Sugar seasonality Chart

– For last 10 years, Sugar prices have rallied 9 out of 10 years in the month of October followed by correction in Nov (6 out of 10 years) and Dec (6 out of 9 years)

– Feb, Mar and May remains the weakest period in terms of sugar price

– While Aug, Sep and Oct are stronger period

For CY15, 4 months have seen positive months for sugar prices - worst year was 2013 where only 3 months where sugar prices were in positive trend. On an average, every calendar year 5-6 months see poisitve trend in sugar prices followed by decline in sugar prices…

to highlight further…from Dec-Jun period, only two months see positive trend which suggests sugar prices at most can sustain at these levels or closer to cost of production

Things which can be explained for such rally in sugar stocks is:

- Sugar price improvement by 20-30% from low in August (Seasonality chart suggest 9 out of 10 years, sugar price have rallied in the month of October - which explains festive seasonality) 2. Ethanol blending and excise exemption 3. 1-1.5MT lower production expected in upcoming sugar season 4. And, 4MT sugar exports mandated by Govt to reduce sugar inventory of current year’s surplus

Now from here onwards, key trigger for sugar sector will be UP SAP which is going to get announced in few weeks from now as UP will start crushing from Nov-end and Dec onwards. With the SAP price, one need to track the sops UP govt will add to it - last year they provided assistance of Rs 280/quintal which was linked with sugar price capped at Rs 31/kg. So this year one need to see how much saving millers will get from the sops which will determine profitability of the companies for coming season. Also if sugar price firm up closer to cost of production then also companies will turn profitable.

4 Likes

According to Assocham study sugar prices in india is likely to firm up from summer of 2016.

Assocham press release about sugar study. Also as per recent concall of EID Parry, bounce in sugar prices from recent low of around 11 cent / lb to 15 cent / lb is technical in nature as most global projections estimates deficit of around 2-3 million tonne for consumption of around 182 million tonne for year 2016. However projection for 2017 is more supportive of global sugar prices. Also US FAO project that sugar prices can touch 18-19 cent / lb based on fundamental factor by 2017 which can be fair value of sugar considering expected demand supply scenarios. However from 2018 again some surplus is possible. All bounce back in commodity prices start with bit skepticism but gain ground based on future events playing out. However with severe deficit of monsoon in 2015 usually shock in sugar cane supply mostly surprises in downside and expectation of sugar prices touching 40-45 range sometimes in next 2 years in indian market cannot be rules out as agricultural product prices in india moves up very sharply in short duration. Also logically it does not make sense that in a country where hardly any vegetables or food staples available below Rs 40 only sugar is available below Rs 30 which is more difficult to produce and consumes more time , money and efforts in producing 1 kg of sugar than any other crop based food items.

Bloomberg survey projects even lower sugar output this year itself

Andhra Sugar can be one of the very safe play for those who want to own a sugar stock. Quite undervalued too

Market Cap: 370 crores (having reserves of 547 crores)

D/E: 0.6

Debt: 326crs

Despite being a commodity play has strong dividend payout (dividend paid continuously for atleast last 15 years) providing cushion

Businesses:

SUGAR

CAUSTIC SODA

POWER GENERATION

INDUSTRIAL CHEMICALS

It is a asset-rich company and is one of the most efficient producers of caustic soda and sugar in the country. All the business are showing good profit growth in the last quarter.

Also the company posted a quarterly eps of 6.xx rs. The sugar division has turned around and posted marginal profits instead of losses. The other businesses were already showing good profits and once the sugar prices go higher EPS would increase exponentially.

Company holds 55% in JOCIL. It has got investment in Andhra Petrochemicals and APGPCL (Power Generation).

Gas prices would come down soon due to which power generation costs would also come down.

Company has been trying to make itself self sufficient for its power need and also supplying power to SEBs.

Government has increased power tariff which has led to increased revenue realization for the power division

Recent excerpt From ET paper:

The replacement value of the assets is more than Rs 2,000 crore, whereas the enterprise value (EV) is hardly Rs 500 crore.

And with rupee depreciating badly, caustic soda being a import substitute could be benefited. Therefore both business verticals - sugar and caustic soda - can give robust earnings in the next two years

Disclosure : Invested

Regards

Sri Krishna Bhutra

2 Likes