Makes sense

What do you think about additional fund raising at this point?

Makes sense

What do you think about additional fund raising at this point?

Sterlite Electric is a different entity i believe and was expected to be listed sometime back i guess and then the news died off

Ah! Thanks for clarifying. Yes there’s no new update on that ![]()

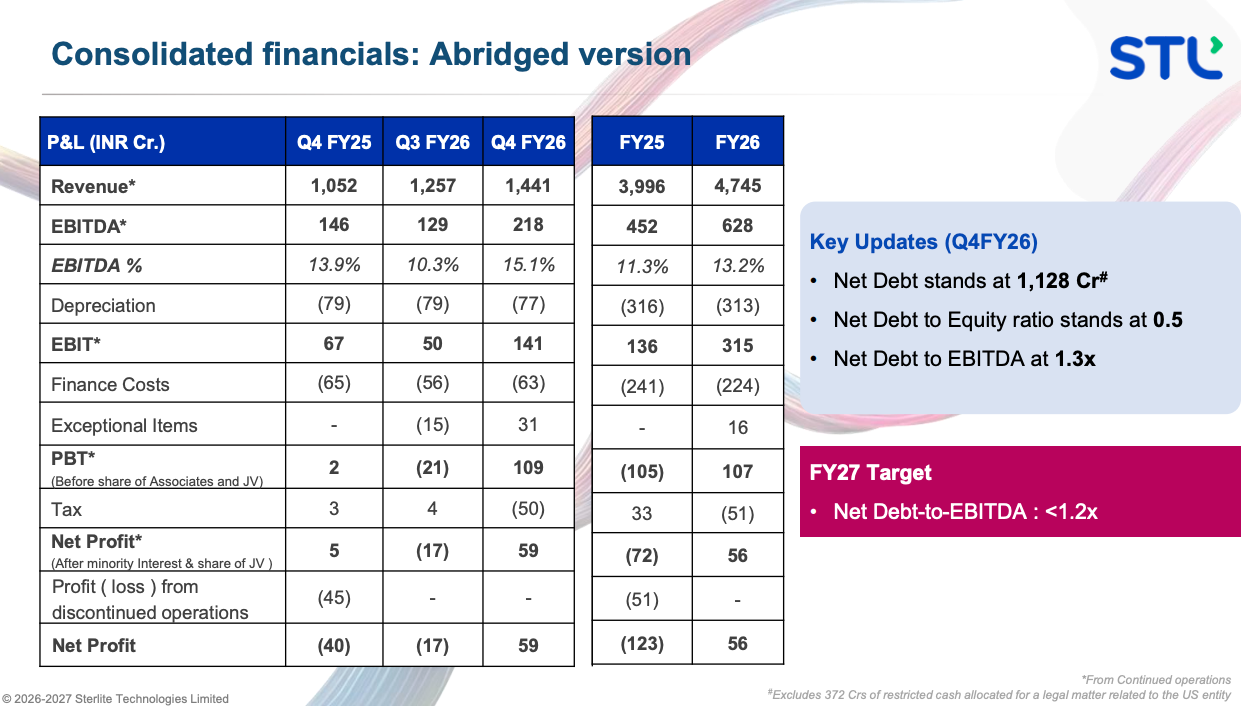

Sterlite’s Q4 FY26 results have been good and their order book has surged to 7,309 cr (67%)

From the earnings call

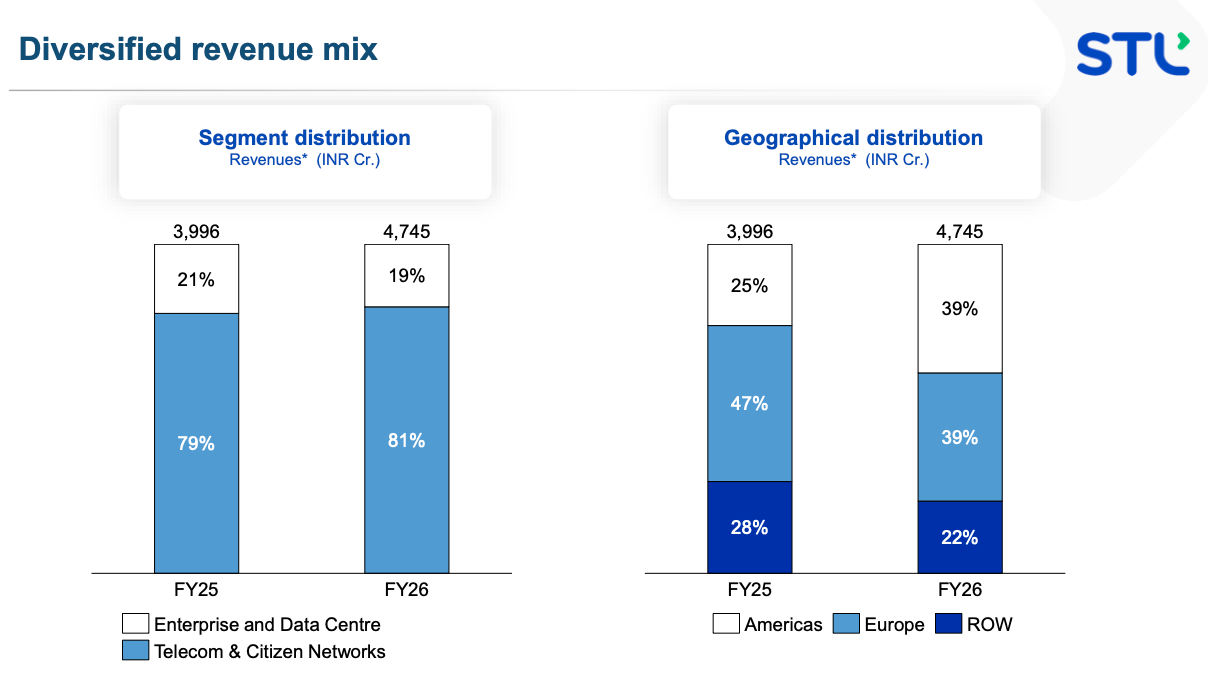

Their data center mix has dipped to 19% from the earlier 22%, which they explained: there has been a sharp acceleration in OFC revenues from telecom operators (like telecos in India and projects in North America like BEAD), and in absolute terms data center business has been growing. The management also mentioned that they are expecting it to be 30% in the current FY.

Regarding the fundraising of 2000 cr: This is a standard raise that they do often, out of which 500 crores will be for their data center products.

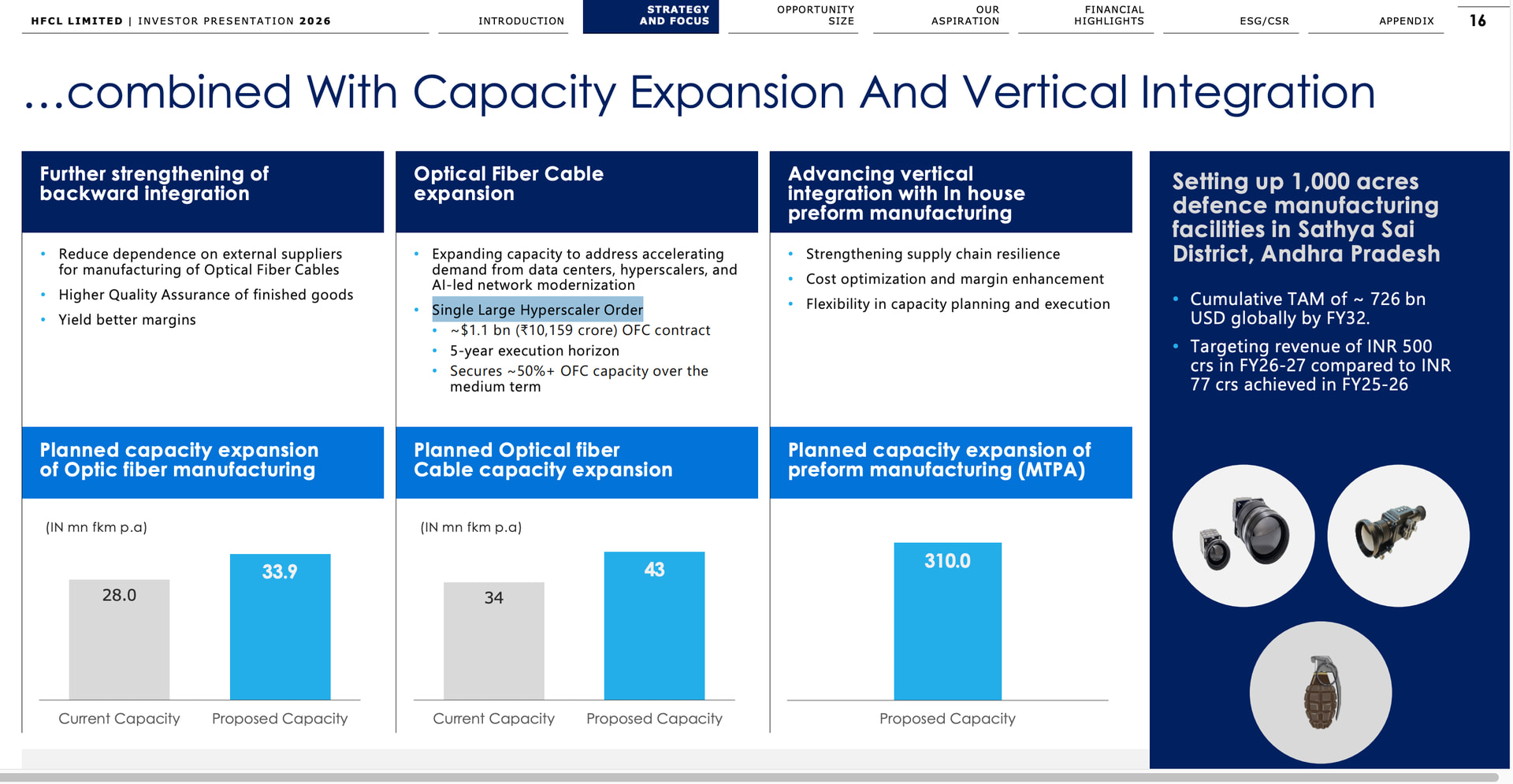

One interesting question was raised by one of the analysts, i.e., why STL was not scaling as quickly as their international peers and even local peers (should be HFCL) and if there was any “product quality issues” with high-fiber-count cables (1728 and 3456 fiber counts) which I guess is the one required by hyper scalers. (most analysts were trying to ask about this)

The management stated that none of this is true and that they were well positioned.

Well, HFCL and international peers have been seeing immediate explosive growth. HFCL has clearly got an order from a hyperscaler too, they have not mentioned who it is though.

Sterlite is definitely trying to bag such orders which is the reason why they have launched Neuralis.

OFC and their AI rally continues - Sterlite a 2500cr EBITDA Opportunity in making

YOFC - Rally continues ( Chinese leader )

Largest Optical Player - Market Cap - 20 lac crores.

Corning - Rally continues - Market Cap - 20 lac crores

STL - 3% of global market share.

Those wondering where it can stop ?

Just follow leaders - YOFC and Corning

It’s not only on leaders but as well as math

Let’s do the numbers as well -

FY27 - 7000cr - 20% Ebitda Margin - 1400cr Ebitda (Best case - 22%)

Fy28 - 8500cr - 22% Ebitda Margin - 1800cr Ebitda (Best case - 25%)

Fy29 - 10000cr - 25% Ebitda Margin - 2500cr Ebitda ( If cycle doesn’t peak Best case 30%)

For Sterlite it looks crazy but, Peak potential value roughly - 50k market cap

At peak - 20x on forward basis and finally will settle at 5 to 10x once cycle ends. Purely cyclical - Anil Agarwal knows how to play it very well ![]()

Nevertheless, I still believe this is a great acquisition candidate, where optionality can be immense ![]() ( Corning will be very much interested or any global player will be very much interested in this asset )

( Corning will be very much interested or any global player will be very much interested in this asset )

The argument that we should just follow the leaders (like Corning or YOFC) often overlooks the structural differences between a global leader and a smaller, localized player.

Comparing market capitalizations directly across different geographies and competitive landscapes is often a valuation trap. Leaders like Corning possess massive intellectual property portfolios, multi-decade customer moats, and diverse revenue streams that provide a buffer during downturns.

A smaller player like STL Tech relying on the same thematic tailwind may not have the same operational resilience if the industry cycle turns.

Atleast sell Half Qty is good when the narrative is at its peak, when industry analysts and forums are discussing limitless potential. When market participants start using terms like peak potential value, it often signals that the easy money has already been made.

In the our market, when stocks that have had massive, rapid runs hit a sudden reversal, liquidity can dry up instantly. If a stock hits its lower circuit of 5%, you may find yourself unable to exit, leaving you holding a position as the valuation corrects downward.

Never Forget The Infrastructure Supercycle of 2007-2008

(Disc: Booked 65% of my Postion, Holding Rest as of now)

Contrarily, there have been multiple scenarios where the run-up has continued and stock went on to provide multiple times returns in a short period of time because tailwind has sustained. If the industry tailwinds are there, returns are supernormal in a short span and booking profits early result in not capturing the overall potential of a winner. I think, continued strong momentum with no major tailwind issue should not be booked prematurely. If the story is genuine it mau retrace some percent but will not erase all gains and in continued momentum that reversal may happen at signficantly higher price point.

100% agreed. STL is in strong momentum and a turnaround story. It is advisable to track the stock based on daily time frame (10,20,40 EMA) for momentum and the same band for exit. If the stock breaches its 20W EMA, sell half as it is very likely that if the market believes that tailwinds are there - the stock is gonna reverse again making an all time high soon. Have seen this enough times playing out over the course of years that I have full faith in the above bands.

MAs are favourite tools/guide for exits. However, how reliable are these MAs in these illiquid T2T segment with 5% circuit limits? I mean when the tide turns you probably can’t get an exit at a price you want…

Exactly, History has shown that when the narrative surrounding a stock reaches a point of limitless potential and market enthusiasm is at its peak, the risks often become skewed to the downside.

we have to recognize that market cycles are often driven by sentiment, and having the discipline to take money off the table is a time-tested strategy to mitigate the impact of the inevitable, and often sharp, corrections that follow.

(Disc: Booked 65% of my Postion, Holding Rest as of now)

I am always apprehensive of investing in Anil Agarwal group of companies. If you go through their track record, you can understand. Whether it is Vedanta, HZL, Cairn , Sesa Goa etc. Coming to STL tech, I think it is time to be cautious. The stock doubled within 2/3 months. Even if the potential is there, it can’t deliver overnight. And it will take minimum 2-3 years to play out. And a lot of things can go wrong in that time. And I just came across news now that MOFS mutual fund has bought 36 lac shares. Such news shake your confidence on MFs. Why could not they buy @ 400 level 2 months back? Then what is the difference between lay investors and MFs? Even a lay investors like me could buy it @380 and sell@670. I will be circumspect in investing MOFS hence forth.

As per my experience, the more the market cap, the better efficiency of MAs irrespective of the circuit limits, because liquidity and free-float is what makes the price action more accurate and stable

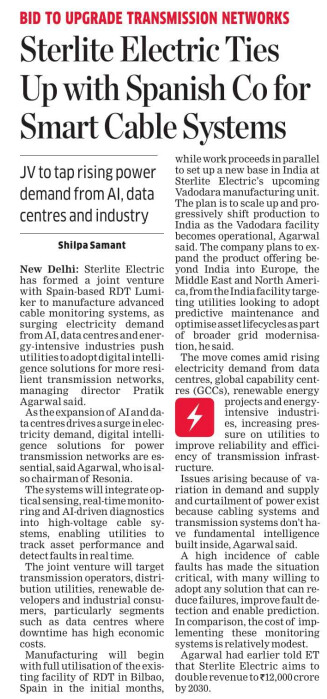

Article related to STL and other OFC players. Though its not clear about the affect on their earnings or biz specifically.