Finmin changes mind, offers ethanol producers Cenvat relief – Financial Express (Impact on Balrampur Chini)

Impact on Balrampur

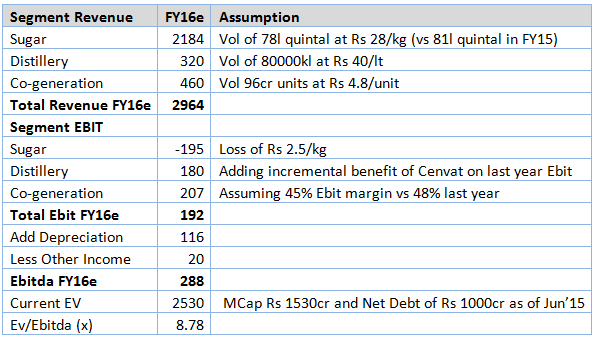

• For Balrampur, Company produced 32500kl of Ethanol in FY15 against total distillery production of 69900kl. With OMC offtake started picking up, company produced 21000kl of Ethanol out of total distillery production of 24500kl in Q1. Further, company is making investment of Rs 200cr in its distillery to align with pollution norms. With that, company will be able to run for 330 days vs 250 days earlier, effectively increasing its production 12000-17000kl of additional volumes by Sep’16.

• Company’s current realization is around Rs 40/lt with this cenvat and excise benefit, company’s cost will decrease by Rs 4-5/lts in upcoming season. Assuming, c15% growth in volumes in FY16, incremental benefit of cenvat/excise will be around Rs 35-40cr to its EBIT for this fiscal. For FY15, Company reported distillery Ebit of Rs 144cr which is likely to increase to Rs 180cr in FY16e.

• Overall, Company likely to report Ebitda of Rs 288cr (assuming Ebit loss of Rs 2.5/kg on sugar), Stock trades at 8.8x its FY16e Ebitda.

Sensitivity of Sugar loss on FY16e Ebitda – In FY15, Company made a Ebit loss of close to Rs 3.5/kg, base case I have assumed Ebit loss of Rs 2.5/kg in Fy16

Computation of Ebit loss for Sugar: FY15 Ebit loss at Rs 278.5cr; total qty sold during FY15 at 81.45lakh quintal, loss/kg works out at Rs 3.42/kg

Discl: Not invested, but sector does look interesting

3 Likes

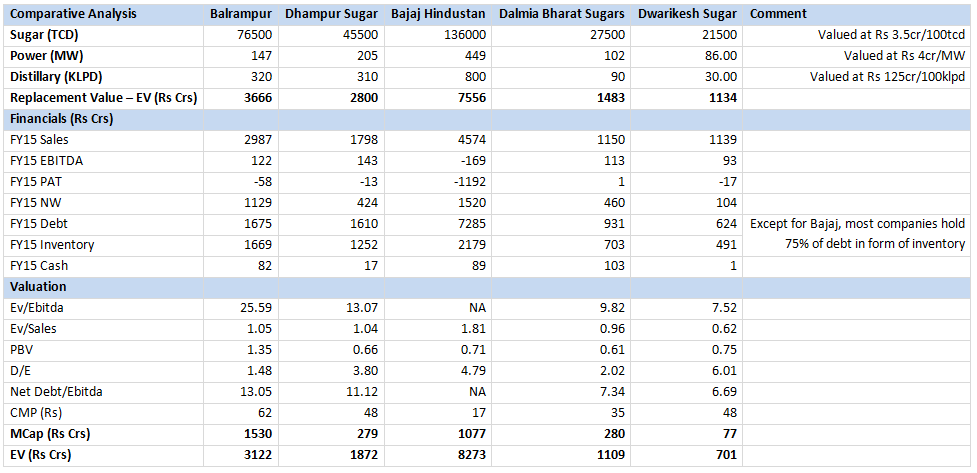

I tried to check few sugar companies based on their capacities and compared it as below:

• Balrampur remains best play in sugar sector with strongest balance sheet

o Compared to Balrampur, Dhampur Sugars have similar capacity of Cogen and Distillery however sugar capacity is half of what Balrampur have. Dhampur’s MCap Rs 279cr vs Balrampur’s Rs 1530cr. On Leverage side, Dhampur is more levered at 3.8x D/E than Balrmapurs’s D/E of 1.5x based on FY15 numbers.

• In Small cap, Dalmia Sugars remains better play given best in the industry recovery rate and have history of turning around sick units which they acquired in Kolhapur. It is one of the very few sugar company to report net profit in FY15

o However, Dwarikesh Sugars have almost similar capacity but have MCap of only Rs 77cr vs Dalmia’s MCap of Rs 280cr. This is partly due to high leverage in Dwarikesh (6x D/E). However, both companies have over 75% of debt locked in inventory.

• I would like to highlight that Debt figure is based on FY15 numbers and there is high likelihood of these figures at present will be much lower after liquidating sugar inventory as well as release of financial assistance by UP Govt in Q1-Q2. For e.g Balrampur had debt of over Rs 1675cr which came down to Rs 1200cr in June and another Rs 200cr which got released by UP govt will bring that debt figure to Rs 1000cr.

• Have not compared Shree Renuka in the list as their losses and debt figures are too high to make any sense plus their Brazilian ops is under bankruptcy.

One can play around the replacement cost for divisions - changing the numbers as feel fit - but just to highlight here…in FY13 and FY14 Dalmia Sugar have acquired 2 units in Kolhapur one was operating and another one was closed for 7 years and have turned it around…Operational one was bought at Ev/tcd of around 5cr (2500tcd at Rs 125cr) while closed one was bought at Rs 1.4cr (Rs 1750tcd at Rs 24.3cr). I have taken Rs 3.5cr/tcd valuation which i think is fairly conservative. Cogen (Rs 5cr/mw for a wind farm, Rs 4cr/mw for cogen is fair) and Distillery (based on interaction with Balrampur Chini IR).

Discl: Not invested in any of the above mentioned stocks, but as mentioned earlier it does look interesting.

9 Likes

Chintan, Great analysis of sugar stocks. It may be more interesting to include some of other sugar companies like Rajshree sugar (13500 tcd), EID Parry (34750 tcd), Triveni (61000 tcd), Parrys sugar (4000 tcd), Thiru Arooran (8500 tcd).Please find various sugar companies mcap potential (rough estimates) if sugar stocks behave in similar fashion as during last major sugar cycle between 2003 to 2006. Some of these projections may look unbelievable.

Sugar Companies MCAP Potential.doc (31.5 KB)

2 Likes

I have been buying (since the last 2 years) EID Parry and DCM Shriram on dips (and boy, do they dip!!). The attraction is a) Sugar Business in both cases is only 30-40% of their total business b)their other business (Coromandel and Bioseeds, in the case of EID Parry, and Fertilizers, Seeds, Alkali and Plastics in the case of DCM Shriram) are extremely well run and well regarded c)debt levels are quite reasonable.

My logic is (was) that I have no control over sugar prices. However, the history of Sugar Prices has been that every few years, these companies have a real blockbuster year. However, even in bad years, these two companies don’t go into a loss, their debt remains under control, and they give dividends. So there is no risk to survival. Frankly, if sugar prices were to stay at current levels for a couple more years, than Shree Renuka iwill not the only one in deep trouble.

The flip side is that you don’t get as much of a bounce if Sugar Prices go crazy. But that is the price I am willing to pay for Margin of Safety.

2 Likes

i am not an expert on sugar but being cyclical a change an uptrend in the cycle will definitely give good returns.

BUT i seriously doubt that the returns will be similar to those as in previous cycle like the one in 2005-06.

The sugar cycle is not purely market based and is severely distorted by the government due to fixing of very high cane prices.

even if there is a sharp rise in sugar price, a part of the cash flow will go in paying off the debts to the farmers. At present the total debt owed by sugar industry is about 12000 Cr +

Also the govt in all likelihood will remove the export subsidy and other incentives given to sugar industry in such case.

The farmers may start demanding higher cane prices which their unions have been doing anyway.

Still since the sugar stocks are quoting at historical lows , the returns can be exciting depending on the jump in the sugar prices.

Disc : Invested in Kesar ent and Triveni eng

2 Likes

@manishinlucknow and @samir_brd - Sugar cycles and cane pricing is well known and has been under discusion under this thread in detail

My point here is not looking back at previous sugar cycles which were dependent on either favourable cane prices or sugar realizations…but this time a structural change happening in terms of aligning cane price and sugar realization (formula is not known) through linkage which is being proposed by Rangarajan committee few years back…if that is implemented (partial linkage has been adopted this year in UP where in UP Govt gave financial assistance to millers of Rs 40/quintal which got linked with sugar realization bench-marked at Rs 31/kg) - assuming process to take place in next 2-3 years - than sugar millers will report a fairly predictable earnings in future…that will drive the rerating for the sector…

Yesterday saw following tweets from Farmer association also recommending market linked pricing - i feel this is very positive signal…pure play sugar companies will be benefitted out of it…

@Chintan

i agree. the linkage of cane prices to sugar will be a clear positive , will bring stability and predictability to the business.

The sugar companies have been demanding same for long and the govt knows about this but at the end of the day its a political decision. Lets see.

hi …TUR (pigeon pea) rates were @ 2100/-q two year back because of low rate farmers were forced to switch to other crops.now rates are 12000/-q .so the cycle changes very fast were is crude oil now .

this year or next year sugar cycle will turn if not this year then it will be sharp drop in stocks prizes and after turn of cycle sharp recovery to…but when it will drop there may be more shree renuka"s same mill will be shut for ever.

i say so confidently Brazil is having problem last year also drought .Brazil have more then 45% world market share so …and i don’t think this market link prizing will be beneficiary to this dept laden sugar cos. they will survive only nothing else…

Just to clear one misunderstanding about cyclical investment like sugar. Ben Graham in his famous book security analysis has following observation " When a rise in the price of a commodity occurs, there will ordinarily be a larger advance, percentage-wise, in the shares of high cost producers than in the share of low-cost producers. Contarary to the general impression, the stock of high cost producers are more logical commitments than those of low cost producers when buyer is convinced that a rise in the price of a commodity is imminent and he wishes to exploit this conviction to the utmost. ". Also generally highly debt and most inefficient companies tend to give higher returns than strong balance sheet companies. So cyclical investing in that sense is bit counter intuitive. Also because conditions of sugar companies are worst among all cyclical like steel, mining, oil etc so their return is also likely to be highest among all cyclical also during up cycle. For example during sugar cycle of 2003 - 2006 , return of popular sugar companies are below in no of times:

Balrampur - 20, EID Parry - 19, Dhampur - 37, Sakthi - 31, Oudh sugar - 44. while for major steel companies return is between 3- 7 times and cement companies return are 5-10 times during similar period in previous major commodity cycle.

Note: This summary is sourced from Parag Parikh book of value investing and behavioral finance.

2 Likes

Nice Counter Intuitive thought.

However, pls remember that commodity price movements don’t always work out in an exact manner.

I sort of remember, that years ago I invested in both SAIL and Essar Steel, at almost the bottom of the steel cycle (Must have been 2002 or 2003). Essar Steel at Rs. 3 and SAIL at Rs. 7. Before the steel cycle turned, Essar Steel wiped out the minority shareholders, and SAIL went on to become at least a ten bagger. Had the pain continued for a couple of more years, maybe SAIL would also have gone the IISCO way.

This thread was started by Donald based on a conversation with someone who was an expert on Sugar Prices, who predicted around 2 years ago that Sugar Prices would now have a 2-3 bumper year situation. Well, at that time Sugar Prices were around 17 cents a pound, and sure enough, they rose to around 20 cents a pound almost immediately. (Or this thread was started around the time of this bounce). Well, instead of bouncing, prices went down to 10 cents a pound, till the recent bounce back up to 14 cents a pound.

Now, if in 2013 end, you would have invested in Shree Renuka, with the counter intuitive logic above, you would have been staring at total capital loss. Similarly, if you invest in say Oudh Sugar today, and prices fall back, you could be staring at total capital loss. I personally don’t have confidence in predicting that prices won’t fall back from here.

Ultimately, it depends on the kind of investor you are. It depends on your target return (which in my case happens to be post tax high teens over a looong period), your aversion to capital loss, your insistence on margin of safety and so on. That should dictate your choice of stocks.

8 Likes

Samir, you are right that it is risky bet with lots of if and but and most things depend upon future scenarios playing out both in local and global market. However one thing is quite clear that with this industry a big vote bank (more than 3-4 cr) is also related and any govt cannot afford to disappoint them for long. Indian sugar mills even if they are forced is not in position to pay to farmers in any case. So if current scenarios continue for next 1-2 years atleast half mills have to close down even in that scenarios sugar prices in india has to suit up with or without favorable policy outcomes as sugar demand is inelastic. Also it is highly illogical to force somebody to continue producing something even if he is not interested in producing. So probability of man made (govt in this case) or natural uptick in sugar prices is likely for next 2-3 years. Quantum of gain nobody can predict and we have to keep in mind that we are in bull market for last 2 years otherwise sugar stocks may be even lower than what was 2-3 months back.

3 Likes

I see recommendations on ‘sugar’. Fundamentally, given government policies on cane prices, a company in sugar cannot make money. And politically, the government cannot let sugar prices shoot up. Unless there is total decontrol of sugar and sugar cane, it is unlikely that there will be a story. This is a slippery slope upwards.

from ;- bala 's blog

@samir_brd

well said about commodity prices.

I think it is not possible to time the bottom (without luck). The cyclical downturn generally lasts for few years and varies from industry to industry. For sugar it is going on for sometime now, we are not at the beginning of the downturn. Now how long this continues is anyone’s guess.

Since the sugar companies are under lot of financial stress, the most important point to look is which company can survive the downturn that is which companies are unlikely to go bankrupt and have decent management .As per hearsay some of the sugar mills in eastern UP have already shut down. Many of the co-operative and small mills must already be under duress.

I invested thinking that as the mills are being forced to buy cane at high prices, the govt is likely to give some support to the sector. The govt did provide export subsidy but as it turned out due to surplus supply the international prices were not remunerative even with the subsidy.

But how long this can continue. Are we going to need sugar after 10 years - Yes. Are we going to let our sugar industry die, farmers suffer and import all our sugar - NO. The present situation is unlikely to continue for several more years as more mills will go bankrupt. Cane dues to farmers are already high and is likely that govt will want it to go higher. So some improvement in the sector should come. Hopefully.

However, i am not considering a scenario of high sugar prices, there will be lot of hue and cry and govt in all likelihood will remove subsidy and reduce import duties. Govt will not like sugar prices to go off limits, how much it can control ? I have no idea.

1 Like

I read quite a few annual reports of sugar companies and one trend that was similar was the shutdown of mills for crushing this season. Most of the mills will not be crushing sugarcane this season which should lead to a lower output next year which i think is being discounted in the prices of companies. However this sector being completely riddled with politicians don’t understand how long such a situation is feasible. The conundrum is that even with higher SAP’s & FRP’s neither the farmer or mill owner is happy. So it becomes difficult to take a bet on this.

Great work Karan

No opinion on your opinion, but very happy to see that someone did the boring work of reading the annual reports and judging the mills situation based on facts

As somebody who actually invested (heavily) in sugar and made a crazy return over the last month, I can tell you the factor you put forward was the one least paid attention to

2 Likes

Ok, technically, Balrampur chini is close to a very important level, any sustained close above 70 is very positive as per the attached chart.

For sectors like this, it is best to go with the leader. Period. I wont be buying anything here, but the chart on a break out looks interesting. I know the promoters of Parrys (of Murugappa group). Very very ethical group, however, not sure how this sugar company of theirs stand. If the business looks good, then promoters integrity may not be questionable.

The below is the 8 year daily chart of Balrampur Chini - With long cyclicals, better to look at very long term charts - broader picture is very important, no myopic vision helps here.

Disclaimer: I’m tired of putting this after every post, there should be some blanket disclaimer  I’m NOT a technical analyst NOT a fundamental analyst, NOT a financial advisor. Do your own due diligence.

I’m NOT a technical analyst NOT a fundamental analyst, NOT a financial advisor. Do your own due diligence.

1 Like

Equity of dwarikesh is 47 cr and price 51. Why M Cap is 78 cr. Every dight is showing same MCap. It should be around 200 cr. Can anyone explain please

@Rajesh1975 total share outstanding as per BSE site for dwarikesh is 1.63cr and CMP os Rs 51.6…so MCap works out at Rs 84cr…so equity is of Rs 16.3cr and balance 31cr is coming from preference shares…of the preference shares majority is owned by Neotia family

3 Likes

Excellent work on the inventory data. If the international prices firm up the debt level of Balrampur , dhampur , dalmia , dwarikesh will come down well. ( in the balrampur conf call they said its possible to export the excess inventory with govt help. Modi govt has promised help in clearing the excess inventory through exports. It has been done before .)

These 4 companies have two more similarities.

• The ‘cash profits’ they make even while posting net losses should be looked at. For eg Dwarikesh posted 20 cr cash profit both in 2013 and 2015. This cash profit is probably due to the high depreciation amount they carry on the books.

• They have paid dividends in the good times(05-06). Balrampur and dwarikesh with high payouts.