Recent example - JSPL & SREI Equipment Finance deal where the company sold the oxygen plant at Angul to SREI Equipment Finance for the consideration of 1121 crores and then leased it back.

There was an interesting question in conf call regarding IPO for equipment finance business which accounts for significant revenue and is growth engine for the company.

Even this quarters results, it was consolidated numbers which look good on top and bottom line. Standalone topline was tad lower YoY.

Company plans to hold 75 % share in the listed entity, and is not in favour of Demerger since it takes a long time.

With this it will be becoming more like a holding company and we all know what valuations holding companies get.

This could be the reason for recent beating stock price got in market.

Any views on this ?

It also depends on the pricing of IPO. The markets are overheated and some of the companies have been very successful in selling their IPO at at amazing valuation. If SREI manages to do that, it would be good for the stock in short term.

I tried to find out about Sunrise Polycon as mentioned in above tweet. Anyone having knowledge on this may please reply.

The company is trading at almost 1x book, seems quite reasonably priced.

1 Like

Quarterly chart of srei…the price has finally touched the lower median line after a long time…median lines act as magnets…they attract the price bars and then repel them too…most probably this median line too will repel the stock price and propel it higher…the next price bar on quarterly charts may be a long greeen price bar…I have.seen such a thing happen in soo many stocks…inclusing Aksh, Axis cades, Aurion pro etc…

chart shows that there may not be a bottom less fall in srei infra…and that eventually the stock is headed towards 300+ level…and even if it falls to 70-75 levels, it gets better and better…

As it is…on fundamentals, this company has been coming out with good results…and is very well placed in that regard

@Mehnazfatima ,this company is on IPO spree for its major cash earning entities. Though they will hold major share in those IPOed companies however with that it will become holding company.

And we all know how holding companies are discounted by market.

What would be the growth triggers as per your understanding ?

61.8% Fibonacci retracement level is 71/72. If it retraces from that level, looking good if you look at the elliott waves.

Disc: Not invested. Looking to enter.

2 Likes

Forming a nice cup & handle in the long-term chart.

Disc: Not invested. Looking to enter.

Yes with eliott wave this cup handle formation looks convincing…

There was a classical cup before actually…

Disclaimer… Interested and watching

1 Like

If I remember correctly the company is coming out with an IPO of Srei Equipment finance - 25% equity of the company will be offered for 2000cr which values this business along at 8000cr whereas present value of whole company as of date is 4000cr.

I could not understand why so?

Yes, you are right. The plan is to issue 25% to public and raise 2000cr. This means they value this business at 8000cr. They value one Sahaj Kendra at 5lacs. For 100,000 kendras, that’s 5000cr. (I don’t know the exact count of kendras, I picked the number from their website which they have mentioned as FY18 target). The value of two business verticals themselves is 3 times more than current mcap of SREI Infra.

BPLG sold its 50% stake in SREI Equipment Finance to SREI in lieu of 5% equity in the parent company SREI Infra Finance.

By that calculation, 100% stake in SREI Equipment Finance is equal to 10% stake in SREI Infra Finance.

Now 25% equity shares of SREI Equipment Finance is planned to be issued for 2000cr, which means whole SREI Equipment Finance is valued at 8000cr.

By that logic 100% stake in SREI Equipment Fin = 10% stake in SREI Infra Finance = 8000cr.

And SREI Infra Finance value must be 80,000cr. Current mcap is 4000cr.

Does anyone know why it’s trading at such huge discount?

Disc: Not invested. Interested.

Haven’t been looking at valuations of proposed subsidiary IPO, but the value in SREI Infra is a no brainer. I had added in recent correction and its now the biggest holding in my PF.

Thesis:

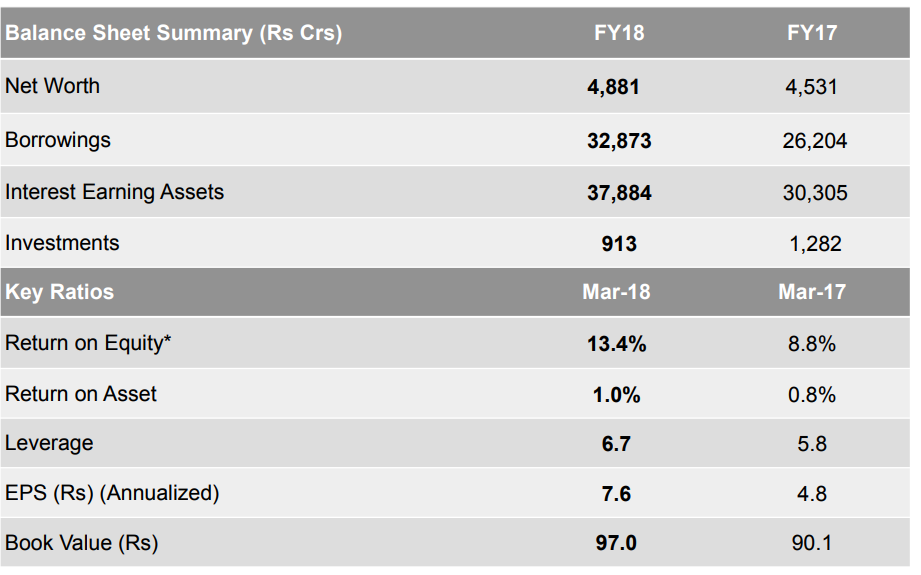

BVPS is ~Rs. 97/ share

RoE went up to over 10% this quarter with increasing disbursements, values stock at <8-9x P/E ratio if we annualized trailing quarter result (there is no major seasonality as it is a lending type of business)

NPAs have been steadily decreasing, and lower provisions should further enhance EBITDA

Cyclically speaking, it looks like the trough in the Infra sector has already been seen in 13/14 and disbursement growth is evident of pickup in Infra activity. This means a cycle of higher disbursements and lower NPAs, as compared to the lower disbursements and higher NPA’s seen in the past. I believe that the governments push to revitalize road projects should fructify, leading to high disbursement growth.

This is a business with high operating leverage and low current-financial leverage (historically speaking). Its simple math that higher leverage will lead to higher RoE in a financial institution, and leverage has been low in recent years due to higher NPA’s, and slower disbursement growth. In fact, SREI’s assets have remained almost constant as equity has increased (from profits), and thus leverage has decreased. This was due to lower Infra activity, such as lower CV sales which SREI finances.

(Srei Investor presentation)

As CV demand picks up, and SREI asset book increases, its leverage will increase, leading to higher ROE’s. Also, the business has high fixed costs, such as employees and credit monitoring costs, which should lead to operating leverage, leading to additionally higher RoE’s. Thus ROE’s could increase to 15-16% levels, which could lead to a re-rating as loan book would also grow at ~20%. Srei could trade for 2x P/BV which is ~Rs. 220 a share in a year, almost a triple from its CMP.

Additionally, even if PB rerating doesn’t happen, its stock could grow EPS ~20%-30% in the meantime, with hidden optionalities like a subsidiary IPO, BOT assets sale, and Sahaj Centre value-unlocking.

Disc: Largest holding in my PF

Additionally, PSU banks still form a HUGE part of the Infra financing space, and as they curtail loan growth due to higher NPA’s and lower equity, Infra players will find it much more useful to lease vehicles from SREI rather than take out large project loans from PSU banks.

I am also personally very bullish on lower transportation costs and higher demand due to E-Commerce playing out in logistics, as its a proxy for E-Commerce boom, and I think a major part of the CV/Truck demand might come from that side. SREI once agains benefits from larger CV sales.

Valuation change over time. Since BPLG sold stake in Equipment finance business, sector has really picked-up pace. Look what happened to Action construction equipment.

I checked the history of group they had some dealings with Kingfisher group but I could not find anything bad, does market has any negativity about the group corporate governance.

Also I find their presentation very confusing. They do not publish their non-performing assets at consolidated level.

Do company has some hidden infra skeleton in closet, which market is aware-off and we as community are not??

Disclosure -

Invested. This is no buy/sell recommendation. Views are surly biased. This is just an expression.

1 Like

The Kanoria’s don’t enjoy a great reputation in the markets, which could be the reason for muted valuation of the stock. There are two issues in the past that I am aware of are:

However, these issues took place some time back. In my personal opinion their governance standards have improved since then.

Disc:Invested

Regards

SJ

4 Likes

This indeed looks extremely interesting. Mar17 book value is Rs98 and stock at Rs78. Company has delivered 234% PAT growth in FY17 followed by 60%, 49% and 65% PAT growth in 1Q, 2Q and 3Q.

1 Like

Market is yet to fully give weight to SREI Infra’s improvement in operating earnings and NPA’s. I think increasing disbursements will lead to higher leverage and RoE as provisions finally abate and SREI can take on more leverage.

Balance sheet cleanup for an NBFC usually takes 2-3 years atleast, given the pain we have seen since 2013/4, there can’t be too much more left with most of the Infra recognition cycle behind SREI. I think for cyclical plays like this, one must keep a longer horizon and have stomach for volatility. Lower slippages in Q4 despite a large amount of NPA identified this quarter in the overall system augers well and SREI is likely to be a multibagger in the next couple years. The signs of a turnaround are everywhere in this stock, and the balance sheet improvement will finally show in the income statement, causing stock re-rating.

Disc. Invested, largest position in PF, may be biased.

2 Likes

SREI INFRASTRUCTURE FINANCE LTD. FY18 Annual Report Notes

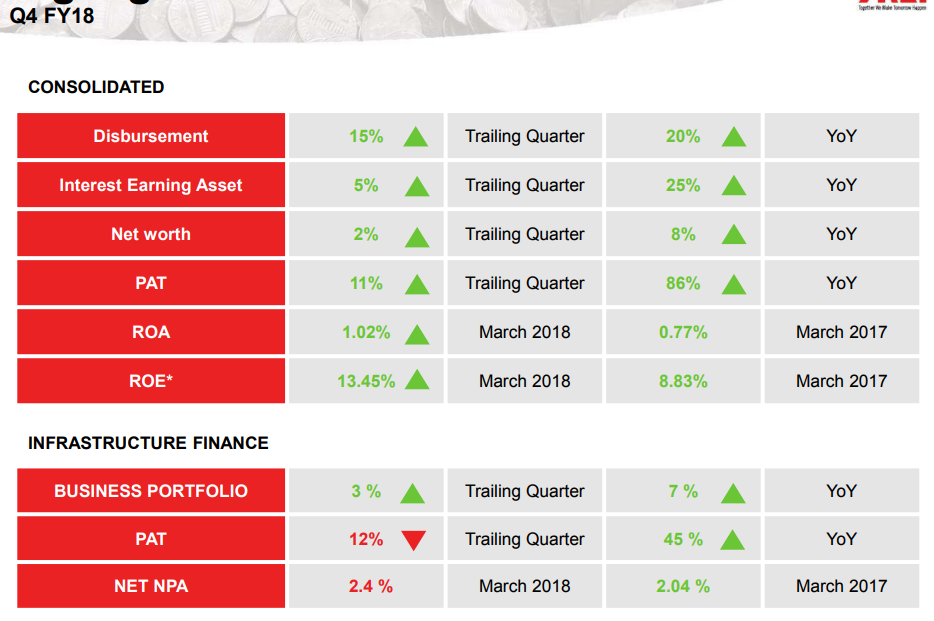

- During the year under review, your Company posted a consolidated income of Rs. 5,262 crore (an increase of 12 per cent over last fiscal’s Rs. 4,681 crore) and registered a consolidated net profit of Rs. 385 crore (a 58 per cent jump over last year’s Rs. 243 crore). It would be pertinent to indicate that our construction equipment segment reported robust growth during the year under review.

- Your Company’s consolidated disbursements stood at Rs. 22,726 crore (Rs. 17604 cr in FY17), registering a 29 per cent year-on-year growth. Disbursement recorded by the equipment financing business was Rs. 16,990 crore whereas that for infrastructure finance was Rs. 5,736 crore in 2017-18.

- Income from the fund-based businesses increased by about 26% from Rs. 3,904 crore in 2016-17 to Rs. 4,938 crore in 2017-18. The Company’s fee-based income was Rs. 58 crore in 2017-18 as against Rs. 33 crore in 2016-17. Income from investments decreased to Rs. 26 crore in 2017-18 as against Rs. 529 crore in 2016-17. Income from investments could vary from year to year as these would depend on the timing of the sale of such investments. Equipment rental income contribution to total income increased to Rs. 211 crore in 2017-18 as against Rs. 165 crore in 2016-17. The Group’s noncore income was Rs. 30 crore in 2017- 18 as against Rs. 35 crore in 2016-17.

- The consolidated net worth of your Company, at Rs. 4,881 crore, registered an 8 per cent growth. Your Company’s consolidated assets under management stood at Rs. 47,050 crore at the end of the year under review, registering a 26 per cent year-on-year growth.

- In addition, on a consolidated basis, the gross non-performing loans (NPL) came down from 2.93 per cent to 2.40 per cent, while the net NPL decreased from 2.00 per cent to 1.75 per cent.

- During the year under review, for its road portfolio, Bharat Road Network Ltd., your Company raised fresh capital of Rs. 600 crore through an IPO, the proceeds of which will be utilized for growth capital and for strengthening the SPV financials. The management is now working towards a strategic divestment, this time in the equipment financing portfolio. The resources thus mobilized will be used for catering to the new demand emanating from the infrastructure space and thus consolidating your Company’s leadership in the market.

- We intend to continue to leverage our experience in CME financing and expand our business by further developing and growing relatively new lines of business such as financing of certain CME equipment categories such as Tippers, MHE, and expanding certain verticals such as Used equipment (within CME), IT and allied equipment, medical equipment, farming equipment and other assets.

- Even during the downturn between 2012 and 2016, when banks struggled with NPAs, our peak NPA did not exceed 4.75 per cent.

- our cost of operations as a proportion of revenues reduced from 19.32 per cent in 2010- 11 to 12.60 per cent in 2017-18.

- SREI was awarded the Golden Peacock Award in 2017 for excellence in corporate governance in the financial services sector in India.

- Company computed the capital-torisk-weighted assets ratio as on March 31, 2018 to be 17.60 per cent, while Tier-I capital/net owned funds stood at 13.71 per cent, above the minimum regulatory requirements of 15 per cent and 10 per cent, respectively.

- Total Debt: Rs. 32784 cr., Short term = Rs. 19638 cr and Long term = Rs. 13146 cr.

- Direct Tax paid was Rs. 525 cr during the year as compared to Rs. 192 cr booked in P&L A/c.

- Srei Equipment Finance Ltd. forms 51.89% of total capital employed and 58.06% of consolidated Profits.

Infra Business

- Your Company has allocated about 41% of its total allocation to Power sector diversified into generation and transmission & distribution. Out of the above, around 18% of your Company’s total power sector investment is in renewable energy sector.

- The port sector now comprises about 5% of the portfolio.

- Your Company has allocated around 14% of its total allocation to SEZ sector.

- Your Company has allocated about 14% of its total allocation to Road sector.

- Your Company has allocated around 3% of its total allocation to Water and Sanitation sector.

Equipment Financing

- The construction, mining, and allied equipment (CME) industry is estimated to have grown by upwards of 20 per cent year-on-year in Fiscal 2018 in terms of unit sales.

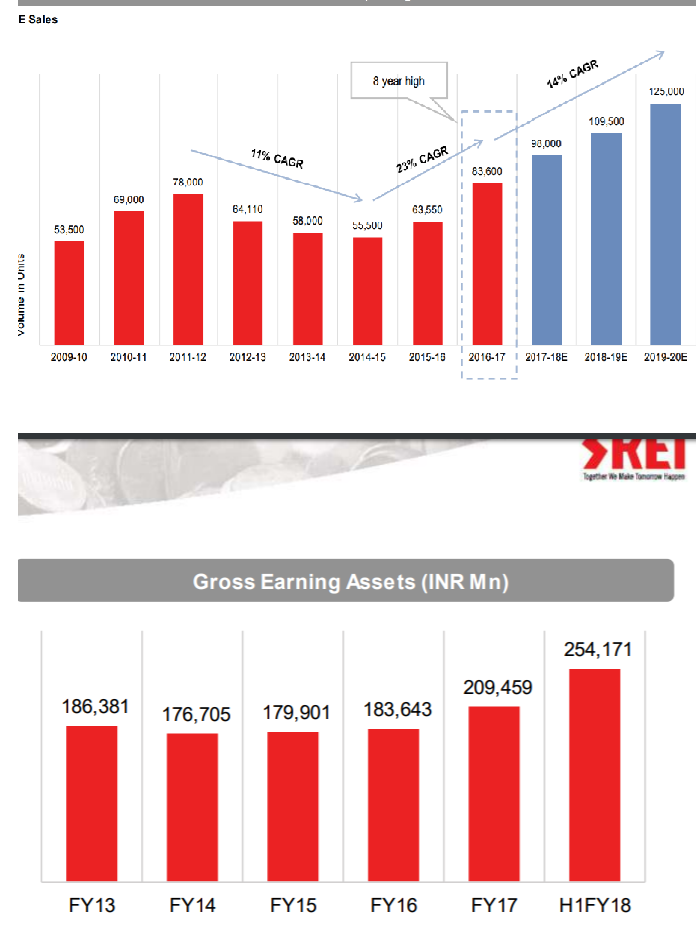

- In a report by Feedback Consulting, SEFL was a leading financier in the CME sector in India, with an approximately 32.7 per cent market share in Fiscal 2017. The report also highlights that the construction equipment finance industry is expected to grow at a CAGR of 19 per cent to Rs. 470 billion for the next three years (2016-17 to 2019-20).

- The total Asset under Management (AUM) grew to Rs. 30,073 crores, representing a 41.64 per cent growth over last year. The Gross Non-Performing Assets (GNPA) reduced from 2.48 per cent in 2016-17 to 1.84 per cent in 2017-18, while the Net Non-Performing Assets have reduced from 1.76 per cent in 2016-17 to 1.30 per cent in 2017-18. The Capital Adequacy Ratio (CAR) remained compliant at 15.94 per cent. The profit before tax grew to Rs. 394.41 crores in the year under review from Rs. 216.42 crores in 2016-17.

2 Likes