It seems the general opinion has been that the company has been limited to being a regional brand but by looking at their numbers the things might be changing. In recent years the growth has accelerated to 20-25% pa vs 10-15% pa in past. Infact in first 9 months of FY18, the growth rate has been at about 45%!!

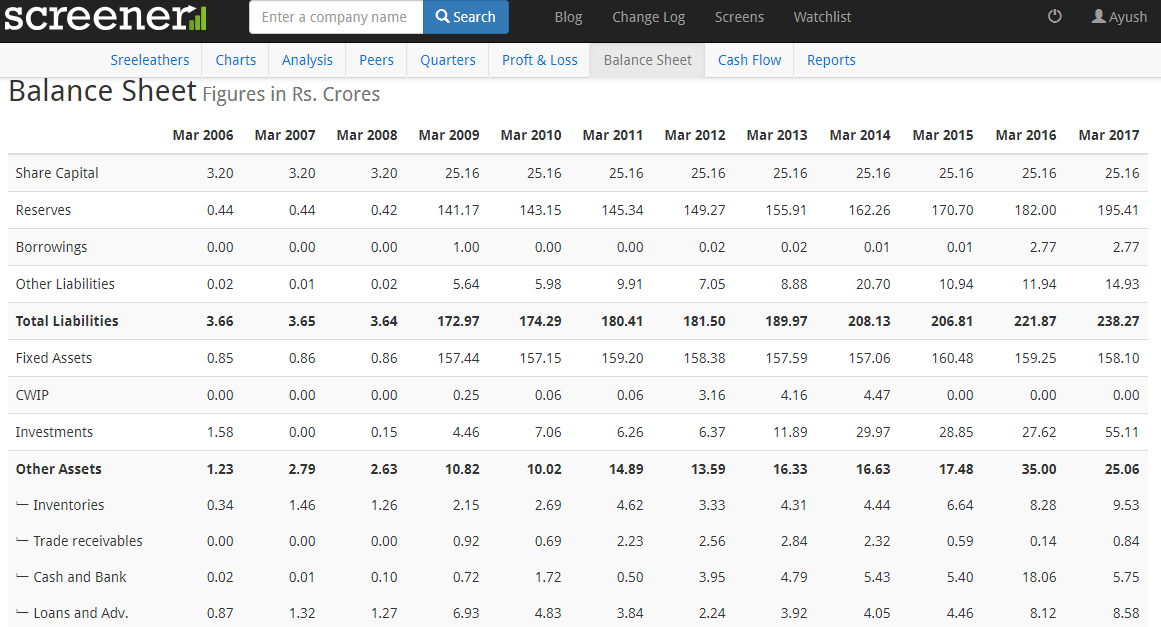

Balance sheet looks really efficient throwing out cash:

The FA are constant, no major addition over last few years (the high value seems to be due to revaluation)

Trade receivables are Nil!

Limited inventory

Surplus funds of about 63 Cr as on 2017. In half year Sept, 17 this has further swelled up.

So by looking at the balance sheet, it seems the company is operating on franchisee model and yet generating very good margins. If the growth can continue based on the current model, then it would be very interesting.

Negatives/Risks:

As per the information memorandum and discussion with friends - it seems the company has some stores in their private unlisted companies, partnership firms etc. Hence conflict of interest and corporate governance issues

Can the company be successful PAN India? How will people know about them outside their regional area?

It has huge demand in kolkata …Every year we see long queue outside the lone store in kolkata especially in puja times in and around Sep- Oct…But failed to understand why it has not scalled up in suburbans in and around where the demand is huge …

Sree leathers is a good name and among first choice of customers in West Bengal, Orrisa and Bihar. That’s what I heard from my various friends from these states.

They have a big showroom in Chennai and I bought shoes from there when I was in Chennai , quality was really great.

It was pure curiosity - I frequently travel in Delhi metro and it’s almost hard to miss

shopping bags carried by their customers. So I was curious why so many people were carrying shopping bags of some obscure company.

Since the store was located in Central Delhi (Connaught Place to be precise - it’s the hottest spot to hang out in Delhi), I got the chance to try out their offering and this is what I noticed -

Their pricing is really competitive vis a vis your local shoe store which sells unbranded products.

Since their store size is really large and therefore you can find all kinds of shoes. So a serious buyer will most certainly get a pair (if brand or leather grade is not the first preference). This might explain their high conversion rate.

Durability is decent.

Perhaps they might be having different startegy for core markets but this might be working for them in Delhi.

Everyone loves a good deal and in India, everyone loves to brag having gotten a sweet deal. So I think grabbing eyeballs shouldn’t be a problem for them since their pricing is perfect for a poor country like India where people want maximum bang for their money at the lowest price possible and Sree Leathers certainly provide that.

Coming to the performance of the company - I believe that GST will be positive for the company (need to know management commentary on this). Mostly, it’s products are directly in competition with SME and MSMEs (having 80% market share pre gst).

Company is currently having 30 stores(as per the website) but the bifurcation between own stores and franchise stores is not available. Apart for retailers, website suggest that they are also wholesaler. Contribution of retail business and wholesale business should be helpful in determining per store contribution.

In 2011 interview management suggested that they had 35 stores operational and they plan to ramp that up to 100 stores by 2013-14 - They closed down some of their stores? What happened to their 100 stores plan?

They sell shoes made of lowest grade of leather. Genuine Leather is synonymous with real leather in India but actually it the lowest grade of leather. That might explain their low priced offerings but what boggles me is that they are able to maintain EBITA of 22%. Especially since they don’t manufacture these shoes themselves. Manufacturer, sreeleathers and franchise all three are making money with Sreeleathers pocketing a good 22% mark up. Some discussion with Franchise owner and SME manufacturers should be helpful in ascertaining whether margins are indeed so high.

Like @ayushmit said, management is using same brand name in their private entities too. Time and again we have seen that in such cases management Quality is very important otherwise you might be holding company having brand name of Milton or BPL, but the benefits of having such brand name is unlikely to flow to minority investors.

@ayushmit . I have been this tracking and invested in this company for a while now. I will add a few things apart from what you have written in the thread

I have sent them 11 emails in the last 3 months and cc’d it to the registrar also but they didn’t reply.

I called the number mentioned on their website 3 times but no one picked up the call.

If you look at the top 10 shareholders mentioned in the AR, 8 of the companies holding Sreeleathers have same directors in permutation and combination.

Shares of all those 8 companies are held in physical form. On top of that, company launched a buy back offer. If you look carefully, it looks like that the buyback offer is done to provide them exit. As of now, none of the shares are bought back. I am not sure if it is a negative even if they are provided the exit.

On the unlisted store side, I read somewhere that some of the stores are owned by their late brother Ashish Dey.

If someone can attend AGM, I think only then our doubts will get cleared.

The sales growth pattern is peculiar. The phenomenal sales growth started after demonetisation and just before the implementation of GST which i found to be dubious.

I took an initiating position at 270 odd levels and it forms currently 3% of my PF. I see an immense opportunity but corporate governance is an issue. Things should get unfolded in time as and when we get a chance to meet the company guys.

In Chennai, there is a mid sized store at Tnagar where they draw good crowd. In regional newspapers, I see they are opening a new store at Purasalwakkam location.

I do not see any information about expansion details in their site, but they are scaling up.

Pros: I see zero debt and huge funds in investments

Negatives: high valuations and no dividends.

Disc: Invested. Planning to add more if there is any correction.

Sharing the personal experience/feedback of certain Investors:

(1) Sree leather has good brand name in West Bengal and Eastern India as value/quality for money product. Back in 2002, I was looking for a genuine leather wallet in Kolkata and some gentlemen guided me to Shreeleathers. Was a good product and value for money, used it for over 3-4 years. Usually if you go elsewhere at this price level, you would get artificial leather products.

(2) I worked on a assignment on market expansion the company. They have a strong presence in west bengal and bihar region. Expanding to north and south.Good people to work with and very focused

(3) Nice focussed business model, did scuttlebutt as well in Connaught place store, product range focussed on mid to low but store was packed wid customers

(4) later around 2006 I saw them opening branded store in Guwahati but the store was not as packed as it was in Kolkata as the brand awareness was not there in Guwahati.Even the store quality was not up to the mark or as refined as the Kolkata store.(Another feedback)

(5) Know the promoters family well. Have not seen the numbers. What I know is they are very orthodox in approach, don’t want to leverage - so am guessing will be low in debt, want to own all retailer stores. CP is also an owned property. Don’t believe in the franchise model but have given some stores on franchisee model in Bihar. I remember my friend who is from 2nd generation says my uncle (promoter) don’t want to work for a bank so he doesn’t believe in loans etc.

Debt free Company and operating margins better than BATA/RELAXO/LIBERTY etc Looks like on account of lower employee cost and lower marketing cost. In fact, variation in material cost is too much (Based on the figures of screener.com)

These are nice set of observations that you have mentioned above.

+ves

Consistent and stable growth in OPM - >19% for last 7years

Sales growth 5Years: 17.60%

Current Ratio >1 and debt to equity is 0.01 - shows the company is almost debt free

Concerns or need clarity - Despite good growth in last 5years

ROE has remained low around 5% and last 10yrs also the ROE is 3%.

another point is that the Price to Book value is almost 3times indicates it is over valued. Unless they can grow north of 40% in next few years the stock looks a tad expensive.

Currently they have about 31 stores across india and only 1 store in South. (Honestly I am from Bangalore I had not heard of this at all)…Need to understand their growth plan

I would be very happy if you could help provide clarity on the concerns. This will be a learning opportunity for me. Thank you

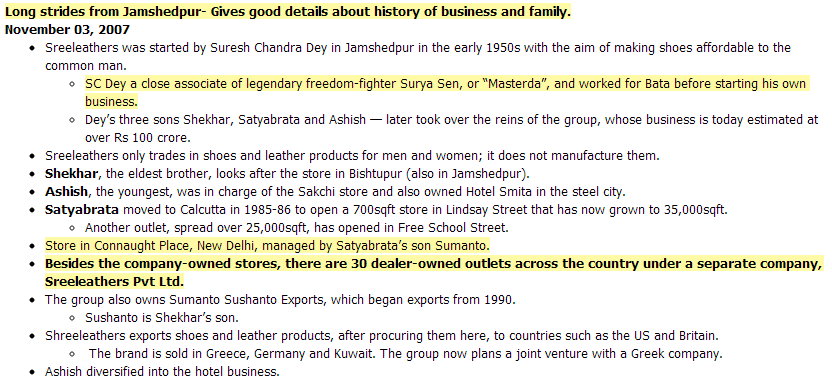

Below are my notes from a news article published in Telegraph on Nov 03, 2007, outlining some key details about the company and the family who runs the business.

Despite knowing that private entity has more stores than the listed entity, why did you decide to invest in sreeleathers? Do you also see an immense potential if management comes on track?

Also, did you ever get a chance to go the AGM of sreeleathers?

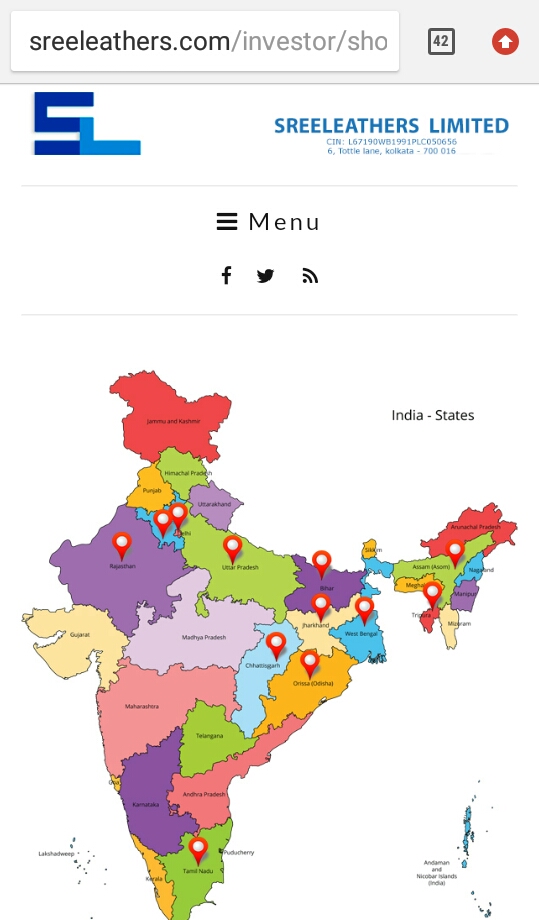

To understand the potential conflict between listed & un-listed companies, we tried doing some work on the unlisted companies. It seems there are 4-5 names, however, only 1 had material revenue and balance sheet:

Did you find numbers for Sreeleathers private limited? The private subsidiary someone in the earlier comment talking about?

I tired googling it but did not find any numbers for that.

Thanks for the reply. In 2007, in the article that you mentioned, it showed 30 stores under unlisted entity and the number of stores in listed entity are also similar hence the first comment.

Thank you for the pointer for checking the revs from MCA website. Didn’t know that the info can be availed by public.

The article I posted above mentioning the unlisted company is from 2007. Sreeleathers Private Ltd got amalgamated with the listed entity in 2010 (Source: Annual report).

@ayushmit

Sir, Many thanks for initiating this discussion on Sreeleathers.

It seems that the company owns 12 stores and the rest are franchisees.

The basis of my hypothesis is the showroom map on their website.