Indian Diagnostics Report (Phillip Capital Research)

Industry Overview:

-Key reasons for industry tailwinds:

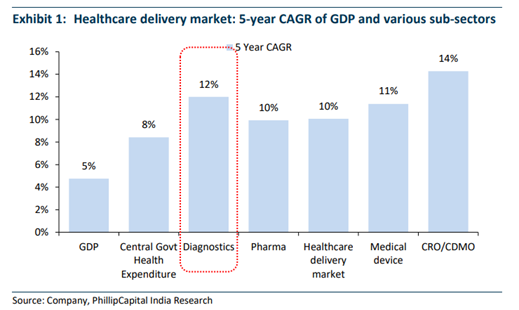

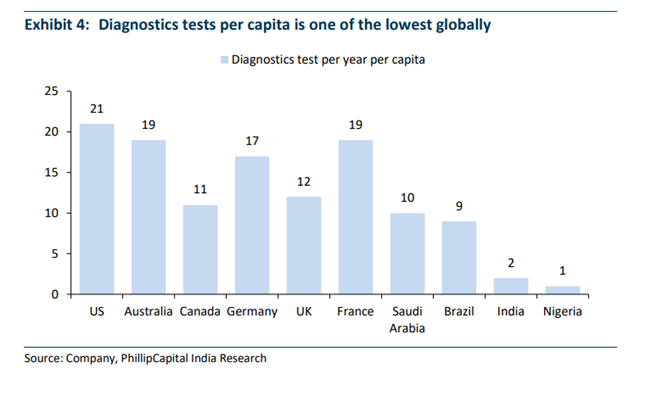

o Significant under-penetration of diagnostic services (6% of healthcare market)

o Low organize market share (15% only) which will increase

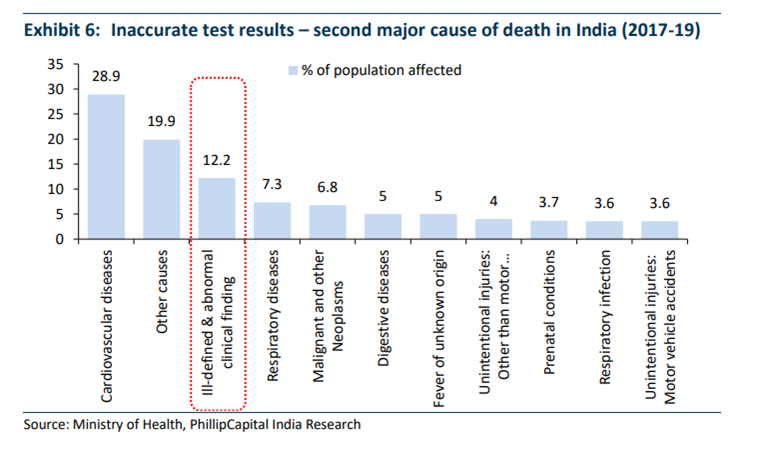

o Low lab accreditation and misdiagnosis (12% causes of death)

o Fast-growing trend of preventive diagnosis (12% Share)

o Initiatives by Govt. of India

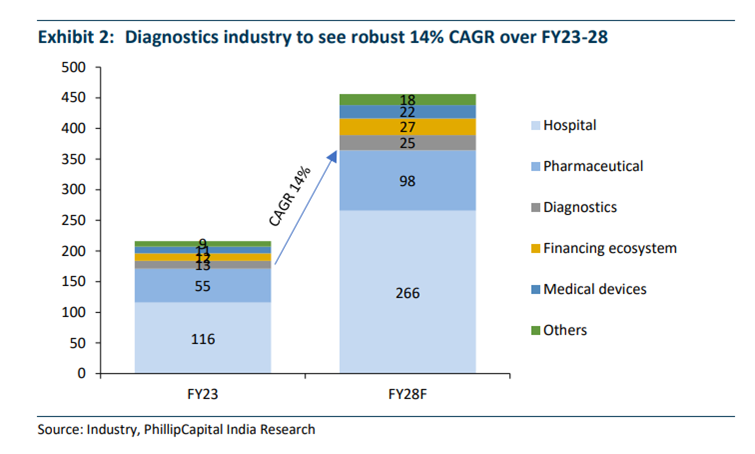

- Organize diagnostics is estimated to grow at an 14% rate over FY23-28, set to outpace industry growth

Industry fragmentation based on Diagnosis Tests:

Current market share distribution in diagnostic industry:

-

Organized Chain – 15%

-

Hospitals: 37%

-

Standalone Centres: 48%

Geographical mix of test volumes:

-

Rural Share: 66%

-

Urban Share: 34%

This highlights vast untapped potential for organized player’s expansion

Structure of pathology market:

- Specialized tests have relatively smaller pie (20% of pathology market) but are growing at a high pace led by an aging population and awareness

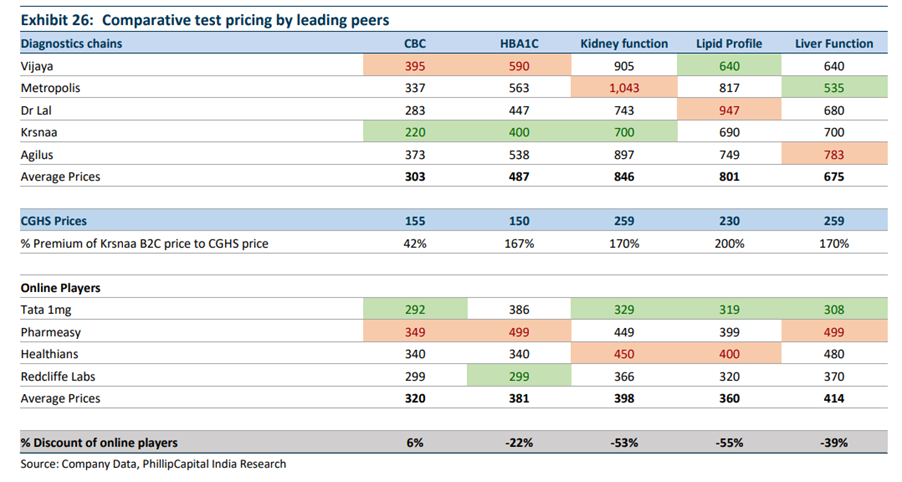

Comparative Test Pricing by leading peers in Pathalogy Market:

-

Premium and high price players: Metropolis in Mumbai & Hyderabad, Dr.Lal and Agilus in Delhi, Vijaya in Hyderabad

-

Krsnaa Diagnostics operate at a lower cost as compared to peers

-

Online players usually have less price as compared to offline players and have uniform pricing across states

![]()

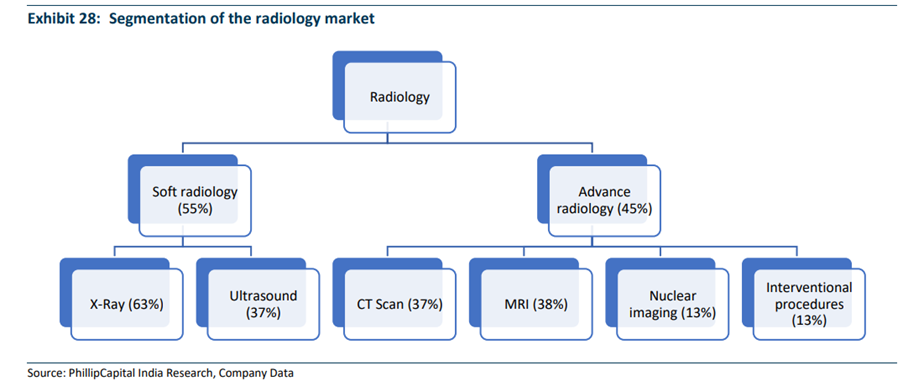

Structure of Radiology Market:

o Soft Radiology: 55% of market; basic tests like X-Ray, Ultrasound

o Advance Radiology: 45% of market; CT Scan, MRI, Nuclear Imaging, etc.

Geographical Distribution of Indian Diagnostics:

-

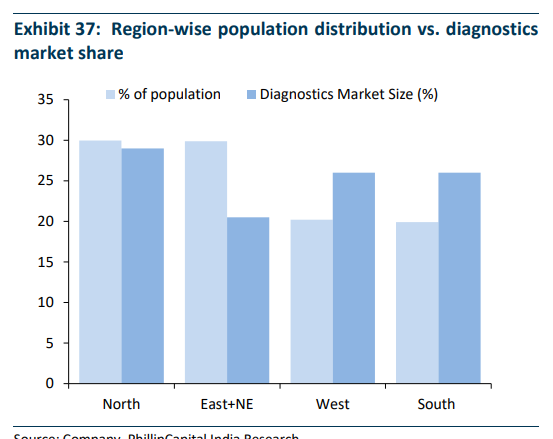

North India leads the market due to high population (28-30%), Dr. Lal has positioned itself

-

South India has the best infrastructure and disease prevalence (25-27%); highest bed density, doctors,etc

-

Western India has the most premium market with around 70% of India’s total NCD (Non Communicable Diseases), which makes it attractive for diagnostics

-

Eastern India lags behind and has highest growth opportunity due to under-penetration

Business Models for Positioning in this Market:

o Nature of Service : Only pathology test with or without minimal soft radiology

o Rationale: For the mass, asset light, lower capital intensive

o Listed Peers (Best to least positioned): Dr. Lal, Metropolis, Thyrocare, Agilus

o Nature of Service: Pathology & Radiology (more focused)

o Rationale: Capital Intensive, less competitive, higher growth, B2C oriented

o Listed Peers (Best to least positioned): Vijaya, Suraksha

o Nature of Service: Pathology & Radiology in govt. hospitals

o Rationale: Scale of operation, high volumes, test realizations are lower, less capital outlay

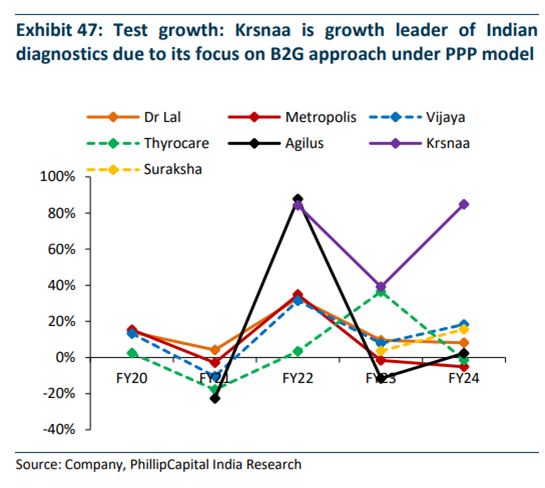

o Listed Peers (Best to least positioned): Krsnaa is the leader, second largest volume in industry (after Dr. Lal), second highest number of tests per patient (after suraksha), largest radiology revenue

Story from Charts:

-

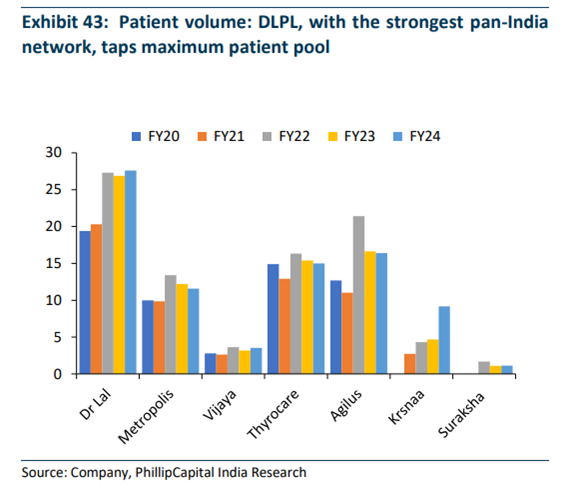

DLPL has highest network and patient pool

-

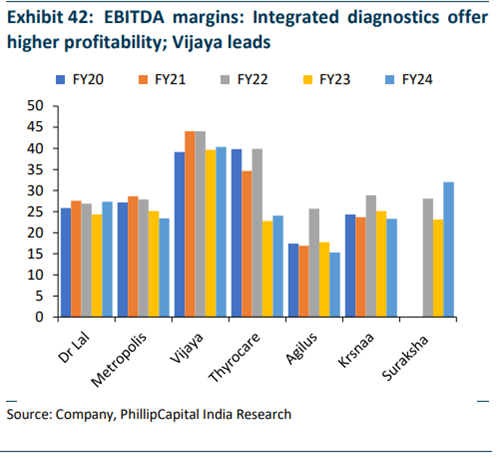

Vijaya leads in margins; Integrated diagnostics offer higher profitability

-

Krsnaa is leading in test growth due to its focus on B2G

-

DLPL leads in revenue growth in Pathology with 12% CAGR over last 5 years

-

Krsnaa leads in revenue growth in Radiology with 30% CAGR