Rupesh,

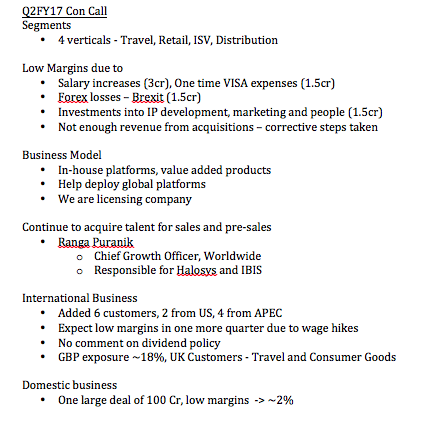

It is not always about ‘ease of doing the business’.TCS,Infy,etc. are massive in size,and the CPG/Travel opportunities may not be big enough for them to address.Those companies may like to focus on bigger market opportunities like Digital,AI,etc.Let’s say the market size of CPG/Travel solutions,is north of 3BUSD.Thus,for a company of TCS’ size,this is not such a great figure…and they won’t like to pursue it with much attention,until and unless,its a part of their ‘legacy offerings’.On the other hand,SMAC & Digital,are touted to be 1 trillion dollar opportunities.Doesn’t it make sense to go after these for TCS,etc.? This lack of attention can create a vaccuum at the services level,which is filled by smaller companies.Moreover,for IT firms,customer loyalty is very siginificant.Thus,if Sonata has been offering Microsoft some services since 15 years,then there is little chance that one fine day,Microsoft would replace them for no reason.

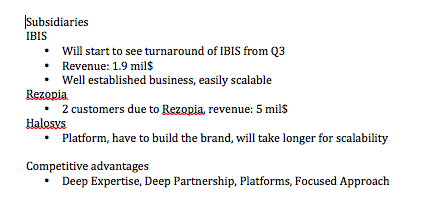

Sonata recently acquired a company called Rezopia,which should help them consolidate their position in the Travel vertical.Moreover,the company is also trying to address the SMAC opportunity through its offerings. https://www.youtube.com/watch?v=4TKSqpe1Uqo

The balance sheet is very strong,and the company has been generating FCF of 85-90cr. in the last two fiscals.Revenue growth has also been decent.Payouts are very high and valuations aren’t demanding.My concern is,about the ‘high base effect’.Sonata’s margins in the Exports offerings are extraordinarily high and might be difficult to sustain(for the record,the company has been conservative in guidance from the last 7-8 quarters) Thus,if revenue growth doesn’t exceed 15-20%,the bottomline may suffer.The good news comes from their cash cow business: Domestic products division,which requires 0 capex & is running on very low(,though improving) margins.This can provide cushion to its earnings in the coming years,even if margin expansion in the exports division is hard to come by.

With a cash pile of ~200cr.,the EV comes out to be 1300 crore.With an annual profit of 135cr.,we are paying just about 10x earnings.Dividend yield too,is very healthy.Remember also,that Sonata is able to generate RoEs & RoCEs,in excess of 30%.

The recent sentiment around IT sector has been very poor,and companies have started to report decent earnings.The best time to buy a sector is always when things are looking gloomy.I see no reason why Sonata is not a ‘good stock’ to own.

Would be great to have some counter views.

Disc.: Invested.

.

.