I read last October that the steel pipes industry in India is going to benefit very much from a $10 billion expected spend on expansion of natural gas network. What do you think?

Also read this:

I have been researching online about the industry and about companies of all sizes which are in this industry. Has this been discussed in some other thread? If not, I will share the information I have gathered and the experts here can share their views and information.

Steel Pipe Companies:

Company name | Market cap (Crores)

- Ratnamani Metal 3,948.98

- Mah Seamless 2,995.22

- APL Apollo 2,648.25

- Welspun Corp 2,394.99

- Jindal Saw 2,383.77

- Surya Roshni 1,097.97

- Srikalahasthi Pipes 772.86

- RMG Alloy Steel 618.85

- Gandhi Spl Tube 487.80

- Man Industries 327.77

- Good Luck 147.59

- JTL Infra 128.10

- Oil Country 60.32

- Surani Steel Tubes 43.0

- PSL 0.96 11.99

- Riddhi Steel and Tube 9.95

- Zenith Birla 9.45

- Umiya Tubes 9.29

- Prakash Steelag 5.43

- Rama Steel Tubes Rs.194 crores.

Ratnamani Metal

Excerpt from annual report:

Ratnamani Metals is the largest manufacturer of Stainless Steel Seamless and

Welded Pipes & Tubes in India. It is also India’s largest manufacturer of Nickel Alloy Pipes &

Tubes and Titanium Welded Tubes.

With fresh capacity expansion of 20,000 MT in Stainless Steel

Seamless, the total capacity will go up to 48,000 MT

Carbon Steel Pipes

L-SAW 40,000

H-SAW / Spiral - 1,80,000

ERW - 70,000

Circumferential Seam 60,000

Sub Total 3,50,000

3 Layer PE and FBE Coating 2.5 mln sq. mt.

Stainless Steel Seamless 8,000 MT

Stainless Steel Welded 20,000 MT

Surani Steel Ltd

Came out with an IPO recently. Current market cap is Rs.43 crores. Makes ERW pipes. Current capacity is 25,000 MT. Based on this, the market cap is about 1.75 crores per 1000 metric ton capacity. https://www.chittorgarh.com/ipo_review/surani-steel-ipo/2754/

IPO price was Rs.51-52. Currently at same price. Listed on NSE.

Umiya Tubes

Installed capacity of plant is 3000 MTPA. Mcap is 9.51 crores. So, about Rs.3.17 crores per 1000 MT. FY18 sales were Rs.45 crores. Been making losses for last few years. Promoter shareholding is 62%.

Riddhi Steel and Tube

Came out with IPO in September 2016 at Rs.38 per share. Current market price. Rs.12.60. Mcap is 9.95 crores. Capacity of ERW pipes is 100,000 MTPA. So about Rs.10 lakhs per 1000 MT.

Sales were Rs.270 crores in FY18. HY sales as of September 2018 were Rs.186 crores (Up from 101 crores in Sept 2017).

Jindal Saw

Total Capacity: More than 1 Million Metric Tons per Annum. Jindal Saw had sales of 7,334.91 and NP of Rs.386 crores in FY18. NPM is 5.26%. This rose from 1,123.30 crores and Rs.55.70 crores in FY04. Total networth was Rs.400 crores in FY04. This increased to 5,913 crores in FY18. This is a 15 fold increase in 14 years. In September 2000, the stock was at Rs.3.63. In September 2004, this was at Rs.37.50. Today it is at Rs.81.45. This company has had a complex history which required a whole thread to analyze.

Zenith Birla

This is a penny stock quoted at less than one rupee of a company that is making losses. So I’m not analyzing it.

APL Apollo Tubes

APL Apollo Tubes is estimated to have a market share of 14% to 15% in the ERW segment, ahead of DP Jindal Group (7%), Tata Steel (6%) and Surya Roshni (6%).

As of April, 2018 the company had an installed capacity of 2 million tonnes per annum. Mcap of 2,767.96 crores at CMP of Rs.1166. So per 1000 MT, the valuation is Rs.13.85 crores. The NPM for FY18 was 2.54%…

The top line and bottom line are now at 4,193.02 crores and Rs.112.69 crores in FY18. This was Rs.125 crores and Rs.1.68 crores in FY05. The networth in FY18 was 905.59 crores up from Rs.6.86 crores in FY05. This is a 130X jump approximately but their IPO came only in 2011. it listed at Rs.145. It touched a peak of Rs.2528.80 in January 2018 and is now at Rs.1166.

From the IPO DRHP

IN 1993 the Company initially setup a plant to manufacture ERW Black Pipes with an installed capacity of 6000 MT/Annum at Sikandarabad, Distt. Bulandsahar in the state of Uttar Pradesh. The plant started operations in October 1987. After achieving full utilization of the installed capacity, the Company subsequently expended its ERW Black Pipes manufacturing capacity to 24000 MT/Annum in the year 1989. After that Galvanized Plant was commissioned in March 1994 with an installed capacity of 16000 MT/Annum. Thereafter, the Company has achieved the following milestones by adding further to its manufacturing facilities to reach 4,90,000 in 2011. Now it is at 2 million tonnes.

Promoter stake has been declining. It was 40.64% in 2016 and is 37.25% as of December 2018. This needs to be looked into.

Man Industries

One of the largest manufacturers and exporters of LSAW and HSAW pipes in India. Capacity of 1,000,000 MT.

3 LPE/FBE coating capacity of 6.4 Million sq mt.

Cement wet coating capacity of 1.25 lakh cubic metres.

In the year 2000 their capacity was 100,000 MT.

https://www.moneycontrol.com/company-facts/manindustriesindia/history/MII#MII

There was an ownership dispute within the family that controls this company from 2009 to 2016. Apparently that is now resolved. That had to do with demerger.

Mcap is 333.20 crores.

Sales (FY18) 1572 Crores.

Mcap per 1000 MT is Rs.33 lakhs approx.

Last five years growth has been mediocre.

2014 sales were 1005 crores.

This was at Rs.3.88 in June 2005. Reached Rs.224 in October 2012. Now at Rs.58.

Networth has grown from 78.63 crores in March 2004 to 653.35 crores in FY18.

RMG Alloy Steel

Been making losses for last 4 years. Seems very overvalued at mcap of Rs.627 crores and 200,000 MT capacity. Not analyzing this.

https://www.bseindia.com/stock-share-price/financials/results/500365/#!#equity

Good luck India

Sales as of FY18 are 1303 crores, PAT is Rs.14.75 crores. Sales as of 2014 were Rs.1001 crores with PAT Rs.17.71 crores. Interest costs have gone from Rs.36 crores to Rs.56 crores in the same period. There seems to be some capacity expansion happening. The increase debt and depreciation also points to it. They are increasing capacity from 230,000 MTPA to 302,000 MTPA.

The proposed manufacturing facility is coming up at company’s already owned land in Gujarat with the total investment of Rs 74 crore which will met by debt and internal accruals/promoters contribution. The plant is expected to be commissioned by April 2018, the company said.

At mcap of Rs.152 crores, the mcap per 1000 MTPA is Rs.50 lakhs (Including proposed capacity addition).

Oil Country Tubular

There was a lockout in FY16 in February 2016. This was lifted in August 2016.

The Company lost major orders for Drill Pipe, Casing and Tubing during the period for which the Tenders are floated in the previous year.The Company was not able to effectively participate in the Tenders, as the delivery is critical and time bound with provision of liquidated damages for default on deliveries.With the commencement of the Operations from September, 2016 the Company submitted its bids for the Tenders floated which normally take four to six months for the techno-commercial evaluation and placement of Orders. The Company expects placement of Orders against these Tenders during the year 2017-18.

Sales were around Rs.11 crores in FY18 and Rs.7 crores in FY17 and mcap of Rs.66 crores.

It has current liabilities far exceeding current assets. I’m not going into an in-depth analysis of this company.

Welspun Corp

Flagship Company of the US$ 2.3 billion Welspun Group

Incorporated in 1995

Total pipe capacity of 2.425 million tonnes per annum (MTPA)

Total plate coil capacity of 1.5 million MTPA

2nd Largest Line Pipe Company in the World

Manufacturing Locations

- Anjar and Dahej in Gujarat, India

- Mandya in Karnataka, India

- Little Rock in Arkanasas, USA

- Damman in Saudi Arabia (one of the largest spiral pipe manufacturing facilities in the region)

Partner of Choice for more than 50 Oil & Gas Giants across the globe with a geographically diverse client base including Chevron, Exxon Mobil (Golden Pass Pipeline), Saudi Aramco, British Gas, Trans Canada

Anjar and Dahej Units officially certified with the SA 8000:2008 standards of Social Accountability

http://www.welspun.com/pipes.asp

This is one of the market leaders. At 2.45 million MTPA and mcap of 2,992 crores, the per 1000 MTPA valuation seems to be around Rs.1.20 crores.

FY18 sales were 5,259.89 crores. Mcap to sales is 0.55X approx.

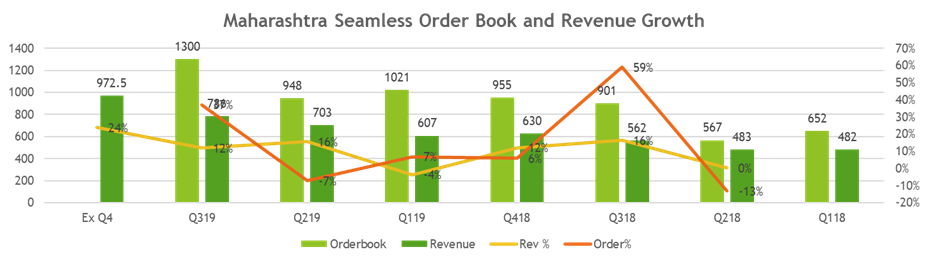

Maharashtra Seamless

Mcap is Rs.3290 crores.

FY18 sales were Rs.2160 crores.

OPM was 16.89%

PAT was Rs.198.42 crores.

Seamless pipes have higher profit margins than ERW pipes.

Current PE is 15-16.

March FY04 sales were Rs.555.29 crores and PAT was Rs.71.46 crores.

For last ten years sales have been about Rs.1500-2000 crores every year. Stagnant.

Promoter stake is 61.78%

MaharashtraSeamlessLtd(MSL) Seamless pipes capacity is 550,000 MTPA

and ERW pipes capacity is 200,000 MTPA

http://www.jindal.com/msl/pdf/Initiating-Coverage-on-MSL-by-India-Nivesh.pdf

I am not researching this company further given its stagnant growth in the last decade.

PSL

This has a capacity of 1 million MTPA. That is huge.

However the mcap is only Rs.13 crores.

It is a penny stock trading at about 1 rupee per share of face value Rs.10.

From FY15 it started making losses and its networth is -2400 crores now.

I’m not researching this further.

Srikalahasthi Pipes

Mcap of Rs.848 crores.

FY18 sales of Rs.1506 crores. PAT of Rs.147 crores.

They are also into cement. They seem to have good liquidity.

Requires detailed analysis.

*Rama Steel Tubes

FY18 sales were Rs.340 crores. FY19 9 months sales have been Rs.290 crores. If the same trend is maintained can expect full year sales to be around Rs.400 crores with net profit around Rs.6 crores. This is a net profit margin of about 2%. EPS will be around Rs.2.76. PE is around 40. Growth in sales and profits has been poor so far. FY16 sales were Rs.243 crores with net profit of Rs.6 crores. This points to sliding margins. EBIDTA was Rs.24.4 crores in FY16, Rs.17.7 crores in FY18 and Rs.12.5 crores in 9 months this year. Interest costs have gone up sharply in December 18 quarter probably because of loans taken for expansion. Company is expanding capacity.

I will keep editing this post with more information about each company’s existing capacity, expansion, leverage etc. Feel free to contribute.