Adding some reading I did on the ABS market and players in the industry

Market Size and Growth

The Acrylonitrile Butadiene Styrene (ABS) market in India has shown significant growth and is projected to continue expanding. The demand for ABS stood at approximately 0.32 million tonnes in FY2021 and is forecast to reach 0.56 million tonnes by FY2030, growing at a compound annual growth rate (CAGR) of 6.44% during this period. Another report indicates that the ABS market was 238 KTPA in 2018 and is expected to grow at a CAGR of 9.21%, reaching 677 KTPA by 2030.

Key growth drivers

- Electrical and Electronics Sector: The increasing use of ABS in electrical appliances due to its excellent insulation properties is a significant driver of demand. The domestic electronics market is projected to reach $120 billion by 2025, further boosting ABS consumption

- Automotive Industry: ABS is favored in the automotive sector for its lightweight nature, which contributes to fuel efficiency, as well as its resistance to heat and impact. The implementation of new vehicle regulations has also spurred demand for ABS components in vehicles

- Medical Applications: The use of ABS in manufacturing medical equipment, including inhalers, has emerged as a growing segment, especially following the COVID-19 pandemic

The outlook for the Acrylonitrile Butadiene Styrene (ABS) market in India appears promising, with strong growth potential and increasing domestic production, although there are some factors that could affect the market in the short term.

Current market situation

Market Size and Growth:

The Indian ABS market is estimated to be around 300,000 to 320,000 tonnes per annum.

The market is experiencing robust growth with demand expected to increase by 7% to 10% annually.

This growth is driven by increasing demand from key sectors such as automotive, household appliances, electronics, medical devices, and toys.

Import Dependence and Opportunities:

Currently, India relies heavily on imports to meet its ABS demand, with approximately 50% or more of the market being supplied by imports.

The major countries that export ABS to India include Korea, Thailand, and Taiwan.

This high import dependence presents a significant opportunity for domestic manufacturers to capture market share by substituting imported ABS.

Domestic Capacity Expansion:

Several domestic players, including Styrenix, Supreme Petrochem, and Bhansali Engineering, are undertaking capacity expansions to meet the growing demand and reduce reliance on imports.

Styrenix is planning to increase its ABS production capacity to 210,000 tonnes by FY28.

Other companies are also increasing their capacity which is expected to add capacity to the market in the next few years.

These expansions are aimed at meeting the increasing domestic demand and potentially reducing imports.

Competitive Landscape:

The market is expected to become more competitive as capacity expansions come online.

While there are several players in the market, including private limited companies in the ABS market, there are no private limited companies that are direct competitors to Styrenix in the ABS market.

Despite increasing competition, Styrenix believes that the market will grow at a healthy rate, ensuring that all capacity expansions will be comfortably absorbed by the Indian market.

Pricing and Margins:

ABS prices and margins are influenced by global market dynamics, raw material costs, and product mix.

Freight costs can impact the pricing of imported ABS, providing domestic suppliers with a competitive advantage.

Styrenix has a strategy of focusing on specialty grade ABS, which commands better margins than commodity grades.

Styrenix has also implemented measures to improve efficiencies, increase capacity, and optimise product mix to mitigate the effect of fluctuations in raw material prices.

It is able to pass on raw material price increases to customers, which protects their margins.

Trends

The trend is towards increased domestic manufacturing, with the Indian government promoting initiatives like “Make in India”.

There is a growing preference among consumers to buy from domestic suppliers.

There is increasing demand for value-added products and blends of ABS, which provide higher margins than standard products.

Potential Challenges:

There is a possibility of short-term pricing pressure as new capacities come online.

There may be volatility in raw material prices which can impact margins.

The company has to be prepared for some volatility in the market as it operates in a normalised business environment.

In conclusion, the Indian ABS market is poised for significant growth, with increasing domestic production and strong demand from key sectors. While there might be some short-term challenges related to competition and pricing, the long-term outlook remains positive due to the large market potential and the shift towards domestic manufacturing. Styrenix, with its established market presence and focus on value-added products, is well-positioned to capitalise on this growth.

Market share and growth

- Bhansali Engineering Polymers

Market Share: Approximately 37.5% of the Indian ABS market.

Overview: A well-established player in the ABS manufacturing sector, Bhansali Engineering has a significant presence and contributes to the domestic supply chain.

- Styrenix

Market Share: Approximately 37.5% of the Indian ABS market.

Overview: A global leader in styrenics, INEOS Styrolution has a strong operational capacity in India and is known for its innovative solutions in ABS production.

- Imports

Market Share: The remaining 25% of the ABS demand is met through imports, primarily from countries like China and South Korea.

Overview: These imports fill the gap in local production and offer competitive pricing, although they are subject to tariffs aimed at promoting domestic manufacturing.

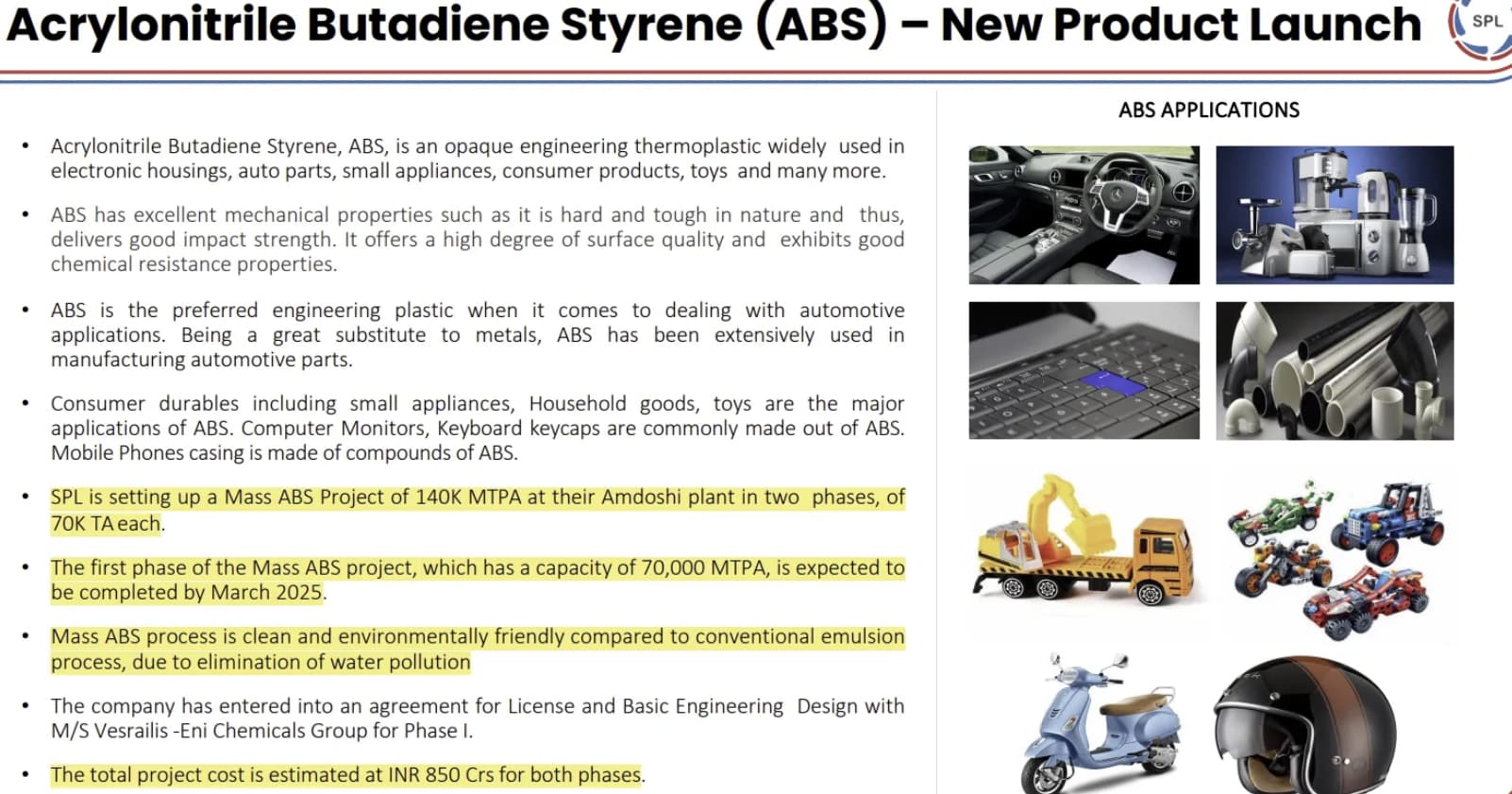

Supreme Petrochem

Supreme petrochem is entering ABS currently. It putting up a new capacity of 1,40,000 MTPA (2 capacities of 70,000 MTPA each).

First capacity will commission by Mar-2025.

Styrenix Platform

The company aims to increase ABS capacity from 105,000 tonnes to 210,000 tonnes and is undertaking a brownfield expansion project to achieve this.

Initial Capacity: Prior to debottlenecking efforts, the company’s maximum production or sales of ABS from its own production was around 65,000 tonnes

Debottlenecking Target for FY24: Through debottlenecking, the company achieved a production volume of 90,000 tonnes of ABS in the previous financial year1.

Debottlenecking Target for FY25: The company is targeting a production capacity of 100,000 to 105,000 tonnes of ABS through further debottlenecking in the current financial year

The company aims to increase capacity to 210,000 tonnes of ABS by FY28

Bhansali Engineering

With regard to enhancement of ABS production capacity from 75000 TPA to 200000 TPA at Company’s existing plants at

Abu Road (Rajasthan) and Satnoor (Madhya Pradesh), the Company had appointed Toyo Engineering India Private Limited

(‘TOYO’) as Engineering consultant for Front End Engineering Design (FEED) and CAPEX Cost Estimation.

The realistic project cost for 200000 TPA ABS capacity will be arrived based on TOYO’s report, detailing the project cost of

increase in SAN, HRG and Compounding capacities at Company’s plants.

The expansion will be funded through internal accruals and the Company will continue maintaining its “Zero Debt Status” in

future as well. As capacity expansion is the “Need of the Hour”, the Management shall endeavor to implement the project likely by March, 2026.

The Company deals with single business segment viz. manufacturing of ABS and SAN resins (which is classified under the

category of Highly Specialized Engineering Thermoplastics)

The Company optimally utilized the production facilities and achieved growth in production and sales quantities. The Company

recorded the highest ever production levels of ABS and saleable SAN aggregating to 75152 TPA, thereby achieving a capacity

utilization of 100.20 % of the installed capacity of 75000 TPA. Similarly, the Sales volume for the FY 2023-24 stood at 75143

TPA as against 73388 TPA during the previous year 2022-23, registering a growth of 2.36 %.

Market share and competitors

Styrenix Performance Materials Limited has a significant presence in the Indian market for both Acrylonitrile Butadiene Styrene (ABS) and Polystyrene (PS). Here’s a breakdown of their market share and competitive landscape, drawing from the provided sources:

Styrenix’s Market Share:

ABS: The company holds approximately 30% market share of the Indian ABS market. In the previous financial year, their market share was around 26% to 27%, indicating growth in this area.

Polystyrene (PS): Styrenix’s market share in the PS market is about 20% to 23%. In the previous financial year, their market share was around 17%, also indicating growth.

Overall Market: The total market size for ABS and PS in India is around 300,000 tonnes. This implies that Styrenix sells approximately 90,000 tonnes of ABS and 60,000-65,000 tonnes of PS.

Competitive Landscape:

- ABS Market

Imports: A significant portion of the ABS demand in India is met through imports, with about 50% or more of the market being supplied by overseas companies. This indicates a substantial opportunity for domestic players like Styrenix to gain market share by substituting these imports.

Key Importing Countries: ABS imports come primarily from countries like Korea, Thailand, and Taiwan, and sometimes from Europe.

Domestic Competitors: There are other domestic ABS producers in the market including Supreme Petrochem and Bhansali Engineering who are also expanding their capacity. However, there are no private limited companies in the ABS market that are direct competitors.

- Polystyrene (PS) Market

Imports: PS is also imported into India with key suppliers being Iran and Thailand.

Domestic Competitors: There are other domestic PS producers but Styrenix believes the market is large enough for both Styrenix and its competitors.

- Blended Market

There is a market for blended materials like polycarbonate ABS and nylon ABS blends. Styrenix estimates the addressable market for these blends to be around 40,000 to 50,000 tonnes.

Market Dynamics:

Growing Demand: The Indian market for both ABS and PS is expected to grow. ABS demand is expected to grow at 8-10% per year and PS demand is expected to grow at 5-6% per year.

Capacity Expansions: Styrenix and its competitors are undertaking capacity expansions, driven by the demand in the Indian market. Styrenix believes that there will be sufficient demand to absorb the increased production from all domestic manufacturers.

Preference for Domestic Supply: The company believes that consumers are increasingly preferring to buy from domestic suppliers.

Pricing pressures: While the market is expected to grow, there could be some pricing pressure in the short and medium-term. However, in the long term, the increased domestic production is expected to reduce imports.

Key Takeaways:

Styrenix is a leading player in both the ABS and PS markets in India, with a strong market share and good relationships with customers.

The company is well positioned to capture a significant portion of the market, particularly in the ABS segment, given the high level of imports currently entering the country.

The company faces competition from both domestic and international players.

The company’s focus on value-added products and expansion will be important in increasing their market share and profitability.

In summary, Styrenix holds a strong position in the Indian polymer market with a substantial market share in both ABS and PS. The market has considerable opportunity for growth. This growth will come from a reduction in imports as capacity increases from Styrenix and its competitors.