Stallion India Fluorochemicals Limited

About the company:

- Stallion works in the fluorochemicals space, dealing with refrigerant gases, specialty gases, semiconductor gases, next-gen refrigerants (HFOs), and even liquid helium.

- Their gases find applications in a wide range of industries, including automotive, pharmaceuticals, fire safety, defence, power, solar, and semiconductors.

- So far, their focus has mainly been on formulation, blending, debulking, and distribution. Now, they’re moving into backward integration, manufacturing R-32, to cut down on imports and boost margins.

Customers:

- OEMs: BlueStar, Voltas, Daikin, LG, Amber, etc. (approved vendor).

- Aftermarket Service Providers & Distributors: which together form 80% of refrigerant sales.

- Industrial Users of Speciality Gases: across auto, pharma, defence, fire safety, power, semiconductor, solar, and fibre optics industries.

Details of expansion plans:

1. Rajasthan (Bhilwara) R-32 Plant

- Products:

- R-32 (refrigerant gas): base molecule.

- Will also support HFO blends (R-410A, 404A, 454B, 513A, etc.) since all need 50-60% R-32.

- Capacity:

- Stage 1: 5,000 tons.

- Stage 2: Another 5,000 tons (total 10,000 tons).

- Start Date:

- Land already acquired; construction in progress.

- Commercial production expected mid-2026.

2. Andhra Pradesh (Mambattu) - HFO & Specialty Gas Facility

- Products:

- HFO refrigerants & blends (next-gen, low GWP, e.g., 454B, 513A).

- Semiconductor gases (helium, argon, other high-purity gases).

- Hydrocarbon handling facility also included.

- Capacity:

- Originally a 5-tank facility, scaled up to a 10-tank facility.

- Also includes a semiconductor gas facility similar to Khalapur.

- Start Date:

- Construction ongoing in 2025.

- Expected completion by Oct 2025; operations in late 2025/early 2026.

- Benefits:

- Close to Southern OEM hub (Voltas, BlueStar, Daikin, etc. nearby).

- First mover in HFO blending before industry shifts in 2026-27 due to global quotas.

3. Maharashtra (Khalapur) - Semiconductor & Specialty Gases

- Products:

- Semiconductor gases, liquid helium, high-purity specialty gases.

- Designed to handle 300-bar cylinders (latest global standard, vs. 200-bar earlier).

- Capacity:

- Full blending + debulking facility for semiconductor gases.

- Start Date:

- Civil work completed, machinery ordered.

- Expected commissioning by late 2025.

- Benefits:

- Semiconductor ecosystem in India & globally is expected to grow at a strong double-digit CAGR.

- Higher entry barrier (takes 2-3 years for customer approval once product is qualified); sticky revenue

Management:

Shazad Sheriar RustomJi started this business as a first-generation entrepreneur when he was 22 years old. He has been running and growing it successfully for the past 32 years.

Market Information:

- In developed products, the aftermarket is 80-85% and OEMs are 15%.

- In new products like HFO, OEM requirement is almost 80% or 90% and the aftermarket is 10%.

- As per management, India has a production capacity of 30,000 tons per year in R-32. 15K tons are used internally, and the rest is exported.

Risks:

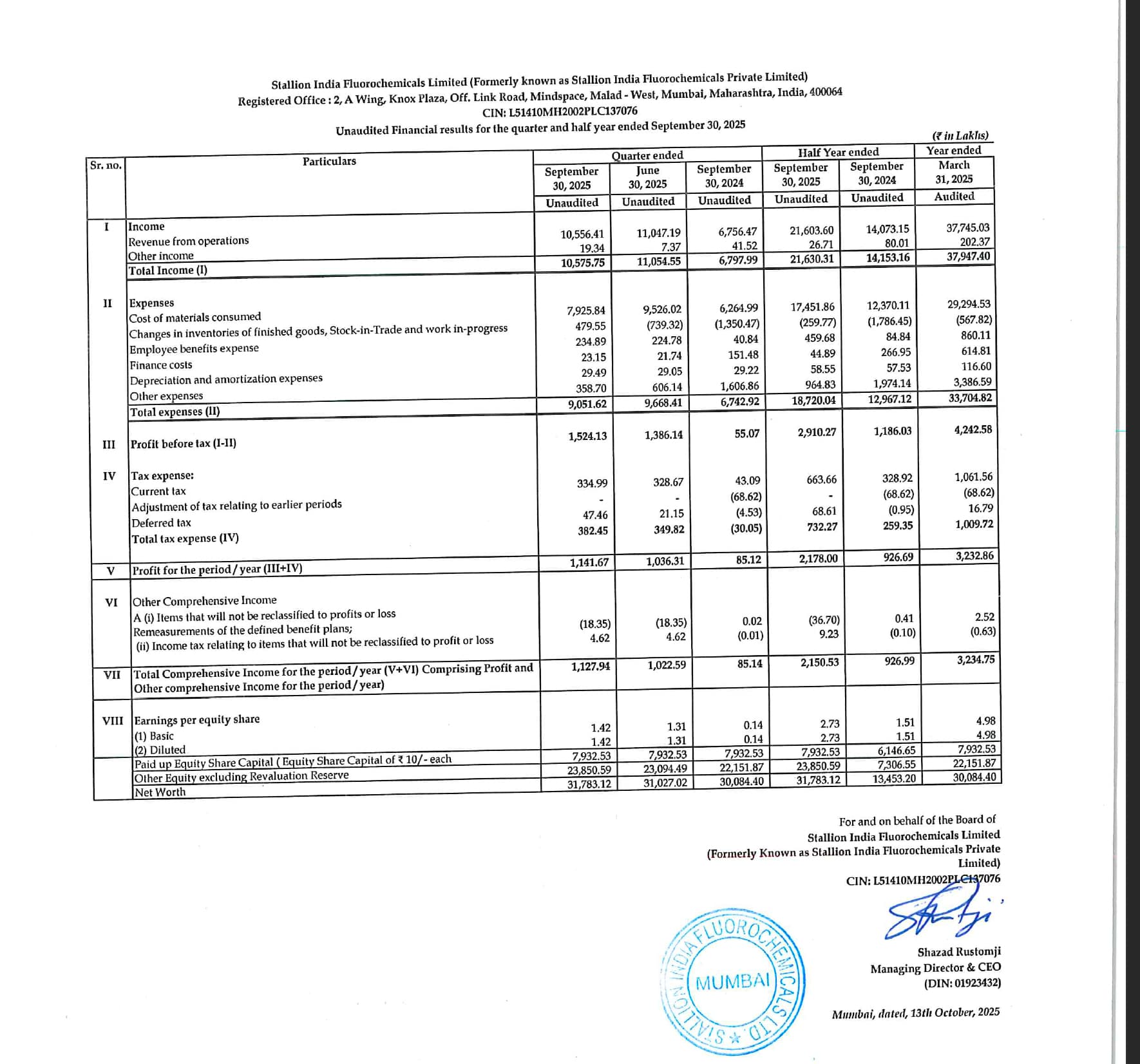

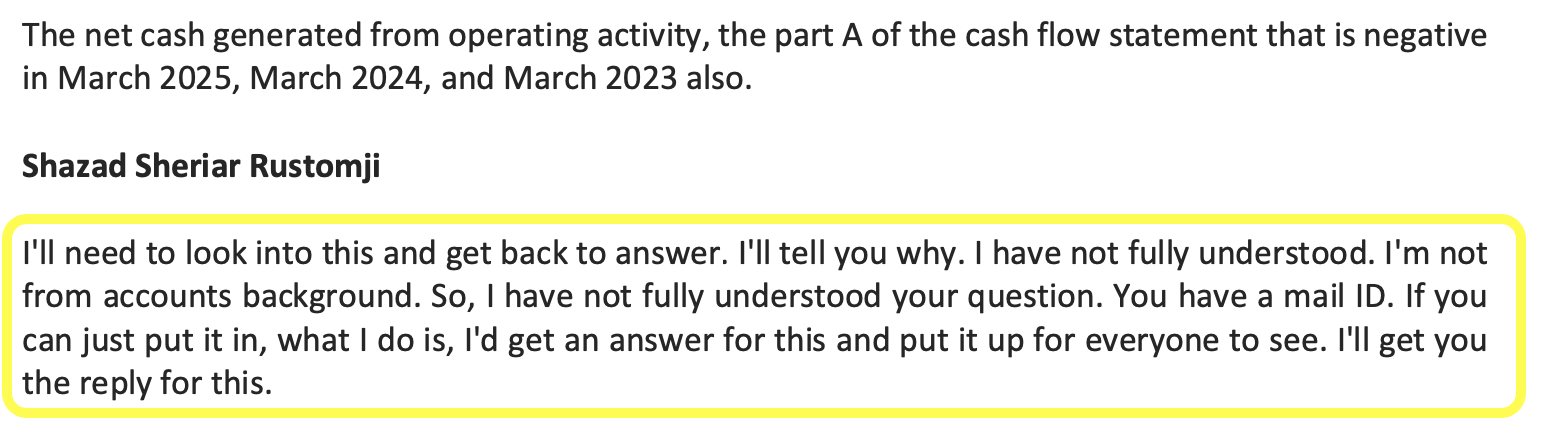

- Negative cash flows in the last three years

- The company has never done molecule manufacturing, needs to be seen if they can execute.

- A lot of company money is tied up in inventory and receivables, and with such aggressive plans, it might face a cash crunch.

- Management gave a below response when asked about negative cash flow

Investment Thesis:

- Increase in PAT margins to 17-18% because of backwards-integrated manufacturing.

- The company has an ambitious target of 2500 cr topline by 2030.

- Even if the company achieves 2000 cr topline at 15% Net Profit Margin, with a modest PE of 20, it will have 6000 cr MCAP. Roughly 6x from here. A 43% CAGR return in 5 years.

Thanks to @satishwe for sharing this company idea.

Current MCAP: 1154 cr

Disclosure: Invested with a small allocation