South West Pinnacle Exploration

BSE CODE - 543986, NSE - SOUTHWEST

CMP - 115

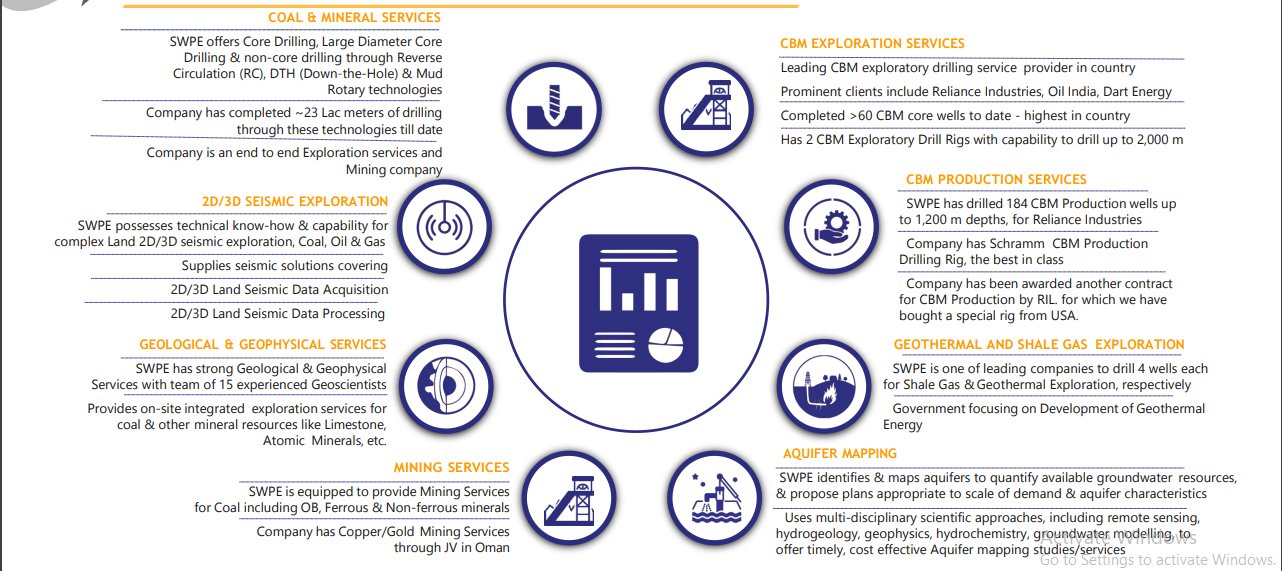

Company is present across various domains of drilling & exploration like Coal and Mineral drilling services, 2D/3D Seismic exploration, Aquifer Mapping etc. This segment is expected to grow at 15% with EBITDA margins in the range of 20-22%.

Some details about all the segments company is present into.

Company entered into a JV with renowned Australian exploration & mining company, Alara resources in 2018. Company was awarded $125 Mn. Copper mining Contract for 11 years in February 2022.

The company looking for their next phase of growth had bid for 3 coal block and amongst them won a coal block for commercial coal mining in the state of Jharkhand. The estimated Geo reserves of this block is 84MT. Company plans the start coal production by FY26-27 with a capex of 240 crs. According to the management the coal block alone could generate 700-800 crs. of revenue from Fy 27-29.

Risks -

The coal block alloted to the company is supposed to be at the place where they live. The management said that will help them as they know the area in and out. But coal is a risky business in India.

There is Govt. approvals required in every stage so this can be a hurdle as well. Many a times there have been huge delays because of approvals.

Disclosure - Holding the company so my views could be biased. I am not a SEBI registered analyst. Please consult your financial advisor before investing.

The company is present in the entire value chain of exploration and drilling services. It undertakes drilling and exploration of coal, minerals and coal-bed methane. The company has expanded into aquifer(water) mapping programmes for state and central government agencies besides 3D and 2D seismic data acquisition and processing for renowned oil and gas companies in India. It also provides consultancy for geological field services, mobile field services and other allied services. The company has 41 operational rigs with capacity to drill between 300 and 2500 meters.

The company has won orders from Reliance Industries for CBM, has entered into a JV in Onam for copper mining and has won a coal block in Jharkhand. This makes the company a full fledged exploration and mining company.

Exploration Services

As detailed above the company provides a host of traditional services which include the coal and mineral drilling services, 2D/3D seismic exploration of minerals and Oil & Gas both onshore and offshore. The company also provides geological and geophysical services.

It is the leading CBM exploration and production provider and has won an order from RIL and Oil India. it has 2CBM drill rigs for now which are capable to drill upto 2000m.

The company is also present in unexplored energy industries like geothermal and shale gas exploration service

The company earns an EBIDTA of 20-22% in these services and a growth of 20%.

Order book position as of March 24 is 221cr. CBM Reliance Project.

In FY 23-24 the company won a production project from Reliance for Rs. 84cr. The company expects that it is possible that the size of the project can increase to 270cr. Onam Project

In the year 23-24 the company has won a copper mining project of Rs. 1,050 cr. The company has a 30% share in the JV. The entire contract is outsourced and it expects to provide a steady PAT of 2-3 crore every year.

The company has created a Saudi Arabia subsidiary under this JV to carry out similar mining services out there.

The company expects further orders for the JV in the coming years due to diversification of revenues implemented by Oman. Jharkhand Coal Mine

Company won the Jharkhand coal mine which has potential reserves of 84 MT. in 2021.

The company expects to start the production of mine in FY 26.

The company would have to incur a capex of 240cr for this project. Out of this Rs. 72cr approx. is payable as upfront fee which shall be adjusted against future payments to Government by way of Royalty and revenue share. Hence the effective capex comes to Rs. 168cr .

The company expects to generate a revenue of Rs. 700-800cr from FY27-29. On the above revenue it expects to generate a EBIDTA of 40-42%. Financials

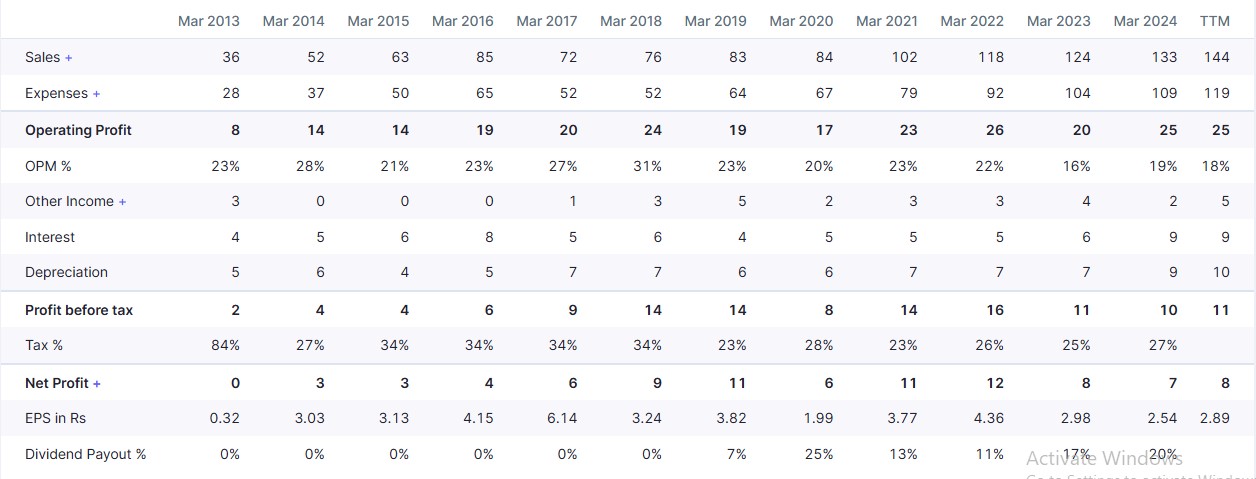

For FY 24 the company earned a revenue 133 cr with a EBDITA Margin of 18% amounting to 27cr and PAT Margin of 5% amounting to 8.3cr.

In Q1 FY 25 the company earned a revenue of 30cr, EBDITA of 7cr and PAT of 2cr.

It is trading at a TTM PE of 40, EV/EBIDTA of 15 and Mcap/Sales of 2.7

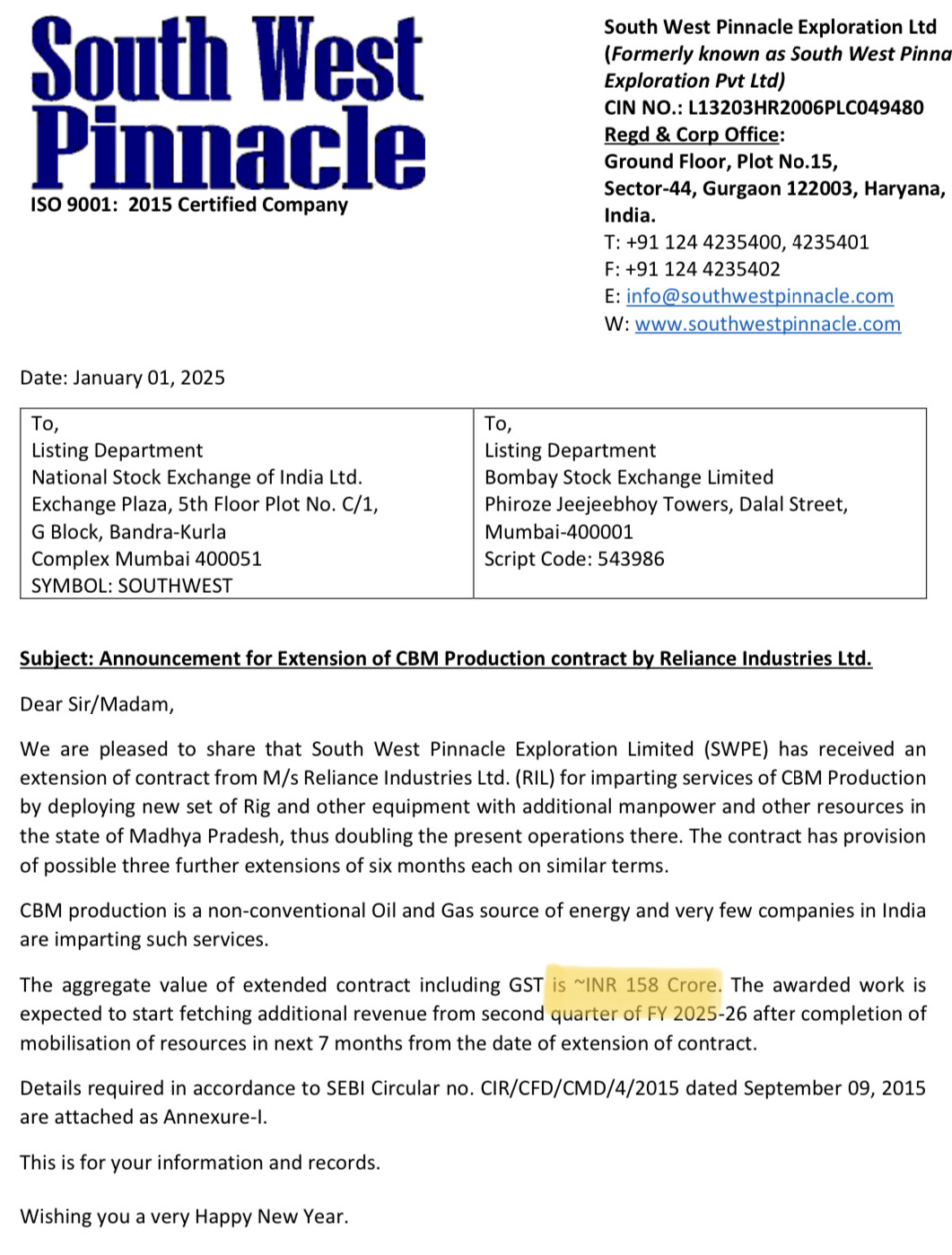

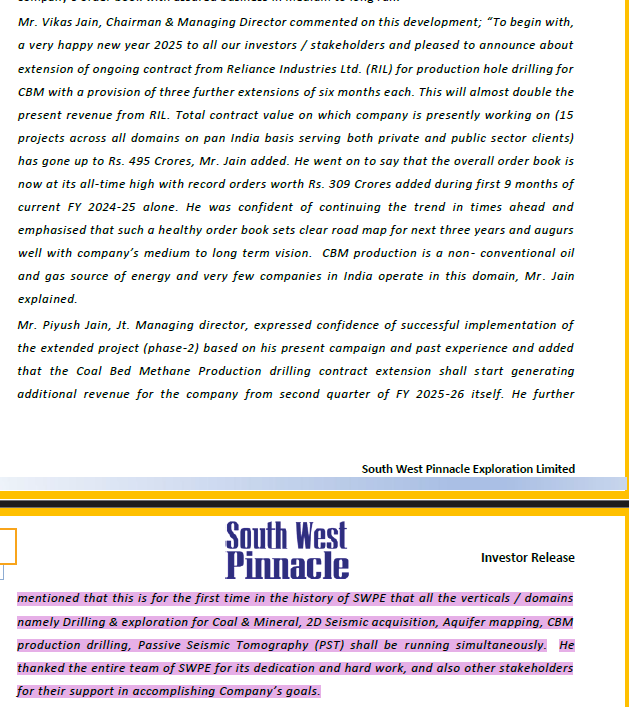

South West Pinnacle Exploration Ltd. (SWPE) announced a contract extension with Reliance Industries Ltd. (RIL)

➤ 𝘙𝘦𝘷𝘦𝘯𝘶𝘦 𝘐𝘯𝘤𝘳𝘦𝘢𝘴𝘦: The ~INR 158 Crore contract is expected to generate additional revenue starting in the second quarter of FY 2025-26.

➤ 𝘗𝘰𝘵𝘦𝘯𝘵𝘪𝘢𝘭 𝘍𝘶𝘳𝘵𝘩𝘦𝘳 𝘌𝘹𝘵𝘦𝘯𝘴𝘪𝘰𝘯𝘴: The contract includes provisions for three additional six-month extensions.

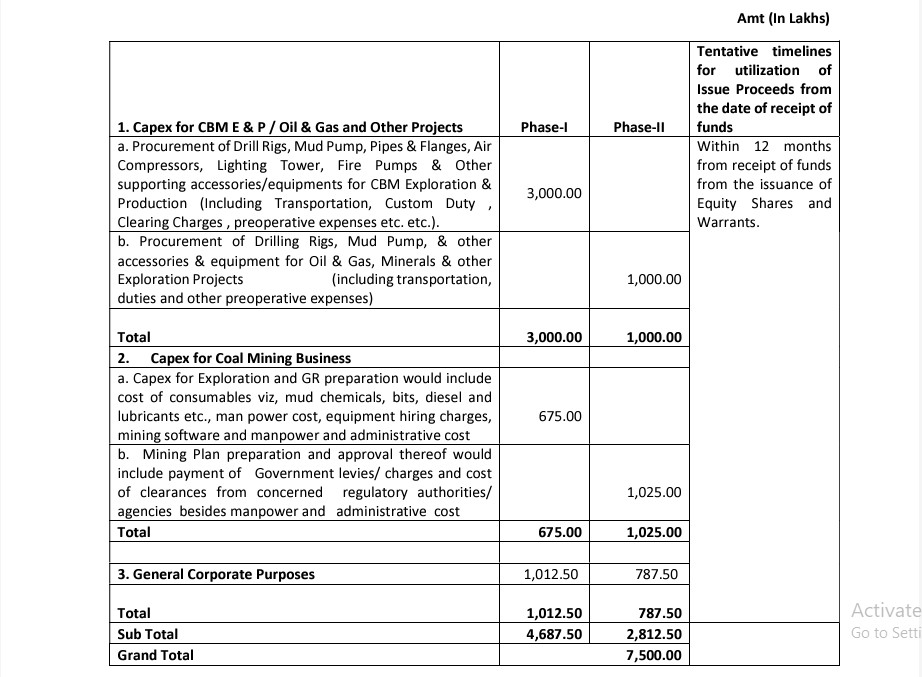

Can you help me in understanding the capex plan?

Current debt is 84 cr. Raising 75 cr through preferential.

Mining requires 168 crore capex. As per 75 crore share issuance intimation, they have allocated only 17 crore for mining capex.

So does that mean rest will come through debt ? Because I do not see they can raise rest of the amount again from preferential or QIP route.

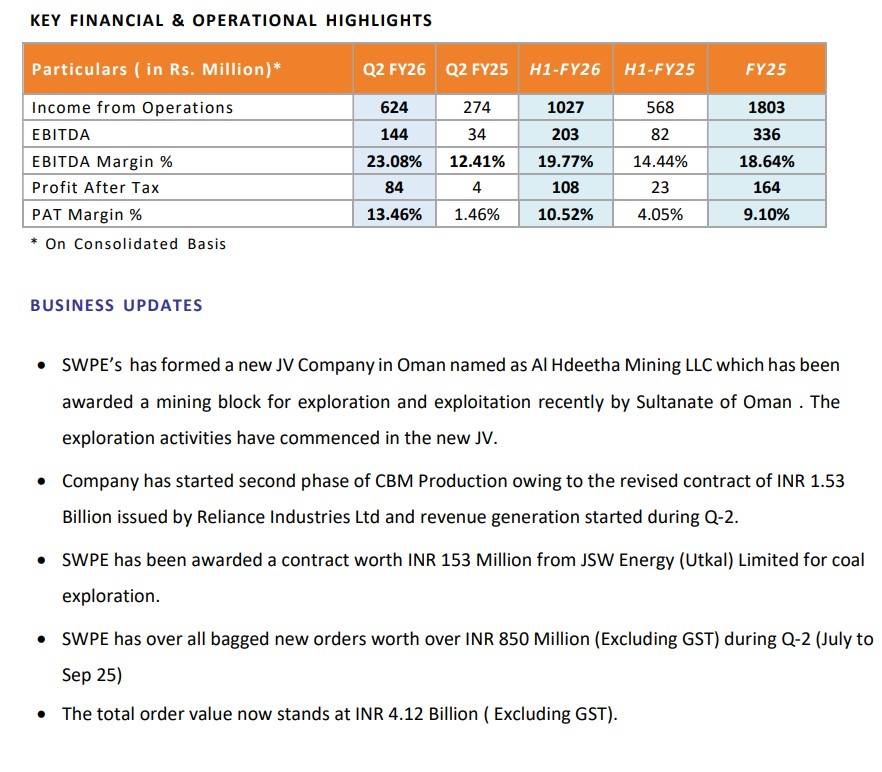

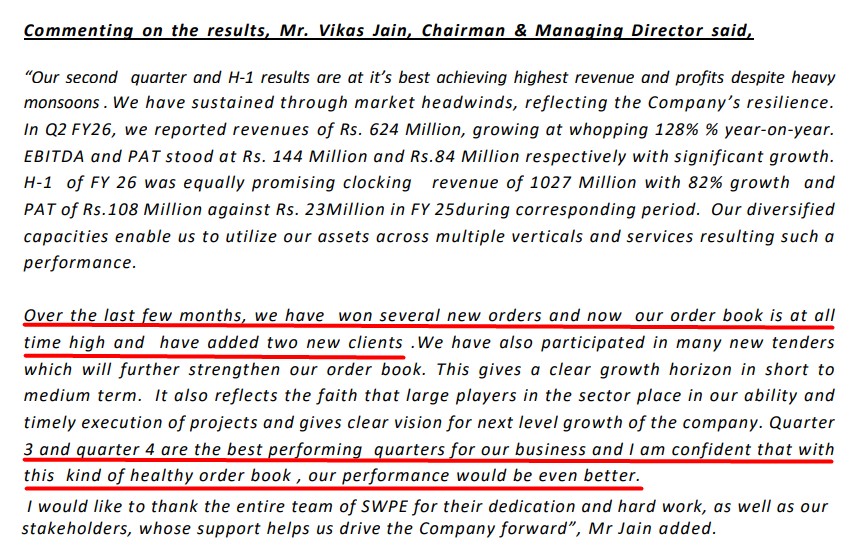

#SouthWestPinnacle exploration Q2 con-call updates

-H2 has historically been better then H1. So expecting good amount of revenues to come in H2. With higher revenue operating leverage will also play out.

-Order book as of now is around 410 crs. with an execution timeline of around 1-2 years. This gives good visibility for the short term.

-Bidding pipeline is also substantial as per the management.

-Coal mining operations in the Jharkhand mine is expected to start and contribute fully by FY28. Mining operations will have 40%+ margins and can alone throw free cash flows of around 100 crs.

Company came on my radar after bumper Q2 results and recently did a first ever concall to discuss the business and results. Sharing a few notes after going through results and concall transcript :

Company is showing rapid growth - Q2 revenue is +128% YoY and +55% QoQ. In fact, earnings momentum has picked up from Q4FY25. Company started booking revenue for 150 crores CBM project for RIL this quarter.

Growth is profitable too - Operating Margins in 2 quarters out of last 5 are 20%+ and Net margin has improved from 1% in Q2FY25 to 13% in Q2FY26.

Order book of 412 crores is at all time high with 136 crores in CBM orders and 88 crores in Aquifer mapping orders. These 2 segments have become major revenue drivers for the company since FY24. One more upcoming opportunity is Jharkhand coal mining block which has a revenue potential of 300-400 crores starting from FY28.

Combination of high growth, higher margins, and improving asset turnover ratios (especially Fixed asset turnover ratio) has resulted in improved RoCE and RoE over the last couple of years. Leverage remains low consistently. I think they are going for internal accruals and QIP route than taking on debt to fund their financing needs.

Cash conversion is good since the company hasn’t invested a lot in working/fixed capital to grow revenues. 75-80% CFO/EBITDA ratio over the last 2 FYs.

Valuations for a company this size & in a cyclical/commoditized sector are on the higher side - 23x TTM earnings, 3x P/B, 4x EV/EBITDA.

Technically, chart is showing strength on higher time frame with a break out from 1+ year range high of INR 150.

One thing which put me off - Mgmt. has shared unrealistic revenue guidance of 15-20% revenue growth in FY26 which means they don’t really have a guidance. I am calling this guidance unrealistic because by their own admission, H2 is stronger than H1 and in H1 they have already done 102 crores which is 81% growth vs H1 FY25. No guidance is better than sharing unrealistic guidance in my opinion.

Can someone from the industry shed some light on whether these tailwinds are industry wide or company specific or how sustainable are these?

Disc. : Invested with a tracking position. Studying further. Please do your own research. Above is not an investment recommendation.

Thanks for this post. I too was looking at the company and have a couple of questions. It appears from the segmental results that with effect from FY26, the company has exited the coal trading business. However, I found no explicit mention of this in the investor presentation or the analyst call. Meanwhile, there is a sudden & disproportionate increase in Other Operating Expense in FY26. What is the reason for this, and are these two points related? Is there any reclassification of expenses in FY26? Please share if you have any insight on this.

A third concern I have is that neither Piyush Jain nor Vikas Jain have technical qualifications i.e. degrees in something like geology, mining engineering or metallurgy. I do get they will have qualified employees on payroll but in small companies like these, you need the promoter to be hands on with the core business himself.

The company has announced that they have been notified as accredited prospecting agency for carrying out prospecting operations for the exploration of coal and Lignite. They will now be able to commence exploration, GR preparation / approval and mining plan preparation / approval etc. for early exploration and development of coal block. The company Press Release is self-congratulatory with terms such as “…very positive and bold step…landmark development…game changer…” blah blah blah.

However, it appears that the company was already a QCI-NABET approved APA at least as far back as 2022, with a certificate valid till 2025 . The FY2023 Annual Report says “SWPEL has also received Certificate of Accreditation from National Accreditation Board for Education and Training (NABET), Quality Council of India for Preparation of Comprehensive Geological Report (APA). It is a very prestigious accreditation giving the Company an edge over competitors in this domain.”

The above image is from the FY2023 Annual Report. But the FY2024 & 2025 Annual Report quietly changes the language to “had” received Certification of…

QCI – NABET certification is typically valid for a duration of 3 years, so they seem to have lost the 2022 certification a year later, during the Annual Review. There is no mention of this in the Press Release and makes it appear as a new development.

Not exactly a landmark development but just a matter of relief, may be.