I am curious if anyone else is feeling this way, or if it is just me. I have been fortunate enough to achieve an XIRR of 34% over the past 8 years and 18% over the last 15 years in the Indian stock market. I should probably admit that most of these significant gains have come from a highly concentrated portfolio of less than 5 stocks, which I was lucky enough to pick.

However, I am now finding it incredibly difficult to identify new investment opportunities. Indian valuations seem quite high across the board, and I am struggling to find quality companies at reasonable prices. It is making me doubt if I can replicate my past success in this current environment.

Is anyone else experiencing this challenge, and how are you adapting your investment strategies? I would love to hear your thoughts and insights.

Echo the sentiment. Stocks which are producing earnings are priced to perfection and other set is just forgotten. Its a very stock specific market. Auto has entered in slowdown mode, property sales have started to fall, consumer is struggling due to low wages, high taxes and inflation. IT sector may see a major slowdown going forward, IT sector Job losses will spiral down whole economy. Govt is trying to extract most of taxes and this strategy is going to backfire in coming 2-3 years. Good is expensive and cheap is useless.

Though I agree to this analysis in part. I feel the market is very polarized and such times give us fantastic opportunities. To keep the post short let me give you example of two stocks.

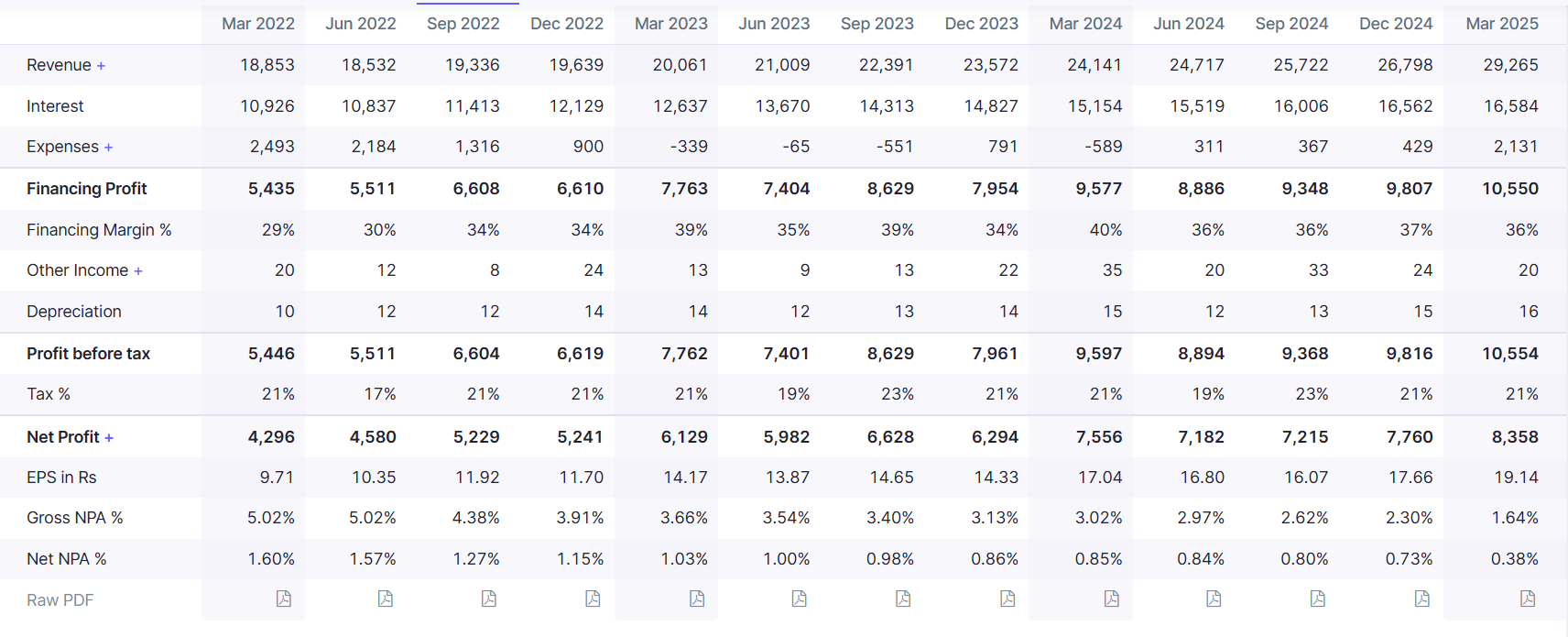

Please take a moment to analyze the following data and form your own opinion on their valuation. First image is the quarterly results over last 12 quarters and second one is the annual results reported over last 10 years. Please see the profit figures and come up with a valuation in mind. (I understand valuation involves multiple factors, come up with a valuation on the data given below.) The figures given below are in Rs Crores.

Profit for last 12 quarters

Over the past 5 years, both profit and dividend payouts have grown consistently each year. Over a 10-year horizon, the performance is even more remarkable, with consolidated profits increasing sixfold. The steady upward trend in quarterly profits over the last 12 quarters further underscores this robust growth.

Now, here’s the exciting part: this stock is available at a market cap of ₹1,35,000 crore, with a P/E ratio of less than 5 and a dividend yield of 4.5%.

For context both PFC and REC are trading at a P/E of around 5 and offer a dividend yield of approximately 5%. This stock has always been available at a dividend yield of 5 for last 5 years. Forget regular funds but you may expect such a stock to be found in every Dividend yield fund out there. Behold PFC is found in the dividend yield funds of only 4 actively managed funds (Out of 10 actively managed I could count) and its weightage is not more than 2 % in any of the funds. You will even more surprised to find that in some dividend funds its weightage is similar to Nestle (Stock which is at 70-80 PE and around 1% of dividend yield) or less than PVR Inox (which does not give a dividend). While valuations are influenced by many factors, a decade of consistent outperformance deserves greater consideration.

I don’t want to go into detail of merits and demerits of PFC valuations. This discrepancy highlights my key point: market polarization creates undervalued opportunities. Stocks like PFC and REC, with strong fundamentals and attractive valuations, are prime examples of value plays waiting to be seized.

Sometimes ..looking for value in your own portfolio holding stocks helps…

even if there is value in the stocks we have been owning from several years, we will avoid adding them because our earlier purchase has been at lower levels..

I would agree to a large extent, but value is also available outside the hot sectoral plays, such as Defence, Energy Transition, and QCom, as well as similar types of names.

Specific industrial names are not exactly at par value but available at decent risk premiums. Similarly, names are prevalent across the metal converter sector and the agrochemical sector. Pharma and NBFCs, there is value in some mid-cap and large-cap names. Specific Autos are at good buys if we are willing to hold for the long term.

There are stocks which are available at a decent valuation if you take into account the future growth in those sectors. For eg Defense, Railways and infrastructure will grow at a percentage more than other sectors. May be one can pick up the best performing stocks from these sectors. Besides this, there are values in some of the public sector banks for eg., SBI. If SBI starts demerging their subsdiary and come out with IPO’s, the value created by such action will be phenomenal.

Except that,

When you see the PBV over the years, its 0.6 and 0.7 over a 5 and 10 year horizon. Right now the PBV is 1.2. So its expensive against itself.

I have seen this with many PSU stocks, that they always sell cheap, irrespective of how well the business does. Look at Indian Bank or Canara Bank. You will find the same situation there.

Having said that, some of these PSU stocks were available almost free in 2019-20. From there, they have run up a lot. PFC/REC seem to be taking a breather right now.

Someone wrote that few of them (like NTPC) have there ROE capped at 15%. Why would that be, no idea. But these stocks are paying a PSU penalty for sure.

It will be pertinent to note an opposite situation in some of the non-psu growth stocks. If we look at these stocks, we find that they have always been expensive. Which means if we couldn’t buy them in the past because they were too expensive, we can’t buy them now also, and we won’t buy them in the future because some of these almost never fall too much.

I appreciate the viewpoints you presented, and I’d like to share my counterarguments and tell me what you think. Please feel free to share your thoughts, even if you slightly disagree with my perspective.

I’ll follow the same order as your points. First: Historical PBV of 0.6 and 0.7. This was when their GNPA stood at 5-6%, the Bankruptcy Code was either not implemented or not yet refined, and the power sector faced significant challenges.

The RBI regulations on classifying accounts as NPAs were also less stringent. Now, if a state government owned DISCOM delays payment beyond 90 days, the repercussions are far more severe. The state would face difficulties rolling over debt in the bond market or raising funds for associated entities.

I find it challenging to accept the comment ‘expensive against itself’ because so many things have changed. Base interest rates at that time were much higher, and the ROE of PFC was nowhere near its current level. Naturally, valuations were much lower then. Second: The curse of being a PSU. I disagree with this partially. Forget PSU’s in other sectors, within the same sector, we have IREDA and IRFC. Both IREDA and PFC operate in exactly the same space , primarily lending to the power sector. Yet, IREDA trades at nearly 4 times book value, and IRFC trades at over 3 times book value, which really surprises me.

The challenge for banks like Indian Bank or Canara Bank lies in their inability to grow deposits competitively and, consequently, their loan books.

This is not an issue for PFC or REC. Additionally, these banks do not offer dividend yields of 5%.

A well-run NBFC inherently has a higher likelihood of achieving better ROE than a bank due to exemptions from SLR, CRR and priority sector lending requirements.

I can identify fundamental reasons (based on first principles) why Canara Bank or Indian Bank should trade at lower valuations.

However, I have yet to encounter a fundamental issue with PFC or REC. I would welcome your thoughts on any specific risks you perceive in their business models. Third: (Future gazing.. I may be completely wrong here) I foresee a big threat to these very highly valued consumer companies. With the cost of capital decreasing and, more importantly, access to capital becoming more democratized, real competition is emerging.

The focus is shifting to which companies operate most efficiently and deliver greater value to customers, rather than who can secure debt at the lowest rate, as was the case previously.

I am sorry as this thread was regarding the general valuation of markets, I am may be being too specific about two three companies.

This is exactly what I was talking about when I said the expensive consumer names. Mind you , this is the valuation given to these companies with huge royalty payments as a percentage of revenue , not profits. I hope Indian fund managers and investors take notice.

There has been substantial increase in Direct Stock investors since 2000 to 2025. Also Mutual Fund investors have risen during the past 20+ years. Some times when large number of investors and mutual fund managers believe that, current high valuations are sustainable they continue to invest in such slightly over valued stocks. Sometimes, these trends can last for 5-6 years which seems to be the case.

During 2016-18-19 there was massive corrections in Mid caps and Small caps and valuations were attractive and that period can repeat but when is anyone’s guess. It can happen within next few years as well, and suddenly you will see investors not interested in the same stocks.

Markets are generally efficient but I guess, some times they believe that, they know every thing and this drives the prices to P/E of 50+ where an investor should be cautious. But most of the MNC companies often tend to trade at higher valuations due to general belief that their corporate governance is good. Why investors are not considering some other undervalued names ? Because they fear that they are trading at low valuations due to some known and unknown reasons.

Mid caps and few small caps are definitely looking overvalued and an investor may not find much value there as of now. She/he may have to consider some boring large caps for value investing as of now. This is actually an opportunity to invest in large caps. TCS has corrected from P/E of 40+ to 22 in last few months. Is it such a bad business ? May be No but investors are not interested in it as of now. Same is true for some private sector banks. Value investing often need courage to be a contrarian and this is the Test of an value Investor.

There is huge section of market (35%) which is fairly valued - Lending biz and large cap IT.

e.g. PNB Housing. This is trading at 1 BV with excellent growth and asset quality. Largest independent housing fin. Only event is CEO has resigned for better career opportunities.

At the same time people are paying 100 PE for some mid cap defence names which have little disclosure.

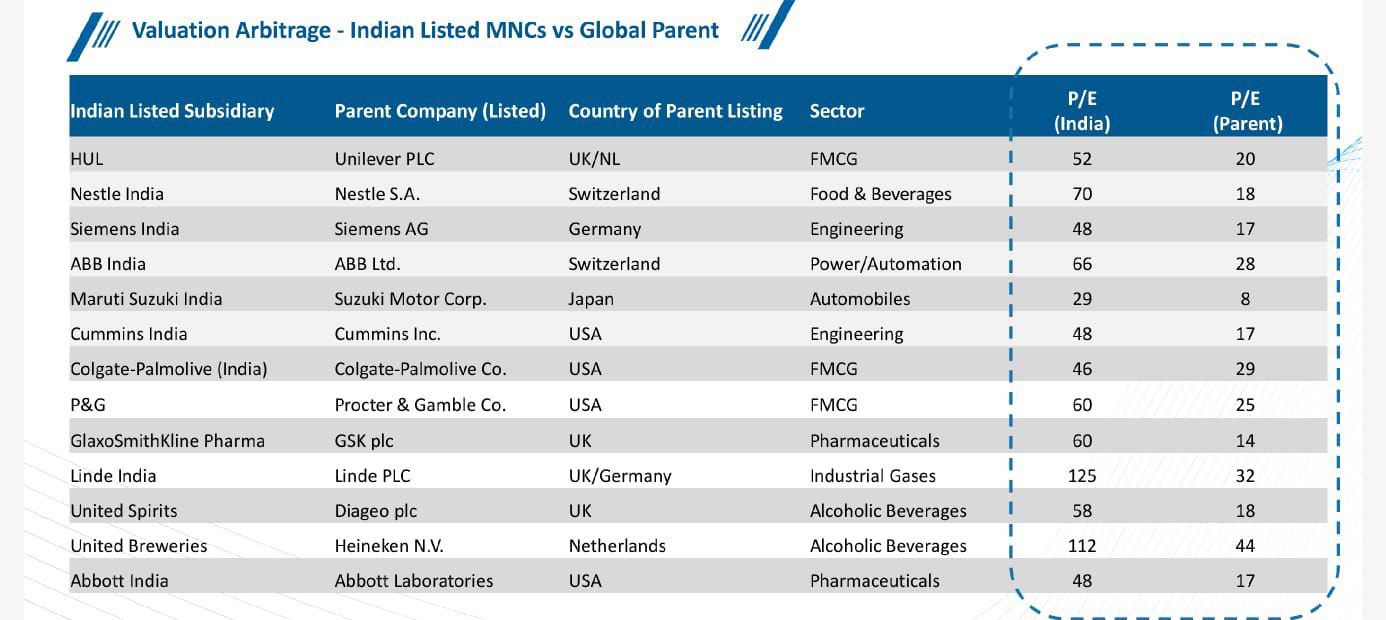

We also need to consider the growth rates of some of those foreign parent companies when making such comparisons.

For instance, Nestle S.A. had 89 billion revenue and 9.1 billion net profit in 2015.

In 2024, its revenue was 91 billion and net profit was 10.7 billion. It has registered flat-to-negative growth rates in the last couple of years.

Nestle India’s revenue and net profit have multiplied 2.5x to 3x in the same 9-year period.

But I do agree that at 70 P/E, Nestle India might underperform most benchmark indices over a long enough timeframe.

My point is that most companies in India have increased their profits and revenues by 2–3 times over the past 10 years. Even Reliance Industries has seen its profits grow 5 times. Reinforcing your point in a different way: India’s competitive landscape has transformed significantly compared to ten years ago. Such high PE multiples just for being an MNC, combined with a poor show in past 2-3 years, are unjustified in my view.

I agree with the originator of this post. Value is becoming v difficult to find. Sure, you can argue that some PSUs are undervalued. Could be many of these will provide good returns, but when that’s the only segment looking cheap… it does mean that the overall market is expensive…

Sorry for my delayed response.

For the valuation they are at, I still see tremendous value in PFC and REC.

I still have one or two issues with both.

For REC:

Bad Part: The loan book degrew QoQ. The management said it is because of repayment from the Telangana govt for the Kaleshwaram loan. The amount was around 13,000 Cr. If it’s a one-off, it is fine, but my issue is that their parent organisation PFC still has around 26,000 Cr lent to the Kaleshwaram project, and it was mentioned in the concall that they don’t see any issue with this account. The reason for this is not clear.

Good Part: Loan growth guidance of 13% maintained in spite of the de-growth in this quarter. So we have to watch out in the next few quarters.

For PFC:

Bad Part: I have not done the work thoroughly, but by rough estimates, the hedging strategy looks off at PFC. Total foreign-denominated loans for PFC are around 90,000 Cr. For the last quarter and this quarter combined, hedging losses reported were around 1,100 Cr. I don’t have any extra insights into their exact strategy, but by any measure, these figures look extremely large.

REC, with a similar book size, did not report such large hedging losses. PFC management in the concall has said there would be write-backs in the next few quarters, but it remains to be seen. They have been extremely vague in this part of the communication, and repeated mails to the investor relations team did not give any good answers.

Good Part: NIM and Credit Spread guidance maintained. Loan growth guidance still intact.

I just hope the managements become a bit more dynamic and increase the loan growth rates at PFC and REC. I feel both entities are too conservative and non communicative in a lot of areas.