I see interest here has died completely just as things are beginning to look up. The OpIndia article must have been a scary read for investors when it happened. A lot of things in this piece are outright unprofessional but I think post the settlement with Padmaja last year, things seem to have been laid to rest.

I feel the old management may have done some questionable things, especially when I compare some of the old disclosed data that are laughable in retrospect

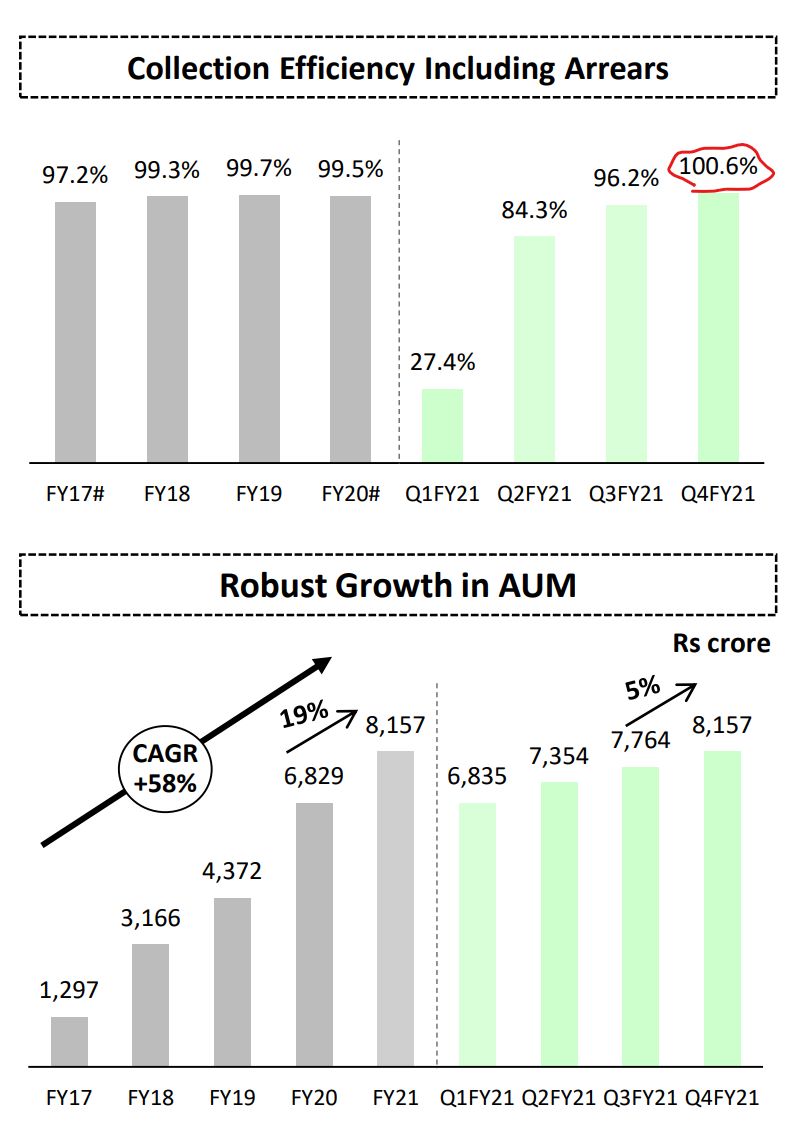

Not even CreditAccess Grameen had such numbers during the pandemic. My theory is Kedaara wanted a management changed to get better transparency and thankfully they have been successful after a lot of hurdles and have now built a very good team. The business now is doing concalls and last 5 concalls track the trajectory of the business nicely and we are now at a great place

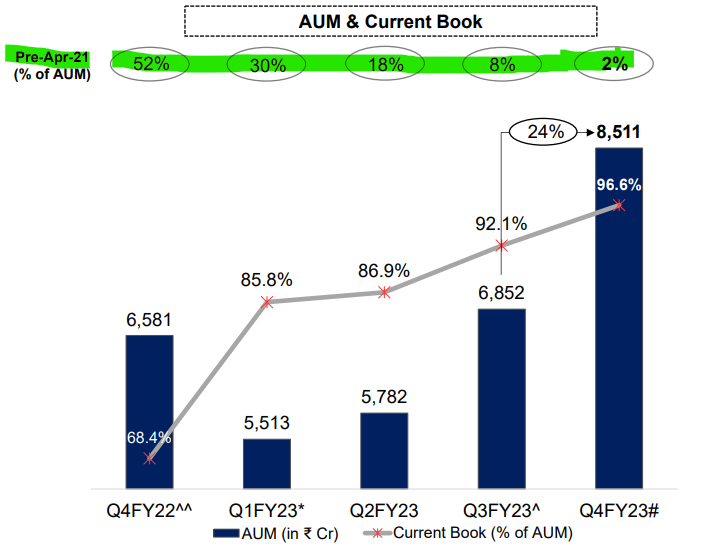

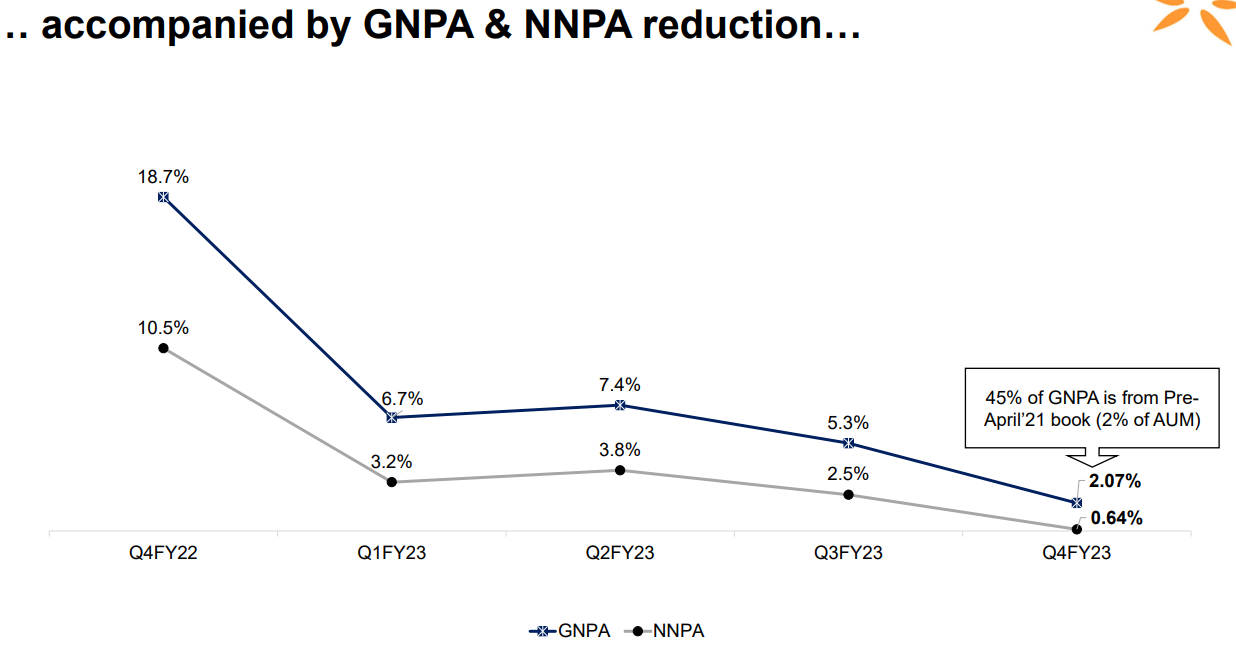

The new management is doing good things and walking the talk. The Pre Apr '21 book is now just 2%.

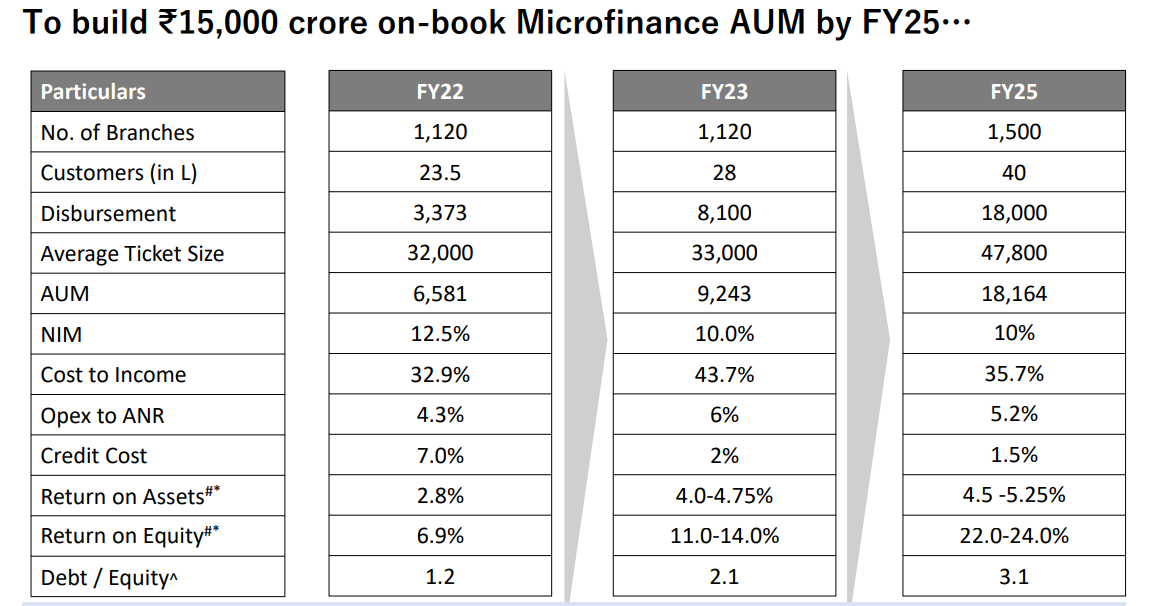

The Vision 2025 document (Slide 25 onward) talks of growing AUM to 18,000 Cr by FY25 (Microfinance is 15k in this). They are at 8500 Cr and so far have been almost on track on everything they have promised in Jul '22 Vision document for FY25

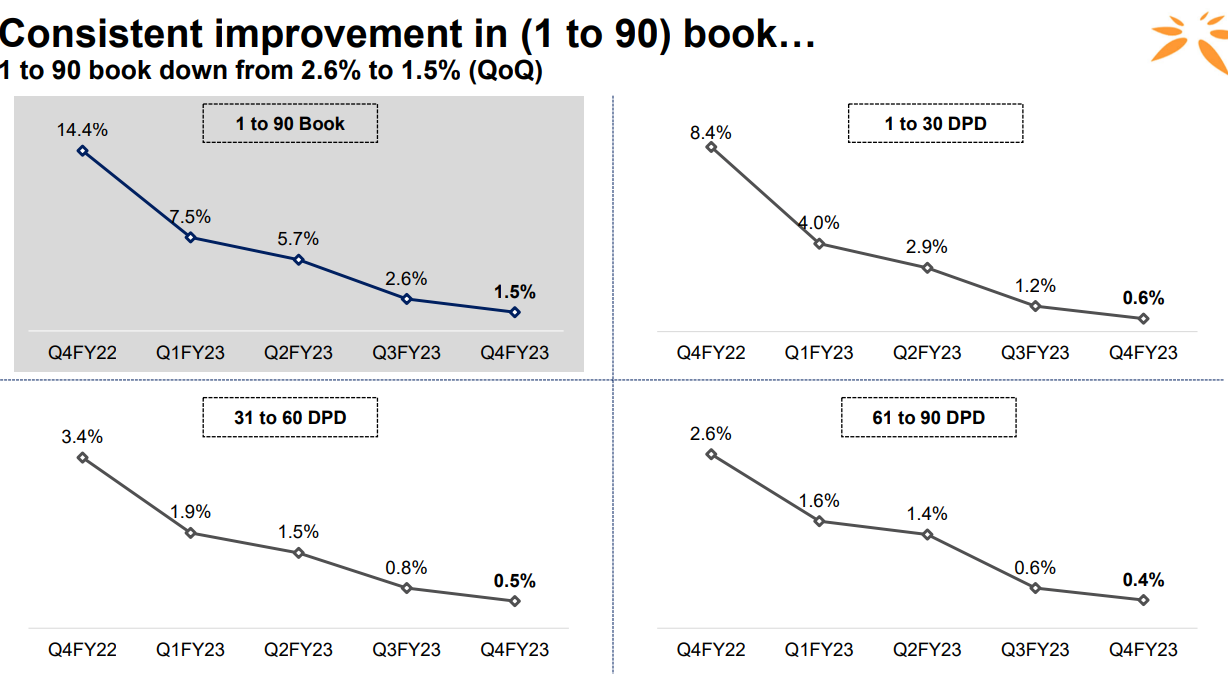

They have done a good job in cleaning up the pre Apr '21 book

RoE for Q4 FY23 was at 14.1% and management sees this trending up to 22-24% levels

The issue I don’t see clearly addressed is why is the pre Apr '21 book so bad vs post Apr '21, even though both were during the old management’s tenure? I see analysts in the call fishing for something on this. The new management has been professional not to do any mudslinging and has owned up the book as it stands and have done the cleanup. With Padmaja still being a large shareholder, I suspect they cannot speak their mind openly anyway if there was any misreporting in the pre Apr '21 period

That brings us to the risks

-

Padmaja’s shareholding is an overhang on the stock though at the management level and CXO level there has been a complete cleanup. She refused to sell at 1.5x book to Axis (according to her claim that Kedaara wanted to exit at 1.5x to Axis, for her reason to resign), so don’t see why she should do so now. It might be better for the business as a whole and other shareholders if this exit happens sooner than latter though

-

Is Kedaara in this for the long haul or did they replace the management only to exit at whatever valuations? Going by the zest of the new management, I think Kedaara is in this for the long haul and is building a better quality business under a very well-paid professional management

-

The usual MFI and political risks - At this point in the cycle though, I think we are at the start of a new cycle with clean books and good growth prospects. At cyclical bottom, this is perhaps not the risk to worry about

Valuation is very much in favour due to the risks above but the sector as a whole looks set for a re-rating. Spandana run by a professional management (mostly ex-BFIN) could command a much higher valuation like 2.5x or 3x P/B and book value itself is set to grow ~20% for the next 2 yrs, so overall there appears to be a scope for making 2-3x here in the next year or two.

Disc: Have positions in the stock from current levels. Not SEBI registered and could be wrong with my assumptions and views. Please do your own research