About Company-

SRM Contractors Limited incorporated in 2008, is into EPC ( Engineering, Procurement, and Construction), PBMC ( Performance Based Maintenance Contract) and sub-contracting assignments. Company majorly operates in Jammu & Kashmir region but recently diversifying into other states like Gujarat, Himachal Pradesh, etc. Company has expertise in constructing roads, tunnels and slope stabilization projects in very difficult terrain. Company has also done joint venture and sub contracting with major EPC players like ECC, Patel Engineering Ltd, Gammon, etc.

Completed & Ongoing Projects-

Reasi slope stabilization project (Completed)

T5 tunnel in J&K (Completed)

Chenani Sudhmahadev Road (Completed)

Tutan Di Khui Road (On-going)

Some other on-going projects are

-

Multiple road realignment project awarded by Border Road Onganization under project Vijayak in 2023 of value 205.68 Cr.

-

Bridge construction project awarded by Border Road Onganization in 2023 of value 202.3 Cr.

-

EPC project for upgradation and strengthening of Nashri-Chenani section awarded by National Highway Authority of India on 15 July 2024 of value 278.48 Cr.

-

EPC project for construction of slope stabilization and protection of Parwanoo-Solan section NH-55 awarded by NHAI on 22 July 2024 of value 118.53 Cr.

-

PBMC project for strengthening and maintenance of Jetpur-Somnath section excluding Junagarh Bypass (103Kms) in the state of Gujarat awarded by NHAI on 29 July 2024 of value 171.24 Cr.

As on 31 January 2024 according to their RHP, the order book of company stands at 720.14 Cr. And recently company has been awarded 3 new projects by NHAI whose combined value is 568.25 Cr. Therefore, total order book stands at 1288.39 Cr.

IPO-

SRM Contractors in March of 2024, have brought mainboard IPO to raise 130.2 Cr. Purpose of raising money from market are

- 31.5 Cr to fund capital expenditure.

- 10 Cr to fully or partly prepayment of outstanding secured debt.

- 46 Cr to fund working capital requirement.

- 12 Cr for investment in joint venture projects.

- Rest amount for general corporate purposes.

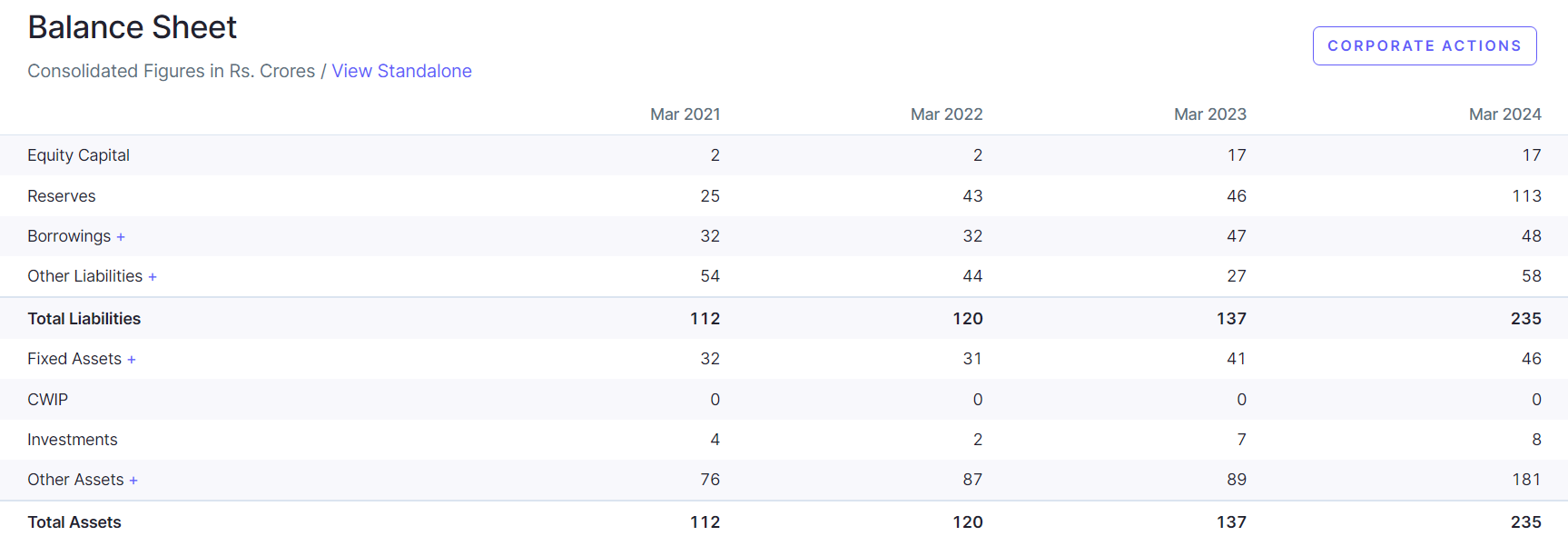

Financial Health-

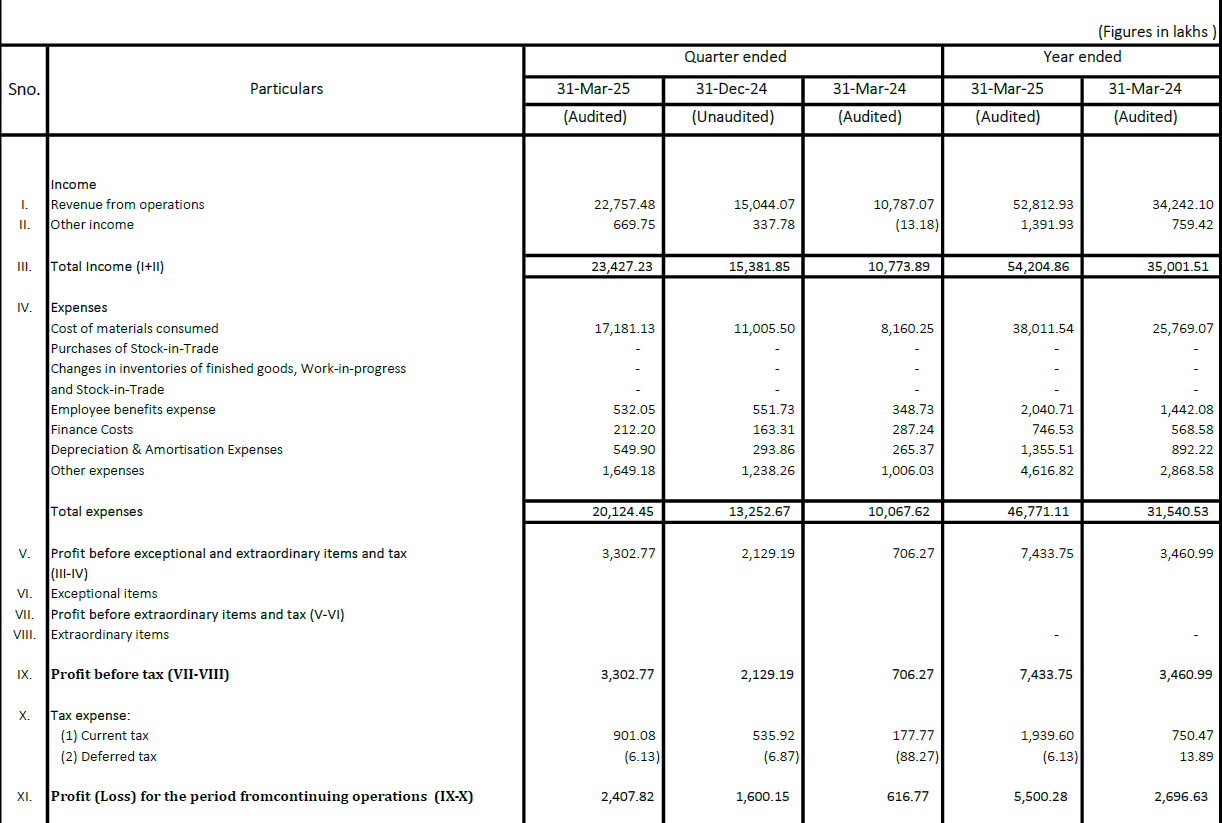

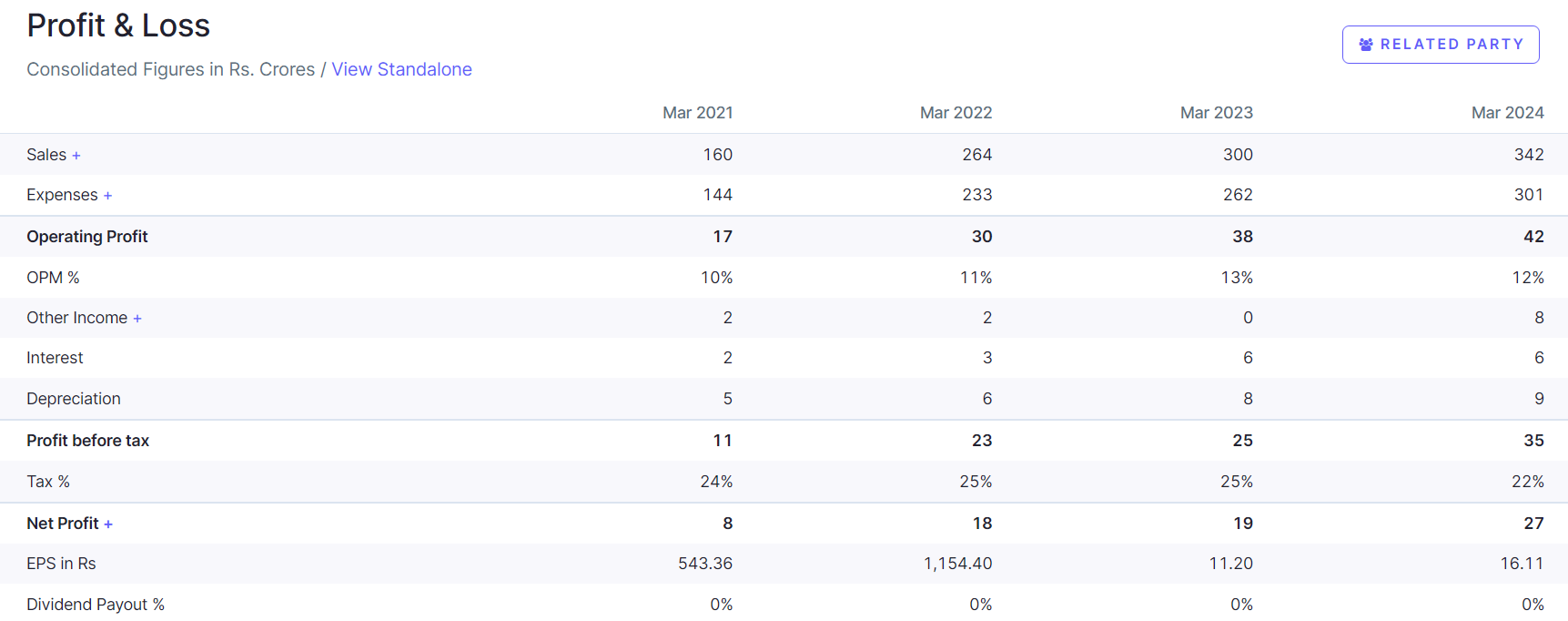

SRM contractors ltd have shown healthy revenue growth from 160 Cr to 340 Cr within the span of 3 years, i.e, at the CAGR of 28.8%. Similarly in same time frame, profits have grown from 8 Cr to 27 Cr at 50% CAGR. Operating margin have remained stable within 10-13% range. Historically, company has shown 5-6% PAT margin. But in FY24, PAT margin has jumped to 12% due other income component.

Company’s debt is very sustainable. Recently, company has raised money through IPO and proceeds are going to be used in prepayment of some debt. As of FY24 debt to equity ratio stands at 0.37. ROE and ROCE both are at 28%. Company’s debtor day and cash conversion cycle are 33 and 27 respectively.

For technical analysis I have used vstop and ADX in weekly time frame which can be viewed by clicking given like - #SRM_Contractors All time high breakout for NSE:SRM by TINTIN2718 — TradingView India

Clientele-

Strengths-

-

Management has a proven track record of executing projects successfully in harsh and difficult terrains like in Himalayas of J&K, Himachal Pradesh.

-

In past company has done joint ventures and sub-contracting with reputed player like HCC, Patel engineering Ltd, Gammon,etc.

-

As government is pushing for infrastructure projects especially in border areas. This presents a huge opportunity for future revenue potential.

-

They have a very healthy order book of 1288.39 Cr which is twice the Market cap of company as on July 2024.

-

Company has won major projects from the likes of Border Road Organization, National Highways & Infrastructure Development Corporation Limited, Indian Railways, etc.

Weakness-

-

This type of business requires very high capital expenditure. Various types of equipment and vehicles are required to complete projects on time like drill machines, compactors, excavator, trucks, etc.

-

Projects are awarded to the company by bidding process, which is very competitive in nature. If company is not able win new tenders, it can be detrimental for future revenue.

-

Company is highly dependent on government policy of capital expenditure on road, tunnels, bridges, rail tracks, etc. If government changes its policy in future then revenue can get impacted in a negative way.

-

Highly concentrated in a single geography i.e, Jammu & Kashmir. Though company is trying to expand to other states like Gujarat. Still it’s majority of the projects are from Jammu & Kashmir state.

Disc- Already Invested and not a buy or sell recommendation.