Their Balance sheet looks to be in a mess! Look at the increase in debt and receivables

Though debt increased, D/E improved to 1.75 from 1.8

Stylam emerges leading exporter of laminates in Italy http://www.dailyexcelsior.com/stylam-emerges-leading-exporter-of-laminates-in-italy/

5 Likes

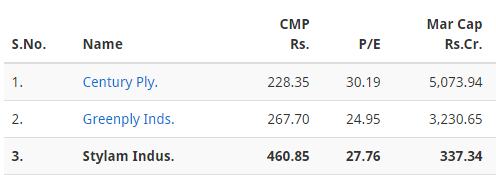

Interestingly, Stylam’s Laminate capacity will almost be at par with Greenlam once its expansion is done which is expected by Dec 2015-March 2016. (it currently has capacity of 6.5mn sheet which will increase to 12.5mn sheet). Greenlam has yearly capacity 12.02mn sheets. Stylam’s market cap is 1/10th of Greenlam

Disc - Invested.

4 Likes

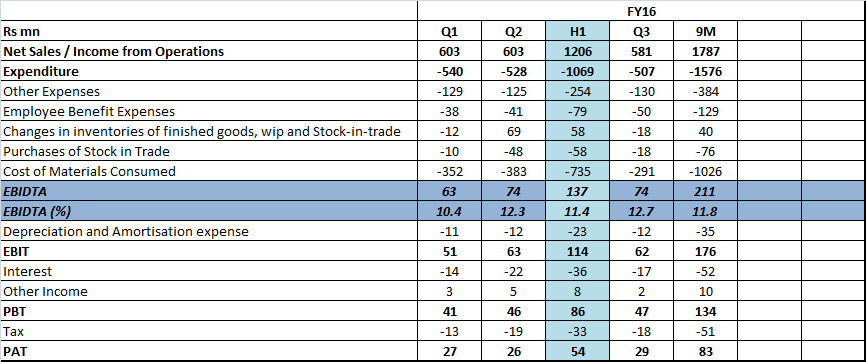

Stylam Quarterly nos table…

- Stylam trades at 13x based on 12m trailing nos…which is big valuation gap compared to peer with similar margin profile.

- Capacity will double to 12mn+ sheet ( by Dec 2015-March 2016)…which is as big as GreenLam in terms of production capacity.

It provides good risk reward given huge valuation gap and big capex coming up.

Disc - Invested

Before comparing with Greenlam capacity, please also compare the debt equity ratio then valuation gap is justified.

1 Like

I understand sir…hence said production capacity. Greenlam has the largest network and better ratios. My limited point is gap is very big…whether that gap comes down or not… market will decide over time

1 Like

dear investor,

i checked the credentials of stylam industries and found that debt to equity ratio is very high and also part of the promoter’s holding are pledged. in this context will the market be ready to give a higher p/e 12 to 24 months down the line. waiting for your reply.

thank you.

Sir,

I guess, Debt Equity should not only be looked at on a standalone perspective.

One should also try to see if the Interest is adequately covered by the operating profits and the repayments is adequately covered by the cash flows.

The TTM operating profit is 26 Cr while the Interest cost is 5.65 Crore.

It should also to be noted that a significant portion of the debt is towards construction of a building which is supposed to be rented out. And so the debt in the main business is not that high.

Though it is not good that they are using debt to construct a building. But Yes, If it gets completed by this Fiscal year, then maybe some rent should start coming in.

Besides, they are trying to enter domestic Markets (Earlier, They were Exporting more than 2/3 Of their Production uptill now) and it will require more working capital compared to their Export operations.

So the working capital may get stretched considering above points.

with regards to the Pledging, I think it has been there for a while now. The promoters have pledged 23.23% of their holding starting from Dec 2011. And it has been there constant. The march 2016 also has 23.23% Pledging. Not that it is good, but it has not increased that should also be looked at.

Regards.

Disc - less than 1% of the PF (Tracking Quantity)

1 Like

Dear Sir,

have you invested in stylam industries. and if yes what is your time horizon.

waiting for your reply.

thank you

Sir,

I have added the disclosure in the post.

Splendid results from Stylam

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/D4A77D44_E91A_4484_989F_82FC3F5A12EC_151420.pdf

But, balance sheet becomes more stressed.

1 Like

Good set of results by Stylam; revenue grew by 20% and profit grew by 75% in march quarter. Eps for march 2016 quarter is 5.26 compared to eps of 2.99 in march 2015 quarter. FY16 EPS is 16.60. With capacity expansion FY17 EPS can be around Rs 21-22.

Compared to its peers it looks undervalued, may be due to the debt and inventory levels on the balance sheet it is trading at current valuations.

Looking forward to the AR for more details.

Discl: Invested

Stylam posted excellent numbers. However, i am not comfortable with the debt level. Interest outgo is very low vis-a-vis its debt level, which means they are capitalizing the same.

I started this thread when stock was at 90, which provided a good margin of safety.

However, at current levels it should be watched out closely as it looks fairly valued now.

3 Likes

Hi,

From my talk on some Query, I think Management is responsive. And So, Members closely tracking this company may put up a Questionnaire, which would then help clarify all the doubts.

Regards,

Saket

Valuation gap with peers is narrowing.

Disc: Invested

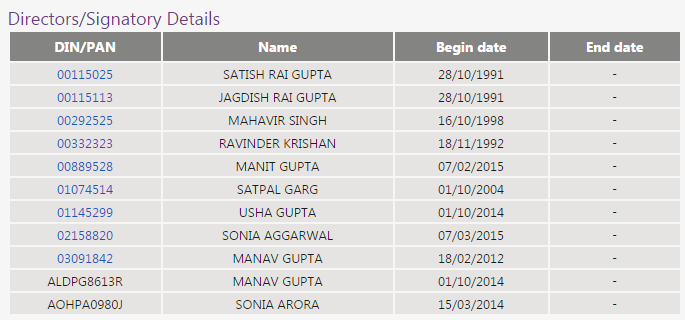

As per Shareholding pattern as on March 2016, a certain Manav Gupta holds ~4.9% shares in the company.

And there is one more Manav Gupta who is present on the Board of the Directors.

http://www.stylam.com/about/directors.html

Is there a way to find out if they are same person or different persons?

The Manav Gupta that holds 4.9% is listed in Public Shareholding group and not in Promoter Group.

So most likely, it is a different person.

Thanks,

Rupesh

Does Stylam, have any significant exposure to UK. If yes, then they might have to face Forex volatility. If hedged, then they will show gain, if not, then will show loss.

As per the data available in MCA, Looks like both Manav Gupta’s are different.

2 Likes

What a crazy move…

with today’s up move PE reached 30. Now there is no valuation gap… lets see how profits move up from now.

Disc: Invested at average price of 100