Is it worth staying invested in this company considering recent fall and bad results?

1 Like

this might help with your decision.

https://www.icra.in/Rationale/ShowRationaleReport/?Id=111470

The company is also contemplating raising equity funds to reduce borrowings and fund its growth plans

3 Likes

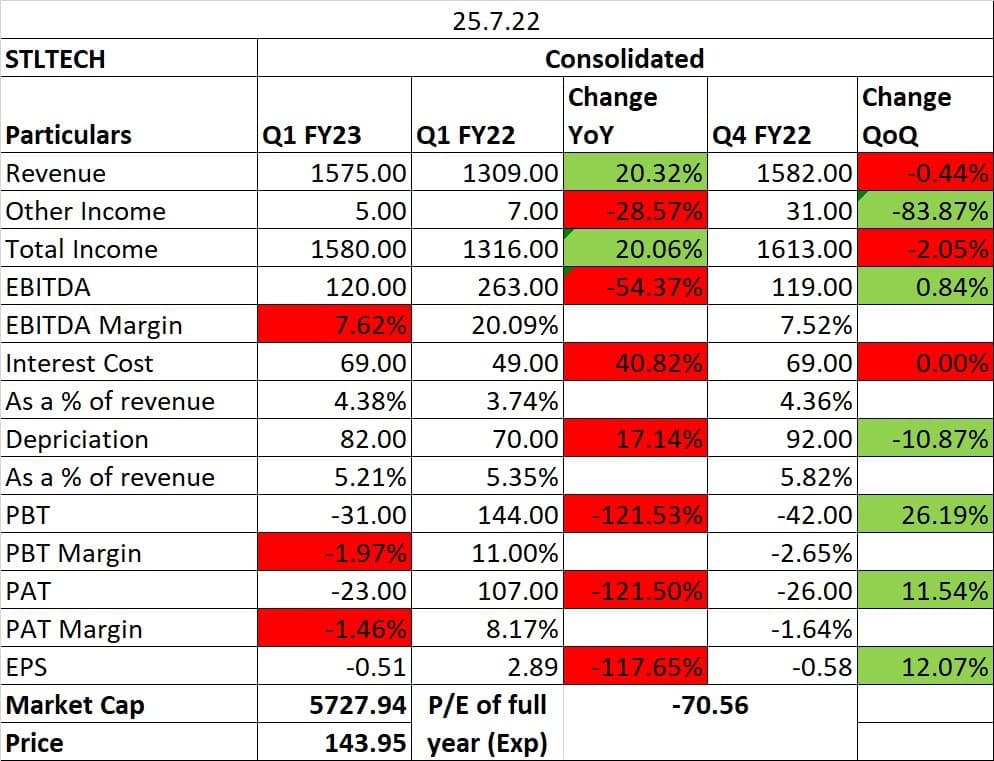

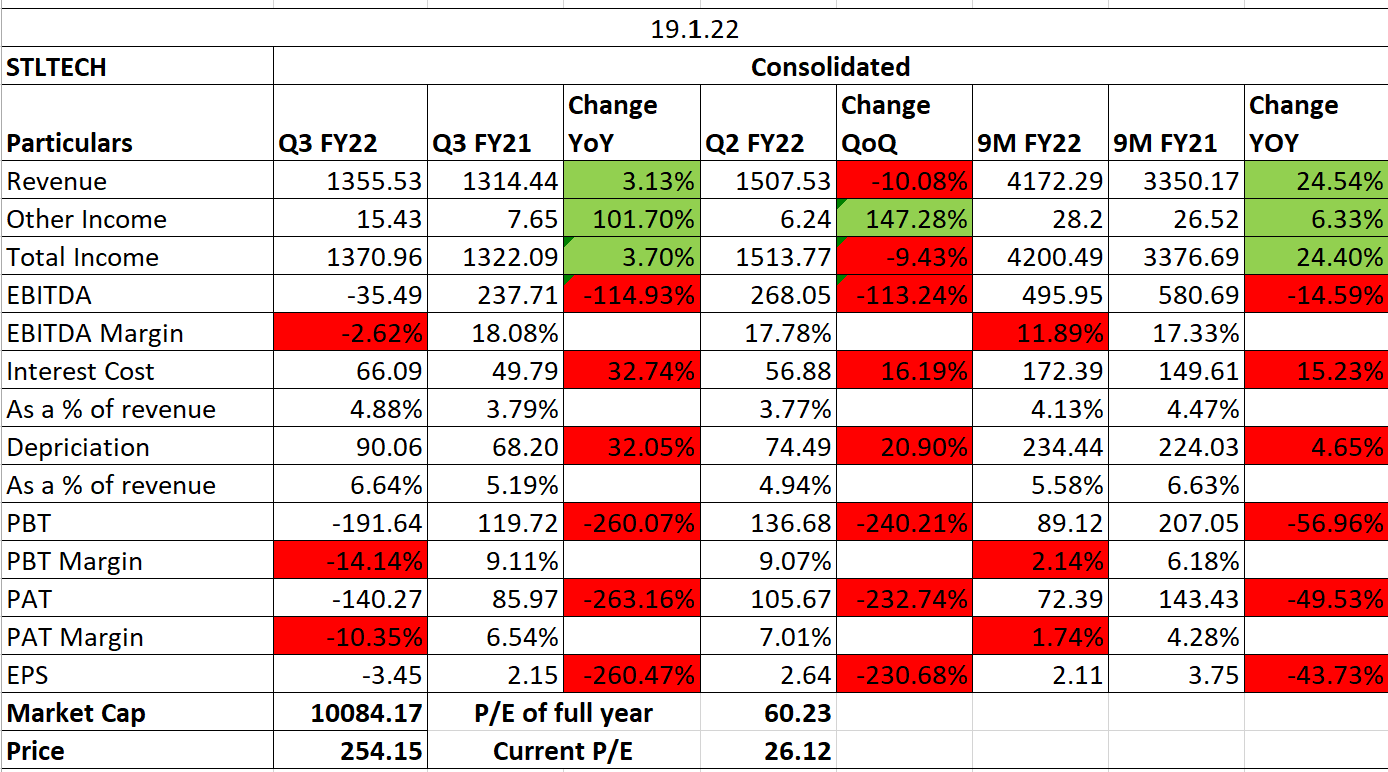

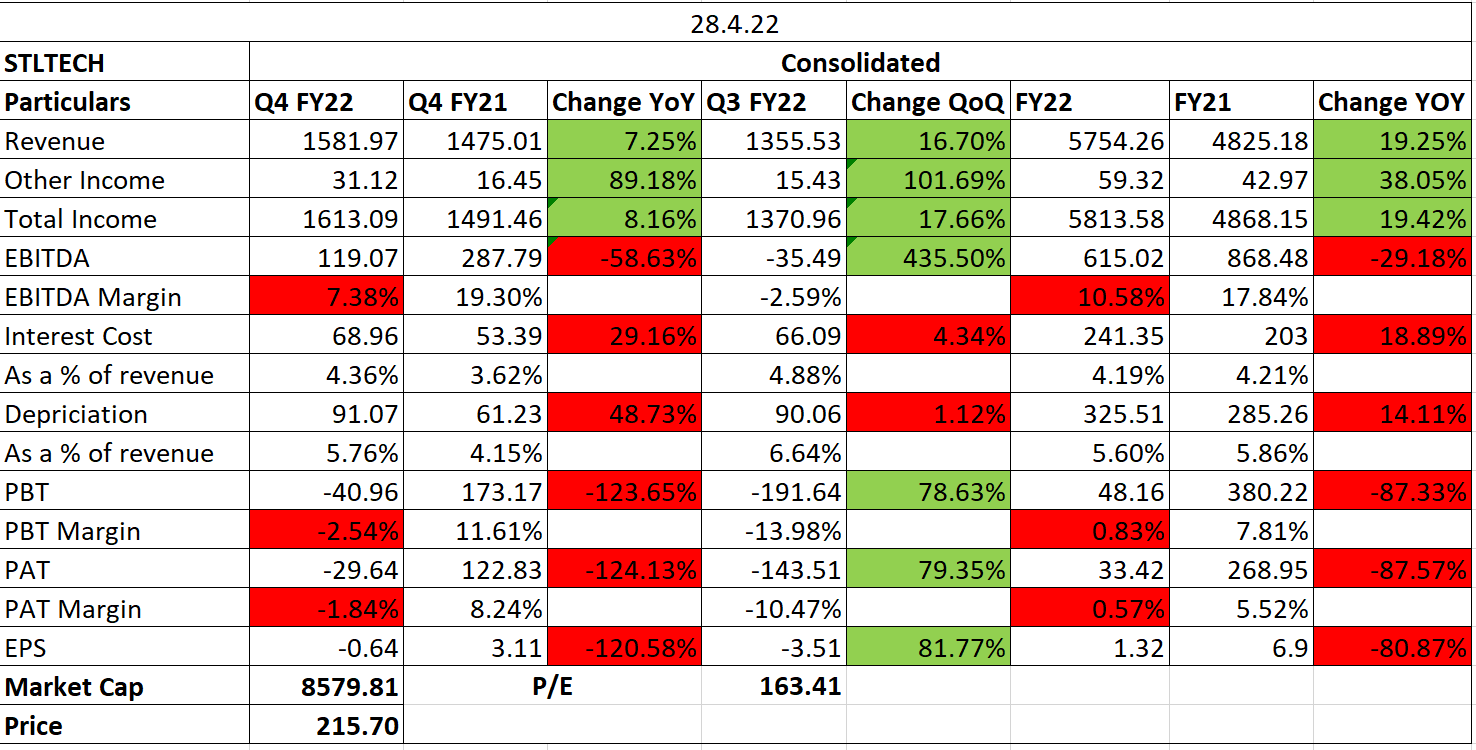

The company has been continuously guiding for 10000 crore topline and 1000 crore bottom line for the whole of 2020 and till Sept 2021.

The results are just not in line. Kuch toh gadbad hai Daya!! ![]()

![]()

4 Likes

Yeah, ever since I’ve started following them in 2018, multiple long shot goals like $1B revenue, doubling revenue in 3 years etc., It’s very difficult to do scuttle-butt as it’s a B2B company.

But, looks like the industry has a lot of growth ahead and Sterlite tech does have differentiator technology and services.

Their sudden Q3-22 restatements were surprising, but in hindsight seems they had (have?) huge problems agreeing with Indian customers their work is done (sign-off) and getting invoices paid and if paid at the quoted rates. They’re taking an year from Q322 till perhaps Q4-23 to reduce India dependence (unless it’s private sector) and increasing UK/US business.

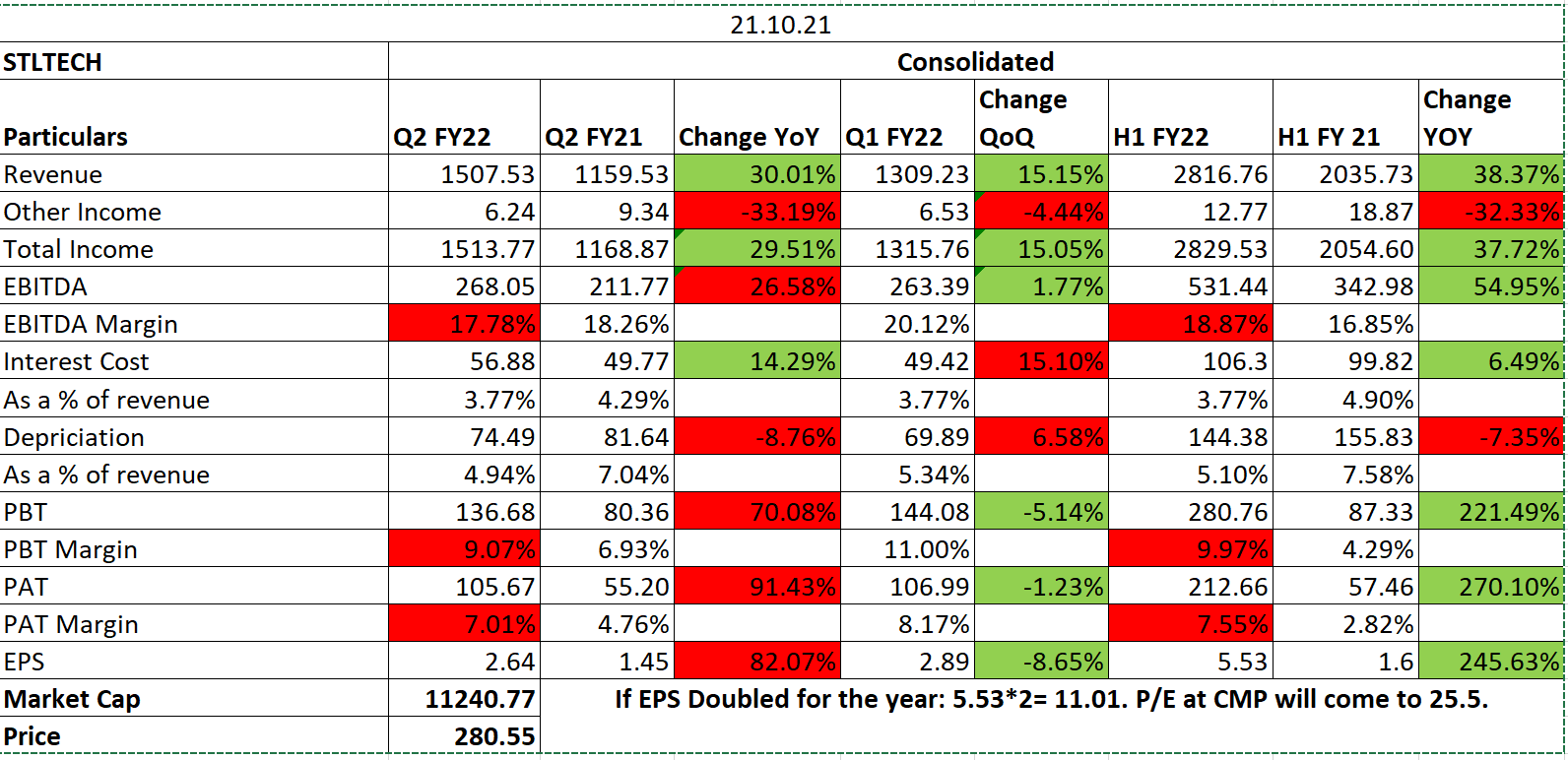

To give them credit, they’d communicated both revenue/profitability hits till Q4FY23 or so right during their Q3FY22 call, but it was too late to sell at then recent high of 300 ![]()

I booked a small partial profit at 190 but still largely invested from early 2020 levels and watching closely to add more.

3 Likes

I was and still am extremely bullish on fibre optics and connectivity solutions. Presently I am (wait for it) 45% (~10L) down on this stock after having been positive for a few months last year. Didn’t exit at the point of Q3 write-off’s thinking it will eventually get compensated by the market share grab in US/UK and subsequent quarters of profitability. Promoter track record is the only (and probably the worst) concerning aspect. They seem to be getting into more value added products and I’m really intrigued by the tons of patents that are getting granted (hope those are verified claims) and how it will help sales / margins.

Some of the other purchases alongside like RajRatan, Avantel, Page etc are growing like crazy and there have been disasters like Muthoot Finance & IndiaMart.

So the question is how do you handle such a scenario from a portfolio (~25 stocks) point of view. I’m just at around 1.5% in red maybe. When such a stock gives mixed signals, do you cut the losses and redistribute whatever is left or considering the pain has already been inflicted, stay put and hope the recovery wouldn’t be too slow.

3 Likes

After their recent results I was expecting stock to drop lower, but it came back today. I just cursorily verified their patents at Google scholar Google Patents. Not a big fan of patents, but they seem to have world class capabilities in fiber and fiber-connect. Service org also seems to be ok, led by an ex-TCS guy and talking in “resourcing” language. Not a great differentiator in my opinion, but a good support org which has been scaled well recently. Better than having likes of ITES companies as partners for this kind of work.

I was thinking stock would drop a lot from 140+ levels going by recent results, but I also strongly believe one can never time the market. I’m confident about the company’s fundamentals and capabilities though, but vacillating if US/EU recession will affect their business. Reading other OF companies for business outlook.

4 Likes

The stock is trading at around 35% higher compared to July 27th levels (last discussion). Does the recent jump have anything to do with the news around Vedanta’s semiconductor foray? Are there any synergies to be expected?

Any other info on new orders won or signs of higher demand in Indian market with the deployment of 5G that could prove beneficial? IIRC, they had claimed to cancel some of the lower margin orders in favour of higher margin ones.

Is the EU/US economic recession likely to affect international demand in a significant way or the current orders are likely to help them tide through.

Q4 FY 23 Results are looking good, why this company stock prices are not moving

what are the negative factors about this company

Can any one point out bullish and bearish about this company for near term and long term view

Sterlite Tech:

Future relies on below 3 things:

A] USA Business shouldn’t tamper (Currently companies sitting on inventory, so from H2 needs to be seen)

B] Software Business should show growth (5 years+ ) - Currently starting

C] India Services Business- Currently loss (High fixed cost) new orders should pick up. (Demerger)

Failure Thesis:

A] USA going in down turn.

B] Software Business again in failure trajectory.

FY24:

Cashflows should be improved (Capital Employed in the services, will be reduced )

Slowly they will reduce debt, will not be significant.

1 Like

Sterlite Technologies Limited Q1 FY24 Earnings Conference Call Transcript July 27, 2023 [Rephrased for my understanding]: Source

-

Based on current US OFC industry situation, new revenue guidance is growth of 7% to 9% % [was 10 ~ 12% earlier] while targeting net debt to EBITDA to be at 2.5 times.

-

CAPEX: Last year about 400. This year talked about 350, 400, but looking very closely at net debt, EBITDA, etc. Want to make sure that generate cash as a business and then reduce our debt.

-

Optical Network: Working capital-light but more CAPEX-heavy, needs more investment in the manufacturing. Grow the optical business by increasing OFC market share and the connectivity attach rate. Engaged a tier-one management consulting firm to further optimize our operating costs. The 5G deployments continue to remain strong globally. Also, fiber-to-the-home deployments continue to remain strong. The Biden administration has recently announced the distribution of funding of over $4.2 billion, the BEAD program. The funding shall be used to primarily deploy last mile fiber networks. The funds expected to flow to states early next year and shall start to fund projects by the middle of 2024.

- North America: High channel inventory. Depletion will still take 2~3 quarters, Slow deployment by the operators, and higher interest rates and inflation.

- Optical fiber interconnect business: Underestimated the cycle of development and approval. In trials with various customers. After successfully passing this trial phase, expect good volumes. Invested both in the product development as well as the team development. Also, at the customer end, adding resources who are very comfortable with this product portfolio. Expect improvement in sales by Q3, Q4 and certainly into next year. Margins on interconnect are closer to 30%.

- US operations helps in terms of branding and positioning. Ensures quick service to the customers.

- US quarterly revenue dropped from 750 to 450 Cr. in Q1FY24. By when old run-rate possible? Not sure. It is a function of both volume and realization. Could have some reduction in realization. Putting our all the efforts to ensure that we are at this kind of a margin although we may have challenges to make the volumes. If realizations are at the current level, overall margins shall improve.

- China Mobile has announced the results for 2023-24 tender. The tender volume is 108 million fiber kilometers. The tender war might mitigate any price risk that we see out of China in the near term. In addition to the China Mobile, China Telecom has also announced a tender of 50 million fiber kms.

- In the short-term global OFC demand contracted by 3.4% in H1 2023, particularly in North America, demand contracted by 11%. Strongly feel that new products in the connectivity business should see a jump in attach rate from H2’24 onwards.

-

Global Service: Working capital-heavy. Do large scale deployment of networks and system integration. Expect BharatNet phase-III tenders to be released in second-half of this FY. That will be a large 3-4-5 year, execution and then maintenance of that going forward. Consolidate global services, build new capabilities for value added services, and improve the UK operations profitability. Would be demerged by end of next FY.

-

Digital: Acquired new customers in the US and India across technology and service industry verticals. 20 plus active customers at the end of Q1 FY24. Delivery team scaled to 950 plus consultants. Open order book is at 900 plus crores [3~5 Yrs. duration]. Focus is to make the business breakeven by Q4. Build the digital business through focused investments in new technologies and capabilities.

2 Likes

I have almost losen hope in sterliite technology. I have buyed @230 rupees. My original thesis was that 5G deployment will enhance the optical fibre demand manifold times and in this anticipation I brought this share. That time I do not know about the cyclical nature of optical business and in fear of missing out I bought at much higher level and finally getting averaged @230. This always reminds me of my mistake of buying cyclical stock at peak margin. I think that why people say, Market is very expensive teacher.

2 Likes

This stock is not suitable for long-term holding due to below aspects:

-

Revenue and profitability growth from its major and most profitable vertical (optical network, contributed ~80% of the total revenue in FY23) depends upon two factors: volume and realization. In turn, business must balance the below aspects:

- Unavoidable Debt for upfront capex to achieve the volume growth.

- Persistent margin pressure due to commoditized product - Price realization is market driven as end consumer cares only about the service from the network instead of the product that enables the network.

-

Usage of the cumulative cash flow for the periods of 10Yr. and 5Yr. makes it clear that business is least beneficial to the equity shareholders, particularly retail investors (promoter takes a regular paycheck in the form of opex). After taking care of Lender, Capex, WC and taxes, only ~5% of the cash flow reaches in the hands of an equity shareholders in the form of dividend with an ever increasing debt. Here are the numbers :

| Usages of Cash | 10Yr. | 5Yr. | |

|---|---|---|---|

| Direct taxes. | 6% | 8% | Government |

| Working capital changes. | 9% | 15% | Customer |

| Fixed assets purchased. | 41% | 36% | Supplier |

| Repayment of borrowings. | 24% | 20% | Lender-1 |

| Interest paid fin. | 16% | 14% | Lender-2 |

| Dividends paid. | 4% | 6% | Investor |

| Sources of Cash | 10Yr. | 5Yr. | |

|---|---|---|---|

| Profit from operations. | 45% | 54% | |

| Proceeds from borrowings. | 55% | 46% |

7 Likes

I guess,

Recent anti dumping duty on Optical fibre imports is beneficial to Sterlite Technologies Ltd

4 Likes

Fundamentally, yes. It will add to order book and subsequently revenues in coming quarters. Also its creates a good positive news for the stock since it has been ignored like nothing else. Technically, it is at a tested and retested bottom of 150-ish made over past 1-2 years, and just waiting to start in this bull market.

1 Like

Hello Mr. Surender,

Have you had a chance to study HFCL ?

If yes please share your thesis on that stock as well.

Thanks

Sterlite has data Center business.

Anyone has details about this

Pls share

Broke a long term bottom. Exited

2 Likes

India’s Sterlite Technologies develops world’s slimmest 160-micron fibre.

Please share your thoughts on new development, as stock touches 52W low.

https://twitter.com/business_today/status/1718164426451275973?t=LUUMoNtcPDa8JnLejzwsVw&s=19

1 Like