I see very Similarity on Sterrlite stocks Price movement & Graphite Stock Price movement. Both Stocks rose on the premises of shortage of the OFC/Graphite and both are falling now as we have Oversupply now and Prices of OFC/Graphite is falling sharply, so is the stock price and same reason for fall oversupply due to china

The Q2FY20 presentation has some interesting slides

-

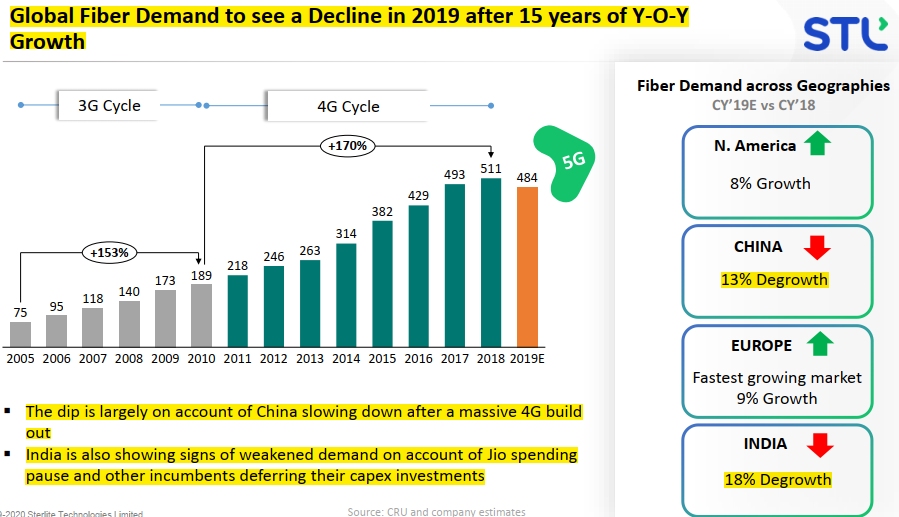

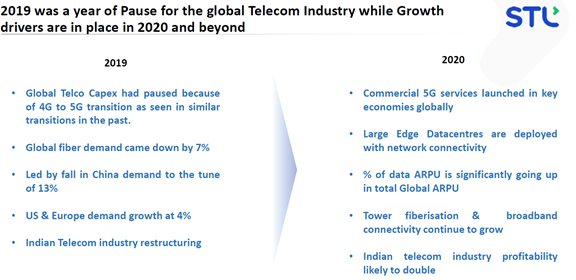

Global Optical Fiber demand has reduced after more than a decade

-

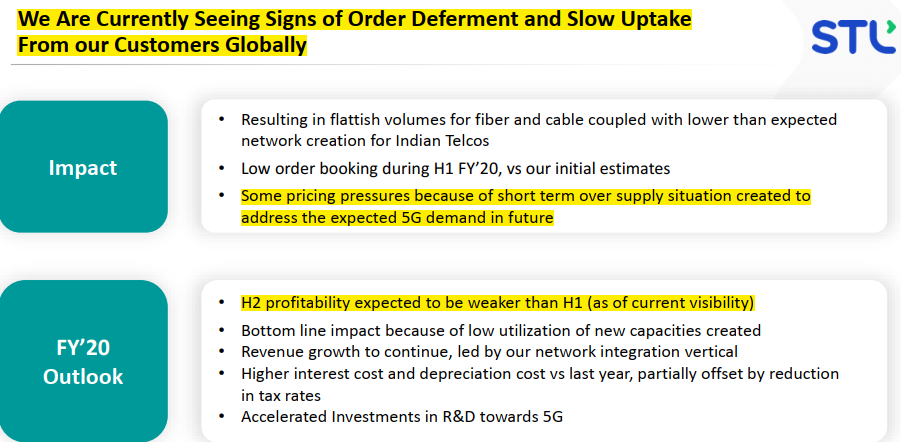

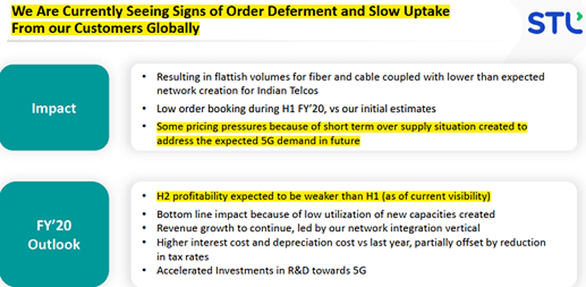

There are cases of order deferment, price reductions

2 Likes

Except earnings have increased for Sterlite and they have fallen by 4x for Graphite. ![]()

Sterlite is selling everywhere while Graphite cannot defend their own home market without ADD. ![]()

After 15 years of non-stop growth, even during 2008, somethings need to take a (small) break ![]()

good video to learn about 5g… in simple terms

ted talk

I have put Sterlite Tech on my stock watch list after reading the above posts. No management issues (I didn’t read every single post) and it is undervalued according to DCF analysis as well.

I’m now waiting for STRTECH to signal an entry on monthly RSI charts.

I’m just a remisier and my main job skill is website theming so I do not have a license with SEBI for stock recommendations.

Sterlite Tech. AR & Q1 FY20 Imp. Points!

https://drive.google.com/open?id=13p9F0_gT0YoOLV-eEeowoXsFRQyjlt0S

Prepared by E-global Group of Companies!

https://www.e-global.in/

(Will Update Q2FY20 soon)

(Disclaimer: Not an Investment/Trading Recommendation)

2 Likes

Sterlite Tech. Q2 FY20 Result Update!

https://drive.google.com/open?id=1JWLISM1GhTH2zo-ma_PLDaM20-vO2Vz8

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

1 Like

Overall good feedback from rating agency.

Some of the key points captured from notes:

Pros:

- Market leader in the domestic Optical Fiber (OF) and Optical Fiber Cable (OFC) market - 45% Market Share

- Increasing market share in export markets - 7% Globally

- Increase traction in European market post IDS acquisition

- Entry into few larger cloud service providers globally through IDS acquisition

- Increase traction in in 5G - 10 million 5G subscriptions are projected worldwide by the end of 2019

- Geographically diversified revenue mix - ranging from telcos, government agencies, private organizations and cloud companies

- Covering entire spectrum of telecom products starting from preform manufacturing to software products for network integration with digital intelligence

Cons:

- supply overhang issue in the near term will pressurize profitability

- Persisting low offtake from China could impact realizations going forward

- Elongation of working capital cycle due to increase in share of services business

- Any delay in receipts(especially in services business) from the counter parties could impact the company’s liquidity position

3 Likes

Stock may get boost from https://www.livemint.com/industry/telecom/govt-may-impose-25-safeguard-duty-on-imports-of-single-mode-optical-fibre-11573173269061.html

Supply to China is very less of total portfolio.

1 Like

Sterlite Technologies in partnership

with Cognity, a leading European systems integrator, announced signing of a multi-year, multi-million dollar

strategic digital transformation agreement with Telekom Albania, the first mobile communications company in

Albania.

Details are available in link:-

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e072edc3-c3f6-4f04-8b28-3f46dad38260.pdf

2 Likes

Throughout the FY19-20 annual report the management talks about working with big cloud players. For example, see an excerpt from page 6:

"As the data ecosystem expands across the value chain,

Cloud and OTT players are heavily investing in network

creation for massive connectivity. With expertise in

design and deployment of high-capacity networks, STL is

now a technology partner to two trillion-dollar global

Cloud companies, for their hyper-scale data networks. "

Does anyone know which trillion dollar companies does sterlite technologies work with, and the specifics of the contracts?

1 Like

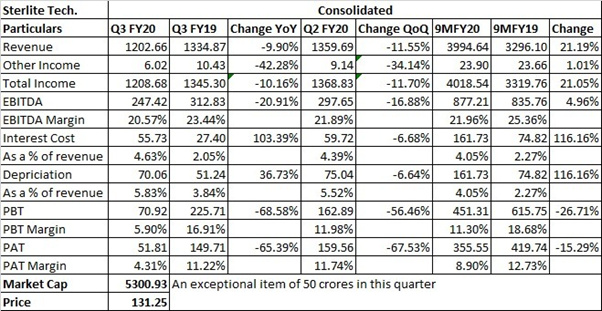

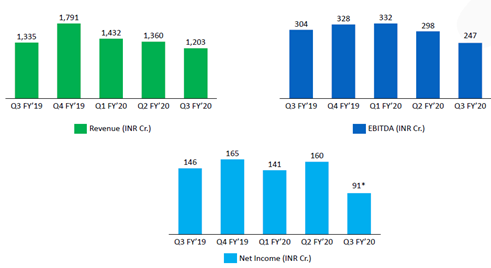

Results (Q3 FY19-20) - YoY Comparison

The company has reported net sales of Rs.1208.68 crores during the period ended December 31, 2019 as compared to Rs.1345.30 crores during the period ended December 31, 2018.

The company has posted net profit of Rs.52.63 crores for the period ended December 31, 2019 as against Rs.145.60 crores for the period ended December 31, 2018.

The company has reported EPS of Rs.1.29 for the period ended December 31, 2019 as compared to Rs.3.59 for the period ended December 31, 2018.

2 Likes

Sterlite Q3 FY20 Results!

Q3FY20 IP:

Q3FY20 CC:

- Future Statements:

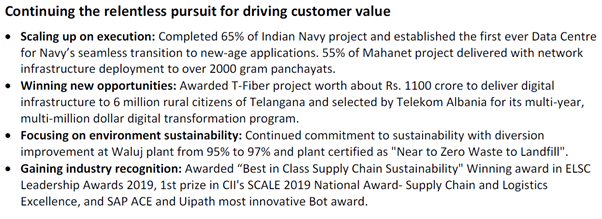

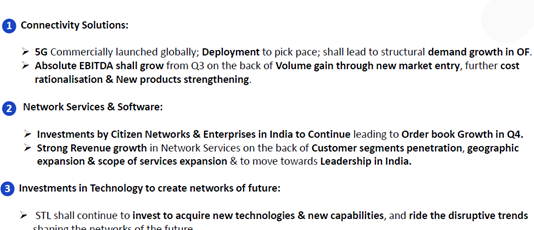

- 5G services: One clear point which is coming is the commercial 5G services are getting launched in key economies. At the same time, large edge data centres are getting deployed with the network on top of their own network connectivity. We are also seeing that data ARPU is increasing as a percentage in the total global ARPU and both tower fiberization as well as broadband connectivity continue to grow. And with the recent changes in ARPUs and the tariff changes in the India telecom industry, we believe the profitability is likely to improve as it moves forward. Coming to India, although 5G deployment is still some time away, the telecom industry profitability is going to increase following the tariff’s hike. And we believe that the investments required to create future networks, which are pretty much due in terms of tower connectivity, et cetera, should start happening in the country.

- Cloud Based Services: In terms of cloud, we have seen a massive hyperscale and edge data centers getting built by global cloud companies. In 2020, the CapEx by global cloud companies is expected to grow by around 20% to almost $103 billion. The new cloud network infra architecture will require many more data centers to be built. And additionally, we are also seeing cloud companies owning their transmission, the fiber network between data centers. Going forward, this customer segment shall significantly impact the optical fiber demand. And we have also, as we have been talking for the last 2 quarters, we have initiated sales in this segment.

- Citizen Networks: If we move on to the citizen networks, we – the Indian government launched the national broadband mission in December of 2019, which aims to fast-track growth of digital communication infrastructure, bridge the digital divide and provide affordable and universal access of broadband for all. The main objective of this mission is to provide access to all villages by 2022. And this – it envisages almost INR 7 lakh crore investment in the next 3 to 4 years. The ambitious project will involve going beyond what BharatNet has been doing. And it talks about laying almost 3 million route kilometers of optical fiber cable, which will involve increasing fiberization of towers from 30% to 70% and increasing tower density from 0.42 to 1.0 tower per 1,000 population. Thereby, significantly improving quality of services for mobile as well as Internet.

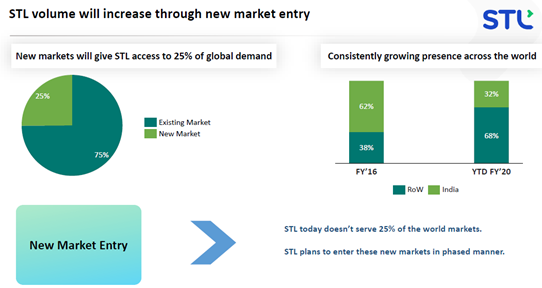

- Geographical Expansion: We are looking at Southeast Asia. We are looking at Middle East, and we are looking at North America. And as we have done in the past, wherever we go, we go deeper. We take some time. We invest in those markets. And so in all these markets, we have started seeing a good degree of traction. Latin America is picking up in terms of volumes that we do. And we are very clear that as we have succeeded over the past in India, in China, in Europe, it’s the same methodology that will apply. And North America, you’re right, is a market that we are investing in, and we have started seeing some initial successes there as well.

- Q3 Performance:

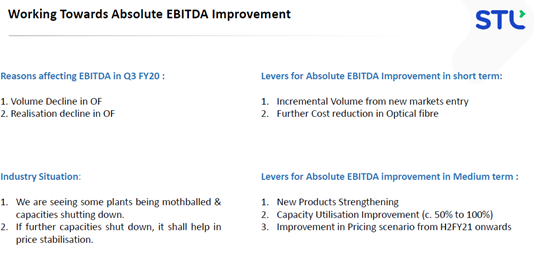

- Our volume in Q3 in fiber has come down, but our cable volume has remained overall intact. We are currently operating at about 46% utilization for the expanded capacity of 50 million kilometers in optical fiber, and 76% utilization in the cable capacity of 18 million kilometers. The cable capacity, as we have talked about, will go up to 33 million kilometers by June of 2020.

- In the new product segment, we have launched some of the new product, the one product that we launched called TruRibbon is – in March of last year, is finding very good response from the customers. As the networks of the future is requiring dense fiberization, TruRibbon is answering the call by offering almost 2,000 fiber in a single cable, which is – and it does it as the most compact cable packaging and superior handling design to enable first-time light installation.

- Leveraging on our strength of most integrated manufacturing and supply chain, we also started Project [Junoon] in January of 2019 to focus on the overall cost structure in optical fiber. And we have found a cross-functional team to work on the cost-reduction possibilities across raw material, manufacturing as well as fixed costs. In the raw material costs, we’ve used the levers of yield improvement; renegotiation with existing vendors, alternate vendors; as well as in-house process improvements. In the manufacturing cost reduction, we have looked at areas like consumables as well as power load optimization. And in the fixed cost area, we have reorganized ourselves in a lean and agile organization. We have been able to achieve very significant good results so far. And we – going forward, also, there are several projects to further do cost rationalization as we continue to move forward.

- So in the current quarter, the connectivity solutions business, the absolute EBITDA has been affected on the back of both lower volume as well as some lower realizations in the optical fiber business. In the – globally, what we are also seeing some plants starting to get mothballed and capacities shutting down. If further capacities shut down, we believe it will help in price stabilization. In the short term, we expect that the – this business unit’s absolute EBITDA will improve on the back – both of incremental volume as well as cost reduction, which we are continually doing. And in the medium term, we shall continue our work on new products strengthening as well as increasing capacity utilization by entering new markets. We expect that as the overall pricing environment improved on the back of global demand, the Absolute EBITDA will be going up.

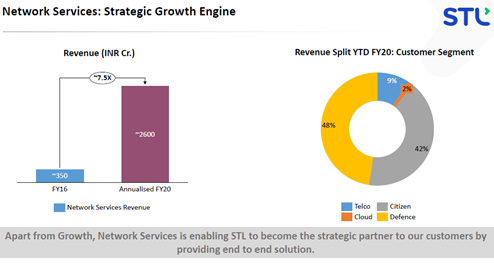

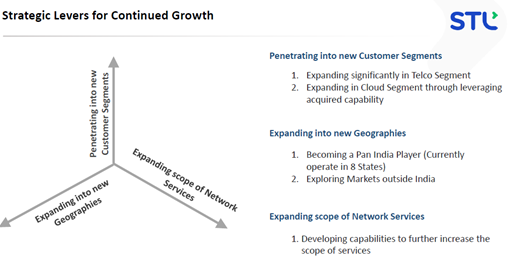

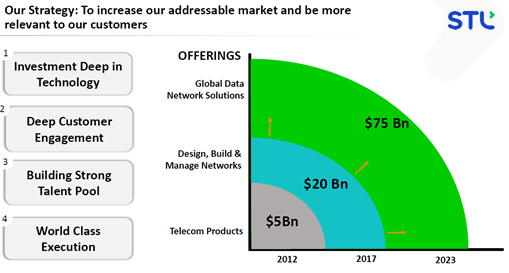

So in this context, if you see, we are no more a pure-play fiber player. We have quietly transformed ourselves from a fiber and cable manufacturing company to an end-to-end solution provider. And this business is almost like between 50%, 51% of our total revenues for the quarter and for the year. And apart from the growth, it is enabling STL to become the strategic partner to our customers by providing end-toend solution from network design to implementation, operation and management. We have also grown our capability from network implementation to complex system integration, and we are continuously adding more and more product offerings. We also see that the overall total addressable market for network services in India itself can add up to almost $15 billion from the forward segments of telecom companies, citizen networks, cloud as well as the large enterprises. And as we are taking shape, our clear aim is to become a full leader in network services in India, while we will initiate a global place through our data center offering with the acquisition that we had done last quarter in IDS in the U.K.

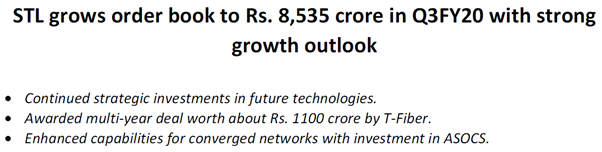

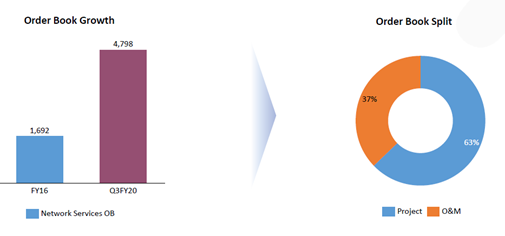

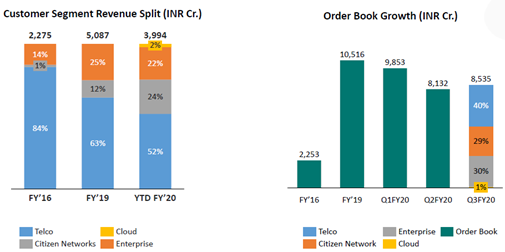

So overall, what we see is that the services business shall clearly expand in 3 vectors. On one side, we will do customer expansion. Till date, most of our revenues, which were coming from enterprise and citizen networks, we are also now increasing our order book as well as revenues from telco and cloud segments. We are doing geographic expansion. We have already expanded in India from 3 states to 8 states. And we are slowly moving to a pan India presence. At the same time, as I said earlier, we are also moving to global markets with the IDS acquisition. And in terms of – we are also looking at scope expansion. We’ll continue to develop our capability to take on further scope to provide end-to-end offerings. So overall, the business order book has grown from about INR 1,600 crores – INR 1,700 crores to almost INR 5,000 crores in the current year and is expected to continue to grow up in the current quarter. The interesting part is that the business is also now, as the projects are getting completed, the O&M revenues is becoming a sizable part in terms of providing that visibility. So we have, out of the INR 5,000 crore order book, almost 38% is O&M, which will result in significant revenue stream as well as predictability in the future years.

I would also like to just talk about that we’ve reorganized ourselves to an organization structure that places the customer at its center on an – in an account-based organization, which will help us to offer both and fulfill power-of-one offering of Sterlite as well as the industry-shaping and customer-specific solutions with presenting us a single face to customers as well as creating lifetime customer value.

Management Interview:

Prices are stabilising. Hold onto upper hand of the price band. Holding onto 22% EBITDA margin. Demand to move up due to 5G implementation. Working on cost optimization. Good movement in receivables. Liquidity continues to be good. BSNL receivable has been delayed. Order Book likely to increase. H2 will be muted. FY21 looking at revenue growth of more than 25%.

From Q2 FY20 Concall/IP: (for comparison)

Based on the visibility that we have today for FY '20 for both, overall volumes of fiber and cable would be mostly flattish. This supports the deferment of some of the orders of high value-added fiber to translate into lower average fiber pricing for the second half. On the revenue front, we are confident of growth this year a bit driven by more system integration and software business. The profitability will be impacted mainly on account of lower utilization of our new capacity, higher interest and depreciation costs and incremental investment in 5G-related R&D investment. As for our current visibility, H2 profitability would be weaker than H1. As we progress further into the second half of the year, we will keep you apprised on any new developments.

On the cash flow front, we are very happy to share that we have generated strong positive cash flow of Rs. 260 crore in H1 of the current year, and net debt-to-equity has been consistent at less than 1. We could bring down our debt levels by around Rs. 300 crore as compared to the previous quarters through a strong cash flow management.

3 Likes

I dont understand…why market dont like this counter…experienced folks can throw light on this

“During the current quarter, the Company has made an application under Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019 (SVLDRS), for settlement of the disputed excise matter of Rs. 188 crores demanded by CESTAT in 2005-06 which the Company was contesting at Supreme Court, and also some other litigations under Central Excise Act, 1944 and Chapter V of Finance Act, 1994 which were pending as of June 30, 2019. Based on the provisions of SVLDRS, Management has determined the duty payable in respect of all matters offered for settlement under the scheme and accordingly made an additional provision Rs. 50.71 crores in the current quarter. The Company is awaiting acceptance of the application by the department as of date.”

Sabka Vikas Scheme gives one time discount on tax payed to remove pending tax litigation.

So the company which seen as a consistent compounding machine suddenly had drop in sales and an even further drop in profit and eps.

YOY Quarterly profit growth: -39.50 %

There was issue of pledging by promoter last year which started the fall.

2 Likes

Promoters removed pledge…continous orders…what is missing here …market knows more than me…please throw light …senior members

As per STL,

- Global OFC demand came down in 2019 and there is degrowth in China and India,

- Expecting demand and price recovery in H3FY21E

- The Service revenue is increasing but margin is low as compared to OFC.

- There is decline in fibre prices and hence margin have come down.

After 3 quarters if there is visibility in the OFC revenue and price pick up then maybe we can see some re-rating

Regards,

Manoj

2 Likes

Since China consumes and exports a large part of the worlds optical fiber, is there a positive for Sterlite during this Corona crisis?