Very bad numbers posted by the company. Revenue from export division fell by 20% YoY due to 2 of their customers going into administration. PAT fell by 93% YoY due to write-offs of MEIS incentives.

kitex garments which operates in the same industry had a fantastic performance this quarter. shows the huge difference in quality of the two companies.

SP Apparels has decided to sell its retail division on a slump sale/going concern basis to SP Retail Brands Ltd, an independent firm promoted by strategic investors along with the promoters of the former. The deal worth ₹81 crore will be settled by the latter partly by cash and a portion through its compulsorily convertible preference shares.

Looks like this is a distress sale and the buyer is a promoter backed firm. I think better to stick to firms like Kitex Garments

adjusted revenues stood at rupees 145 crores, which degrow by 21.6% year on year basis

adjusted EBITDA margin stood at 12.7% for this quarter. The margins comparing year or year decreased by 340 basis points.

The primary reason for the reduction in the margin is due to government’s recent decision to roll back incentives given to garment exporters under MEIS, which impacted our margins by 4%, which is around Rs. 22 crores

Second, due to the loss of revenue by rupees 25 crores due to the impact of the global pandemic situation

Third one due to the appreciation of foreign currency against the Indian rupee, which impacted our hedges

our current capacity is 5500 sewing machines, and we are currently utilizing 68%. Due to the consolidation of small rented factories, we are expecting the utilization to be better going forward.

Retail Division

the retail division did not get shareholder’s approval during March 2020.

total revenue for this quarter stood at Rs 12.7 crore as against the sale of 20.7 crores year on year.

This decrease is mainly due to the COVID crisis

EBITDA was at -3.9% as against -9% last year

SPUK

quarter ended: GDP 1.26 million as against last year’s performance GDP 0.96 million in revenue

margins were at 3.5% as against the negative margin of 1.6% year on year

Even though SPUK grew by 31.5%, orders worth GDP 0.7 million were not executed due to the pandemic crisis

General outlook:

the current order book for fiscal and restoration of the business for .P.S.P. Apparels garment division it’s clear evidence that we are in the niche segment of babies and kids. Most of our customers with online business and the supermarket businesses have grown by 50 to 100% under this segment we cater to. The customer’s spending pattern gives priority to spend on the product which we cater to, and the current prices that the company s have been able to raise through this process only because of the strong fundamentals.

There are opportunities opening due to China’s situation, which we are real to make use of

Vietnam is a challenge. So, they have gone into FTA. Vietnam is again like China big volumes and more of the millions of the unit orders and where in India the order size and the sizes are completely different from what Vietnam is doing. it is too early to comment on anything on the Vietnam one, but we are getting prepared for the competition. we faced Bangladesh and Sri Lanka, we will face Vietnam also.

Operations

all the factories are operating at around 60% capacity

our utilization is 3300 sewing machines as against between 3600 to 3700 machines pre-COVID scenario

reduction of working days to the extent of 30% to all staff and all employees, including the senior management till September 2020

Small rented factories are in the process of consolidation with big factories, which will reduce the operating overheads going forward considerably

retail stores are closed. March onwards we have spoken to the landlords that we are not passing on the rents during the closedown period and also with the malls where we are closed, we are not paying any rent

Order Book

current order book is at rupees 210 crores

Financials

MEIS withdrawal

total percentage of sales which we get as an incentive - 7.25%. Earlier it was 11.25%

we are trying to make up to the same 17-18% EBITDA, despite the loss of MEIS of 4%.

we are working on so many touchpoints for cost-saving. There are about 5-6 touch points where we can easily save another about 4% to 5% hopefully

we have re-modeled all the factories to a lean production which will definitely improve the efficiency. Our efficiency is going to be better by 5% which will again save another 1% or 2%

machine utilization used to be 80% or 85%, now we are expecting by the end of this financial year we will be raising to around 87% to 90%. By targeting the overheads of the factories, costs will be drastically reduced.

reducing cotton prices

there is no relation with the garment division margin and the cotton prices. How do we work here is that we go by current yarn prices, and not the cotton prices.

will definitely help a little bit in the margin of the yarn and but then it comes to the garment it’s very little

COVID impact

garment division: despite the uncertainty, lockdown, and supply chain disruptions, the company did not witness any significant order cancellation from the garment division export customers

witnessing significant recovery in the order inflow from the customers since May 2020

We are expecting the migrant employees to return in another five to six weeks’ time

Forward Looking Statements

with regards to like H1 it’s not like we are in a state where we are like losing money, and so effectively we will still be slightly profitable, but by Q3-Q4 we expect to be normalized and also have an ability to utilize our enhanced Capex which we have done and executed.

Any idea what can be a moat in this business. The stock is very cheap today- so got interested. However, cant gauge how well or worse is it positioned vis-a-vis a competitor from Bangladesh, Pakistan or Vietnam?

Interesting thing is however, that their garment exports have grown every year (although less than 10%)- this means somewhere business is flourising and competitiveness is there but hard to gauge.

Export incentives at 6% now (Earlier 11%). IF this goes away too (although unlikely in my view), there can be risks to margins. EU has FTA with Bangladesh and Pak and for India it attracts duty.

If it is able to hit a run-rate of Rs250 cr from Sep FY22 quarter (as they guide), PAT could be Rs80-90cr. Hence i got interested in stock, but evaluating further

Haven;t seen anything posted for almost 3years.

I have been recently studying this company and got interested due to the cheaper valuations available in this market.

My major concern is around promoters’ intent. Would seek the guidance of people tracking this company for long time.

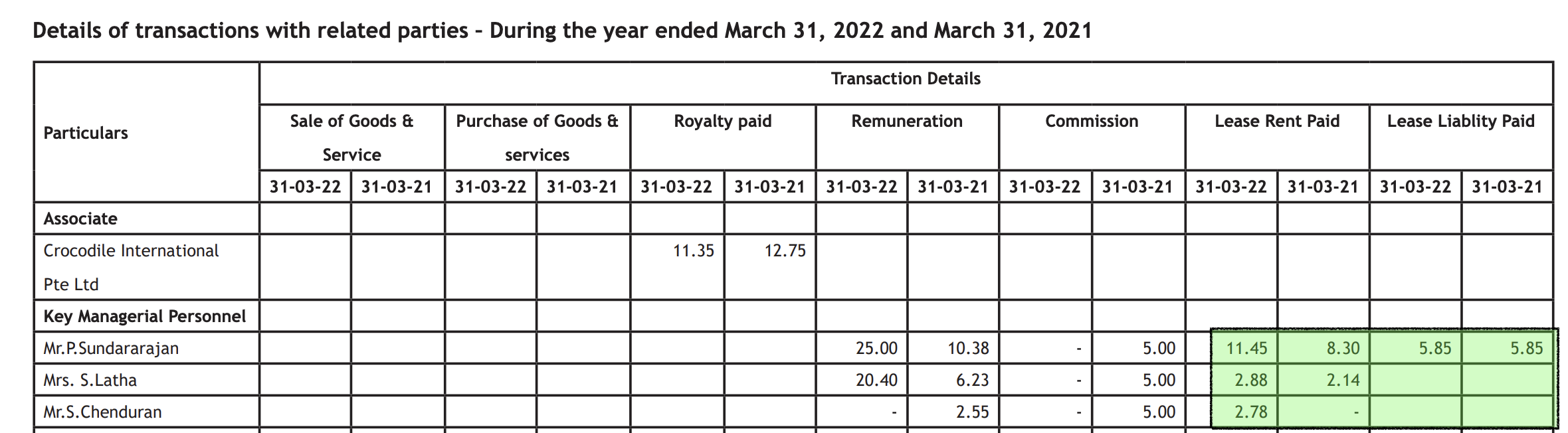

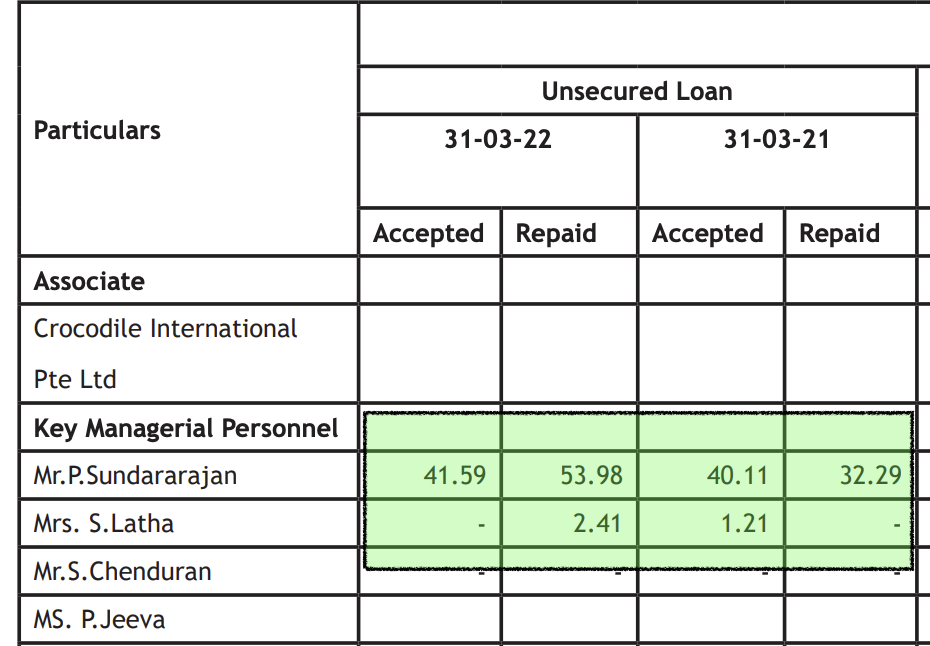

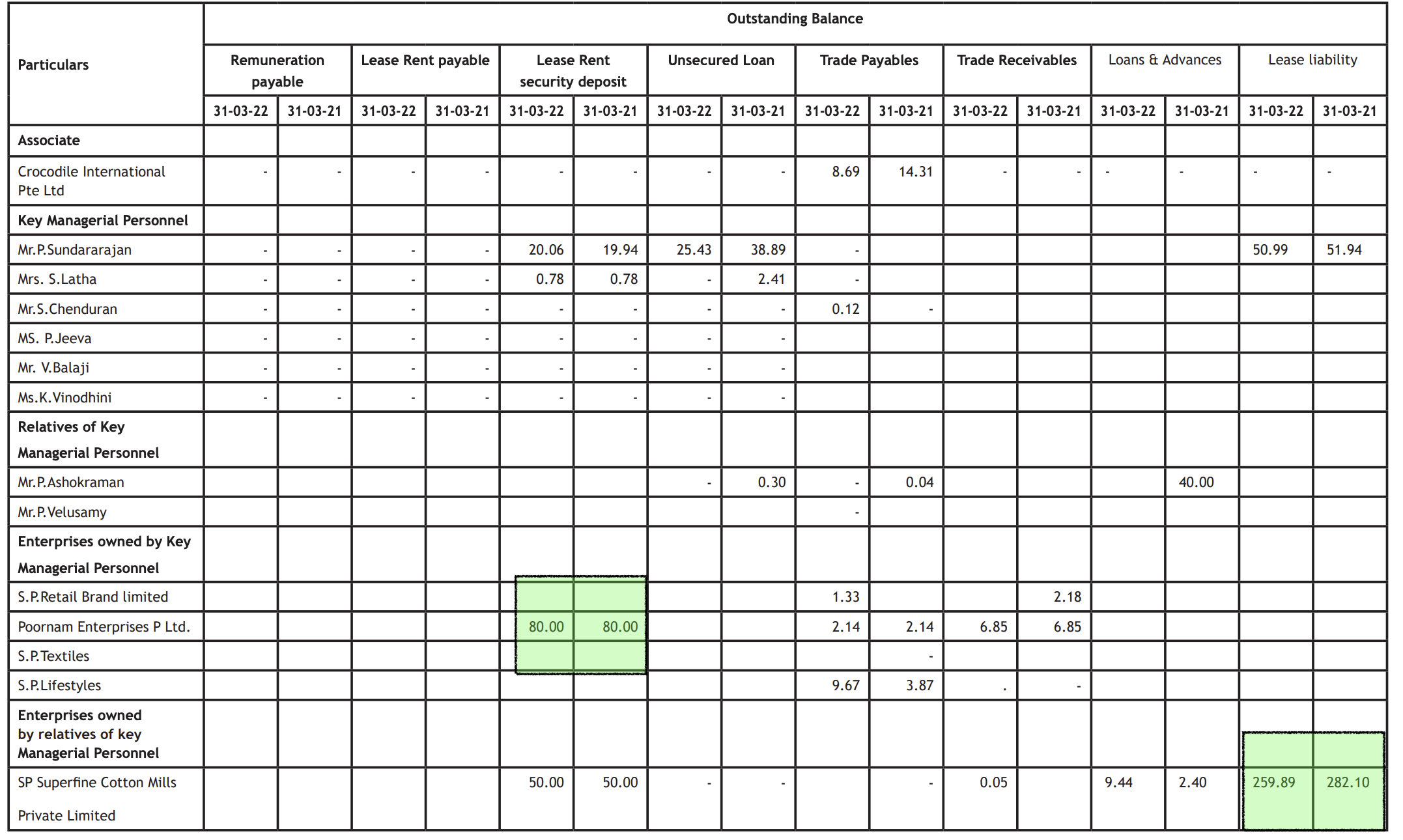

I was going through the related party transaction page of FY22 Annual report and had below doubt (Page 199)

What does Lease Rent Paid mean? Does this mean company is paying rent to Promoter ?

My board-level understanding is that whenever company pays rent, loans etc to promoter /other subsidiary company, it looks like the promoter is trying to make money for themselves harming the interest of minority shareholder.

Please let me know if I completely misunderstood above points

Hi. There are many textile players available cheap There is no moat around Sp Apparels. Promoters dont seem to have the vision for growth and expansion. You can look at gokaldas exports which is a fast growing and expanding textile global player.