If you’re a frequent traveler from the late 2010s, you might know this company called SpiceJet. Many other airlines in India, like Jet Airways, Kingfisher, Go First, and even the original Air India, have gone bust under the weight of high debt—each a fascinating case study in itself. The airline business is notoriously capital intensive, and with major players like IndiGo and Air India dominating the sector, competition is intense.

As value investors, we typically look for businesses with strong earning power, real competitive advantages, low debt, and high entry barriers. Unfortunately, the aviation sector rarely checks these boxes—instead, it’s marked by fierce competition, heavy debt, low earnings, almost no sustainable moats, and extreme cyclicality. Still, it’s worth noting there are only two publicly listed airlines in India: IndiGo, with a market cap of ₹2,25,000 crore, and SpiceJet, with a much smaller market cap of just ₹5,000 crore.

There’s no doubt IndiGo has built a great brand image and driven down costs, resulting in higher profits. But do you really know what’s currently happening with SpiceJet?

SpiceJet has faced a series of problems in recent years, and understandably, this has been reflected in its share price. Surviving such stormy weather is no easy feat. At the heart of this comeback story is Ajay Singh, who left SpiceJet in 2010 but returned in February 2015 by acquiring a 58% stake. Here’s a detailed thread on SpiceJet’s journey—from turbulence to triumph.

Here’s what I’ll cover in this thread:

- The company’s history from 2008 to 2015 (what went wrong during this period)

- The years 2015 to 2020 (the “unlucky” phase)

- The impact of COVID from 2020 to 2023 and how IndiGo capitalized on the crisis

- The story behind SpiceJet’s QIP (Qualified Institutional Placement)

- The company’s future vision

- Financials

- The current tailwinds

Let’s dive in!

1. The Company’s History from 2008 to 2015

Back then, Kingfisher and Deccan Airlines were truly famous names, having captured a huge share of the market. Both, as you know, no longer exist—and the reasons behind their downfalls are well documented, so I won’t get into that here. During this era, SpiceJet operated as a determined low-cost carrier with a clear vision to grow in the budget airline segment. However, the 2008 financial crisis sent airline valuations crashing across the industry. SpiceJet reported significant losses of ₹344.73 crore for the nine months ended December 31, 2008, compared to just ₹9.89 crore the previous year.

In July 2008, Ajay Singh managed to secure a major boost for the company by convincing renowned American investor Wilbur Ross to invest $80 million (about ₹345 crore) in SpiceJet. Ross, well known as a “vulture investor” specializing in distressed assets and company turnarounds, brought both money and confidence to the airline.

The Remarkable Turnaround (2009–2010)

Singh’s efforts—coupled with Ross’s strategic investment—sparked a remarkable recovery. SpiceJet posted a net profit of $12.9 million (approximately ₹61.4 crore) in FY2009–10, turning around from a loss of $74.2 million the previous year. This achievement made SpiceJet the only listed Indian airline to report a profit that year.

By the time Ajay Singh left the company in 2010, SpiceJet had managed to build up substantial cash reserves of ₹800 crore. Around the same time, Wilbur Ross sold his 37.5% stake for ₹750 crore to Kalanithi Maran’s Sun Group in June 2010.

Downturn After 2010 – The Irony of Success

Ironically, Singh’s departure marked the beginning of turbulent times. Under Kalanithi Maran’s leadership, SpiceJet’s fortunes reversed dramatically. Despite having ₹800 crore in cash when Singh exited, the airline accumulated more than ₹3,000 crore in losses over the following years, nearly collapsing by 2014.

Maran’s strategy emphasized rapid expansion, including the purchase of Bombardier Q400 aircraft to tap into smaller city markets. Unfortunately, this aggressive approach led to severe financial troubles: the company’s debt skyrocketed from ₹55 crore in 2011 to ₹1,678 crore by 2013. Experts believed that this downfall was due to poor administration at top level, lack of funds, high loan repayment charges and surging ATF cost.

By 2014, SpiceJet was on the brink of bankruptcy. But just as things looked their bleakest, a dramatic twist was about to unfold…

2. The Years 2015 to 2020 (the “Unlucky” Phase)

Ajay Singh took control of SpiceJet in 2015 by acquiring a 58% stake, bringing with him a clear vision to rapidly expand the company, both domestically and internationally. However, patience is essential in any business—expanding too quickly, especially by taking on heavy debt when demand isn’t keeping pace, can spell trouble (just look at the fate of Jet Airways).

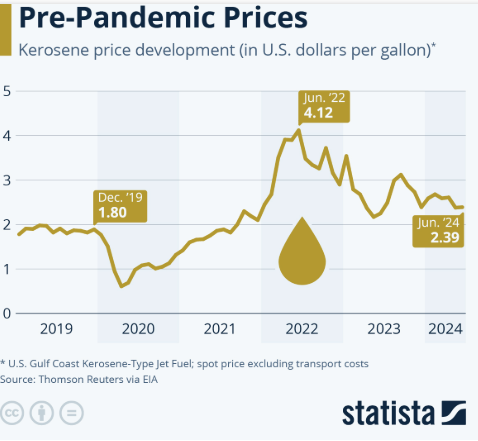

Initially, Singh made responsible moves by prioritizing the payment of outstanding dues and staff salaries to stabilize operations and restore morale. But in 2017, he made a bold bet by placing a massive order for 205 aircraft—a staggering capex commitment reportedly worth around $22billion (about ₹1.5 lakh crore; you’re close on the numbers). This included a large number of Boeing 737 MAX aircraft, which, at the time, promised 20% greater fuel efficiency compared to older models. Given that fuel costs often account for 30-40% of an airline’s expenses, this seemed like a win-win for SpiceJet.

CREDIT- STATISTA

Unfortunately, tragedy struck: the Boeing 737 MAX was grounded worldwide due to safety concerns after high-profile accidents. This left SpiceJet in a tight spot—they had already committed to buying the planes, and unlike shopping online, returning such orders isn’t an option. The company was forced to bear the costs of the new aircraft while dealing with depreciation and the burden of expanded loans. Meanwhile, competitors moved ahead with newer, fuel-efficient planes but without the same safety issues, putting SpiceJet at a distinct disadvantage.

The financial strain was evident: annual aircraft lease costs reached $180-190million, and repeated cash flow crises led to delayed salary payments and damage to the company’s reputation. Just as SpiceJet was navigating the Boeing 737 MAX crisis, the COVID-19 pandemic hit, dealing the business a brutal “double whammy.”

Still, it wasn’t all bad news. Ajay Singh and his team managed to accomplish several positive things during this phase:

- Paid overdue staff salaries.

- Settled outstanding dues with oil companies.

- Rebuilt passenger confidence.

- Maintained reliable schedules with minimal cancellations.

- Cut unprofitable flight routes.

- Achieved higher fleet utilization by making the most of available planes.

Despite the relentless challenges of this period, these actions helped stabilize the business and kept the dream of a turnaround alive.

3. The Impact of COVID (2020–2023) and How IndiGo Pulled Ahead

At the start of FY21, India went into lockdown and, as we all remember, travel came to a complete standstill. “When you’re down, the whole world seems to hit you harder.” For SpiceJet, already saddled with massive debt, the lockdown delivered another major blow: with no one flying, business took a nosedive. That year alone, both IndiGo and SpiceJet saw sales plunge by around 60%.

As if that wasn’t enough, there was a sharp post-COVID surge in fuel prices—nearly doubling—which ballooned costs even further for all airlines.

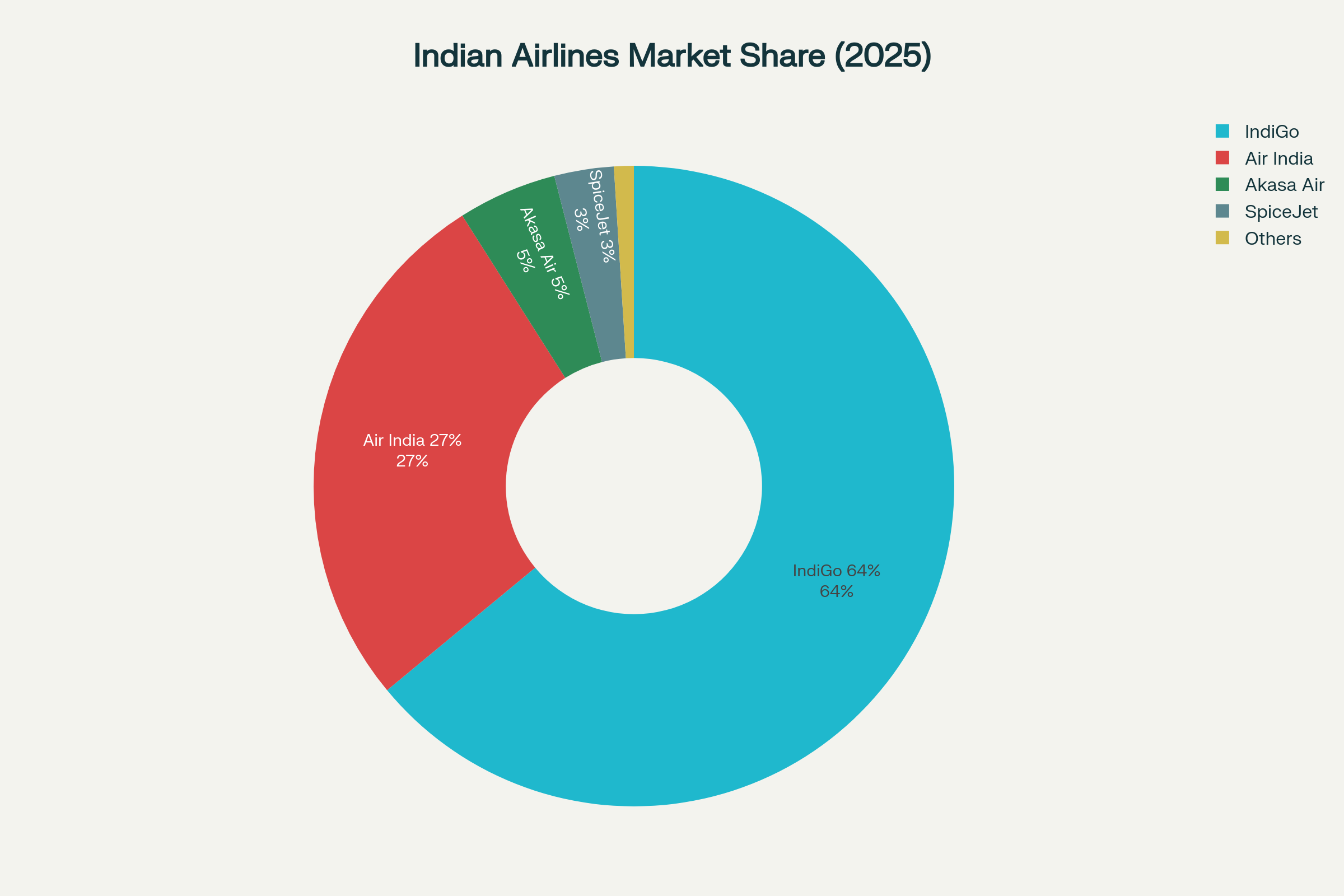

For SpiceJet, the situation was especially tough. The grounding of their Boeing 737 MAX planes became a financial nightmare: the company had to keep paying hefty lease payments on aircraft they couldn’t even operate, leading to even greater losses. To make matters worse, SpiceJet’s market share evaporated, dropping from 13% in 2019 to just 2% today.

You might wonder why, after the dust settled, IndiGo bounced back while SpiceJet continued to struggle. After all, if IndiGo could recover, why couldn’t SpiceJet? Honestly, even I don’t have all the answers on what happened to SpiceJet’s post-COVID recovery, but if anyone does, I’d love to know.

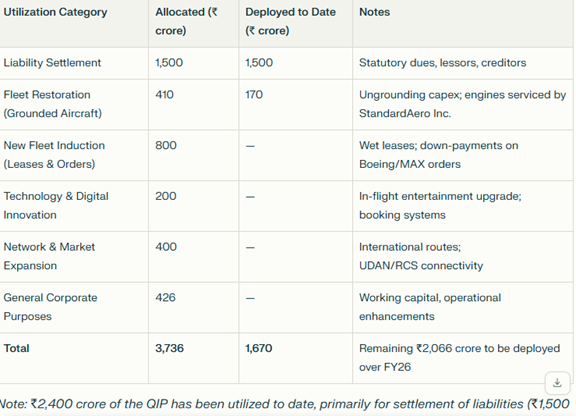

4. The Story Behind SpiceJet’s QIP (Qualified Institutional Placement)

SpiceJet’s Qualified Institutional Placement (QIP) of ₹3,000 crore was conducted between September 16 and 18, 2024, and was oversubscribed, attracting participation from a broad mix of institutional investors, mutual funds, and prominent family offices. The company allotted more than 48.7 crore shares at ₹61.60 each to over 80 investors.

Major institutional investors who participated in the QIP include:

- Goldman Sachs (Singapore) Pte – ODI

- Morgan Stanley Asia

- BNP Paribas Financial Markets ODI

- Nomura Singapore Ltd – ODI

- Societe Generale – ODI

- Discovery Global Opportunity (Mauritius) Ltd

- Tata Mutual Fund

- Authum Investment and Infrastructure Ltd

- Bandhan Infrastructure Fund

- White Oak

- Carnelian Bharat Amrikaal Fund

- 360 ONE Equal Opportunity Fund

- The Jupiter Global Fund

Additionally, several leading Indian family offices—such as those of Madhu Kela, Akash Bhanshali, Sanjay Dangi, and Rohit Kothari—also took part in the allocation.

This QIP was seen as a strong vote of confidence in SpiceJet’s potential turnaround and revival strategy, giving the airline the capital needed to pay overdue dues, revive its grounded fleet, invest in growth, and restore market reputation.

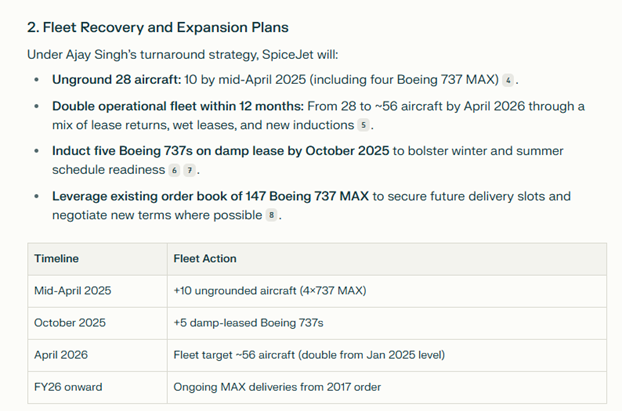

5. The Company’s Future Vision

Mr. Ajay Singh has consistently demonstrated remarkable management skills. Just imagine—a business with unfavorable economics, intense competition, and mounting challenges, yet this man has managed to steer the company clear of bankruptcy. Surviving in this sector over the past two decades is no small feat, and Ajay Singh has truly given his full potential to keep SpiceJet afloat and moving forward.

Despite the odds, he’s navigated the airline through turbulent times, restoring stability and charting a clear path toward revival and growth. The future vision for SpiceJet under his leadership focuses on revitalizing the core airline business, expanding the fleet, tapping into new technology, and exploring fresh market opportunities—while continuously negotiating to reduce costs and improve operational efficiency.

For those interested, here are some insightful interviews where Ajay Singh himself discusses the company’s vision and journey:

It’s also worth noting that there were legal cases filed by the former promoter (remember I mentioned Kalanithi Maran earlier?), but that dispute has now been resolved. Just a couple of days ago, the Supreme Court dismissed Kalanithi Maran’s plea seeking damages worth ₹1,323 crore against SpiceJet, finally putting this long-standing issue to rest.

All things considered, Ajay Singh’s persistent efforts and ability to adapt have set the stage for a potential turnaround, and the future of SpiceJet looks a lot brighter under his watch.

Currently, SpiceJet operates 147 daily flights across 38 domestic locations and 3 international destinations.

I also read that they recently entered into a deal with a U.S.-based company to repair their grounded Boeing planes, enabling them to bring these aircraft back into service. This move should help SpiceJet restore capacity and improve operational efficiency. Secured mandate from Government of India for Haj operations from Srinagar, Guwahati, Gaya, and Kolkata.

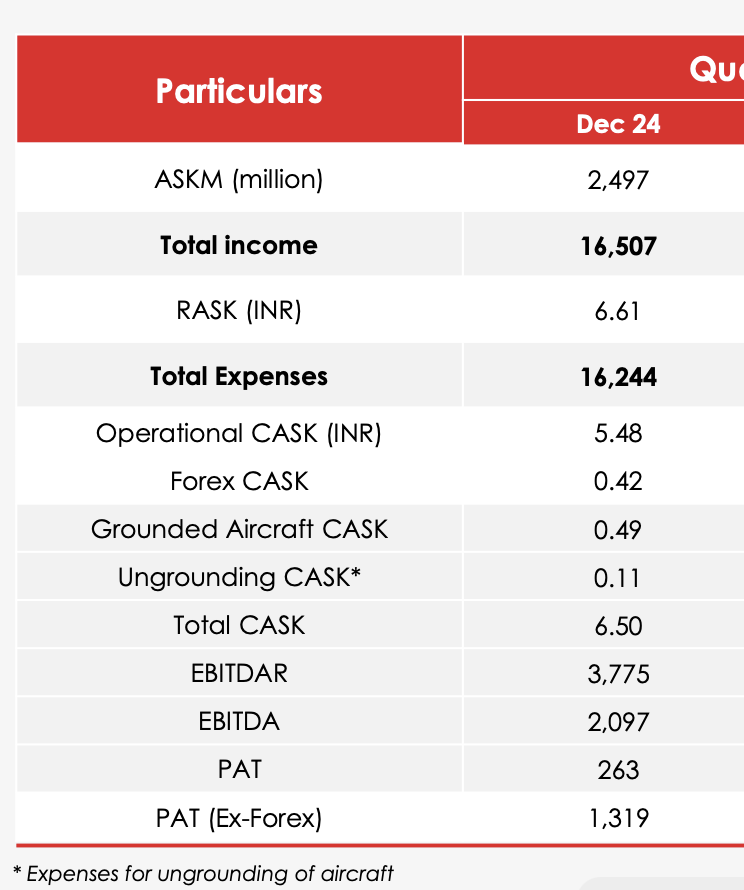

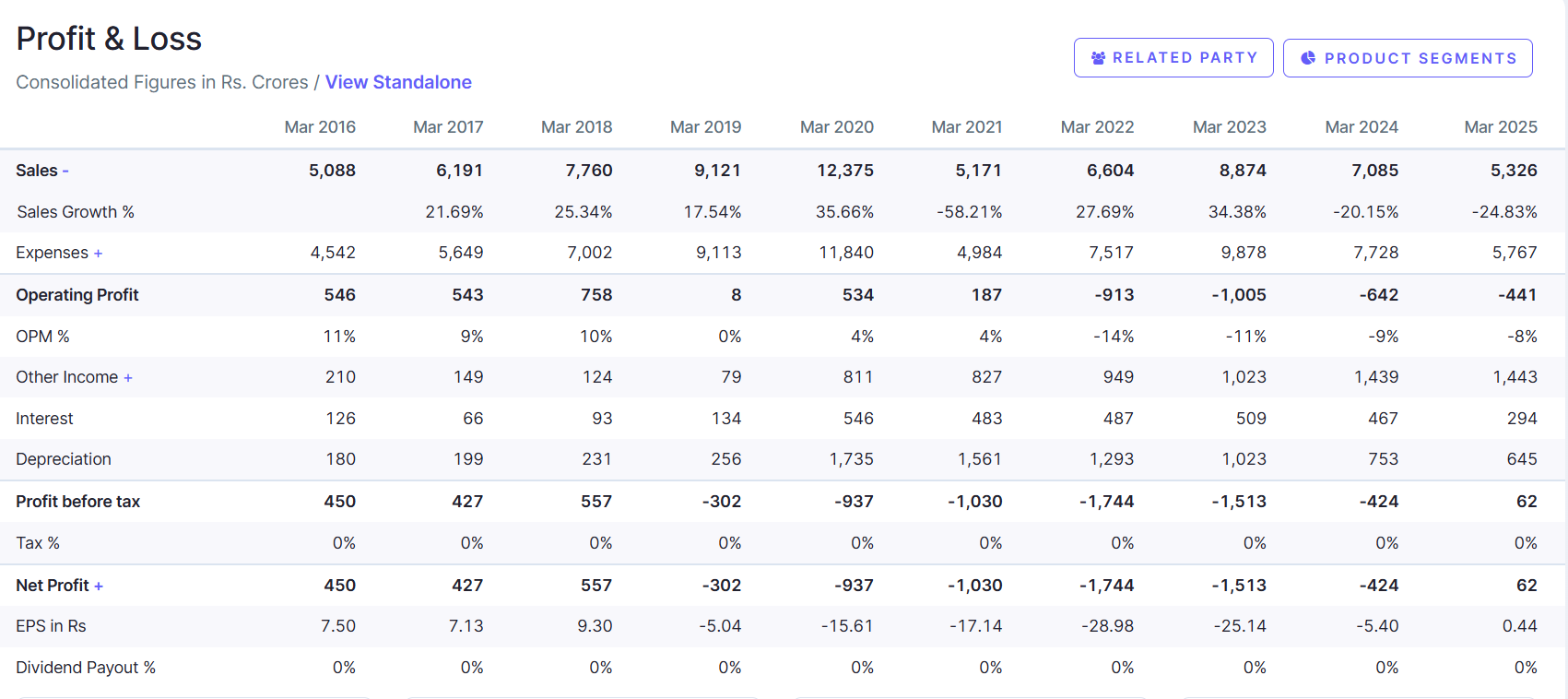

Financial Details & Recent Highlights

- Increase in Other Income:

There has been a significant rise in “other income” for SpiceJet over the past couple of years, echoing a tactic also used by IndiGo. This includes items like interest income, foreign exchange gains, and profits from sales of assets or other non-core activities, which help support overall earnings when operational revenue is under pressure. - Gradual Decrease in Borrowings:

SpiceJet has been steadily reducing its outstanding borrowings, which is directly reflected in lower interest expenses on the profit and loss statement - Positive ROCE:

For the past two years, SpiceJet has recorded positive Return on Capital Employed (ROCE) numbers, indicating more efficient use of capital and early signs of business recovery. - Negative Cash Flow:

Despite improvements in other areas, the company continues to report negative operating cash flow - Q4 FY25 Kumbh Mela Opportunity:

In Q4 FY25, SpiceJet smartly capitalized on the Kumbh Mela by redirecting flight routes to tap into surging demand during the event, resulting in a standout performance—posting a profit of ₹340 crore in just one quarter.

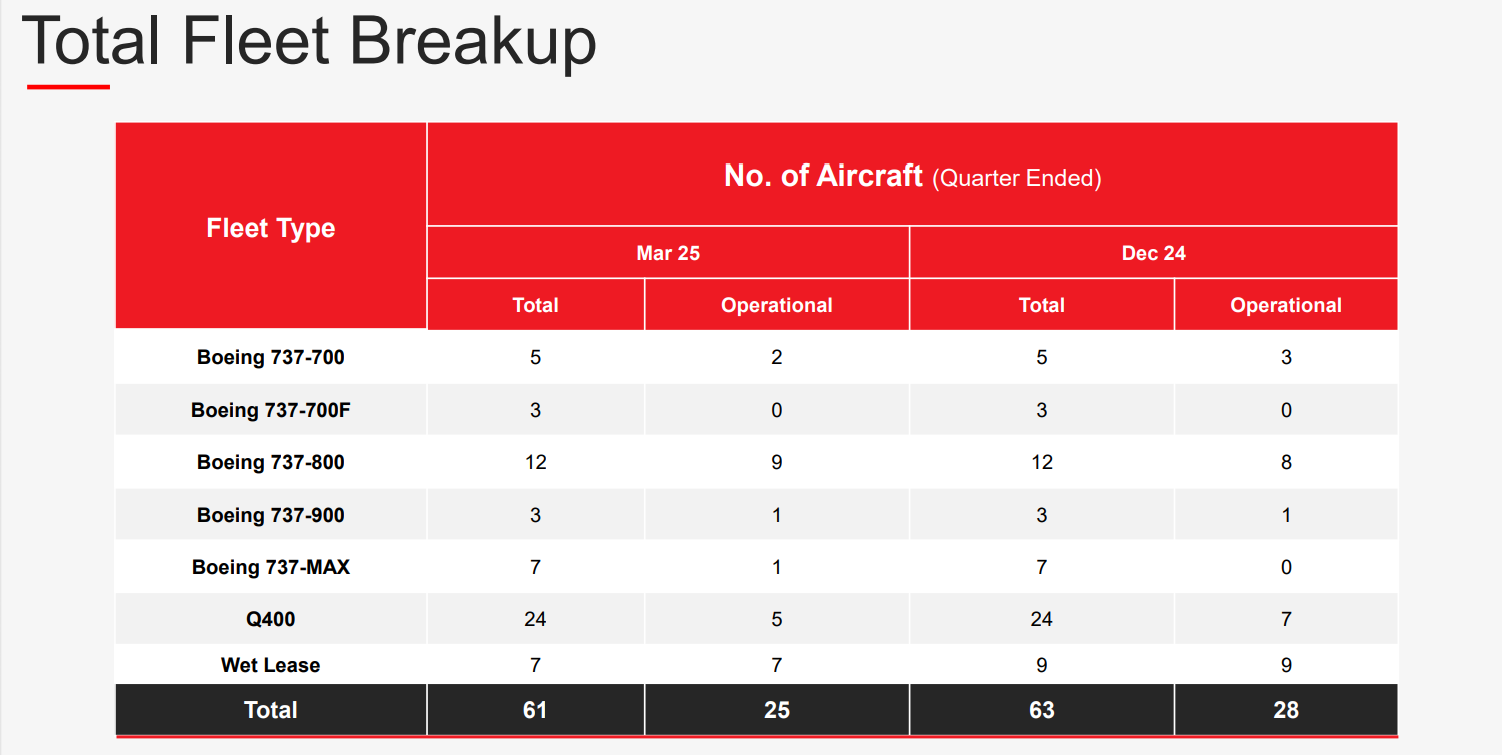

DETAILED BREAKUP OF THE AIRCRAFTS

BALANCE SHEET

PROFIT AND LOSS STATEMENT

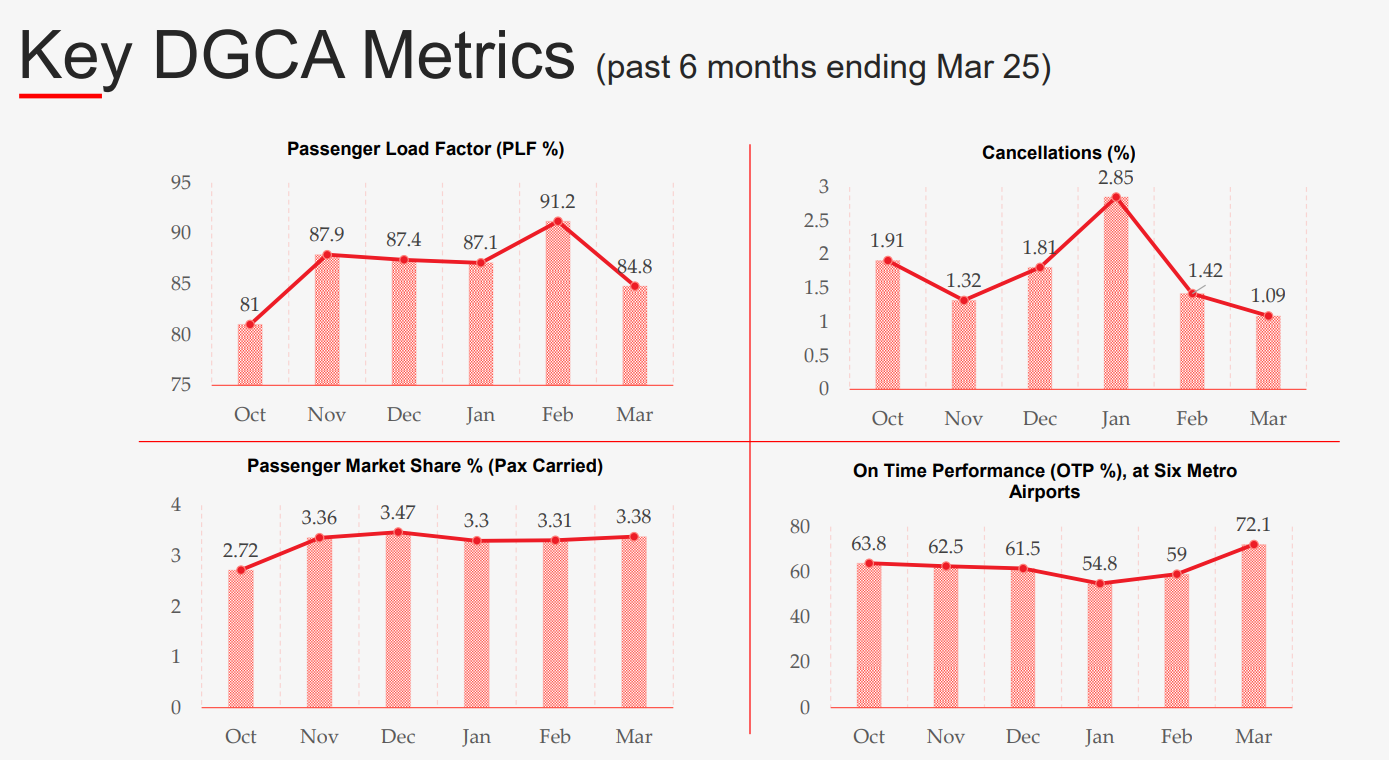

Key Metrics

Risk Factors

-

Things that happened before COVID can happen again; after all, there is a luck factor involved too.

-

There might be issues with the new aircraft ordered.

-

High fuel prices in the future could increase operational costs.

-

Possible management issues could arise.

-

Government restrictions and regulations may impact operations.

-

Intense competition in the airline sector.

-

The turnaround strategy might fail to deliver the expected results.

-

Challenges in paying for new planes and interest on loans.

-

Any incidents similar to the recent Air India crash in Ahmedabad.

-

Damage to goodwill caused by human error.

Thanks for reading! If you spot any mistakes in my numbers or information, feel free to reply and correct me—I genuinely appreciate your participation and input. Let’s keep the discussion going!

Credit - " Abhishek Pokharna"

Disclaimer - invested