Water is the next big mega trend~

India will be going through a major water crisis in the coming years owing to~

- Rising urban population and a below-par water supply situation in cities with intermittent supplies. inadequate coverage & low pressure

- Increasing water demands due to population pressure and urban sprawl.

- Industrial Growth

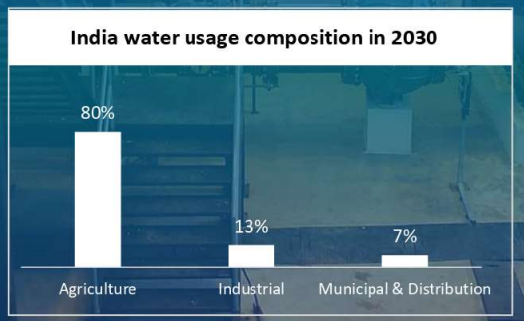

- Industrial Waste ‘Water Increasing irrigational and agricultural demands

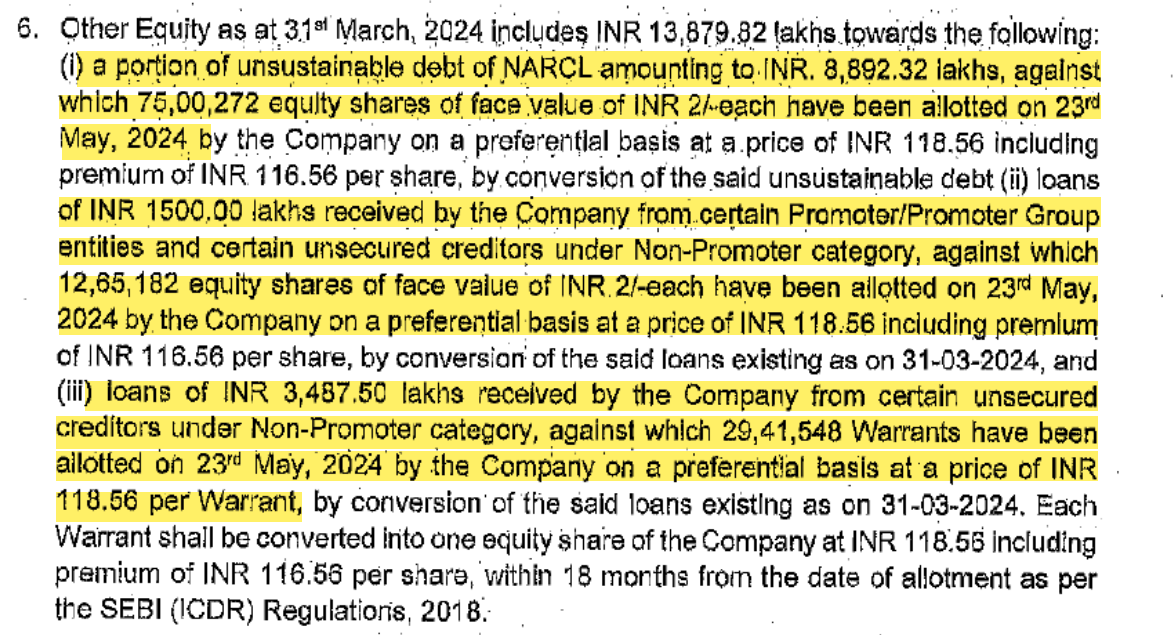

- ‘Water cycle imbalances and stress

- Over exploitation of water resources

- Water quality for various applications and availability

- Political & regulatory disputes (Prime eg. being Kauvery river dispute between Karnataka & Tamil Nadu)

Important stats~

“Only 64% of India’s urban population is covered by individual water connections and stand-posts, compared with 91% in China, 86% in South Africa and 80% in Brazil. “

“ Roughly 70% of untreated waste water goes into river”

“60-70% of towns have no underground sewerage facility”

As a result, govt. has been very proactive & taking major capex & policy initiatives like ~

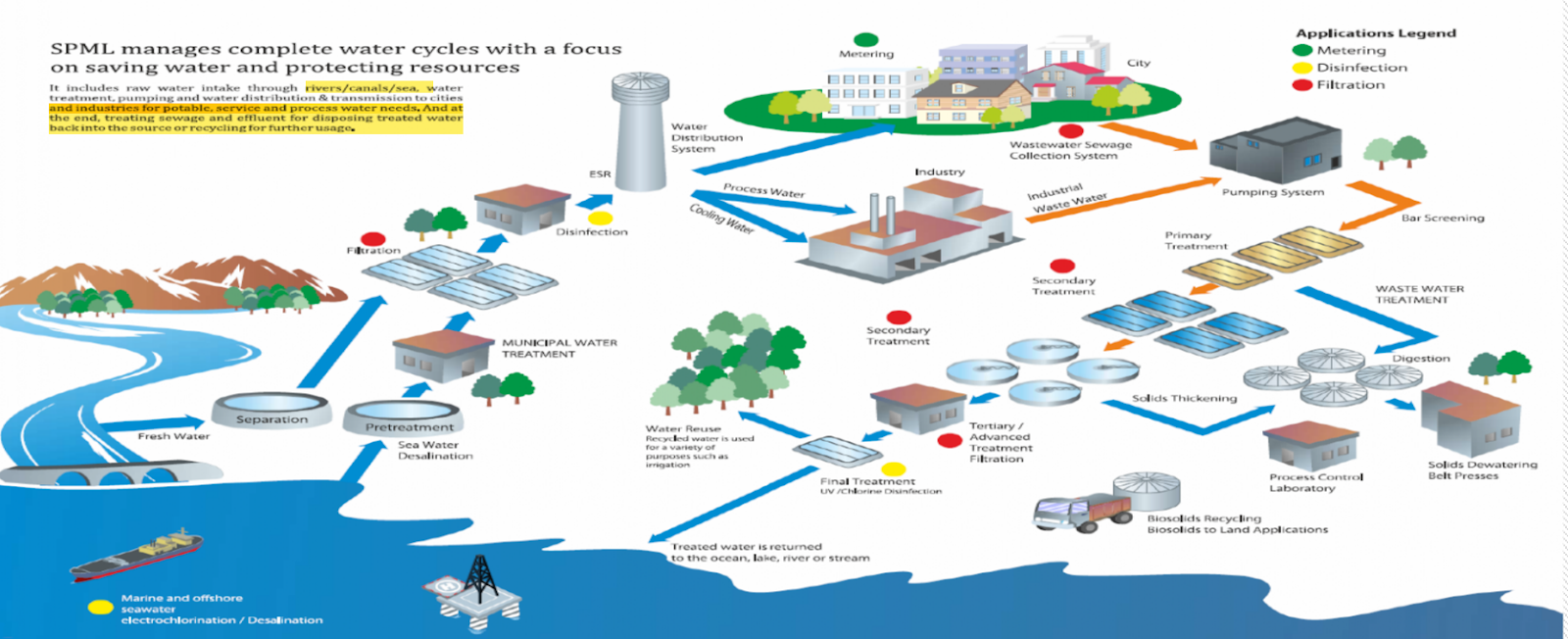

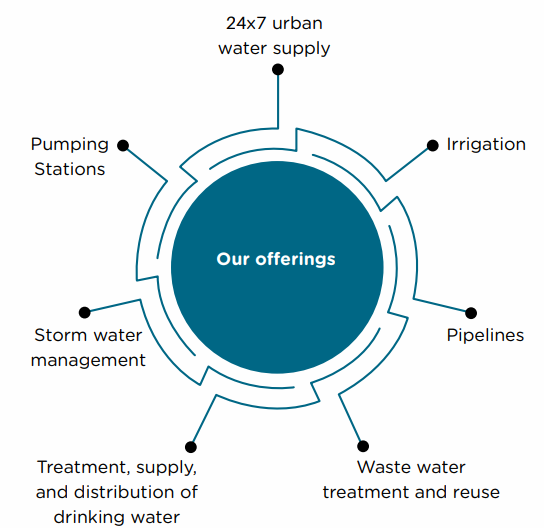

One such company that is strongly positioned in the entire value chain is “SPML INFRA”~

It includes raw water intake through rivers/canals/sea, water treatment, pumping and water distribution & transmission to cities and industries for potable, service and process water needs. And at the end, treating sewage & effluent for disposing back into the source or recycling for further usage.

About the company~

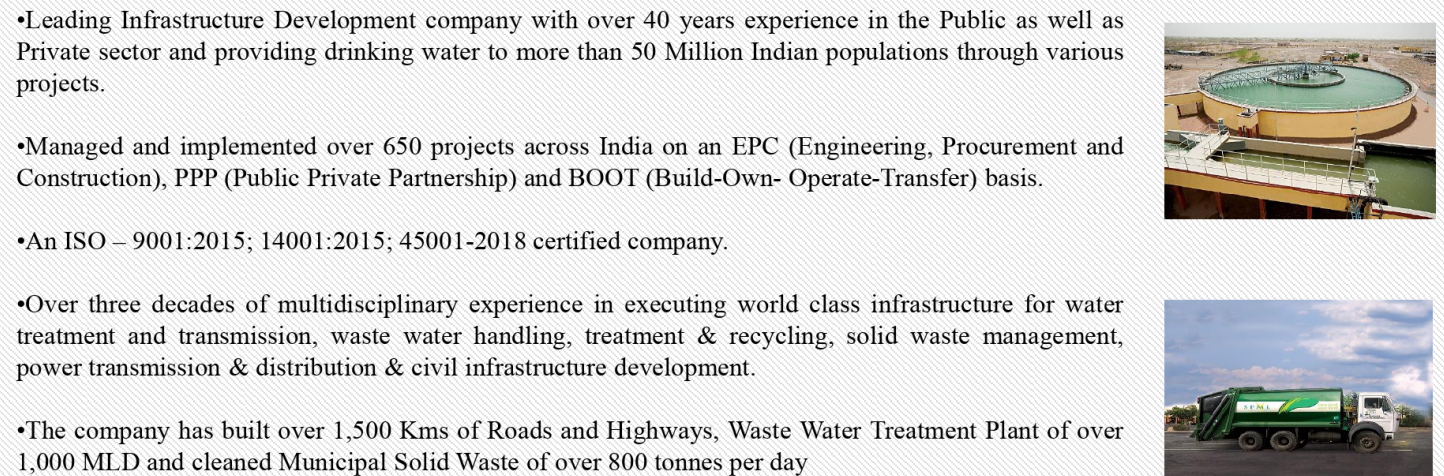

SPML Infra Ltd. is India’s leading publicly listed Infrastructure Development Company with over four decades of experience in the public and private sectors. The Company has executed and commissioned over 650 large and medium infrastructure projects across India and created significant value for the country, thus touching the lives of millions of people with the provision of drinking water facilities, wastewater treatment, integrated sewerage network, better municipal waste management, power transmission & distribution and lighting up homes. The Company features among the World’s Top 50 Private Water Companies and among India’s 50 Best Real Estate & Infrastructure Companies. The Company operates in the engineering, procurement, construction (EPC) segment

The company started as an EPC player focused on water, power & sanitation projects.

However, in recent times, the Company has mainly engaged in the water sector where there is enormous opportunity by way of Govt. spending and allocation of fund for the water infrastructure project.

Key tailwinds~

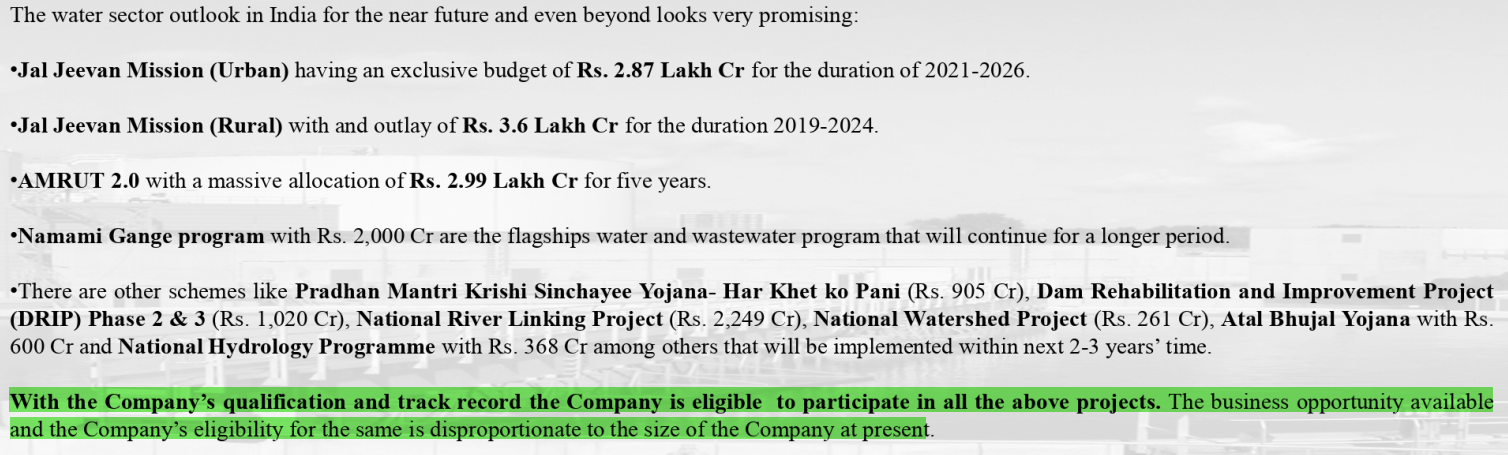

The govt. has allocated approximately 7.30 Lakh Crore to be spent in the next few years which will give a good business prospect to the Company in the water sector by obtaining various contracts from the central/state Govt.

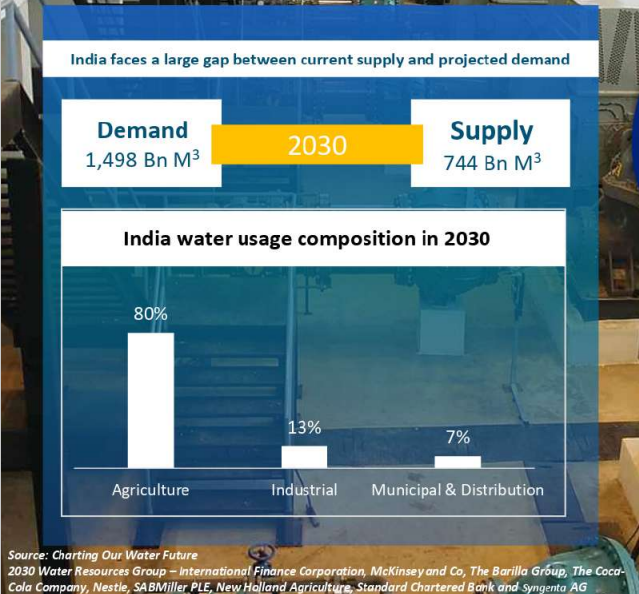

India needs to spend heavily in developing its water infrastructure to avoid a catastrophic condition ~

Debt resolution~ the key Trigger

While the industry tailwinds are very strong for the infrastructure-focused EPC businesses, the best way to find valuation comfort is by betting on companies that are going through internal restructuring like~

1. Demergers (Bajel Projects getting demerged from Bajaj Electricals)

2. Management change (WS Industries getting taken over by new promoters)

3. Balance sheet restructuring (which is the case for SPML Infra)

Before we delve into the restructuring, it is important to understand what went wrong~

- Non-availability of BG limits and increase of bank charges and interest

- Delay in the realization of Arbitration Amounts

- Delay in Debtor Realization (Majorly from the govt. projects)

- Delay in Project completion coupled with COVID Impact

This led to borrowings ballooning to an unsustainable level~

It is important to note that this was the case with majority of the companies in the industry due to consistent delays in repayment by govt. (both central & state) coupled with poor pricing of tenders (mid-single digit EBITDA margins) making the entire business & industry economically unviable.

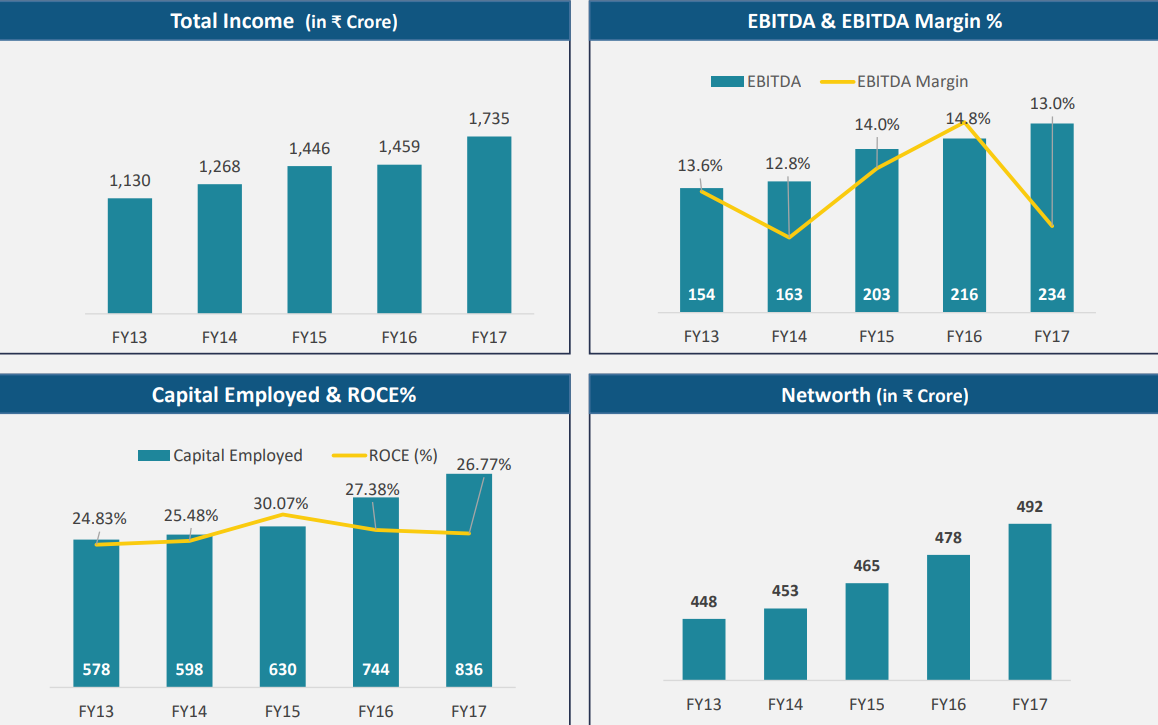

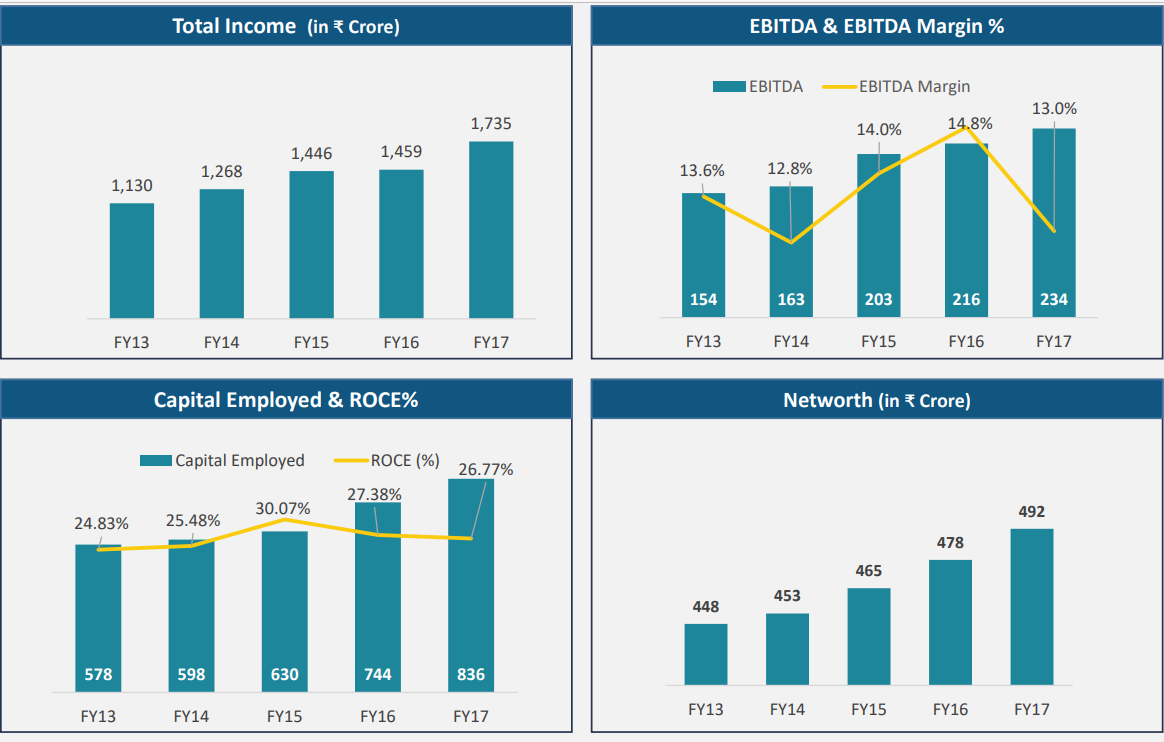

During good times, the company used to clock an ROCE of 25% with an EBITDA of 14%~

However, given the requirements for larger companies to develop the critical infrastructure, banks have started assisting these companies in restructuring their balance sheet through a separate body- NARCL i.e National Asset Reconstruction Company Ltd.

Restructuring~

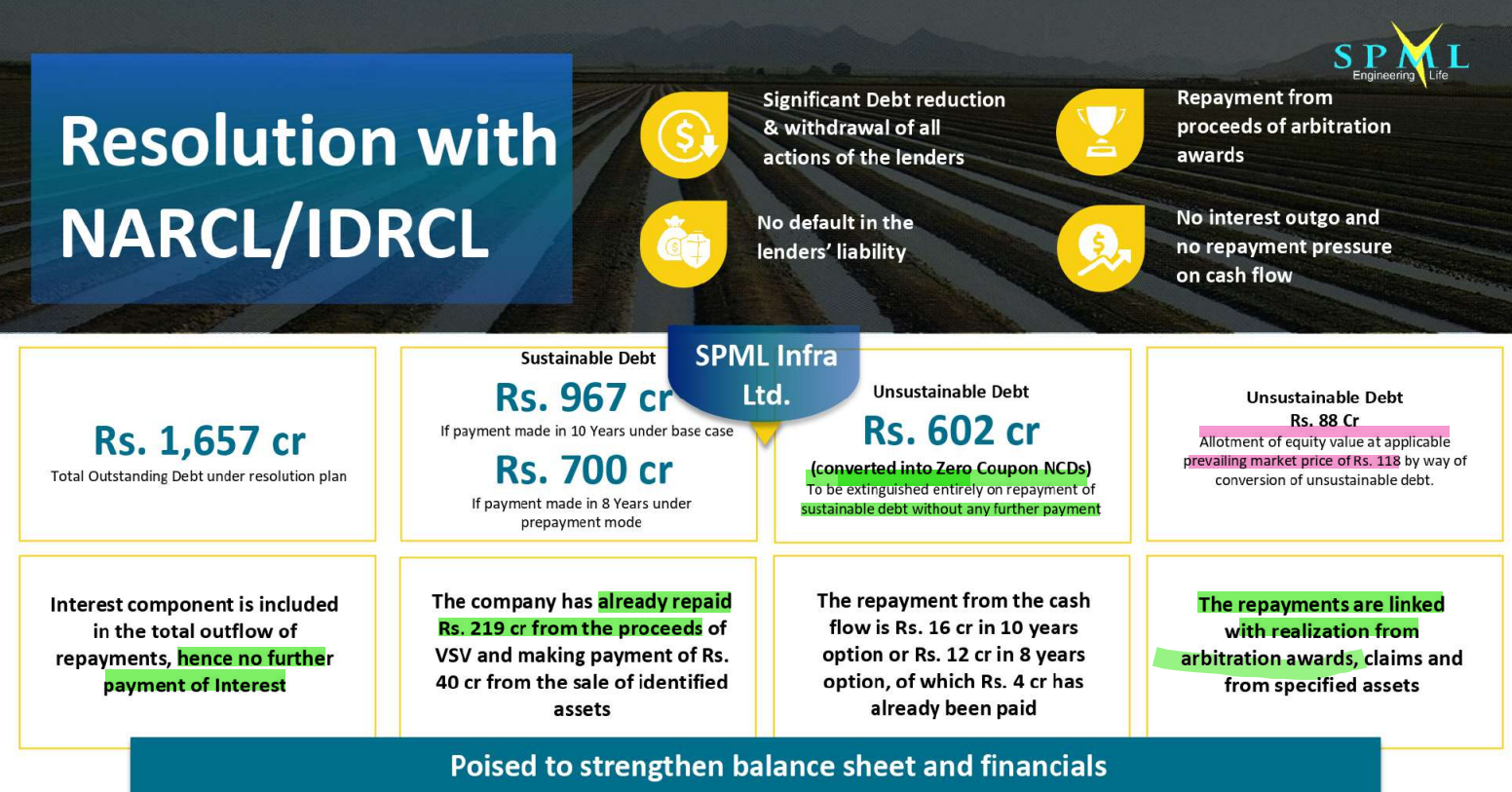

As per the master restructuring agreement, company saw the following developments~

- The company’s total principal debt of Rs.1657 Crs + Interest accrued of Rs.947.5 Crs (i.e. Rs. 2600 Crs debt) was restructured in such a way where~

The debt was bifurcated as:-

- Unsustainable debt of Rs.1637 Crs- Further bifurcated into the principal of Rs.690 Crs & unpaid interest of 947 Crs

- Sustainable debt of Rs.967 Crs-

1. For the unsustainable debt~

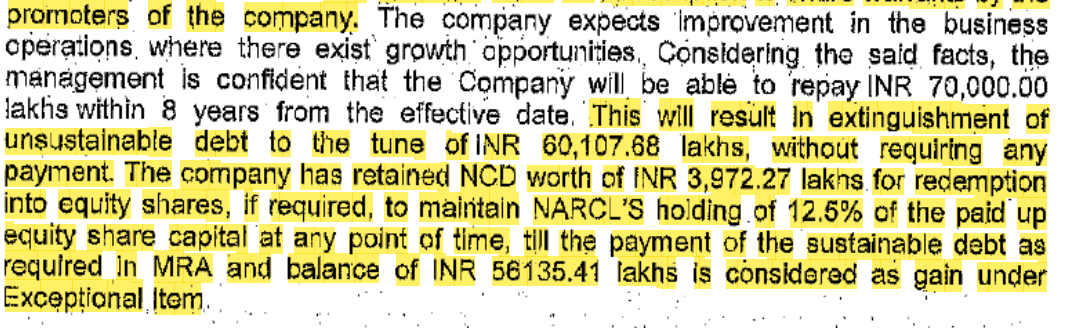

Unpaid interest of 947 Crs will be written off after allotting 75Lakh equity shares (12.5% of total shareholding) at Rs.118 per share to NARCL & converting the remaining unsustainable debt of 601 Crs by issuing Non convertible debentures (NCD).

It is important to note that the shareholding of NARCL should not fall below 12.5% (i.e. company will need to issue more equity to NARCL incase of any dilution in future)

Further,the unsustainable debt portion of 601 Crs won’t be required to be paid through NCD’s if the company is successful in paying off the sustainable debt portion in the given timeline.

2. Sustainable Debt of 967 Crs~

As per the terms of MRA, the Company has to pay INR 967 Crore in 10 years to NARCL. However, there is an early payment option of INR 700 Crores in 8 years. Out of the aforesaid payment Company had already repaid INR 223 Crore.

It is important to note that the company’s cashflows won’t be strained one bit as a result of this settlement owing to an interesting settlement mechanism wherein~

The company has applied for several disputed claims in the court worth around 5000 Crs in different schemes (One being the Vivad Se Vishwas Scheme), & all the cash received from the claim settlement will flow away in meeting the debt settlement~

Based on the recent conference call, management explained that it has already paid around 220 Crs through the sale of properties & funds received from vivad-se-vishwas scheme & it expects a further receipt of 40 crs from arbitration receivable & a huge award (in return of the claim filed) in Arunachal Pradesh which will ensure that it will easily pay off the 700 Crs liability in 7 years.

(Note~ the company has a cash balance of 75 Crs as of today)

There have also been several positive developments on the arbitration settlement side with the timeline for redressal reducing substantially post amendments in 2019 which levied the law that an award shall be given by an arbitral tribunal within a period of twelve months from the date of completion of pleadings ~

In addition, the payment of debt, company as per the requirements of MRA~

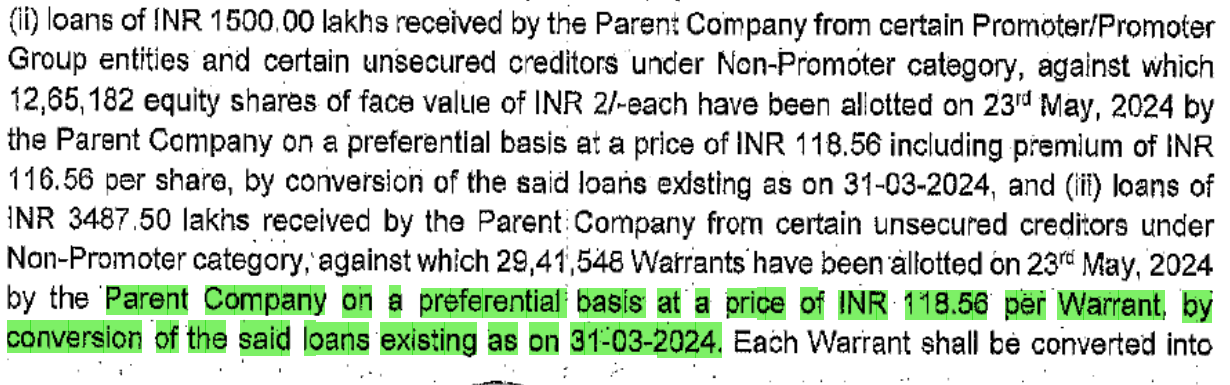

- Issued warrants worth Rs. 50 Crs to promoters in Conversion of promoter’s existing loans of 50 Crs.

- 30 Crs infused by promoters

To conclude in a nut shell~

1. The company has issued around 1.7 Cr shares to NARCL, creditors & promoters for restructuring the debt

2. The company is required to pay off 700 Crs worth of borrowings in the coming 7 years out of which, 220 Crs has already been paid

3. The entire payment of the remaining borrowings is linked with the arbitration claims that the company has filed & it won’t result in any outflow from the company’s core business operations

4. If company is successful in paying of the borrowings, then the NCD’s worth Rs.600 Crs that were issued to NARCL will dissolve with immediate effect.

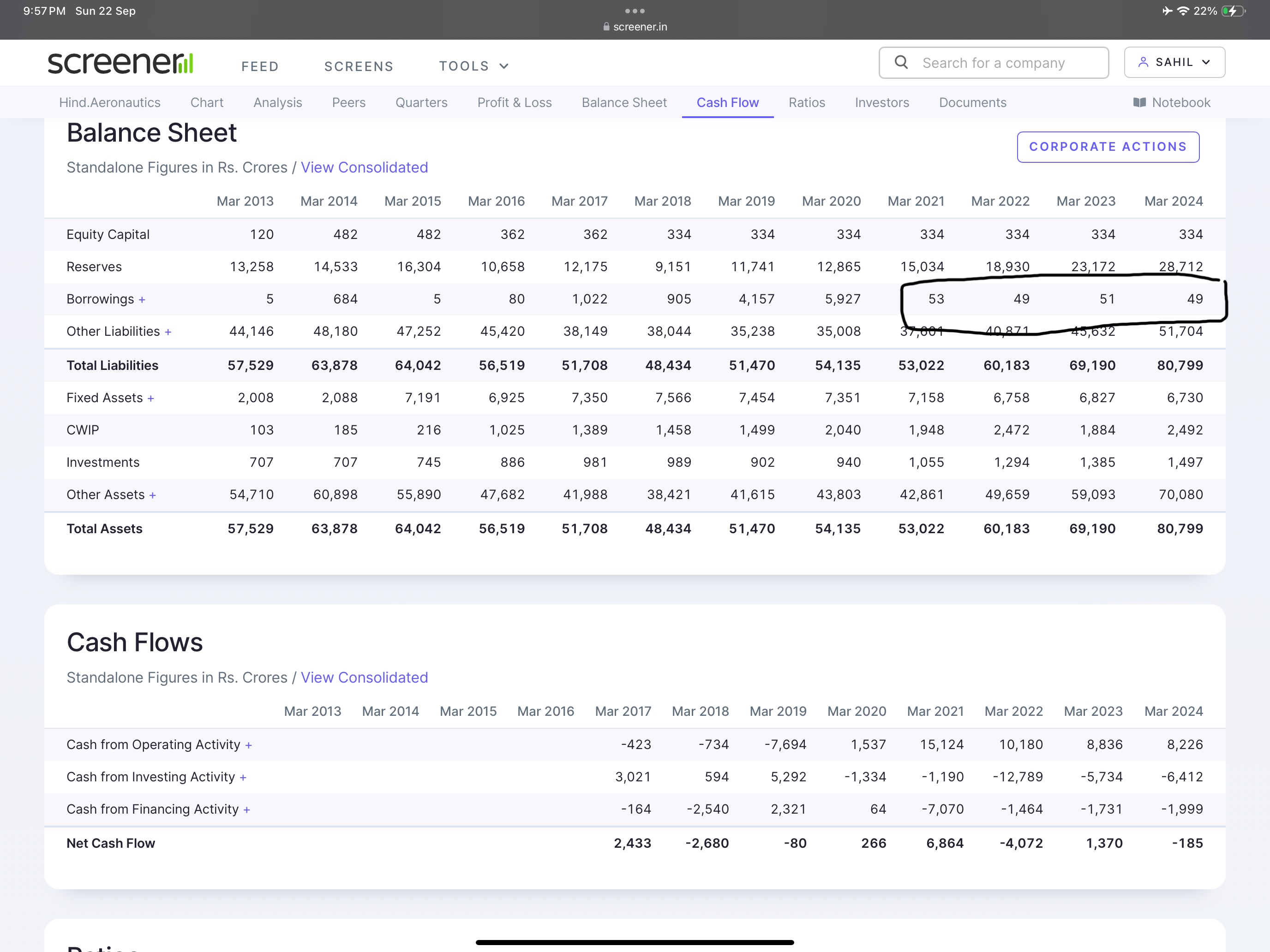

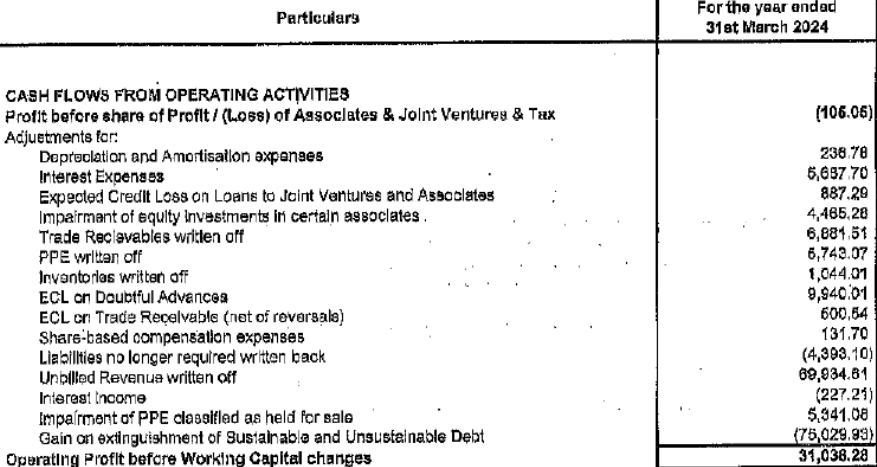

If we look at the Balance sheet as of 31st March 2024, the majority of the clean-up has already happened wherein~

- write-off of contract assets in the form of unbilled revenue amounting to 69,934.62 lakhs

- impairment logs cn PPE assets classified as ‘held for sale’ amounting to INR 5,341.09 lakhs

- write-off of inventory and fixed assets amounting to INR 1,152.36 lakhs

- reversal-of ECL provision of INR 14,007.43 lakhs on certain. Trade Receivables and simultaneous write-off of an equivalent amount of the said Trade Receivables.

Based on my understanding a major portion of the balance sheet-related shocks (be it write off of unsustainable debt, inventory, trade receivables amongst others) have been absorbed & therefore internal restructuring process has been ‘partly’ fructified which is reflected in the stock price rising from 50 Rs. to 150 Rs.

Therefore, going forward, external tailwinds can drive the next leg of share price movement~

Company’s key competitive advantages~

1. Prequalification~ Based on the recently conducted concall, the company is one of the only few players (other than VA tech WABAG & L&T) that can participate in all the govt. tenders~

This is a big edge as based on the commentary of management, they plan on targeting only higher value tenders where competition is very less leading to higher EBITDA margins of 15-20%.

2. The company has a strong past track record of 43 years & rich legacy winning several accolades in the past ~

The company’s customers include key Water & Sewerage boards of states like Gujarat, Rajasthan,Karnataka, Chennai, Uttar pradesh & Odisha among others~

The company has also executed several marquee big-ticket projects~

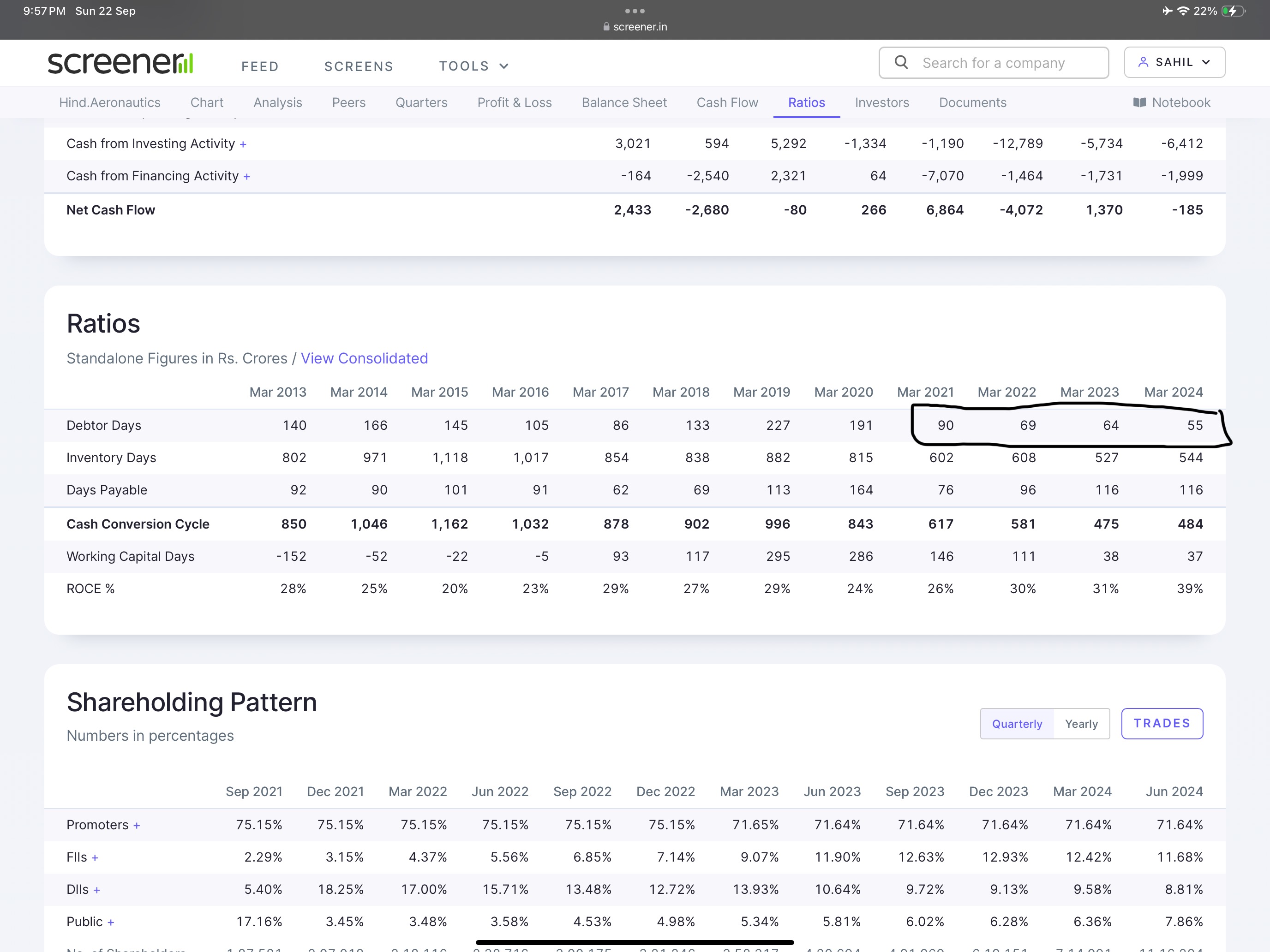

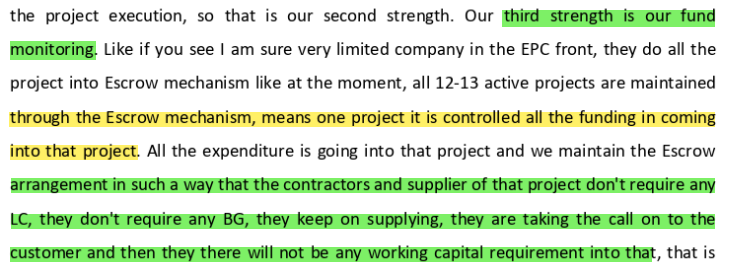

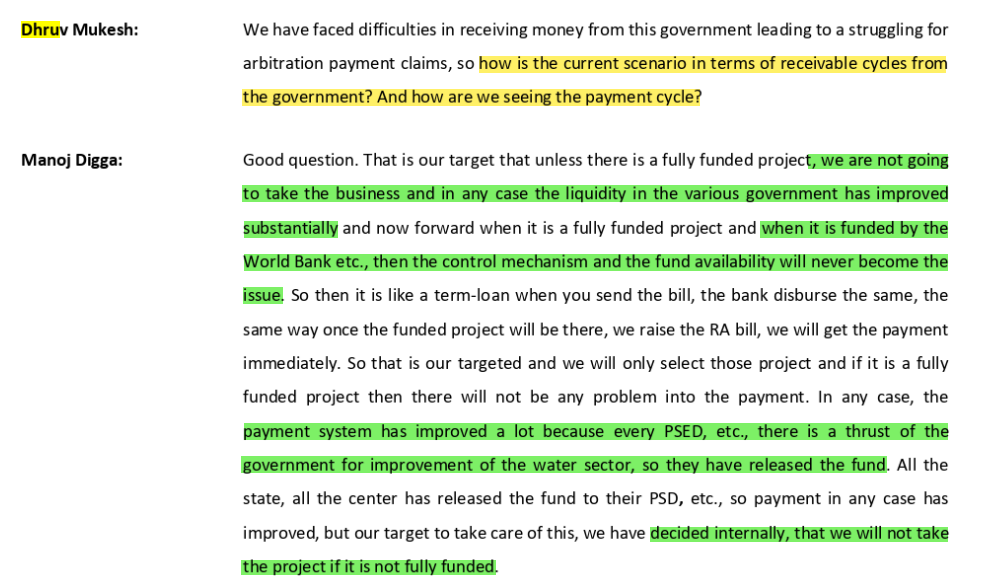

3. Strong focus on working capital cycle & recovery of receivables ~ The company suffered dearly in the past owing to poor recovery of receivables from several government projects.

Therefore, it has become more cautious, focusing on fully funded projects & reducing its working capital cycle requirements through an Escrow account mechanism wherein~ All the funds movements are routed through a single account wherein suppliers directly receive funds from any movie received from the customer directly without any major initial working capital funding requirements for the company.

(source: concall, Investor ppt)

4. Strong tailwinds in the industry~ It is expected that govt. Will spend around 1 Lakh cr per annum for the next decade in building the water infrastructure.

While the current leg of capex on water infrastructure is being led by government & municipalities..Given the stronger implementation of pollution-related measures by the pollution control board, the Industrial segment is expected to be the next key driver of capex (where implementation was very poor till now).

5. Improved payment cycle coupled with higher focus on fully funded projects will ensure higher ROCE (lower working capital cycle)~

Risks~

1. Poor past track record~ From clocking consistent ROCE’s of 25% to opting for a 12.5% equity dilution & debt restructuring just to survive..company has come a long way!

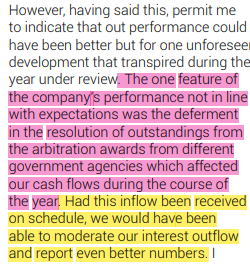

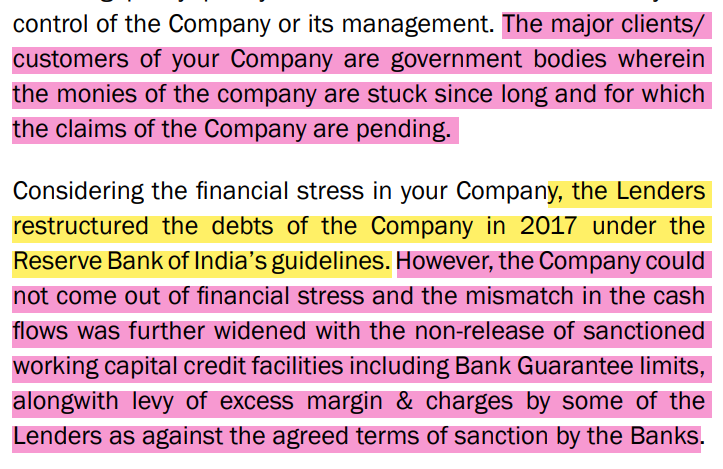

While the company was still struggling from a balance sheet point of view in 2017-18 where the debt kept piling up owing to non-receipt of arbitration awards (inability to realise receivables) as mentioned in the AR 2018,the company was able to secure a restructuring of existing debt during 2017 period~

However, things only became worse in the coming years with revenues reducing (especially post covid) coupled with margins reducing drastically & cashflows suffering as a result of inability to recover money from its customers (govt.)~

Company’s renewed focus on water industry (Vs other segments like Power & salination) & better payment terms from govt. Projects might ensure that past issues doesn’t arise again~

2. Equity dilution~

The company as a result of restructuring its balance sheet has converted a major portion of its borrowings into equity shares & warrants which led to a huge dilution of equity~

There can be a potential equit dilution in future as well wherein,incase company is required to raise funds through issue of shares, then it will be required to issue requisite number of shares to NARCL to maintain their 12.5% ownership levels.

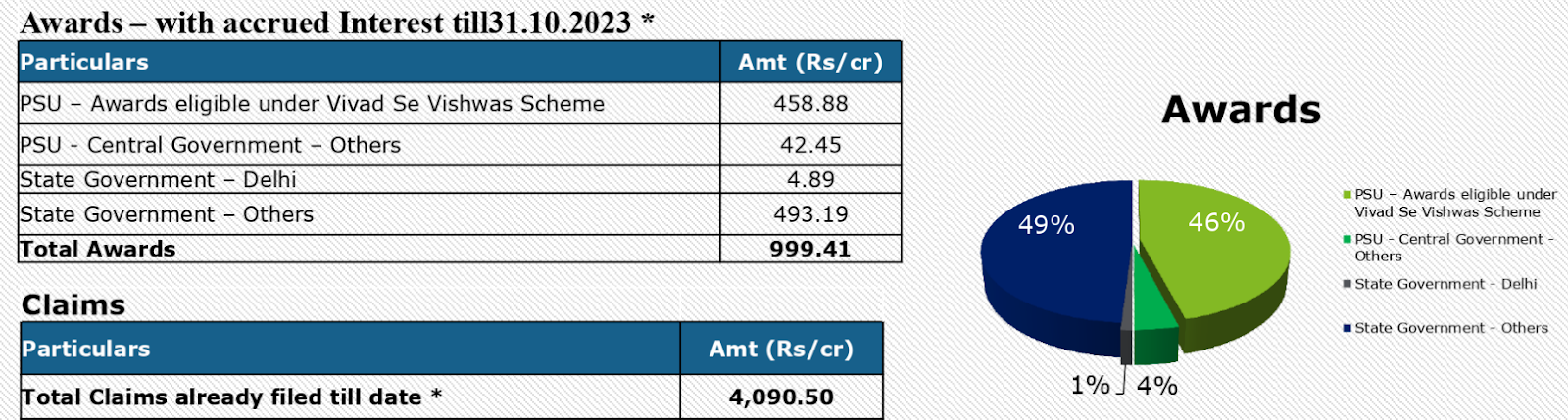

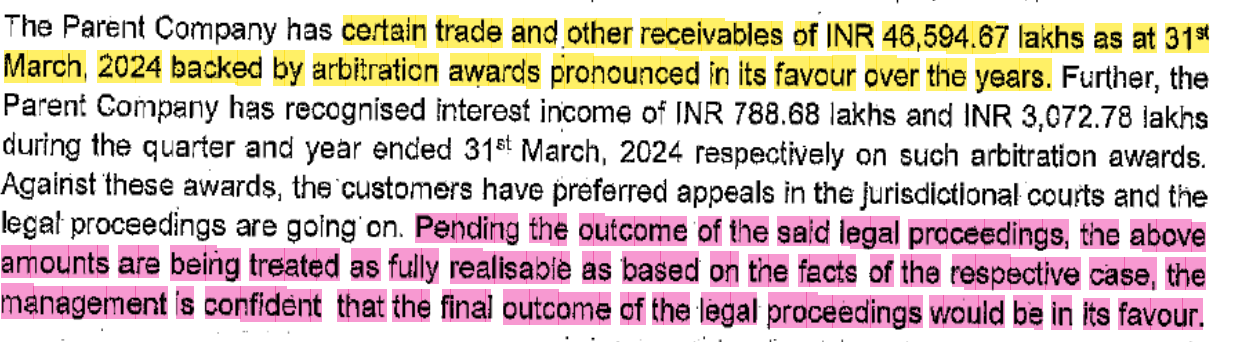

3. More write-offs on the receivables front are possible~ Management has around 465 Crs of Disputed receivables where the company has filed arbitration claims.

However, it remains to be seen if the company will realize the same in cash in the near term given the long dispute settlement process historically.

4. Uncertainty about the order book & revenues going forward~ Dependence on government projects for getting new tenders coupled with realisations of the same is a key risk that the business faces.

Infact in AR20, management when questioned about poor performance mentioned this~ “Basic reasons for the above were delay in payments from clients due to allocation of funds to other vote-bank purposes than using for projects, working capital shortage, and inadequate financial support from lenders.”

The company’s current order book stands at 1300 Crs & it is initially targeting orders of Rs.2000 Crs per year.

However, given the lack of any major bank guarantees & its focus on a niche segment, it remains to be seen if it will be able to garner a decent order book & clock the desired EBITDA margins of 15-20% considering its margins in recent years have been poor owing to the legacy order book’s pricing.

The key metric to focus on here is the order inflows as that will be the key indicator of the “Operational turnaround” after the recent internal restructuring.

5. Bad feedback during scuttlebut - After talking to several people having an understanding of the water infrastructure space, one common sentiment was their negative thoughts about the management with one even saying - “ They are technically competent but morally questionable” & given the strong profitability in the past followed by a sudden downfall out of nowhere, it won’t be an overstatement to say that there might be some weight into the same.

However, since the company has recently undergone restructuring, management has converted their loans into warrants & Industry tailwinds are strong, management might change their way of operations & focus on more shareholder friendly value creation (similar to what Vatech Wabag did & some early indications of its efforts includes doing its maiden concall)

6. Complicated corporate structure~ The company in the past had too many subsidiaries, JVs & associates where a lot of related pary transactions used to happen coupled with constant write-offs of subsdiairies amongst others makes it very difficult to understand the fund flow in the organisation especially given the fact that company gave several loans to the related parties which got dissolved without repaying any.

Another big redflag was that these Joint ventures & subsidiaries where not audited by the statutory auditor (making it difficult to rely on numbers).

A good thing is that majority of the JV’s & associates have been dissolved (which were focused on the power sector), making the structure more streamlined to assess.

Valuations~

- Equity dilution makes it a little complicated to value:-

As per the concall~ Total additional shares to be issued ~ 75 lakh shares given to NARCL, promoters got 25 lakhs (1 Crs total shares given for restructuring), promoter has infused 50 Crs (70 lakhs warrants)

As per the latest diluted equity shares, the company post conversion will have around 6.61 Cr shares outstanding.

![]()

At the current market price of Rs.140, the implied market cap stands at around 925 Crs.

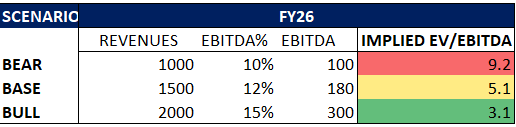

While it is very difficult to model the numbers going forward, assuming an order book of 2000 Crs on annualized basis (current order book stands at 1300 Crs) & 2 yrs execution period, I feel company can clock around 1500 Crs in the coming years.

Here are my rough workings on the numbers going forward~

Please note that actual numbers can vary significantly from my estimates.

As per the recent concall~ SPML HAS TARGETED EBITDA% OF 15-20% & ORDERBOOK OF 2000-4000 Crs

Other player like Wabag & EMS trade at 9-12X EV/EBITDA multiple (2yr forward) therefore valuations do look lucrative however, A) These players have lower risk & better track record warranting higher valuation multiple & B) the execution is the key for any alpha to be generated by SPML.

Note~

- WABAG GUIDANCE~ 15-20% SALES CAGR WITH EBITDA% OF 15%

- EMS HAS GUIDED~ 35% SALES GROWTH IN FY25, HOWEVER, I AM MODELING 2YR CAGR OF 25%

Management

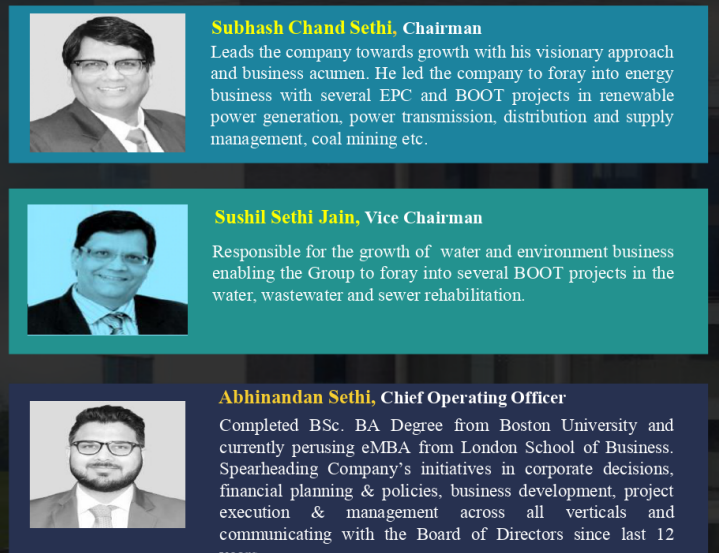

Management not only has a rich legacy, but they are also fighters~

Promoter Subhash Sethi beat Cancer resiliently during Covid period owing to the help of his family & Love for his business.

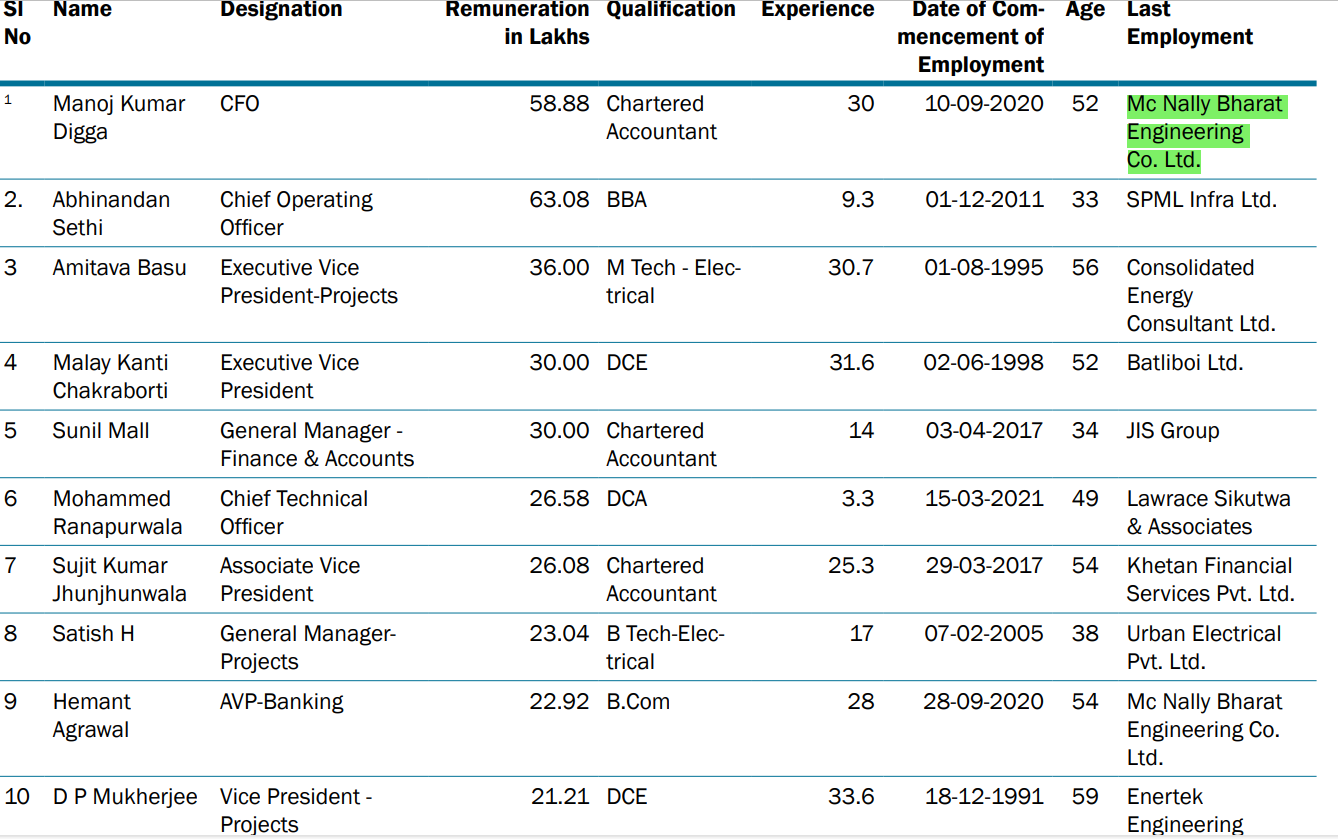

CFO Manoj Digga post joining the organisation in 2019 has led the company’s restructuring exercise & has led strong improvements in the company’s accounting policy by making it more conservative.

He was recently involved as an additional director as well showcasing his increased role in the organisation.

The promoter’s son- Abhinandan Sethi has become more involved in the business based on our scuttlebutt which is a good sign from the succession planning point of view.

The most common way to assess a management’s skin in the game is generally to see their shareholding~

Therefore, while the 1st assessment of any investors will be that since, the promoter has shareholding below 50%, promoter’s skin in the game is absent..However, I believe otherwise~

- Shareholding has been improving steadily in the past 2 years led by the release of pledged shares

- Another interesting event highlighting promoter’s skin in the game involves the promoter’s efforts to convert their loans to the company into shares, thus increasing their skin in the game coupled with indirectly reducing the stress on company’s balance sheet.

- Lastly, promoters are infusing funds & converting their loans into warrants

Note~ Altough track record from technical stand point is superb given the marquee projects that they have executed, however, the track record on the operational front is poor & given the delays in completing contracts due to lack of funds, the company was debarred from certain tenders & promoters don’t enjoy good reputation in the eyes of suppliers based on my scuttlebut as a result of the past issues.

However, given their intention to restructure the balance sheet, infuse funds closer to current market price (Rs.118 per share) & their focus on suddenly communicating with the shareholders regarding the growth prospects in investor presentation & maiden concall, I feel that the company might be nearing an inflection point.

As a result of the poor track record coupled with high debts in the past & uncertain future growth prospects..company is trading at a very lucrative valuations.

It would definitely be safer to wait for the company to get new order wins given the uncertainty surrounding bank guarantees & policy implementation.

However, this uncertainty is what gives us the margin of safety & higher chances of alpha due to the lower valuations.

Closing thoughts~ Company is at an inflection point owing to the restructuring of the balance sheet & tailwinds surrounding the water infrastructure sector, however, given the uncertainty & poor past track record of the company & promoters, it is a highly risky bet at the moment..similar to what Va Tech Wabag was 3 years back!

Disclosure: Invested (Highly risky bet), will intently be tracking the quarterly results & any announcements related to the order book going forward.

Trivia~

Idea generation process: 1st conference call