In FY26Q2 concall, they said that, Q3 will be softer but Q4 will be better as they are hoping for tariffs issue will be solved. They said they will always maintain 28% to 29% of OPM with 20% annual revenue growth for the next 3 years. I think it is very decent bet for long term investment at the current price point. Please correct me if I am missing any other point. Also, they are no longer interested in defence sector as the bidding process is tiresome and they see good opportunities in their own sector.

1 Like

1. Company History, Manufacturing Facilities & Operations

Founded in 1960 as a partnership firm, Steelcast transitioned into a private limited company in 1972 and a public limited company in 1994. Co-founded by Mr. Manmohan Fulchand Tamboli and currently led by Mr. Chetan Manmohan Tamboli, the company boasts over six decades of legacy in the high-integrity steel and alloy steel castings industry.

Steelcast operates a robust manufacturing facility in Bhavnagar, Gujarat, with an installed capacity of 29,000 tonnes per annum (TPA). The facility houses four production plants, including a dedicated state-of-the-art machine shop, and utilizes both sand and shell molding processes—a rarity among global casting manufacturers. The company manufactures over 298 distinct parts, ranging in weight from 5 kgs to 2,500 kgs.

A significant operational edge comes from its locational advantages and power self-sufficiency. Positioned in a power-surplus state, Steelcast operates its own 66KV power transmission station for an uninterrupted 10 MW supply and meets 80% of its power needs through captive renewable energy (9.5 MW of commissioned hybrid/solar power plants). Furthermore, the proximity to Alang (Asia’s largest ship recycling yard, just 50 kms away) provides access to competitive scrap steel, while the Pipavav port (130 kms away) facilitates seamless export logistics.

2. Segmental Breakdown, Products, and Revenue Contribution

Steelcast operates as a pure-play B2B manufacturer, dedicating 100% of its output to Original Equipment Manufacturers (OEMs) rather than the retail replacement market. The company’s focus on value addition is a significant margin driver, with approximately 75% of its castings shipped globally as fully machined, ready-to-use components.

The company maintains a vast and complex portfolio, manufacturing over 298 distinct parts per month (up from 269 parts previously), with weights ranging from 5 kgs to 2,500 kgs. It utilizes both sand and shell molding techniques—a rare dual capability that provides immense manufacturing flexibility.

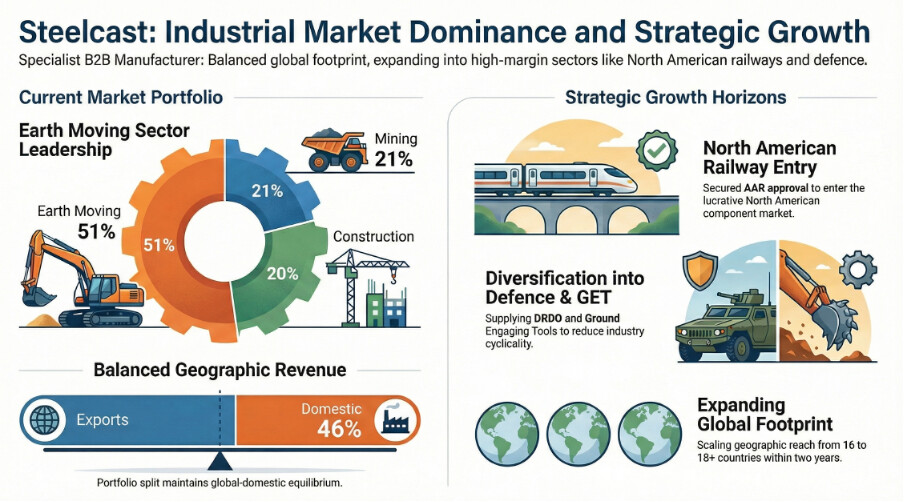

The top five sectors combined account for 96.8% of the company’s total revenue. The specific end-user industry breakdown and product lines are as follows:

· Earth Moving Equipment (51% of Revenue): This segment forms the backbone of Steelcast’s top line. The company manufactures critical, heavy-duty components such as track shoes, track links, backhoe buckets, teeth, and specialized adapters that endure high stress in continuous operations.

· Mining & Mineral Processing (21% of Revenue): Focusing on wear and abrasion resistance, Steelcast supplies highly engineered crusher components (jaw plates, cone crusher liners, and impact plates) and heavy excavator/shovel parts, including dragline chains and crawler shoes for massive dragline buckets.

· Construction Equipment (20% of Revenue): Benefiting from global infrastructure cycles, the company provides robust castings including heavy counterweights, crane attachments, and suspension system components designed for graders and bulldozers.

· Locomotive (5%) & Railways (1%): Though currently a smaller portion of the pie, this segment offers the highest margin optionality. Products include Cast Manganese Steel Crossings, bogie frames, couplers, and drawbars. Having secured the stringent Tier 1 Association of American Railroads (AAR) accreditation, Steelcast is heavily targeting the lucrative North American freight wagon and locomotive market.

· Others - Defense, Ground Engaging Tools (GET), Cement & Steel (2% of Revenue):

o Ground Engaging Tools (GET): The company is aggressively developing dozens of new products in this category, with initial export dispatches already commencing for OEMs in North America and Australia.

o Defense: Steelcast is scaling its defense footprint, transitioning from sample testing to serial production for track components used in combat vehicles, notably engaging with an Israeli OEM.

o Cement & Steel Plants: Supplies include durable grinding media, mill liners, grate plates, and kiln nose rings designed for high-temperature applications.

Customer Concentration and Geographic Footprint Client stickiness acts as a deep structural economic moat. A massive 76% of total revenue is derived from clients whose relationships with Steelcast span over 20 years, including several Fortune 500 companies. Furthermore, revenue concentration risk is well-managed, with no single customer accounting for more than 20.9% of total global revenues.

Geographically, the revenue base is well-hedged against localized economic downturns:

· Exports (54%): Driven heavily by the “China + 1” sourcing shift, the company exports to 16 countries including the USA, Germany, Brazil, South Korea, Canada, and Australia. Strategic plans are actively underway to expand this footprint to 18+ countries in the next 12 to 24 months to further de-risk reliance on any single economy.

· Domestic (46%): Benefiting from ongoing Indian infrastructure capex and the “Make in India” initiative, domestic demand provides a highly stable baseline for operations.

1. Promoters, Background, Remuneration, and Holdings

The promoter group, led by Mr. Chetan M. Tamboli (Chairman & Managing Director) and Mr. Rushil C. Tamboli (Whole-Time Director), maintains a stable and completely unencumbered stake in the business.

· Holdings: The total promoter holding stands firmly at 45.00%. Key individual and entity holdings include Mr. Chetan M. Tamboli (~16.4%), Tamboli Trading LLP (~9.7%), and Manali C. Tamboli (~7.1%).

· Pledging: Pledged holdings currently stand at 2.85% (Appendix A)

· Remuneration & ESOPs: The remuneration for the managerial personnel, including the MD and the CFO (Mr. Subhash R. Sharma), is maintained well within the statutory limits set out by the Companies Act. There are no material ESOP/ESPS dilutions affecting the profitability or equity base, ensuring that retail and institutional equity value remains intact.

2. Quality of Earnings & Return Ratios

Steelcast’s earnings quality is exceptionally high, underpinned by a zero-debt balance sheet and a business model that focuses on value addition rather than commodity pricing.

· Value Addition: Roughly 75% of all castings are shipped as fully machined components, which commands premium pricing and deepens client stickiness.

· Return Ratios: The company exhibits top-tier capital efficiency. For FY25, the annualized Return on Capital Employed (ROCE) stood at an impressive 30.10%, while Return on Equity (ROE) consistently hovers around the 24-25% mark.

· Other Income: Other income primarily consists of treasury yields and forex gains/losses. For 9M FY26, other income was ₹10.37 Cr, compared to ₹5.37 Cr in the prior year period. This remains a minor fraction of the total ₹85.49 Cr PBT reported in the same period, indicating that core operations drive profitability.

3. Consolidated Quarterly Results Deep Dive (Q2 & Q3 FY26)

The company has demonstrated resilient profitability despite near-term macroeconomic volatility.

· Q2 FY26: Revenue from operations was ₹106.65 Cr (up ~42% YoY), driven by inventory restocking cycles in North America and Europe. EBITDA jumped significantly by ~62% YoY to ₹34.20 Cr, expanding margins to ~32.00%. Profit After Tax (PAT) came in at ₹23.20 Cr, an impressive 75% YoY growth.

· Q3 FY26: Revenue saw a slight moderation, coming in at ₹97.40 Cr (a 3% YoY decline from ₹100.5 Cr in Q3FY25) due to softer export demand visibility and geopolitical uncertainties. However, operational efficiencies allowed EBITDA (excluding other income) to grow by 1.8% YoY to ₹27.5 Cr, with margins expanding by 136 bps to 28.2%. PAT for Q3 FY26 stood at ₹20.6 Cr, up 7.2% YoY.

· 9M FY26: On a 9-month basis, revenue stands at ₹310.7 Cr (up 22.7% YoY), and PAT is at ₹63.7 Cr (up 40.2% YoY).

· Corporate Actions: The company aggressively rewards shareholders, declaring three interim dividends in FY26 (36%, 36%, and 45% respectively) and executing a 1:5 stock split in August 2025 to increase liquidity.

4. Working Capital, Cash Flows, and Future Prospects

From a fundamental analysis standpoint, the balance sheet health is pristine.

· Working Capital & Inventory: The company maintains a disciplined approach to working capital. Receivables optimization is a core strategic pillar, ensuring cash conversion cycles remain tight. Inventory management is highly responsive to the demand cycles of OEMs, allowing the company to report strong operating cash flows. Operating profit before working capital changes was robust at ₹59.50 Cr for H1 FY26, translating into a net cash flow from operations of ~₹6.05 Cr after aggressive working capital investments to support the massive Q2 revenue surge.

· Future Prospects: The company expects a ~12% double-digit revenue growth for FY26. Looking further out, management expects capacity utilization to ramp up from the current 45-48% to roughly 58% in FY27, and peak at ~90% (approx. 26,000 tonnes) by FY2029. At peak utilization, current realizations map to an estimated revenue potential of ₹850 to ₹1,000 Cr.

5. Capex Plans, Timelines, and Opportunities

With zero debt and heavy free cash flow generation, Steelcast entirely self-funds its capital expenditures.

· Debottlenecking & Space: The company is executing incremental expansions. For FY27, management has outlined an estimated ₹35 Cr capex plan dedicated to new space requirements for handling higher output and procuring balancing equipment for new product mixes.

· Green Power Expansion: The company is setting up an additional 2.4 MW hybrid power plant (scheduled for June 2026 commissioning) to cater to the volume expansions expected in FY27. This will generate an additional ₹3.5 to ₹4 Cr in annual savings, structurally defending the high EBITDA margins.

6. Acquisitions and Inorganic Growth

Steelcast’s growth trajectory has been almost entirely organic. There are no major acquisitions or complex M&A activities diluting the focus. Instead, the company utilizes a “land and expand” strategy, winning a small part with a Fortune 500 OEM and systematically increasing its wallet share through superior metallurgical properties and lower defect rates.

7. Red Flags, RPT, Contingent Liabilities, & Litigations

A rigorous check of the latest annual reports and auditor notes reveals a clean corporate governance profile:

· RPTs: Related Party Transactions are conducted strictly on an arm’s length basis and are routinely approved by the Audit Committee.

· Litigations/Contingent Liabilities: There are no major outstanding litigations or massive contingent liabilities threatening the going-concern status of the business.

· Red Flags: None. The company’s conservative accounting practices, zero pledging, zero debt, and clean auditor remarks reflect a highly transparent management team.

8. Competition with China & Market Dynamics

The “China + 1” strategy adopted by major global OEMs is providing immense tailwinds for Steelcast. Furthermore, US trade tariffs on Chinese goods offer a direct structural cost advantage. Management highlighted on the Q3 earnings call that across three of their key product categories exported to the US, their pricing remains approximately 5%, 12%, and 13% more competitive than both global and Chinese suppliers. The capital-intensive nature of this industry, coupled with the need for precise metallurgical compliance, prevents new lower-cost entrants from easily undercutting Steelcast’s established contracts.

9. The “Right to Win” (Competitive Moats)

Steelcast possesses several distinct economic moats:

· High Switching Costs: 76% of revenues are derived from clients with relationships lasting over 20 years. Heavy engineering OEMs face immense re-validation and testing costs to switch casting suppliers.

· Certifications: Possessing **AAR, ISO 9001, ISO 14001, ISO 45001, and *EN 9100 (Aerospace) certifications puts them in an exclusive club of validated global suppliers.

· Vertical Integration: By offering end-to-end solutions (design, casting, heat treatment, and precision CNC machining), the company saves OEMs from utilizing third-party machine shops.

· Cost Leadership: Generating 80%+ of power requirements internally and proximity to scrap hubs keeps raw material and conversion costs structurally suppressed.

10. Risk Factors

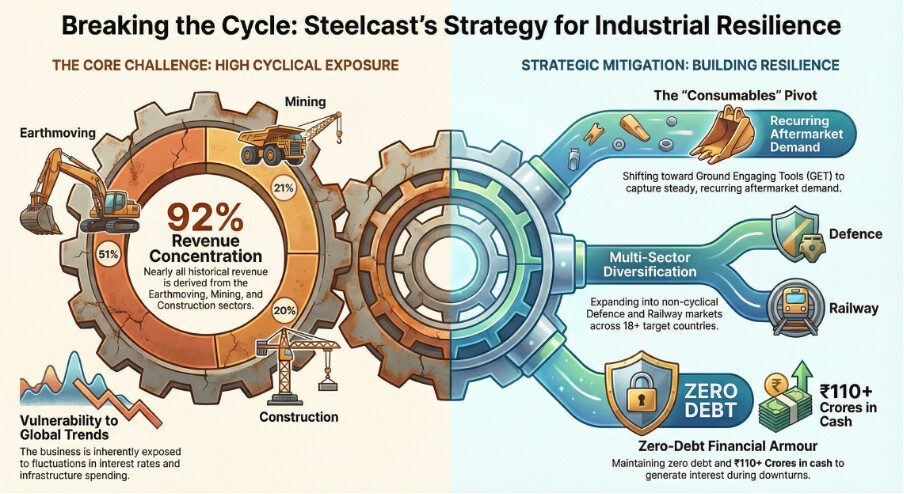

· Cyclicality: The primary risk is the company’s 51% revenue dependence on the earthmoving sector, which is highly sensitive to global interest rates and macroeconomic cycles.

· Geopolitics & Freight: While export demand is robust, disruptions in global shipping lanes or extended geopolitical conflicts (like the recent Russia-Ukraine impact) can create inventory pile-ups at the customer end, leading to temporary order deferrals.

----------------------------------------------------------------------------------------------------------------

A detailed breakdown of the Q3 FY26 Earnings Call Transcript, analyzing the stated facts and reading between the lines to uncover the underlying business dynamics:

Executive Summary

Steelcast’s Q3 FY26 performance reflects a resilient business model navigating short-term geopolitical headwinds. While top-line growth saw a minor contraction due to U.S. tariff-related demand deferrals, the company delivered exceptional margin expansion. Management remains highly confident in structural “China+1” tailwinds, projecting a massive scale-up in capacity utilization over the next three years without needing immediate heavy capital expenditure.

1. Financial Performance & Margin Analysis

-

The Numbers: Q3 FY26 revenue stood at INR 97.4 crores (down 3.08% YoY), but EBITDA grew 6.81% to INR 31.21 crores, with margins expanding sharply by 297 bps to 32.04%. PAT grew 7.17% to INR 20.59 crores.

-

Reading Between the Lines (Margin Sustainability): Despite reporting ~32% EBITDA margins, management conservatively guided sustainable long-term margins at 27.5% to 28%. This cautious guidance suggests that while current profitability is buoyed by favorable foreign exchange gains, lower raw material costs, and cost reduction programs (together contributing INR 3.41 crores this quarter), the aggressive scale-up of new product volumes expected in FY27-FY29 will likely feature a lower-margin product mix initially.

-

Order Book Visibility: The executable order book for Q4 sits at a healthy INR 115 crores, underpinning management’s confidence in achieving 11% overall revenue growth for FY26.

2. Capacity Utilization & The Growth Runway

-

The Numbers: Current capacity utilization was roughly 46% for the quarter. Management has laid out aggressive targets: 58% for FY27, scaling up to ~90% (approx. 26,000 tons) by FY29.

-

Reading Between the Lines (The Execution Moat): A jump from 46% to 90% utilization within three years is highly ambitious. The catalyst for this is an aggressive new product development pipeline: 56 parts developed in FY25, 46 in FY26, and 42 planned for FY27 (144 parts total). Management noted they already have tooling and sample purchase orders for the FY27 batch. The massive utilization leap is predicated on these 144 components converting from sample testing into serial production over the next 24-36 months.

3. Geopolitics, Tariffs, and the China Advantage

-

The Numbers: Management stated their products supplied to the U.S. are 5%, 12%, and 13% more competitive than Chinese offerings across three key categories.

-

Reading Between the Lines (Pricing Power): The U.S. tariff situation has created temporary anxiety and order deferrals, making Q3 “softer”. However, Steelcast possesses immense pricing power. Management explicitly stated they have not reduced prices for any U.S. customers and flatly refuse to offer discounts even if asked, noting that a 1-1.5% discount is meaningless against a 50% tariff burden. Furthermore, switching casting suppliers takes 2-3 years, meaning existing OEMs are effectively locked in. The global supply chain rebalancing is resulting in inquiries from customers actively seeking to derisk from China, reinforcing Steelcast’s “Right to Win”.

4. Capital Allocation, Capex, and Cash Flows

-

The Numbers: FY27 Capex is slated at INR 35 crores for space requirements and balancing equipment. The company is sitting on roughly INR 110 crores parked in government securities and fixed deposits, expected to reach INR 125-130 crores by year-end.

-

Reading Between the Lines (Conservative Capital Stewardship): The balance sheet is pristine, and cash generation is highly robust. Management is displaying deep financial discipline by refusing to initiate major Greenfield or Brownfield expansion capex until the current facility hits an annual run rate of 75% utilization. The INR 35 crore FY27 capex is purely for debottlenecking to handle the new product mix. This implies that free cash flows will continue to compound in treasury instruments (driving the noted increase in “Other Income”) and return ratios (ROCE/ROIC) will remain elevated as the denominator (capital employed) stays relatively flat while operating leverage kicks in.

5. Optionality & Diversification Strategies

-

Defence Sector: A significant near-term catalyst is the development of a combat vehicle part for an Israeli company. After two sets of sampling over six months, serial export orders are expected in the “coming few weeks”.

-

Ground Engaging Tools (GET): Execution of initial orders in the GET and Construction segments commenced in Q2 FY26, diversifying revenues away from traditional earth-moving cycles.

-

Geographic Expansion: The company is actively targeting two new countries within the next 60-90 days, expanding their export footprint from 16 to 18 countries to mitigate reliance on the U.S. market (which currently accounts for 26-30% of exports).

Takeaway

Steelcast is currently at an inflection point. While near-term headline revenue numbers appear muted due to global supply chain hesitations, the underlying fundamentals are strengthening. The company is actively trading short-term margin padding for long-term volume scale-up via its 144-part pipeline. With zero need for heavy capex in the near term, deep pricing power against OEMs, and structural cost advantages over Chinese peers, the company is exceptionally positioned to capture operating leverage as utilization ramps up from 46% toward the 90% target over the next three years.

----------------------------------------------------------------------------------------------------------------

The customers of Steelcast are mostly in industries which are cyclical in nature.

Here is how Steelcast is actively mitigating its cyclical risk:

1. The “Consumables” Pivot: Ground Engaging Tools (GET)

While capital equipment (like buying a new excavator) is highly cyclical, the wear-and-tear parts used on that equipment are not. Earthmoving and mining equipment constantly grind against rock and soil, meaning parts like teeth, adapters, and bucket components wear out and must be replaced repeatedly for the machinery to function.

· Connecting the Dot: By actively expanding into the Ground Engaging Tools (GET) segment with initial orders commencing in Q2 FY26 and dozens of parts under development—Steelcast is shifting a portion of its revenue away from cyclical OEM capital expenditure and toward steady, recurring “aftermarket/consumable” demand.

2. Sectoral Diversification: Moving into Non-Cyclical Domains

The company is aggressively working to dilute the 51% concentration in earthmoving by entering entirely different economic ecosystems.

· Defense: Defense spending is driven by geopolitics and national security budgets, making it largely immune to standard economic recessions. Steelcast’s development of combat vehicle parts for an Israeli OEM (with serial production expected shortly) is a direct hedge against commercial cyclicality. (Appendix B)

· Railways: Having secured the rigorous AAR approval, Steelcast is penetrating the North American railway market. While freight rail has its own cycles, they often do not perfectly overlap with construction or mining cycles, providing a counter-cyclical balance.

3. Geographic Hedging and “Wallet Share” Growth

If the US market slows down, a presence in Europe or Australia can offset the decline.

· Geographic Spread: Steelcast currently exports to 16 countries and is actively targeting two new geographies in the coming months to reach 18+ countries.

· Growth via Market Share, Not Just Market Growth: The company is developing 144 new parts between FY25 and FY27. Even in a downcycle where total industry volumes shrink, Steelcast can continue to grow its top line by simply winning a larger share of a client’s overall casting requirements.

4. Financial Armour: The “Endurance” Mechanism

When a severe cyclical downturn inevitably occurs, highly leveraged heavy-engineering firms often face existential crises due to fixed debt obligations. Steelcast has structured its balance sheet to thrive during these stress periods.

· Zero Debt & Cash Hoarding: The company operates with zero debt and is sitting on roughly ₹110 Crores in government securities and fixed deposits, which is expected to grow to ₹125-130 Crores by the end of FY26.

· Connecting the Dot: During a downcycle, Steelcast does not bleed cash to service loans. Instead, its massive cash pile generates significant “Other Income” (interest yields), which acts as a synthetic cushion for the bottom line while competitors struggle. Furthermore, their self-sufficient power setup (80% captive green energy) keeps fixed operational costs structurally suppressed.

Summary

Steelcast cannot completely escape the cyclical nature of its primary end-users. However, by pivoting toward consumable GET parts, breaking into the non-cyclical defense sector, spreading its geographic footprint, and maintaining an ironclad, zero-debt balance sheet, the company has transformed what would normally be an existential cyclical threat into a manageable earnings fluctuation.

----------------------------------------------------------------------------------------------------------------

How Steelcast can benefit from global mining industry trends?

Here is a detailed analysis of how Steelcast is benefiting, and can further benefit, from global mining trends:

1. The “Green Mineral” Supercycle (Energy Transition)

· The Trend: The global push toward decarbonization, renewable energy infrastructure, and Electric Vehicles (EVs) has triggered a massive surge in demand for critical “green metals” like copper, lithium, nickel, and cobalt. Extracting these minerals requires intensive, large-scale surface and underground mining operations.

· The Steelcast Benefit: To process billions of tons of ore, mining companies require highly durable, abrasion-resistant equipment. Steelcast directly manufactures the exact components needed for this extraction and processing, including crusher components (jaw plates, cone crusher liners, and impact plates) and heavy excavator parts like dragline chains and crawler shoes. As global mining capex increases to hunt for these critical minerals, Steelcast’s baseline demand for its highly engineered castings naturally scales up.

2. Supply Chain Derisking and the “China + 1” Strategy

· The Trend: Geopolitical tensions, trade tariffs, and the vulnerabilities exposed during recent years have forced major global mining Original Equipment Manufacturers (OEMs) to aggressively diversify their supply chains away from a singular reliance on China.

· The Steelcast Benefit: Steelcast is a direct beneficiary of this global rebalancing. Management has explicitly noted that their pricing for key product categories in the U.S. remains 5%, 12%, and 13% more competitive than comparable Chinese offerings. Because casting supply chains are sticky and take 2-3 years to transition, Steelcast is actively fielding inquiries from North American and European OEMs looking to lock in reliable, non-Chinese suppliers.

3. Mine Automation and the Boom in Consumables (GETs)

· The Trend: To improve safety and efficiency, the mining industry is rapidly adopting autonomous haul trucks, remote-controlled excavators, and AI-driven fleets. Because autonomous machines do not need shift changes or rest, they operate closer to 24/7, which significantly accelerates the wear and tear on the physical parts of the machinery.

· The Steelcast Benefit: Steelcast is strategically pivoting to capture this accelerated replacement cycle by aggressively expanding its Ground Engaging Tools (GET) segment. GETs—such as bucket teeth, adapters, and cutting edges—are the “consumables” of the mining world. By developing dozens of new GET parts, Steelcast is moving from selling one-off capital expenditure components to securing a recurring, high-margin revenue stream driven by continuous machine wear.

4. ESG Mandates and “Green” Supply Chains

· The Trend: Global mining companies are under intense pressure from regulators and investors to decarbonize their operations. This pressure is now extending to their supply chains, meaning OEMs prefer to source parts from vendors with low carbon footprints (Scope 3 emissions).

· The Steelcast Benefit: Steelcast has a significant structural and ESG advantage. The company meets approximately 80% of its massive power requirements through captive renewable energy (hybrid/solar plants). They are also adding another 2.4 MW of green power capacity by FY27. This allows Steelcast to market its castings as “green components,” making them a preferred vendor for environmentally conscious global OEMs.

5. Declining Ore Grades requiring Heavier Processing

· The Trend: Across the globe, high-grade mineral deposits are depleting. To get the same amount of refined copper or gold, mining companies must excavate, crush, and process significantly higher volumes of lower-grade rock.

· The Steelcast Benefit: Processing higher volumes of harder, lower-grade rock requires heavier, more durable crushing and pulverizing equipment. Since Steelcast specializes in high-integrity, wear-resistant alloy steel castings weighing up to 2,500 kgs, the demand for their robust mineral processing components will increase proportionately with the volume of rock being moved.

---------------------------------------------------------------------------------------------------------------

*The EN 9100 certification (which is the European equivalent of the globally recognized AS9100 standard) is a highly specialized Quality Management System (QMS) standard specifically designed for the Aviation, Space, and Defense (ASD) industries.

Here is a detailed breakdown of what this certification is and what it strategically means for Steelcast Ltd.:

1. What is the EN 9100 (Aerospace) Certification?

Created by the International Aerospace Quality Group (IAQG), EN 9100 builds upon the foundational framework of the standard ISO 9001 certification but adds stringent, industry-specific requirements tailored to the high-stakes aerospace and defense sectors.

To achieve and maintain this certification, a manufacturer must prove extreme competence in areas where failure can be catastrophic. Key additions include:

-

Stringent Traceability: The ability to trace every single component back to its raw material batch (e.g., tracking the exact chemical composition of a steel casting).

-

Advanced Risk Management: Proactive identification and mitigation of risks related to product safety and delivery.

-

Foreign Object Debris (FOD) Prevention: Strict manufacturing environments to ensure no foreign materials compromise the integrity of the parts.

-

Zero-Defect Quality Control: Rigorous testing protocols (like First Article Inspection) to ensure components endure extreme stress, temperature, and friction.

2. What Does EN 9100 Mean for Steelcast?

For an industrial foundry like Steelcast, possessing the EN 9100 certification is a massive validation of their technical and metallurgical capabilities. It carries several strategic advantages:

A. An Exclusive Competitive Moat

The heavy casting industry is highly competitive, but the aerospace and defense tier is an “exclusive club.” Most standard foundries cannot pass the rigorous audits required for EN 9100. By holding this certification, Steelcast automatically eliminates lower-tier, low-cost competitors (including many standard Chinese suppliers) when bidding for high-end contracts.

B. Gateway to the Defense Sector

Steelcast is actively trying to diversify its revenue away from the highly cyclical earthmoving and mining sectors. The EN 9100 certification is the “ticket to entry” for the defense sector. It directly validates their capability to manufacture critical, high-stress parts—such as the track components they are currently developing for combat vehicles for an Israeli OEM and the DRDO.

C. Superior Pricing Power

Components manufactured for aerospace and defense applications are not priced as commodities; they are priced based on precision, reliability, and certified compliance. Because OEMs in these sectors require EN 9100-certified suppliers, Steelcast can command significantly higher profit margins on these parts compared to standard construction equipment castings.

D. Trust with Global Fortune 500 OEMs

Even if a customer is not in the aerospace sector (e.g., a railway or mining OEM), seeing that Steelcast holds the EN 9100 aerospace certification acts as a supreme psychological and operational trust signal. It proves to global OEMs that Steelcast’s internal processes, machine shops, and NABL-accredited testing laboratories operate at the highest possible global standards.

----------------------------------------------------------------------------------------------------------------

**The AAR (Association of American Railroads) certification is another highly specialized and stringent credential held by Steelcast. While the EN 9100 certification unlocks the aerospace and defense sectors, the AAR certification is the master key to the global railway industry, specifically in North America.

Here is a detailed breakdown of what the AAR certification is and its strategic implications for Steelcast:

1. What is the AAR Certification?

The Association of American Railroads (AAR) is the premier standard-setting organization for North America’s freight rail network. The AAR sets rigorous safety, quality, and operational standards for every component used on a train.

For a steel foundry, achieving AAR certification (specifically the AAR M-1003 Quality Assurance certification) means the facility has passed exhaustive audits verifying that its metallurgical processes, testing capabilities, and quality control systems can consistently produce castings that withstand the extreme dynamic loads, vibrations, and safety requirements of heavy-haul freight trains.

2. What Does AAR Certification Mean for Steelcast?

Currently, the Locomotive and Railways segments contribute 5% and 1% to Steelcast’s total revenue, respectively. However, holding the AAR certification provides immense structural and financial optionality going forward:

A. Access to the Lucrative North American Market

North America operates the largest and most heavily utilized freight rail network in the world. You cannot legally or operationally supply critical railcar components (like couplers, yokes, or bogie frames) to North American rail OEMs or operators without AAR certification. By holding this credential, Steelcast has direct, unrestricted bidding access to a multi-billion-dollar market.

B. Manufacturing High-Margin, Critical Components

Railway components are not simple shapes; they are complex, life-critical parts. Under this certification, Steelcast can manufacture and supply high-value products such as:

-

Cast Manganese Steel (CMS) Crossings: Highly wear-resistant tracks used at railway intersections.

-

Bogie Frames, Couplers, and Drawbars: The massive, heavy-duty linkages that hold train cars together and attach them to the wheels.

Because these parts require flawless internal integrity (no microscopic air pockets or cracks that could cause a train derailment), they command premium pricing and high EBITDA margins.

C. A Deep Competitive Moat

Just like the EN 9100 standard, AAR certification acts as a massive barrier to entry. Developing the tooling, proving the metallurgical chemistry, and passing the physical destruction tests required by AAR auditors takes years and millions of dollars. New foundries or lower-cost, lower-quality overseas competitors cannot simply decide to start selling railway couplers tomorrow. This gives Steelcast pricing power and protects them from cheap commoditization.

D. Strategic Diversification

From an investor’s perspective, the AAR certification is a vital tool for cyclical mitigation. Freight rail infrastructure and wagon replacement cycles operate on different macroeconomic timelines than earthmoving and mining equipment. By scaling up its AAR-approved railway segment, Steelcast creates a counter-cyclical revenue stream that can stabilize earnings when construction or mining cycles inevitably dip.

Appendix- A:

Based on the latest exchange disclosures and data from financial screeners, here are the details regarding the recent promoter pledge in Steelcast Ltd.:

When was it done?

The pledging of shares was initiated during the quarter ended December 2025 (Q3 FY26).

-

Historically, the promoters of Steelcast maintained a strict 0.00% pledge on their holdings for several years.

-

The latest shareholding pattern for the December 2025 quarter reflects that the pledge has now increased from 0% to 2.85% of the total promoter holding (which remains steady at 45.00%).

Why was it done?

While the exact personal or corporate reason for this specific pledge has not been explicitly detailed in recent mainstream news reports, we can deduce the likely context based on the company’s fundamentals:

-

Personal or Group Financing: Promoters typically pledge shares as collateral to banks or non-banking financial companies (NBFCs) to secure personal loans, margin funding, or to fund other private business ventures outside the listed entity.

-

Not for Corporate Debt: Because Steelcast Ltd. itself is a zero-debt company sitting on a healthy cash pile (over ₹110 Crores in treasury instruments) and self-funds its own capex, it is highly unlikely that this pledge was created to secure working capital or term loans for Steelcast itself. It is almost certainly for the promoters’ personal financial requirements or external ventures.

--------------------------------------------------------------------------------------------------------------------------

Appendix B:

Based on the provided corporate documents and the latest Q3 FY26 earnings call, the management has maintained strict confidentiality regarding the exact name of the Israeli OEM (which is standard practice for international defense contracts governed by Non-Disclosure Agreements). However, they have provided specific, highly positive updates regarding the operational progress of this deal.

Here is the gathered intelligence on Steelcast’s engagement with the Israeli OEM:

1. The Product and Application

· Specific Component: The company is developing a highly specialized combat vehicle part.

· Based on their previous annual reporting and capabilities, this is likely related to “track components” or track systems designed for heavily armoured military vehicles.

2. Current Status & Timelines

· Testing Phase Completed: On the January 30, 2026, earnings call, Chairman & MD Mr. Chetan Tamboli confirmed that the progress is “quite satisfactory”. The company has successfully undergone and passed two sets of sampling over the past six months.

· Commercialization (Serial Production): Having secured approval on the samples, management explicitly stated they expect to receive serial orders in the “coming few weeks”.

· Revenue Nature: Management clarified to analysts that this specific contract is “purely export”.

3. The Backstory and Strategic Context

· Connecting the Timeline: In the FY 2024-25 Annual Report, Steelcast mentioned they had received a “trial order for export of defense components” and expected to deliver the samples in Q1 of FY 2025-26. The recent Q3 FY26 update confirms that those initial trial orders have successfully translated into approved, serial-production contracts.

· Testing Moat: Steelcast’s ability to win this order is backed by its specialized infrastructure. The company holds an NABL-certified laboratory that is specifically approved for the chemical and mechanical testing of parts for Defense applications. This allows them to meet the stringent, zero-defect metallurgical requirements demanded by military OEMs.

Takeaway:

While Steelcast’s core business relies heavily on the cyclical earthmoving and mining sectors (which account for over 70% of revenues), this Israeli combat vehicle contract represents a critical breakthrough. Defense spending is driven by national security and geopolitical necessities, making it entirely immune to commercial economic downturns.

Once serial production commences, this creates a high-margin, sticky revenue stream that will help structurally de-risk Steelcast’s overall portfolio and validate their engineering capabilities on a global military stage.

--------------------------------------------------------------------------------------------------------------------------

Compiled Notes from here & there, No Buy/Sell Recommendation

--------------------------------------------------------------------------------------------------------------------------

7 Likes