I started this thread to understand stocks that will go through temporary setback because of new developments in company, policy changes from government, changing public taste for products/services, increase in raw material prices or an X factor affecting the company’s performance.

Hope the investing community will educate us with daily happenings that will affect business performance of company, which will be either growth or degrowth.

Page Industries looks like a good candidate for this. Going through a sales downturn due to Auto Replenishment System implementation, and it can go up again once that is done

Thanks Abhishek. Heard the term Auto replenishment system for the 1st time.

As I come to know from the video, it’s a new initiative from any company to manage inventory system and will benefit the company after 1-2 quarters of pain.

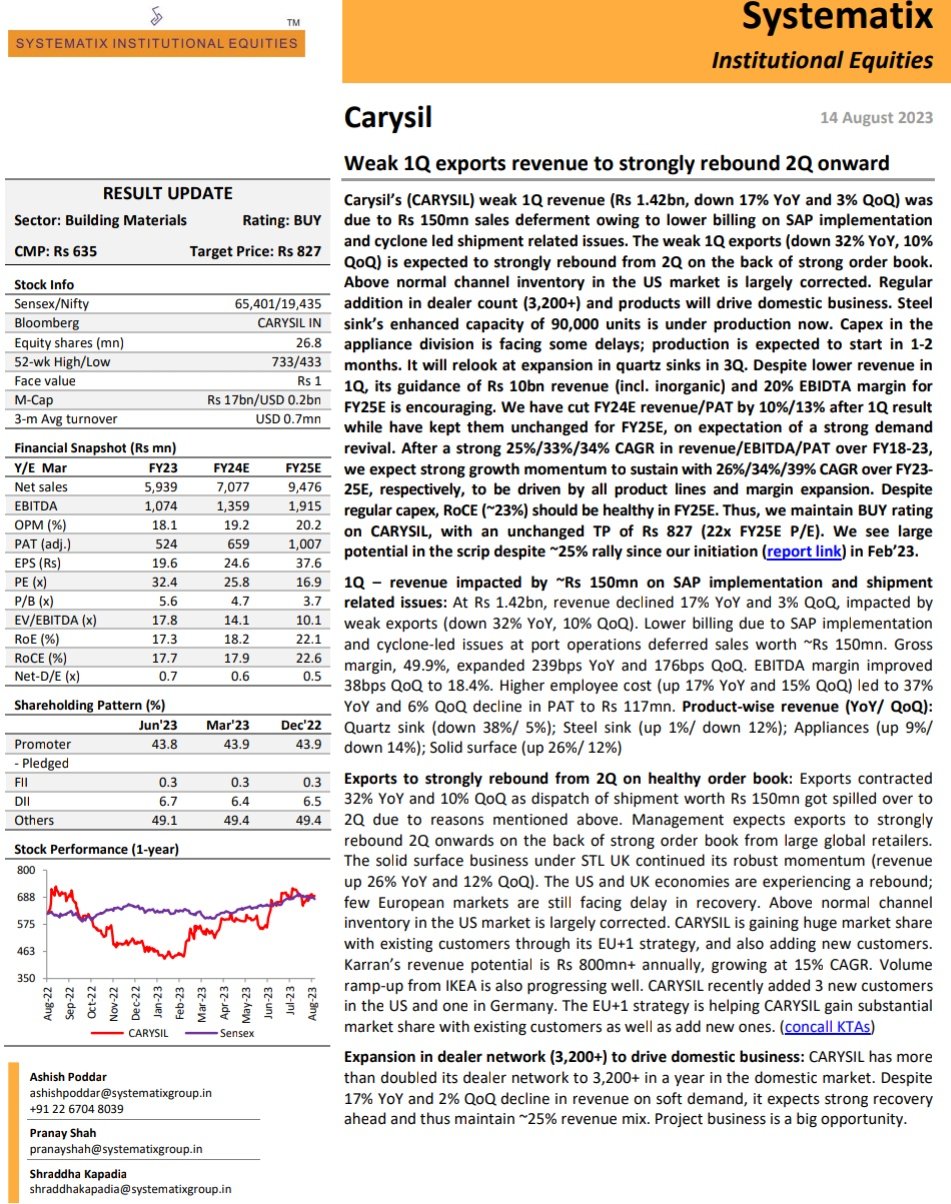

Yes…The company is guiding strong growth momentum and retains the guidance for FY25E despite the headwinds.

The SAP software will help Carysil to automate many of its manual processes, which will free up employees to focus on more value-added tasks. This will lead to faster processing of orders, improved inventory management, and better customer service.

More reference on SAP implementation on Google bard link here :-

Whole agro-chemical space has been facing macro headwinds due to excess production and supply by China at very cheap rates. I believe the sector will be sideways for at least two quarters.

UPL, Sharda Cropchem and Sumitomo to watch out for.

Hi everybody,

I think Biocon is a company going through temporary headwinds and has a good chance that it will come out stronger after this phase of consolidation.

Biocon has 3 business arms: syngene ( research and CDMO) , biocon biologics ( biologics) and generics

It owns 54% of syngene ( which is doing phenomenally well) and it has the same mCap as biocon…( talk about margin of safety)

Biocon biologics is proabably going to be listed in the next 2 years and is growing at 30% and has a good runway in the biologic space.By conservative estimates of private placement to serum india kotak group this part is probably valued at 15000 crores( 48% of current mcap of biocon)

The generic business is trundling along

The.present downturn is due to the ambitious take over of the biologics division of viatris and the resultant debt . However it will allow them to market directly to customers in the US .

Please share your thoughts