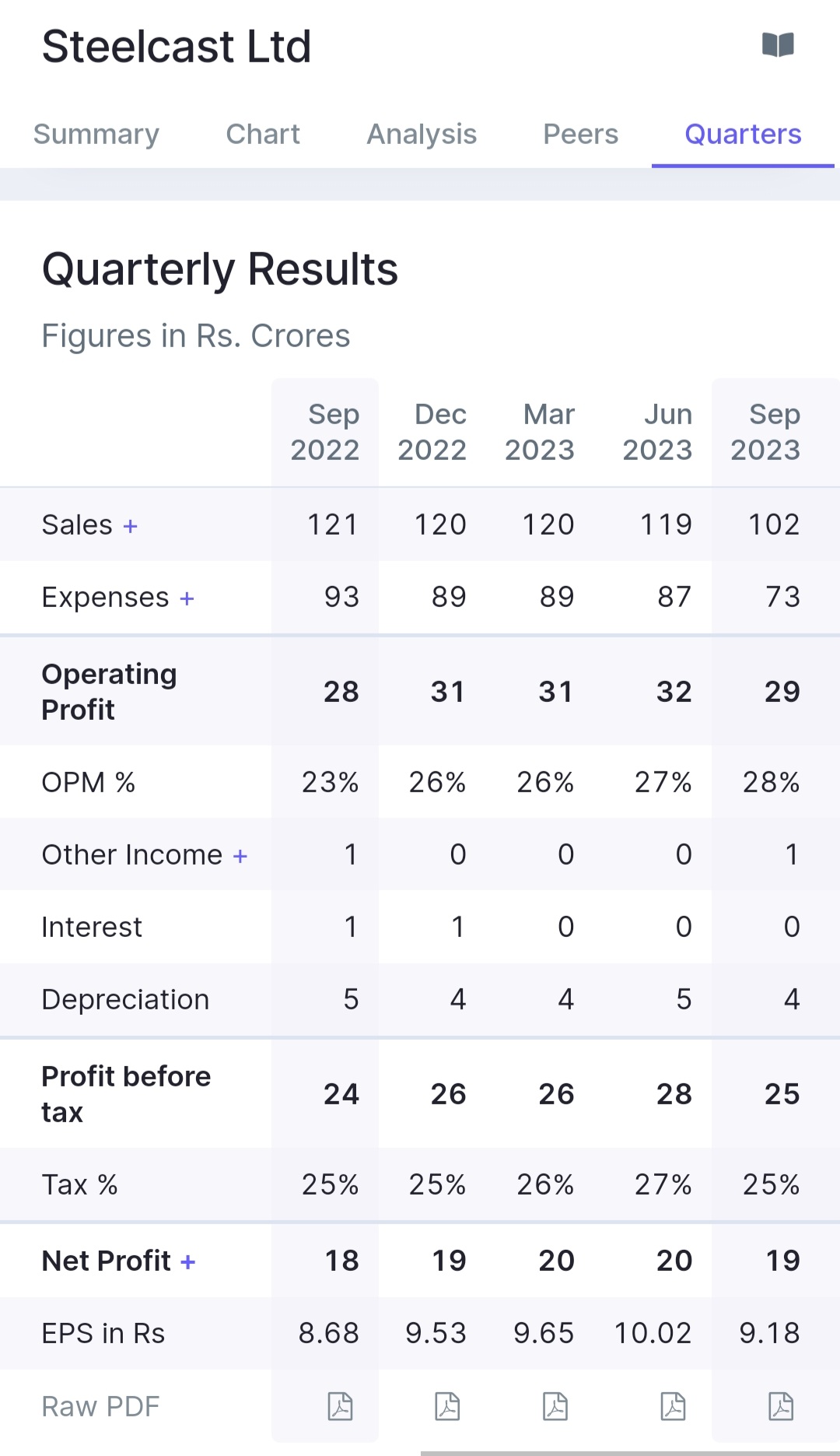

Steelcast has reported another excellent set of results. EBITDA margins have finally started benefitting from op leverage & now at 23.5%.Volume growth remains healthy.

Concall was held today,some highlights:

→ Continue to see good traction from end customers.No signs of slowdown at all.In fact,given poor environment in EU the governments maybe forced to revive the economy via capex.

→ Order book remains at 3-4 months.Mgt said they had wrongly mentioned 300 cr in the last call,they always have 3-4 month kind of order book & that continues.

→ WC will sustain at current levels.Expect to reach 57% capacity utilization in fy23,90%+ in Fy26.Expect to sell 21k MT in Fy24.

→ Will see some price deflation/correction owing to RM & currency movements from Oct. Net impact won’t be more than 1-2%.

→ Power saving plans remain on track.Should lead to 2% kind of margin improvement at current util but in case of higher utilization company will have to buy from external sources.

→ Have been able to enter Japanese market with all prototypes approved.No idea of market size & not targeting any market share but wish to supply high quality castings.Japan will be 10-15% of total exports.American railroad supplies also on track & will start from Q3.

→ Participating in DefExpo & expect to make similar margins on those products.India market in general also continues to be solid.

Management as usual was a bit conservative but continues to deliver very well.Company has also paid another interim dividend.Company should be able to end with ~70 cr kind of pat this fy.

Disc.: Invested.Views are biased.