SPL Industries Limited

Financial Overview

MARKET CAP (RS CR) 91.64

P/E 16.63

BOOK VALUE (RS) 9.70

INDUSTRY P/E 37.99

EPS (TTM) 1.90

PRICE/BOOK 3.26

FACE VALUE (RS) 10.00

Promoter Holding 67.24%

Pledged 0.00%

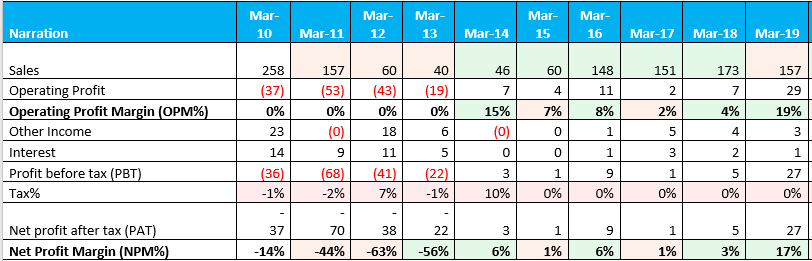

Company posted good figures on yoy basis. Company posted sales in December quarter 29.35Cr from 14.69 Cr corresponding quarter of previous year by 99.79%.Net profit in December quarter 1.51Cr from 0.99Cr corresponding quarter of previous year by 52.52%.

TTM Sales stood at 121.89Cr. TTM Sales is already doubled from last year’s sales 59Cr in Fy15. TTM Profit 5.50Cr from last year’s profit 0.52Cr in Fy15.

Debt to Equity is around 0.19.

Company is expected to give good quarter.

Valuation

Stock is trading with low PE as compare with the Industry PE. Company will post 6 Cr of profit on 2.90 Cr shares and Market cap of 93 Cr. Its available at low value. We all know in coming years brand are in picture. Demand of branded cloths are increasing day by day. Then SPL may be good opportunity.

About Company

Established in 1994

A leading Apparel Export House of India

One of the largest vertically integrated Knitwear plants in India

Reputed for excellent Product Development and Design capability

Incorporated as Shivalik Prints Private Limited in 1991, name changed to SPL Industries (SPLIL) in 1994

Company promoted by Mr. H.R. Gupta and Mr. Vijay Jindal

A leading manufacturer & exporter of Knitted fabric and Knitted garments

SPLIL designs, manufactures and sells a wide range of outer wear – T shirts, sweat shirts, polo shirts, etc. for top end customers in the international market

SPLIL has five factories in Faridabad covering 500,000 square feet spread over 14 acres of prime land

It employs about 4000 people including contract labour

SPL Capabilities

SECTION CAPACITY

Knitted Dyed Fabric 20 Tons per day

Mercerizing 05 Tons per day

Garment Washing & Dyeing 40,000 Pcs per day

Knitted Garments 750,000 Pcs month

Sweaters 100,000 Pcs per month

Strengths

Performance fabric is our major strength for customers like GAP, J.C. Penney, Haggar ( Forever New) and Perry Ellis.

Strong Product Development and Design Team

Yarn and fabric development – new textures and knits in different blends

Developing different washes and finishes on fabrics as well as garments

CAD system for design and fashion folio presentation and knit structure designs

Risk

Consumer Demand

Raw Cotton Price

Wage of workers

Customers

Gap Inc.

J.C. Penney Company

Kohl’s Corporation

Federated Department Store

Phillips-Van Heusen Corporation

Hartmarx Corporation

Sears, Roebuck and Co.

Haggar Clothing Co.

Supreme International

Disc. Please do on your study on script.

share your views. no holding. started tracking.