Meetesh: In Srei, there is a turnaround on weekly charts…as long as the stock closes the week above 73.30, the uptrend is still on…or rather we still have hope for resumption of uptrend. And on daily charts the support is @ 72…It may so happen that the stock may fall during the week and bounce from support and still close the week above 73.30…But as we all know, it all depends on the Q2 results and US election results…

if both the results and election results are favourable…then the uptrend conditunes for quite some time…

if both are unfavourable, then the stock moves below 72 and enters short term correction / consolidation…

The consolidated eps on QOQ basis has risen from 1.03 to 1.23

The bad debts have gone down from 358 crores to 98 crores

Huge pickup in equipment finance business…as was being repetedly told by mngt

The YOY fugures are just stupendous…

In the press release, the mngt is just stressing on YOY improvement …and they are justified as equpment finance business merger has been done in a equity nondiluting manner.

Without going too much into the details…it would be sufficient to say that the much anticipated business turnaround is underway…

The direction of business is now quite good

So if the stock falls in the next week volitility, it is a good buy…

I request my fellow investors to go through the press release of the company (available @ BSE website)… it has lots of details and will make existing investors to smile…

Mngt is scaling down infra finance lending…now focussing only on safe projects…

But this is more than offset by the increase in equipment finance lending business…

I think i will participate in the core sector growth as reflected in increasing demand for material handling equipment through investment in SREI…rather than holding shares of Sanghvi, elecon, eimco, ace etc…

In the earlier concall…the management explained that in the Equipment finance business, the bad debt problem is less…because they can just go and repossess the equipment.

Now that the management is fully geared up to meet the rising demand for equipment finance businees and focussing on that vertical…there will be two fold benefit in this

Further fall in the bad debt thing that will increase the eps AND

Rising topline and bottom line due to 35% growth in this vertical…which is set to double in next 3 years and of which Srei is the biggest player with 30% market share.

Srei can have a year end EPS of around 5.5 -6 rupees with an upward bias…that makes it a good buy at present level…

In this whole analysis, i am not even going into that wonderful thing in Investment theory …referred to as the SOTP…which can be used to justify higher and higher p/e multiple for the stock.

Disclosure: as usual my views have huge bullish bias…i hold a good quantity of stock in my portfolio

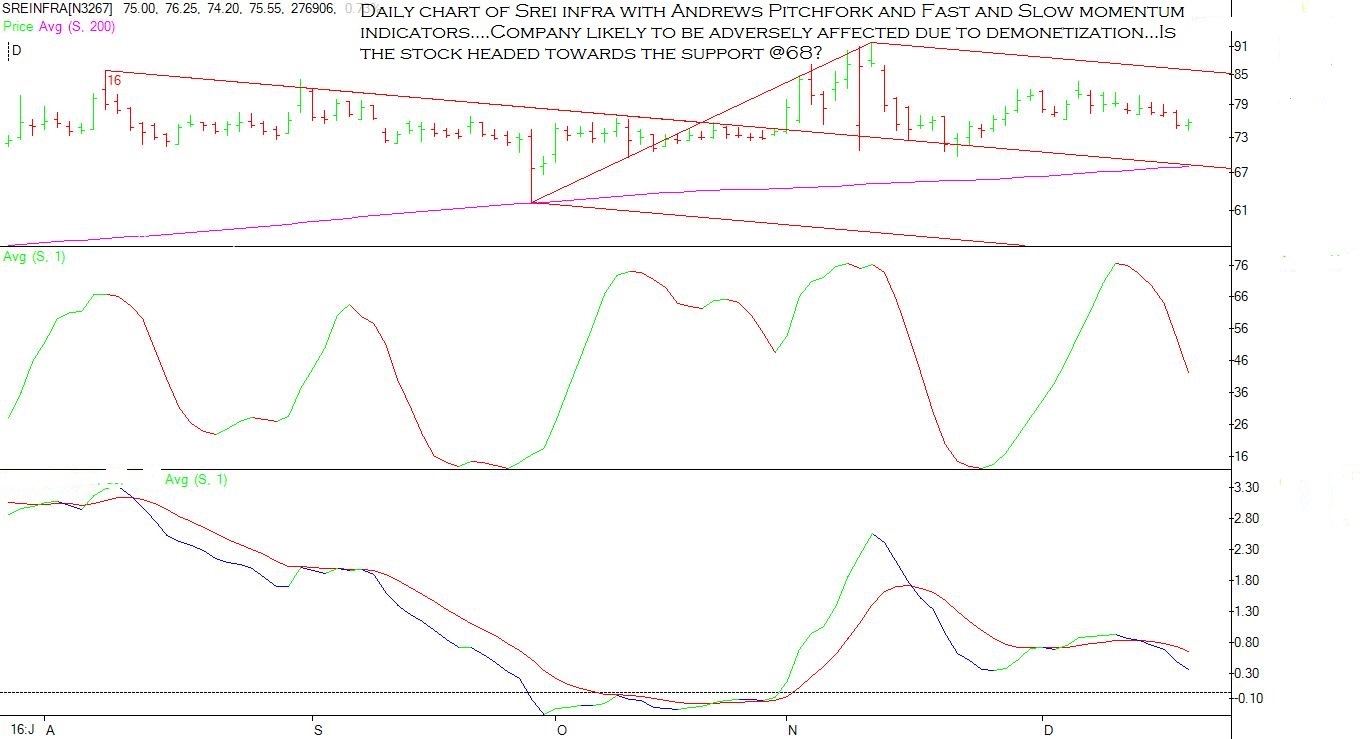

I am much more bullish about Srei Infra…I think, if there is no collapse of the NIFTY in the next 2-3 months…then we may see long green bars on Srei Monthly charts…the stock may even rise to around 140 levels by budget time…if the nifty does not collapse…

The basis for my expectation about srei going towards much higher levels of 140 is on the basis of the monthly chart and the andrews pitch fork technique…which i have posted 5 days ago.

The rules of Andrew pitch fork are that the stock spends most of the time around a fork line…and when it leaves that fork line, then it reaches the next forkline in a relatively short time…i.e within a few price bars…

For 35 to 85, Srei has just moved along the lower fork line…once it leaves this forkline, it can move very rapidly towards the middle forkline within a few price bars…hence my expectation that once SREI leaves the lower forkline, it may reach middle fork line @140 with long green price bars on monthly chart.

And most importantly, i have been writing time and again that it is only the fundamentals which drive the price…with out fundamentals, technicsl analysis is just a few lines on a chart…quite meaningless.

In my opinion, technical analysis is useful only at the very bottom or the very top…when fundamentals dont seem to work.

I also use technicals on long term charts to stay invested in fundamentally good stocks…i use them to get a larger picture and know the possibilities or levels a stock may reach after 2-3 years…if the fundamentals keep improving.

I am not a technical analyst and dont even try to predict short term price movements…i am getting a lot of queries with regards to short term price targets…and i categorically state that i am not qualified for that purpose. Trading is just not my game. i like to think of myself as a buy and hold investor.

Also, the long term charts do not have much predictive value…they only indicate possibilities. So pl dont take my long term analysis seriously…even i dont rely on it…it only helps me not to lose patience…and thats how you guys should look at it.

In behavioural finance they have coined a term …Myopic loss aversion. The more we look at the stock prices, then lesser our holding period becomes.This deprives us of long term benefits of staying invested in a fundamentally good stock.

I realize that one way to overcome this myopic loss aversion is to have a longer term picture of the possible price movement of a particular stock.

I think even a day trader can become an investor if he can look at the price possibilities through monthly charts. And if i can post some quarterly charts with andrews pitch fork…most of us will become committed long term investors…willing to hold a stock even for 2-3 years…or even more.

That is my purpose behind posting monthly charts…

I am not pposting a quarterly charts because they show such fantabulous possibilities over the next few years…that other investors may think i have become delusional.

Lets get drunk on the same illusion / delusion. Why don’t you put those charts with a disclosure so that those of us like us who invest in a stock for a minimum of five years can also see the infinite possibilities that the share price can conquer

Conference call today…everything going well. The company will focus more on material handling equipment finance. Srei sahaj and Bharat roads to be monetized in next 2-3 quarters.

And the best news…ROE in now around 8…in the next 2-3 years, the ROE to gradually increase to 18%…and as told earlier, equipment finance business to double in 3 years…and margins from this business set to improve through value added services in which SREI is the leader.

Srei has filed a declaration with the exchanges wherein it has informed that it has taken up 30% equity in Bhart Road Network limited in lieu of the 340 crore loan that it had extended to BRNL.

As per the newsreports, Srei is looking to sell raise between 750 to 1200 crores by 30% stake sale in BNRL either through private equity or through IPO. Also, in the latest conference call, the chairman - Hemant Kanoria has said that most probably the stake sale in BNRL would be completed in the next 2 quarters…or even if there is a delay, it should not be beyond next 3 quarters.

Earlier, Srei had invested around 1600 crores in Viom and then sold it to ATC for 2930 crores…now on an investment of 340 crores in BNRL…if Srei is able to get 750-1200 crores (as per the Hemant kanoria interview)…then it will be even better than the Viom deal…

SREI Infrastructure Finance Ltd has informed BSE that Srei Equipment Finance Limited, a material subsidiary of the Company has on December 21, 2016 filed Prospectus dated December 21, 2016, with BSE Limited and the National Stock Exchange of India Limited towards its Public Issue of 25,00,000 Secured Redeemable Non-Convertible Debentures of Face Value of Rs. 1,000/- each (the “Debentures” or the “NCDs”), for an amount upto Rs. 2,50,00,00,000 (Rupees Two Thousand and Five Hundred Million) (“Base Issue”) with an option to retain over subscription upto Rs. 5,00,00,00,000 (Rupees Five Thousand Million) (“Overall Issue Size”). The issue will open for subscription on January 03, 2017 and close on January 20, 2017

It is observed that this scrip is facing stiff resistance at the lvl of Rs.80.1 a weekly closing of first week of aug 2016. A weekly close above 80.1 will be very very bullish.

Hi Everyone, any views on SREI now…seems to be moving slowly but steadily…from technical perspective, is it more like heat of moment upward trend or the long march ahead theme. Need your help to understand, is it right time to start accumulating or selective buying

@Mehnazfatima Ji, with BRNL IPO out and listing shortly , could you please provide some inputs on what could be pulling SREI down.Is it some technical parameters which are adverse at this stage. I was hoping bullish momentum due to gains from IPO however it is going the other way around.

I’m an investor who’s seen this company for a few years. 2Q18 results were very good, especially for Srei Equipment Finance (SEFL). Disbursement grew 67% and SEFL loanbook rose 27%. Costs under control, and provisions fell, leading to strong PBT increase. Similarly, INfra division also marginally grew its loanbook, and improved NIMs. Even over there costs were kept in check and provisions declined, despite moving to 90 days past due method (DPD). SEFL is being spun off and separately listed. It would raise 2000 crs for roughly 25% dilution. As such the holdco (SREI) would be 75% owner in SEFL and 100% owner of Infra finance d ivision. Leasing has now become possible post-GST. Leasing is more profitable (about 50 BPs higher RoA ceteris paribus) and it also opens up possibility of financing old assets in a sale-and-leaseback route.

Therefore, fast growth, tight credit quality, leadership position in equipment finance, leasing option ( not available to Banks), rising profitability and cheap valuation (less than 1.2 times FY18 book) and unlocking value through separate listing

I did not kept up with the news, why leasing has been possible now? Earlier leasing was not possible.

How will listing of Equipment business separately help investors of SERI? Infact SERI will become holding company and market will apply massive holding company discount. In fact this may be the case now also.

Hi Gaurav,

Banks are statutorily forbidden from leasing.

Leasing is a win-win for both parties. Borrower frees up debt capacity

which can be better used for BG while bidding etc. Borrower also gets full

tax write-off for operating expenses as against only interest set off only.

Principal has to be repaid from post tax earnings, which is obviously

inefficient. For the lender, leasing is better - they get higher

depreciation, they get to write down 80% asset value within first 3 years.

Post that, they can sell the depreciated asset to lessee at a higher price

than written down value, since asset is only 3 years old. Thus the lessor

can book capital gain also.

Also, lease assets can be immediately repossessed, without resorting to

court process etc.

Finally, lease can be used for refinancing existing assets, while loans can

be used only for new assets. So leasing allows faster AUM growth.

All told, RoA rises by 50 BPs. With 6X leverage, they get 3% higher RoE.

Hope this helps,