Q2 FY26 Concall Highlights

Key Business Highlights

-

SRM Contractors is an EPC contractor which specializes in avalanche protection, RE Wall, Hill slope soil stabilization, tunnel widening, bridge, tunnels, roads, etc.

-

Revenue contribution from road is 48% and slope stabilization is 52%.

-

According to management they only focus on high margin center projects. And avoid state projects.

-

State projects usually have delayed payment problem, which is not present in center projects.

-

They are also expanding into North East region in collaboration with BRO.

-

SRM is doing a capex of 70cr out of which 48cr of capex has already been completed in H1 FY26.

-

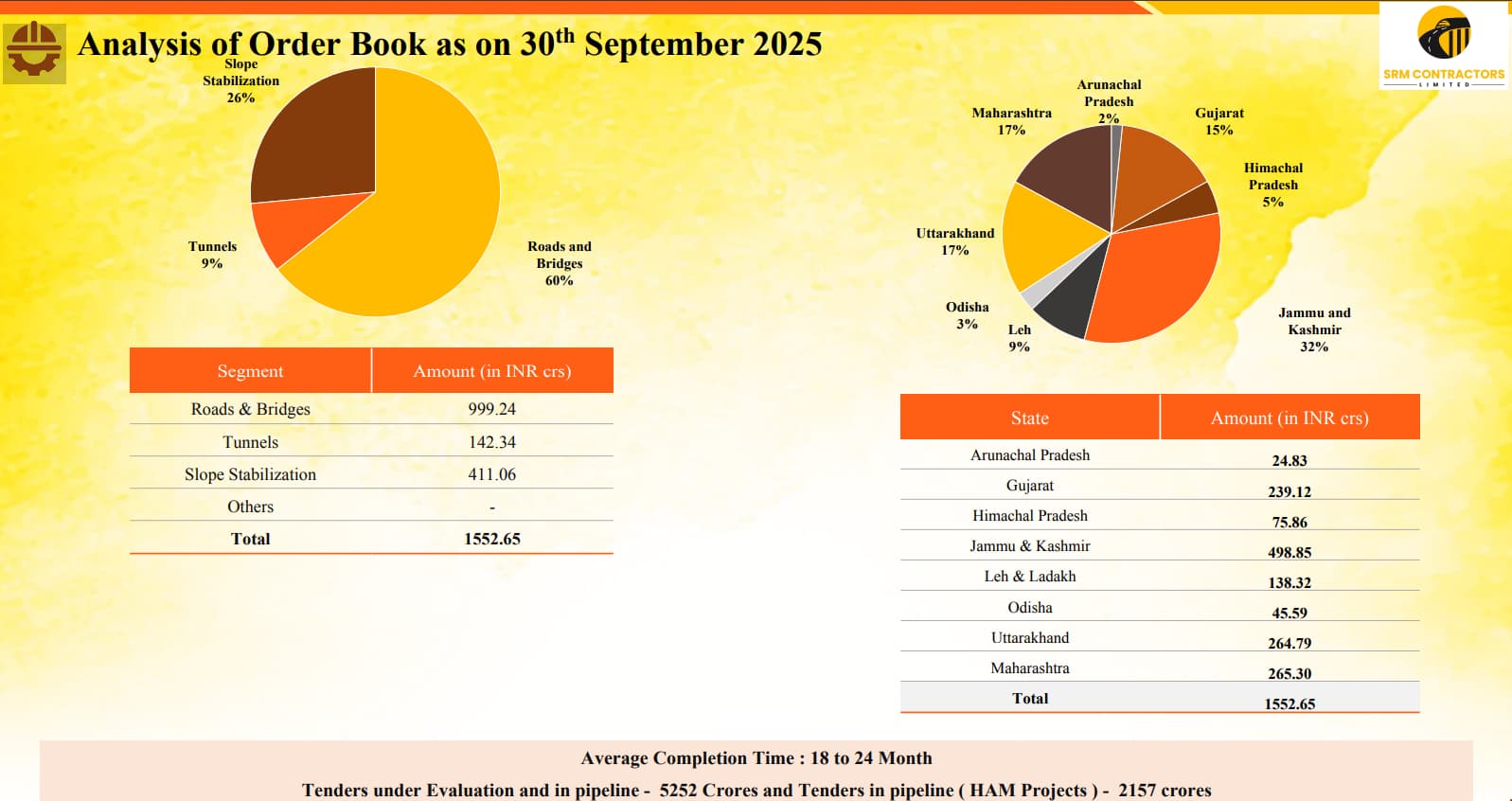

Order book

-

SRM 2 years back was limited to J&K, Himachal Pradesh, Uttarakhand, etc with 200 odd cr of order book . Today they have expanded to Maharashtra, Gujarat, Orissa, etc, with order book now stands at 1552.65cr.

Acquisition

-

SRM has already acquired Maccaferri Infrastructure Private Limited (MIPL) in Q1 FY26.

-

According to management due some technical glitch the share were not showing in Demat. Therefore, have not reported back then.

-

From Q3 MIPL’s revenue will be consolidated in SRM results.

-

MIPL business operation is related to slope stabilization which is very similar to SRM. The margin profile are also same.

-

MIPL is an Indian subsidiary of parent, Officine Maccaferri, Italy. Their business model is very simple.

-

Officine Maccaferi Italy is a construction material supplier and has presence in 100+ countries. In some countries they have subsidiaries which execute project in local level.

-

SRM is doing a strategic partnership with Maccaferi Italy. Therefore, wherever Maccaferi Italy does not have local presence. SRM will be there local project executor in that country.

-

This partnership will give SRM global presence. SRM has already established their office in Uganda and UAE. But can take 1-2 years to become significant.

-

This collaboration brings SRM three key advantages. Firstly, improved road stabilization and reinforcement through cutting-edge geosynthetic technologies that enhance load-bearing

capacity and durability. Second, access and ability to bid for global infrastructure projects.

And thirdly, sustainable cost-efficient construction solutions that optimize resource use and

ensure long-term infrastructure resilience.

Guidance

-

Management is guiding revenue of 800-1000cr from SRM and 300-400cr from MIPL for FY26.

-

Order book can grow to 2000+cr in 2026.