A must listen Q2 FY 23 CONCALL . Bank seems to be in safe hand of new MD. Views invited on SIBank prospects from kerala or south india n others who are tracking it for long.

invested tracking qtyl

A must listen Q2 FY 23 CONCALL . Bank seems to be in safe hand of new MD. Views invited on SIBank prospects from kerala or south india n others who are tracking it for long.

invested tracking qtyl

First question answered by management speaks a lot . SIB is majorly concentrated in Kerala and in last couple of years state is witnessing heavy rains and floods and retail and sme hit by it. So in order to grow business they are looking into corporate loans and thats the same mistake they done in past. In terms of banking kerala is already a mature market and u can see number of psu and private banks, co-operative banks( they are getting big pie of deposits as their interest rates are higher) along with gold nbfc like muthoot, manapurram and number of small players like ICL, koshamattam and others even in a tier 3 city. Federal Bank , CSB all got the same concentration risk in Kerala and i think federal Bank did better in moving out to other Southern states. I have not studied thoroughly the breakup kerala and non kerala business for SIB. IMO we need to be cautious and watch their corporate loans closely.

Looks like SIB is having great leadership at the helm… getting more confident that they will walk the talk this time around…

Asset Quality & banking reach only in 4 states … however things seem to be turning around for them under their new MD

Kerala-based South Indian Bank (SIB) has posted a net profit of Rs 223 crore during the second quarter of the current financial year, as against a net loss of Rs 187 crore during the July to September quarter of 2021-22.

The bank’s total income for the quarter under review increased by 11 per cent to Rs 1,995 crore as compared to Rs 1,804 crore during the same period last year. Murali Ramakrishnan, managing director and chief executive officer of the Bank, while announcing the results, stated that the strategy of realigning the business by the bank had contributed to the above improved performance.

“During this period, Bank could register growth in the desired segments of liabilities like CASA and retail deposits and focus on building quality asset portfolio across all verticals like corporate, SME, auto loan, credit card, personal loan, gold loan,” he added. The bank’s CASA was up by 14 per cent during the period under review. SIB’s gross non-performing assets for the quarter decreased to 5.67 per cent of gross advances as compared to 6.65 per cent during the Q2 of 2021-22. The bank’s net NPA also declined to 2.51 per cent as against 3.85 per cent during the same quarter last year.

He also stated that, in line with the strategic intent of the bank viz, “Profitability through quality credit growth”, the Bank could churn around 50 per cent of its advances portfolio since October 2020 amounting to Rs. 33,768 crore with a NIM of 3.6 per cent and GNPA of only 0.03 per cent. This coupled with a robust recovery or collection mechanism, had helped the Bank to reduce the fresh slippages by 34.09 per cent on Y-o-Y basis from Rs 531.31 Crore to Rs 350.17 Crore, he added. Provisions for bad loans and contingencies declined to Rs 179 crore during the quarter as against Rs 420 crore reserved for the year-ago period.

I was going through the Q1FY23 concall transcript. Looks like he is under-promise and over deliver type of person ![]()

In Q1 FY’23 concall, the MD had given a guidance of 1000 crore slippages for the entire year, wheras after Q2 results and in media interactions he has mentioned the figure of 1600 crores. Can anybody throw some light on this? Attached snippet of Q1 FY’23 Concall.

Where can i find this updated data? Please tell me i want to compare banks with improving digital side.

Follow the company on screener.in .The filings to the exchanges will be updated.

Interesting to see Prem Watsa’s affinity for Indian banks ! ![]()

Very moderate deposit and advanse q-o-q growth… High growth in corporate book when the rest are following retail…

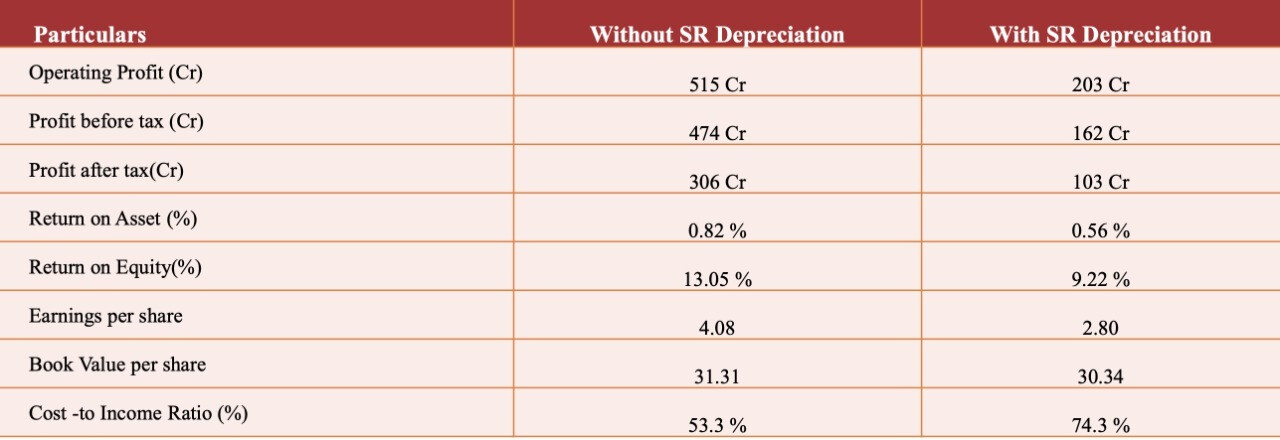

If the SR depreciation was not there the bank would have reported its life time high Quarterly profit !

More on Sr:-

What are Security Receipts or SRs?

When a bank sells stressed assets to ARC, the ARC pays 15% of the asset value upfront and issues 85% worth of SRs which get recorded in a bank’s B/S as Security Receipt assets. At the time of recovery of assets by the ARC, the bank gets its 85% after deducting its fees etc. While the SRs sit on a bank’s B/S, their value may decrease if the ARC company declares that the asset’s NAV has decreased. So banks have to maintain provisions against SRs.

Before 2017 the provisioning is based on NAV declared by credit ratings, so if the SR is of Rs. 100 and the NAV by an independent credit rating agency is Rs. 80, banks need to create provision of Rs. 20 in the books.

In 2017 RBI came out with new guidelines wherein the banks need to create provision as higher of based on ageing analysis or the difference between SR and NAV declared by credit rating agencies and on the basis of ageing rules so for example if SR is Rs. 100 and NAV by rating agency is Rs. 80 and as per old method it needs to create provision of Rs. 20 but if as per the RBI ageing analysis the provision is Rs. 30 so they need to create a provision as higher of both i.e, Rs. 30.

The bank is following this approach on all the SR issued after 2017 but there was some SR issue before 2017 as well like in 2014, 2015 & 2016. There was no clarity on that weather to create provision on that as well or not.

On 05 Dec 2022 RBI issued an FAQ wherein they mentioned that banks need to crate provisions on retrospective basis i.e, if SR are issued before 2017 then they need to create additional provision on that as well.

In South Indian Bank they had the SR issued prior of 2017 as well so now in Q3 they created the one-time additional provision of 312cr. Wherein they have created 100% provisions on all the SR issued before 2017. As on Dec-22 the outstanding SR in the books are of Rs. 215 cr.

Now if we assume there will be no any collection from these 215 cr as well then the bank will need to create a provision of Rs. 48cr in Q4-FY23 and Rs. 15 cr in FY24.

Disc:- invested.

Heared in concall. CMD is confident and NIM of 3.5 is guided for FY 24. SR provisioning(one off) would be there for Q4. Satisfied path which is observed in concall.

Disc: Invested

South Indian Bank conference call was a delight to listen to.

Some takeaways from Q2 and Q3 Conference call.

The thing I like about the current MD and CEO is that he is like a horse that runs with blinders, focused on finishing race on his own terms and not wavering with temptations like high NIMs or high growth or trying to play the game they are not capable of at the moment, along with the excellent executation capablity shown after he joined the bank.

Invested and biased having highest allocation on this stock taken recently.

Are there any book value estimates which you are running on?