Not really. They seem to be very concerned about the warning letter and working overtime to correct the oversight. They were also rather straightforward in accepting the slip up. “A blemish is a blemish” comment from Mr Arun is famous now. At the same time, any future adverse warning letters will impact valuations and also, any adverse observations for stelis would be a severe setback. As per Pharma compliance expert Mr Amit rajan: seee the section on biologics specifically: Pharma compliance issues - #14 by harsh.beria93

Mr Rajan was of the view that biologics manufacturing cant be done in India because we simply do not have the hygiene standards as a people needed for meeting the requirements of sterile manufacturing.

Any investor in syngene, stelis is taking a contra view. Something to be aware of.

pharmacompass is your friend here. You can search for any drug and get addressable market.

Thanks for adding your thoughts on the smaller molecules large market share. Looks worthy of investigating more at a granular depth for all the molecules.

Can you plz share your company primary source of this info so that i can educate myself and also come to the same page. I have not come across this anywhere until now.

But what does this mean? How does company know when it can win market share? Yes, Mylan and Teva are shutting down plants, and this serves as a big tailwinds, but if you see latest concall there is still pricing pressure and i am not sure they are able to maintain market share for all molecules. So clearly all competition is not going away, competition from India is not going anywhere as an example.

Key question is why other indian generic players are unable to do it as well. IIUC their algo is:

- File lots of ANDAs and stay prepared.

- As soon as there is a demand supply mismatch due to supply going away (eg: Teva/Mylan shutting down plants), they utilize their fungible capacities to enter that market and capture large market share.

Only question is why wouldnt other players that are not closing their plants capture the market share first given they are the well entrenched incumbents in this molecule’s market and strides is the challenger new comer.

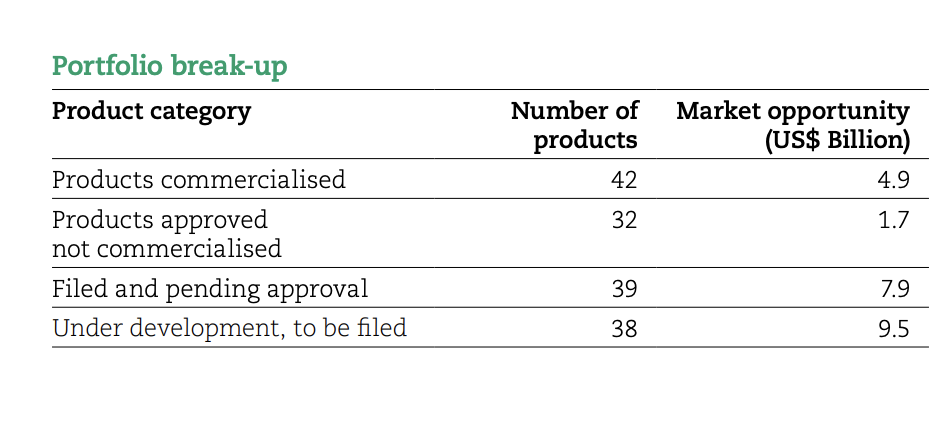

This is correct. At the same time 50% andas does not equal 50% opportunity. Some data here as of FY20 end

One key risk that all strides investors need to be aware of (this has already played out in strides once but still):

As a US facing pharma manufacturing co scales up in multiple manufacturing locations, it becomes increasingly difficult to enforce a common high compliance culture. Probability that at least one of the plants messes up and gets warning letter goes up linearly with number of plants and thus scale of the company. This is also why we see aurobindo get so many OAIs and VAIs. Please do read the compliance thread if you haven’t.