Rswm -a textile stock

Rights issues arbitrarge

Cmp 350

Issue price 100

Ratio : 1:1

Record date : 16 dec, friday

Very attractive opportunity.

Disc :Invested very heavily. Largest position

Please spare some time and checkout.

https://twitter.com/CaJainankur/status/1602338658941825024?s=20&t=uJKg1a8QCGcvS6qy1nOPFQ.

This twitter thread can help.

Will Write in detail later.

How is/was this an attractive opportunity? It would be great if you can share your calculation/justification.

Stock price was expected to nearly halve on the record date (as happened). Taking into this adjustment into consideration, break-even of investment is possible only if we get extra allotment of more than 100% of rights issues. With only about 10% as small retail investors, I don’t know what extra allotment can be expected. Also, we should not forget that there is a risk of fall in the stock price due to market conditions and macro. So it is unclear how this is an attractive opportunity.

I want to know…what should be the strategy of selling shares which were originally bought in case of rights. Should we sell them immediately on the record date or wait for later.

Let me tell this with an example

Suppose on record date you have 10 shares of rswm at 355

Tomorrow it will open at 227.5 ( theoretical ex right issue price) TERP

(But it always depends on Market fluctuations. It opened at 223.65 and now 202)

Now ratio being 1:1 , you get 10 share at 100 rupees.

So you get breakeven, if the Price stays at 227.5 and you are able sell the original share you are entitled at that price

Now for extra allotment

If you apply for extra shares get 2x allotment ( 1x -original, 1x - extra)

So 20 shares at 100 which you can sell at current market price.

And that extra allotment 10 shares will give you the profit.

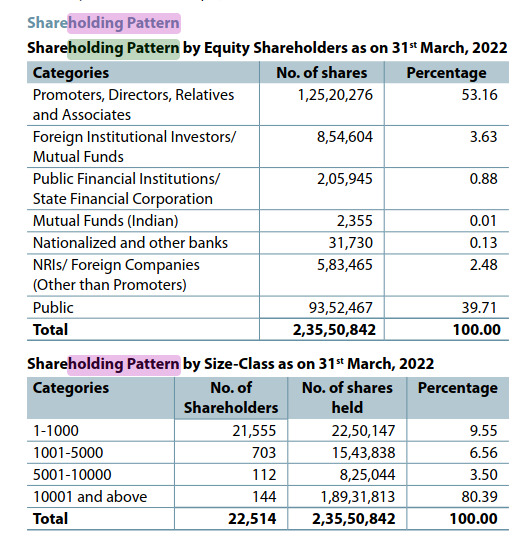

I feel the chance of allotment is good because promoter holding is around 50 and shareholding less that 2 lakh is around some 25 percent.

And yes there is always a market risk. If the current market price goes below the TERP price, you get loss on the original entitled shares

And below the issue price for extra alloted shares.

You must sell that share after the record date so that you can reduce the market risk and free money to apply for extra share

Disclosure: invested 35 percent of portfolio.

Was able to sell only 1/3 of position at 223.65.

Trying to sell the remaining ![]()

Checkout

https://twitter.com/CaJainankur/status/1602338658941825024?s=20&t=uJKg1a8QCGcvS6qy1nOPFQ

This see the pinned thread of this guy

Thursday is the record date for quint. Attractive discount to cmp. Tomorrow is the last date (T+1)

But overvalued in my opinion.

Feel free ask if you don’t understand. I will try to explain better

Thanks for the detailed explanation.

How did you arrive at this percentage? From the FY22 Annual Report, I see shareholders holding less than ₹2L is about 10%, not 25%.

If we assume most of these 25% retail shareholders let their entitlement elapse, how can we expect 1X extra allotment? Should we also assume that shareholders who are applying for the rights do not apply for extra allotment?

On the record date, the price adjusts for dilution due to additional rights issues (It is automatic).

If we got the original shares only for playing the rights issue special situation, it is probably best to sell on the record date, simply for the reason that we don’t have any further rationale behind holding them. In such a case, holding is purely speculation.

If we think that the stock we hold is cheap and of decent quality, and we can hold for a year or so, we arrived at a reason to hold.

That’s just my understanding. Would love to know the answer from experienced investors in this regard.

What is the date of allotment of RSWM Rights Issue?

13 Jan 2023 is the deemed date of allotment. Source: RSWM Rights Issue 2022 Rights Issue Detail

Sir…what is the reason for assumption that the company is going to be sold…and if so what would the time period be taken?

Has anyone recived shares of RSWM in their Demat?

Disclosure: Am trying to understand special situation, below illustration is just for study and feedback purpose.

Sportingking India announced tender buyback with record date as 10/2/2023.

BB size: 580,000 shares @ Rs. 950 = Rs. 55 cr 10 Lakhs; is 4.37% of total stock.

CMP: 693, premium is appro 37%.

Promoter holding: 74.15% which is 98,52,048 total stock; out of that 85,66,048 can be tender by promoter. Total is 1.33 cr stocks represent 100%.

15% reserved for Retail Investor (RI).

BB reserve for retail is 580,000 * 15% = 87,000 nos of stocks.

RI can be defined as Rs. 200,000 / 700 (Considering ~ CMP) = 286 stocks

As per latest AR, UP to 5000 stock is hold by 5.1% which comes to 678,217 numbers.

Not able to find details of holding under Rs. 200,000 or 286 stocks holder. Hence just has to assume…

Ass 1: Assume 33% of 6,78,217 is holding below 286 stocks which is 2,26,072.

If so success ratios of 87,000 stock bb from 2,26,072 is ~ 38.5%

As above understanding correct?

Nos are approximate and taken from recent disclosures and AR.

Help: If anyone suggest where I can find recent details of RI.

Disc: Not holding any position as of now. Not sebi registered, just for understanding and feedback purpose to understand more on special situation.

Team Lease BB:

BB Size: 3,27,869 Equity Shares of Rs. 100 cr

At a price of ₹3050

CMP Rs. 2363 on 6/2/2023

Discount: 29%

Small RR: Rs. 200000/3050 = 65+ shares (actual calculation should be as per mkt price of record date, however for to be more safe we can calculate BB price).

15% discount for small RR:

Total BB size 327869 @ 15% = 49180 shares for small RR BB

Individual shareholders holding nominal share capital upto H 2 lakh 9,06,176 (Source AR of Fy 2022, page 139)

Hence acceptance ration seems 906176 @ 49180 = 5.42%.

This seems low acceptance ratio, imo. Looking for counter opinion.

Disc: Not invested.

Disclosure: Added a major position today

SAREGAMA is going to Demerge its Non Core Biz.

Special situation emerging in Maharashtra Apex, because of 35% holding in Kurl-on. Sheela Foam buying Kurl-on for around 2000cr, shareholders of Maha Apex can expect some windfall gains, though actual value is difficult to gauge. These are very tricky situation, as actual gain depends upon several factors, like promoters integrity, liabilities of the holding company, taxation etc. Still I am expecting fireworks in the Maha Apex counter next week as it will resume trading following SEBI decision on ESM 2nd stage companies. Can I request interested parties, seniors to throw light on the emerging situation for benefit of all concerned?

NB- Have a tracking position, so views may be taken as biased .

The price has already run up quite a bit. Unsure about the margin of safety in the current prices given the uncertainties pointed out by you.

Yes, i agree… going by the fact, that they have around 38% of Kurlon shareholding, their value/share comes to Rs 760 crore… currently the share is around Rs 165 at 250 crore market cap… so it is at one-third of the intrinsic value … Quite a lot Margin of safety is there, but it all depends on Management’s integrity, corporate governance and how their attitude is towards minority shareholders

@Karthikbaskaran i have a question here. Anyone please feel free to answer. If the announcement date and ex- rights date have only 1-2 days in between then how to go about it. How do you guys track these events??

Ex-Date is the day before Record Date. Announcement date can be ignored its usually several quarters before the event.