Is Any one tracking now this company , how do you see the Q3 Result

Fund raising was good for the company. But looks like funds are interested at particular price.

Business front:

Optical Fiber Cable prices trading much lower.

Sterlite will not do good for next year.

Triggers:

USA and Realisation should pick up.

1 Like

Scheme of Demerger approved by shareholders, secured and unsecured creditors. Any idea when the demerger will materialise?

I think around March / April 2025. The demerge share ratio is 5:1. Why the company is not getting profitable is the question.

3 Likes

3 Likes

With the demerger, expecting the optical networking business to do well. Overhang of high working capital requirements gone, and high customer inventory appears to have been exhausted. Credit rating should improve reflecting improved balance sheet and business prospects.

Additionally expecting the demerged entity to list at 24+ based on rough back of the envelope valuations of ~ 1x P/S typical of average B2G EPC businesses. Anything more might be a jackpot. I could be wildly off in my estimates and assumptions though.

I have bet approximately 50 percent of my portfolio on this company pre demerger at average price of 122. Took a risk based on my risk profile.

Consume this information at your own risk.

3 Likes

This entire management is not concerned on cashflow generation just merger vs demerger. Extremely horrible management. Is this how you run a company?

2 Likes

When will the demerged entity be listed?

Be aware of this fraud company and invest at your own peril. For that matter, it is applicable to entire Vedanta Group. You go through entire history of this group for last 10 years and every thing becomes crystal clear. Anil Agarwal has never given anything to investors in general and retail investors in particular. What is happening in this group is mind boggling. So many mergers and demergers that one loses track. At one point the original company was delisted from India at peanut valuation. It got HZL at throwaway price and is still looting it. It has declared dividends to benefit Vedanta and for making debt payment. Even now it is heavily in debt. So my request to all retail investors is to avoid this group or make proper study.

In my opinion this is the worst management amongst all big corporate houses in India.

NB- I have sold my small holdings in HZL. I don’t have any vested interest. What pains me that so many big pundits and analysts have not raised any issue on this management.

4 Likes

The timeline of the demerger has been delayed for Sept 2024 to September this year, and given the current situation, it is not certain whether it is still possible

1 Like

EBITDA stood at Rs 140 crore, up by ~94% YoY, led by cost optimization and operational efficiency. As on 30th June 2025, the company’s open order book stands at Rs 4,888 crore. They remain confident that improved capacity utilization will drive enhanced EBITDA margins, thereby supporting the overall profitability.

Disc: Invested

3 Likes

Still waiting for the demerged shares to be listed. Been 4 months since record date. One thing that the company doesn’t disappoint on is its failure to adhere to its own timelines.

I have exited my position in STL tech at average of 126…. Mostly because of how their promises don’t translate to outcomes. Even if this does do better going forward, I will save myself the anxiety of associating with an unreliable management.

3 Likes

Final information memorandum dated Aug 26th uploaded on Invenia website under investor relations.

Also includes the FY25 results of STL networks. Neither published at stock exchange filings of STL tech.

3 Likes

https://inveniatech.com/wp-content/uploads/2025/08/Final-Information-Memorandum.pdf

Update- STL networks will be listed on 4th Sep 2025 according to exchange circular.

1 Like

Sterlite Technologies and HFCL

Concall must be read. Cycle might be turning here.

Very interesting

Sterlite is sitting on operating leverage. Once revenue kicks in margins will expand.

Disc - Invested

3 Likes

Yes, HFCL Management. Said OFC revival is a multi-year opportunity.

STL TECH - 500 CR Fund Raise at 110/- ( When Anil Agrawal puts money, you know Industry in Tailwinds ![]() )

)

Finally time has come for STL !!!

7 Likes

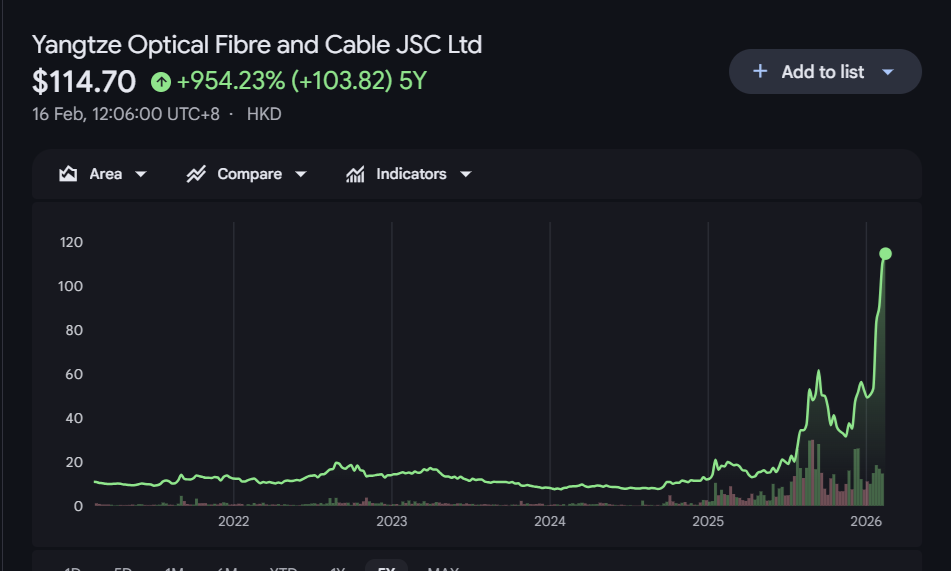

OFC Global Peers and Their strong runup over last year

Firstly margin of safety at CMP are too thin for Sterlite Tech, better one should wait for right entry points closer to management has added position Rs-110/- , rather than jumping in momentum.

**Coming to THESIS pointers**

DATA Center demand will push the prices up for OF AND OFC. Stock Price has already shown momentum across the OFC space.

Many are touching DECADAL highs.

But note as of today - Still the demand is for specialised cables wrt AI not every OFC is going through demand rush, but it might change in upcoming months that’s how commodity cycle will play out.

Checkout this video on Coming growing 20% YOY at such a large base talks about their AI division growth →

Corning is the leader in this space → USA

Prysmian → EU Leader

Fujikura → JAPAN Leader

YOFC → CHINESE Leader

STL Tech → India

~ DYOD

2 Likes