Hey I do not understand sector much, so could you please shed some light on which companies will benefit the most? Is it negative for southwest?

ONGC’s global tender worth up to $20 billion to hire deepwater drilling rigs is neutral for Southwest Pinnacle.

But sentimentally it is positive for the company as this move reflects India’s committment to exploit domestic natural resources, of which SWPE is a benificiary.

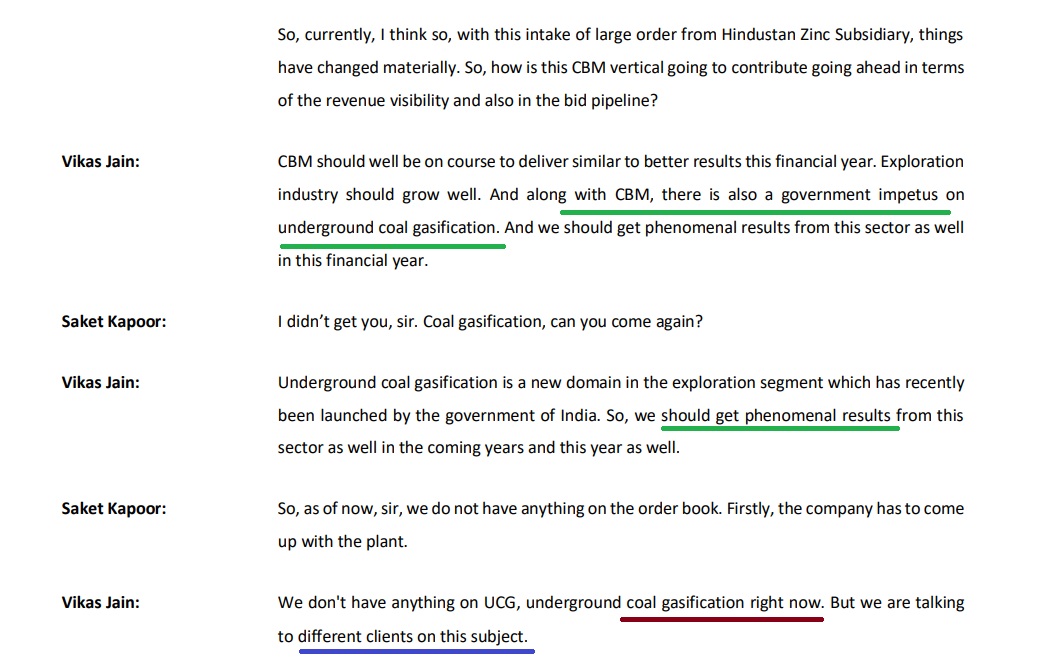

As the Govt. has recently announced the huge plan for Coal Gasification, my understanding is that this company might be a direct or indirect beneficiary of this. Does anyone have any view regarding this?

In last Concall, management explicitly mentioned UCG (Underground Coal Gasification) opportunity. They also clarified, it’s still in discussion phase rather than concrete orders.

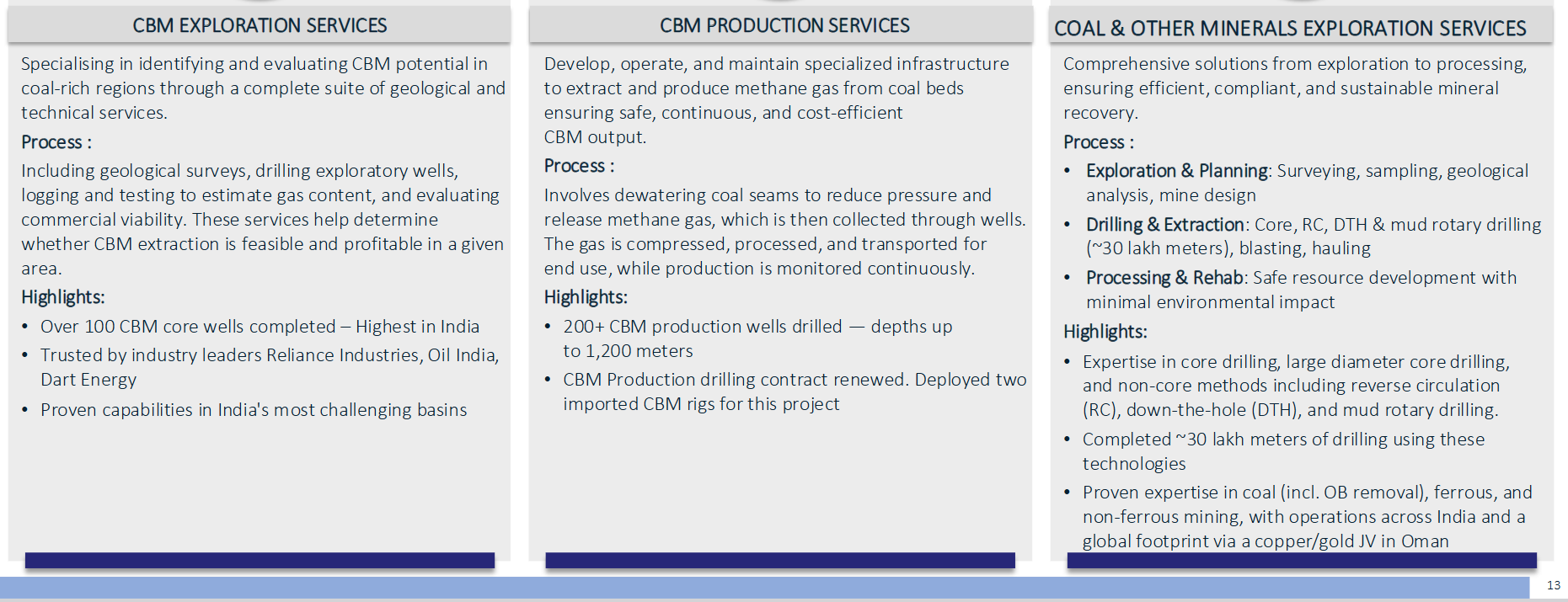

If UCG do get tailwind (very likely due to Govt push on overall coal gasification, and especially because it’s highly advantageous over surface coal gasification), SWPE do have an advantage due to their expertise in CBM (Coal Bed Methane) process. They are running a large CBM contract with reliance.

CBM and UCG technologies are sequential. Operators will first extract the easily accessible Coal Bed Methane from a seam. Once the methane is depleted, they may use Underground Coal Gasification on the remaining solid coal to extract its residual energy.

Right now, I think SWPE will be in the leading position among contractors who can quickly get in to UCG.

Discl: Not invested. Tracking SWPE and peer Asian Energy in the O&G + Mineral exploration space

I have done a detailed deep dive on the business (but very lazy to write in detail). To me it seems mispriced (correct me if wrong). Some key points I am writing here:

-

They have 5 rigs in pipeline four of which will be delivered in 3-6 months (from concall).

-

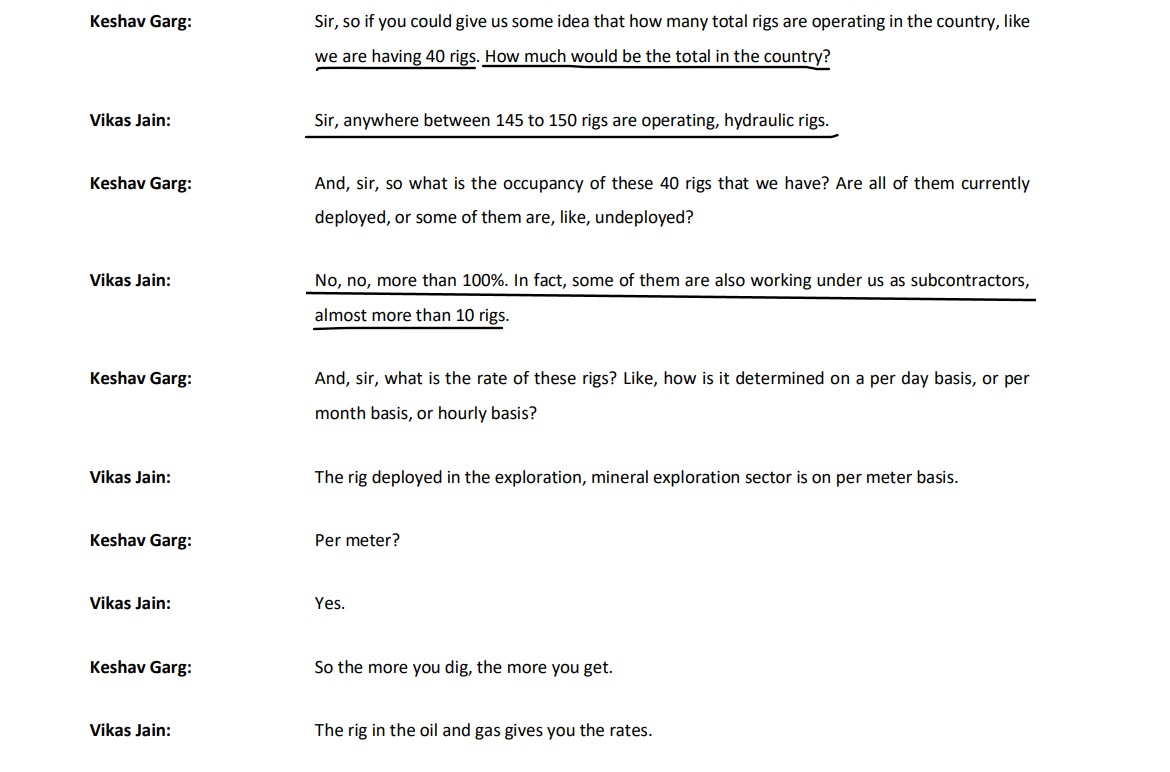

All there rigs are fully deployed. The demand is so high that they have to hire or subcontract extra 10 rigs for deployment.

-

The rigs, once fully depreciate, directly adds revenue to bottomline (operating leverage). One of the reasons they have extraordinary growth in PAT in FY26.

-

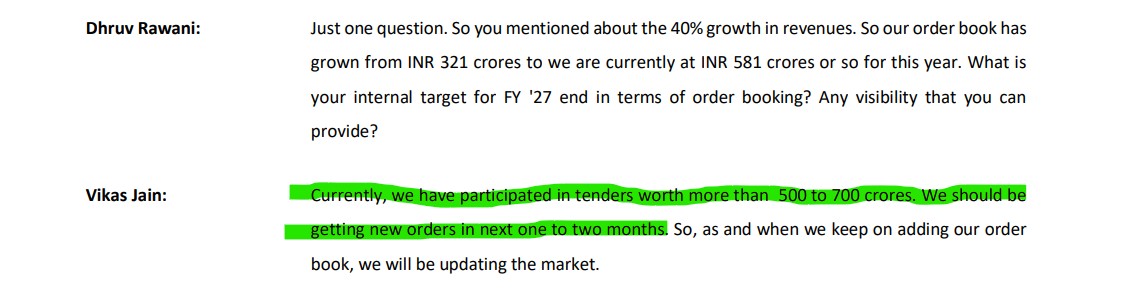

Current orderbook: 581 Cr (2.4x of FY 26 revenue).

Right now market is valuing it on the basis of exploration business which is clearly in upcycle.

What the market might not be pricing in:

-

They own Jogeshwar & Khas Jogeshwar coal block in Jharkhand. This acc to management should start commercial production from FY28. Peak revenue potential: 300-400cr (EBITDA MARGIN: more than 40%).

-

The two JVs in oman can also contribute meaningfully but not in immediate future.

-

The management have guided for 15-20% growth till FY30 in one interview only for exploration business. They are doing more at this point of upcycle. With operating leverage PAT growth can be even more.

Antithesis:

-

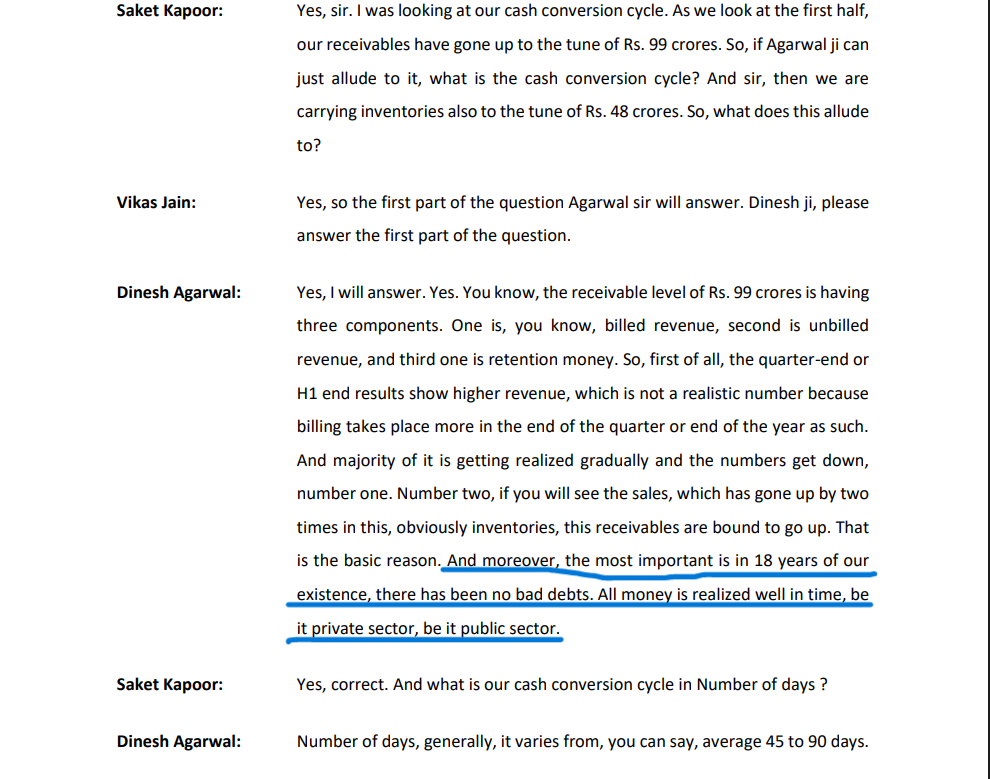

High debtor days (catering to Govt Clients). However, management focussing more on orders from private players now: like recent big order from Hindustan Zinc). Key monitorable.

-

Receivable growth more than revenue growth.

Thats all from lazy me.

Any addition/discussion would be appreciated.

Disc: Biased, Invested. New to equity market, non-finance guy.

Thanks for the summary. To build on your key points, below were mentioned in the latest conference call:

Company has participated in tenders worth 500 to 700 crores.

SWPE’s current market share for hydraulic rigs is 30%

Disclosure: Invested

Thanks. Do you see any scope of valuation re-rating if orders from private client increases??

In my opinion valuation re-rating were to take place in any business, depends on revenue growth and quality of earnings growth. In this case it would be the same. As private or public clients should not be a concern as long as they recover their dues.

Management in their earlier con call was confident and mentioned this:

Yes. On the revenue front management has a track record of underpromise and over-delivering. I think if management can get a order regarding Coal Gasification, this can be the trigger.

Important devlopment:

updates.pdf (309.6 KB)

Yeah but many companies have been selected for the same.