The share price continues to rise. In terms of valuations it is getting expensive now. In my opinion, the positive impacts of GST are getting built in. Numbers for coming quarters will need to hold else it would be difficult to hold these levels for the share price. With only around 4000 public share holders (which means on an average 1 shareholder holds around 700 shares), I am getting jittery with each increasing Rupee in share price.

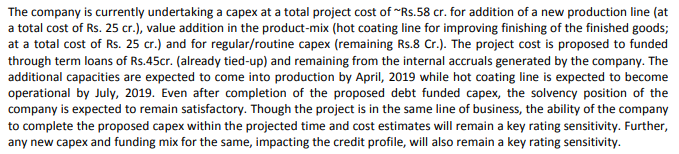

Capex of 60Cr for 60 Lakh sheets/annum of capacity expansion expected to start in July 2016 which is yet to announce. I expect rally in the stock in last few days is majorly because commencement of capacity. Valuation fairly priced now.

Disc: Exited 75% holding, which invested at 250 level

In results commentary by Century Plywoods, they mentioned softness in exports markets for laminates business division. And after the rally in Stylam, and the valuation it is quoting at now, will be cautiously waiting for the results.

Disc: Invested, will look to exit at these levels.

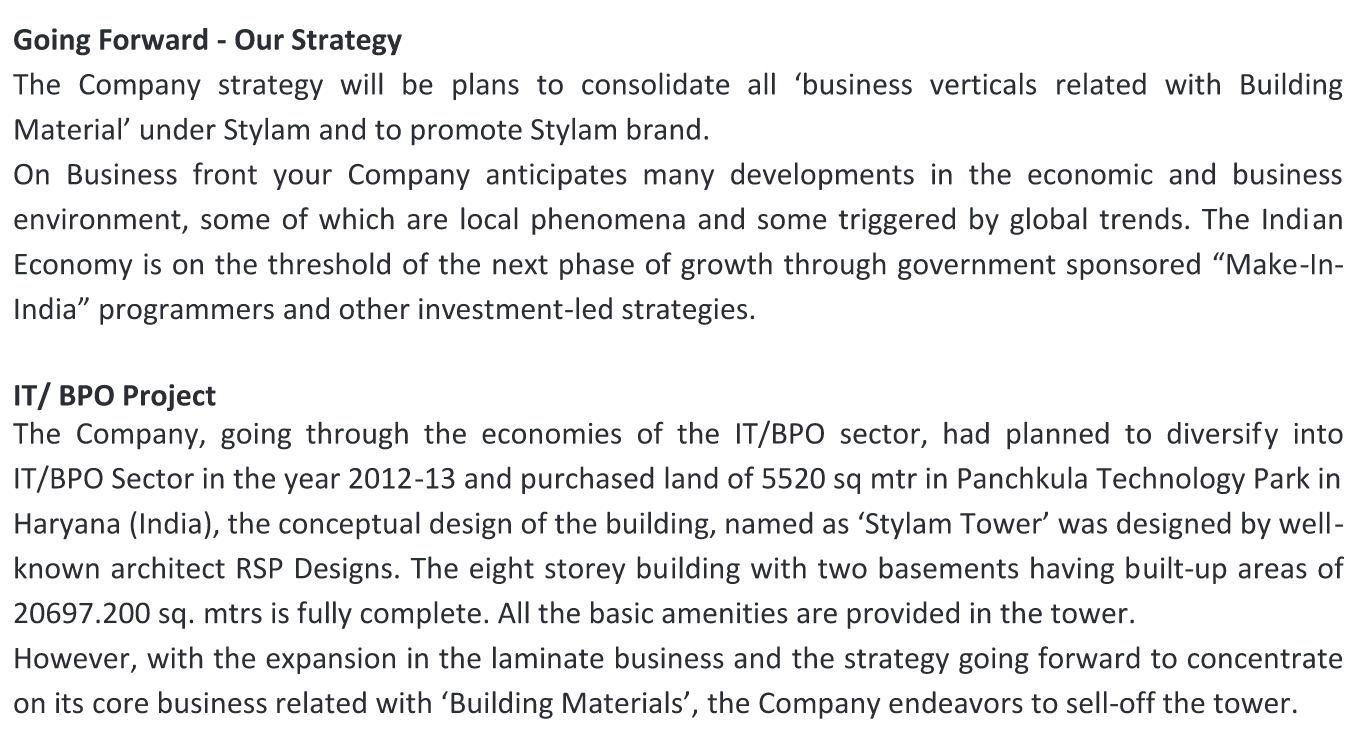

I am hopeful that the management will use land sale to reduce the debt. Is the company obliged to publish when it is sold and the amount it is sold at , or is it just going to be in the ‘other income’ section in the next quarter report to the sale ?

Looking at the announcement, it looks like that the sale is just ‘proposed’ as of now. So, keep a track on its sale. Also, till it gets sold, no other income, and possibly no reduction of debt. after it gets sold, it will be other income.

“We intend to use the infused capital for the growth plans of the company wherein we are doubling our production capacity and launching new products,” said Jagdish Gupta, managing director of Stylam Industries.

concern - Its high time the company looks at reducing its debt. Approx 20% of its operating profit goes into paying interest for last several years.

Stylam introduced 2 new verticals in their current business operations: “Restroom Cubicles & Lockers” by the brand name “CUBOID”.

They are also starting to manufacture “Solid Surfaces” in India by the brand name “GRANEX” and they will be the first one who will manufacture in India with German Tech.

Any reason for significant correction in price?

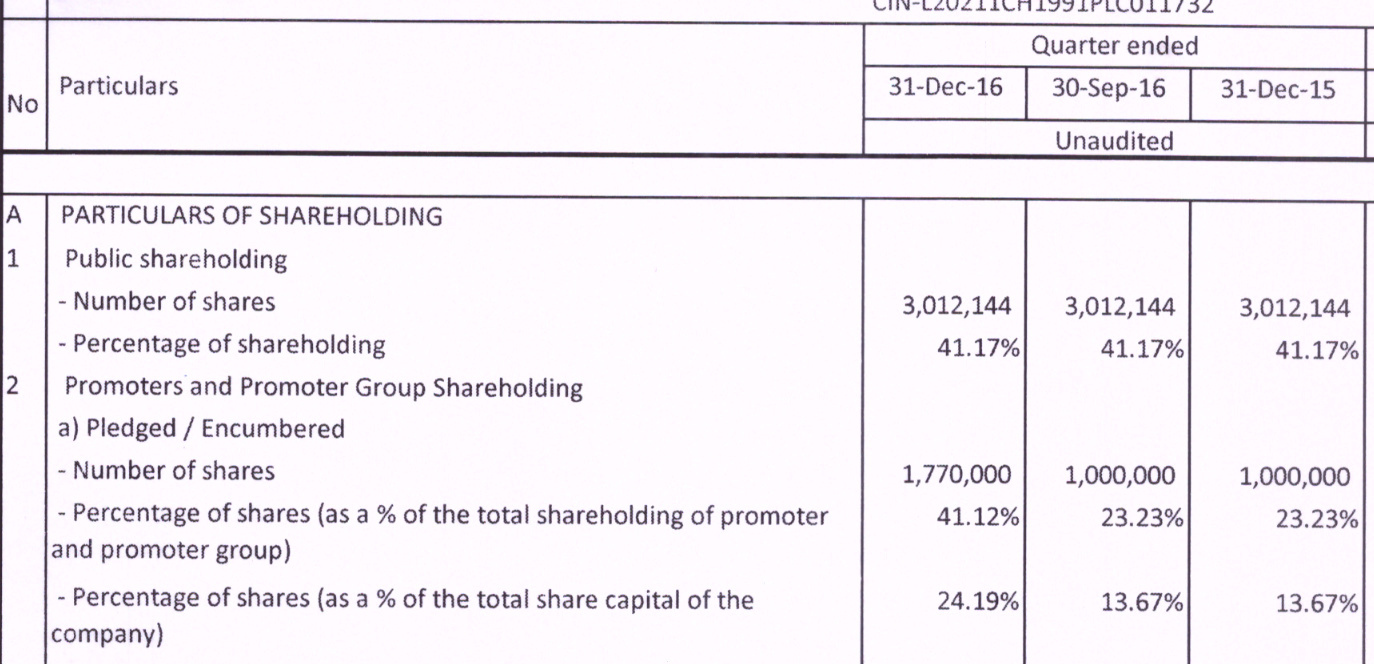

promoters has 41.1% pledged shares, is correction due to forced sell of these shares?

any red flags?

I am just tracking it to invest in it. Kindly share your views on stylam