Spectrum Talent Management- Proxy to Indian Economy Growth ?

. Company Overview

- Business Model: Spectrum Talent Management Limited (STML) operates in the staffing and recruitment industry, offering services such as general staffing, IT staff augmentation, Recruitment Process Outsourcing (RPO), and apprenticeship solutions.

- Global Presence: With operations across several countries, the company leverages global and Indian talent cost arbitrage, especially in IT and US staffing

- Good Promoters: First Gen promoters, friends from college, doing this same business for 10+ years

2. Financial Performance (FY23)

- Revenue Growth: STML reported a significant year-on-year revenue increase to ₹7,688 million in FY23, up from ₹4,832.21 million in FY22, demonstrating a robust growth trajectory.

- Profitability: The company achieved a net profit after tax (PAT) of ₹278.13 million in FY23, with a profit margin improvement to 3.6%, compared to 3.2% in FY22.

- Capital Efficiency: Return on Equity (ROE) stood at 49.83%, and Return on Capital Employed (ROCE) was 59.30%, indicating that they almost turn their Asset base (workforce exployed) 12 times a year, which is logical given the nature of the business, so 12 time Asset Turnover * 3% margin is a 36 RoCE business, current RoCE is probably higher due to a better blended RoCE due to the business of trading of electronics good

- The Fund Flow Analysis provided traces the sources and applications of funds for Spectrum Talent Management Limited over a specified period. Let’s dissect and interpret this data to understand how the company has managed its financial resources over the years

- Equity + Reserves:

- There is a noticeable increase in equity and reserves in certain years, particularly a significant inflow of ₹33 crores in Mar-22. – IPO gains were distrubted between OFS and Working Capital needs for future growth

- Debt:

- The movements in debt indicate both increases and decreases over the years. For example, an increase of ₹10 crores in Mar-21 followed by a decrease of ₹7 crores in Mar-22 suggests debt repayments or refinancing activities.

- Trade Payables + Other Liabilities:

- Increases in trade payables and other liabilities indicate the company deferred some payments or accrued more liabilities, this might be skewed because of the electronics good segment and/or Collect and Pay model which contributes ~50% of the business wherein companies pay spectrum first and then spectrum pays workforce employed

- Equity + Reserves:

3. Market Position and Growth Strategy

- Industry Leadership: STML has a strong market position in a growing staffing industry, which is crucial for companies adjusting to dynamic market conditions. There are multiple manpower agencies in the market, but size of the business of STML is big enough to put them into an organised / large player category. The biggest in India would be Quess Corp, TeamLease as two listed entities and IT services business like TechMahindra, TCS etc who are also kind of competitor to them as well as customer in IT Staffing vertical

- Expansion Strategy: The company focuses on volume-driven growth in staffing, high profitability in RPO, and scaling IT staffing and US staffing verticals. The upcoming Industrial Staffing will be a good and a big market to come where manufacturing companies if they want to grow will hire blue collar workforce through agencies like Spectrum which is a medium margin but a bigger business in Pay & Collect model – their working capital needs will go up naturally as the salaries need to paid to workforce first and then collect

4. Challenges and Risks

- Economic Conditions: Global economic uncertainties and potential industry-specific risks could impact staffing demands. The company needs to navigate these challenges by leveraging its robust service portfolio and global presence. In the last con call they already shown the impact of Layoffs in USA and slow hiring in India IT segment. On the flipside, layoffs help manpower agencies after the market turns up as layoffs also require re-hiring which gives them revenue through recruitment fees. This should be cyclical in nature, so when industry upturn is going on then spectrum earns through fees on salary and in downturn/slowdown through recruitment fees

- Customer Concentration Risks: As with all staffing firms, operational risks such as client concentration and dependency on certain industries or geographies could impact performance. Spectrum’s diversified client base and industry coverage might help mitigate this risk

- Working Capital Risks – things might blow out of proportion if they are not able to recover the dues from comapnies, right now their Bad Debt provision is neglible. So a watch on their Debtor Days and PDD is going to be important

5. Investment Rationale

- Growth Prospects: Given its aggressive growth strategy, particularly in high-margin areas like RPO and global staffing solutions, STML is well-positioned to capitalize on global staffing demands. Promoters have given a CAGR of 30-35% growth prospects overall for the next 3-5 years

- Competition & MOAT: No point of looking at competition as the market is very huge, and underpenetrated, plus there is a Switching Cost applicable on the Customer(Big clients of companies) where manpower agencies levy 3-5% of the total salary bill as one time expenditure- also a Recruitment Skills of manpower agency of hiring good talent and in less than 15-20 days as KPI act as a good Moat. In the conference call they mention that till date no major customer has left them and have 200+ brands associated with them also they maintain no bench (which says they are able to service the recruitment needs of companies as soon as possible). All in all, higher Switching Cost + Higher Customer Retention + Tech Platform as Intangible should develop into a Moat.

- Financial Health: The company’s strong financial performance, high profitability margins(compared to Peer, it has +1-2%) , and these margins will remain 2%+ for the time to come as they have a good tech backup (mentioned in the Intangibles section)

- Strategic Initiatives:

- Recent initiatives such as the IPO gives them opprtunity to fund working capital which is almost 1:1 ratio resulting into sales.

- They are also building Tech needed to handle both Supply and Demand side- in the manpower agency business this kind of advance tech has become very important as it is the only competitive edge apart from recruitment skills.

- Artificial Intelligence (AI) and Machine Learning (ML): These technologies are used for parsing resumes, matching candidates with job descriptions, and predicting staffing needs based on historical data.

- Blockchain: This can be employed for verifying the credentials of candidates securely and transparently, reducing the risk of fraudulent documents and enhancing trust.

- Big Data Analytics: Used to analyze trends, predict industry shifts, and optimize staffing solutions based on data-driven insights.

- Robotic Process Automation (RPA): Automates repetitive tasks such as data entry, candidate screening, and initial communications, which can significantly speed up the recruitment process.

- Cloud Technologies: Provide scalable infrastructure to support growth and enable the seamless integration of various services across different geographies.

- Mobile Applications: Facilitate remote access for candidates to apply for jobs, update profiles, and communicate with recruiters; for clients, these apps provide real-time updates on staffing placements and administrative functions.

- Tax Benefit:- The tax benefit under Section 80JJAA of the Indian Income Tax Act is a significant incentive for companies, including Spectrum Talent Management Limited. Employees must be employed for a minimum of 240 days during the year (150 days for apparel manufacturing employees as per amendments).The employee’s salary must not exceed ₹25,000 per month to qualify for this benefit. Employers can claim 30% deferred tax on the salary cost of these <25K

6. Valuations

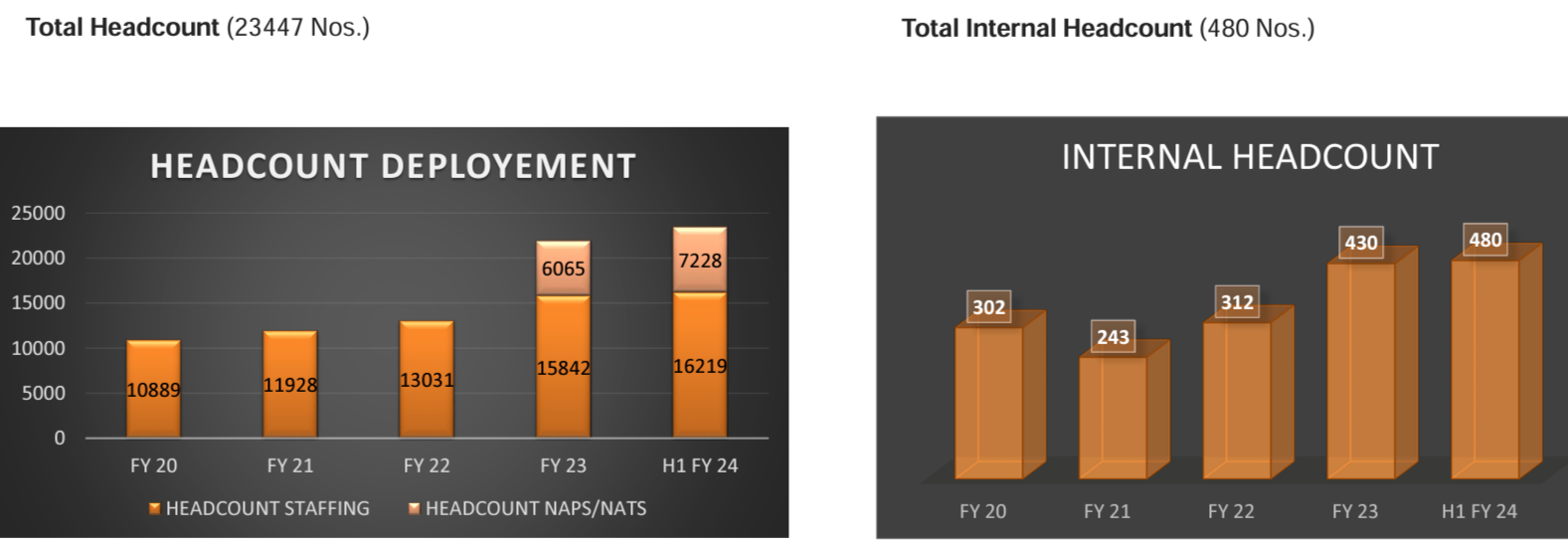

Year Total Workforce Deployed Segment Revenue from Manpower Services

(₹ Mn) Segment Profit (₹ Mn) Total Revenue per Workforce

(₹ Lacs) Profit per Workforce

(₹ ‘000)

FY20 10,889 3,794.4 137.4 ₹34.86 ₹12.6

FY21 11,928 3,790.37 135.19 ₹31.78 ₹11.3

FY22 13,031 5,034.1 187.66 ₹38.62 ₹14.4

FY23 16,219 5,034.1 189.8 ₹31.02 ₹11.7

H1 FY24 23,447 2,851.35 (H1) 41.06 (H1) ₹24.32

(H1 rate annualized) not comparable

from the above table there are two takeaways –

- workforce deployed has become 2X in last 4 years, which shows the business expansion

- they make on an average ~12K profit per workforce annually, this margin range will flucuate between 10-15K as the business grows and industry /customer/ staffing mix changes

At current business they are valued at 10 PE, whereas TeamLease is at 51 PE, which is exactly the same business and has a lower margin % and lesser RoCE, so a potential re-rating candidate with 3-5X possibilities.

Also looking at the future potential and the growth visibility given by the promoters – they should grow 30-35% for next 3-5 year which looks like 2.5 times the current revenue and at the same margin profile and capital efficiency they maintain that makes a proper 2.5-4X opprtunity

so Business Growth plus Earning Re-rating, both put toghether is a 6-20X opportunity from now.

Disc- NISM certified Research Analyst but not a SEBI certified Investment Advisor, this isnt a Investment Advice.