In addition to related parties transactions, I always look at quantum and nature of contingent liabilites. I had not analyzed Sonata so far, but impressed by details on this thread, I was going to take this up for analysis… Pushed it little down with this contingency issue. Thanks Ashish.

Sonata has received favourable orders from SC in it’s case but IT deptt has gone for appeal in some. As per last concall transcript co is expecting a refund of 20 Cr from IT deptt n they have been receiving some refunds regularly over las t few qtrs.

Under new management we have to focus on future best exemplified by presence of classy new HNI quality investors in Sonata.

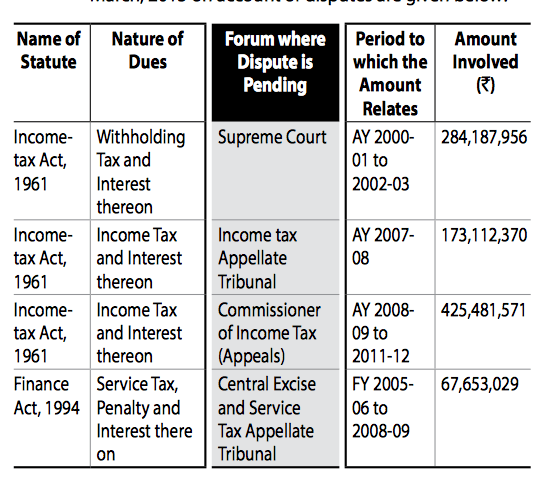

Thanks Rajul. Actually one of my friends runs a business. He told me that Arun Jaitely’s “tax terrorism” is very prevalent in India, different authorities come up with different tax and poor business men have to run from pillar to post to clarify to tax departments. Many times these disputes come from the letters signed by IRS/IAS who should have known that the tax they r demanding for a prticular purpose shouldn’t have been aplied. Recent case of tax authorities’ demand for 1000 crores tax dispute with flipkart may be an example. But till the case resolves, we can be an observer. The thing which unnerved me was Y-O-Y increase in quantum of tax disputes, 250 crores is not a joke, that too is increasing.

Agree with you 100%. I just wanted to share what i found so that we can take informed decision. My search for some contacts in Sonata is still going on, company wont talk to me if i go just like that. If somebody can help me in this area, please deop me a mail.

not that whole investment case goes for a toss. but attractiveness reduces a little.

i am beginning to look into Sasken as well where risk-return looks good.it’s mainly a bet on Anjan Lahiri who has joined Sasken form Mindtree, and team that he has built so far. also, management is shareholder-friendly. am exploring if MPS-kind of turnaround is possible in Sasken, or not.

If u don’t know, there is a thread on sasken on valuepickr and it was started by me only

Yes, its a bet on Anjan Lahiri but right now its a play for cash utilization, 280 crores of cash right now, no debt. They r good in distributing cash to shareholders, lets see.

Sonata declared a fantastic set of numbers in its Q2 results. H1 EPS is Rs 6 and one can expect at least Rs 13.5 EPS for FY15. It has already paid out dividend of Rs 2.75 for H1FY15. There is a stated strategy of keeping the payout high.

Management is executing very well on its articulated strategy offocusing on our strategic accounts; a veryfocused go to market strategy; focused verticals and a certain specialized horizontal services;focus on getting top talent; a very structured approach to M&A and tighter processes acrossvarious account management delivery and bid management; continue to pay dividends.

I believe this can a good story from next 3-5 year perspective.

What’s causing this turnaround ? is it sustainable ? I find it difficult to understand IT mid cap stories because their leeway for growth is quite limited IMHO - they don’t get called into the # 30-$ 50 mn + deals and it’s quite crowded below that.

Can someone enlighten as to what is sonata doing differently ?

Most financials are at all-time highs at the company level.EBITDA jumped 63%,YoY,while the PAT & revenue showed good growth.Company expects the Intl. services business to clock 22-23% margins.Though,better margins may come due to Rupee depreciating against the Dollar,they will be invested to strengthen the services business.Company has generated FCF of 52cr.,in 9MFY15 & will touch 83cr.(same as FY14) by year end.Cash on books is at 211cr.Net Forex swing for the quarter was 2 crore.Billing rates have inched up helping the company clock better margins.Focus in Domestic business continues to be on profitability,PAT margin was 2% this quarter(vs. 1.6% earlier) The company wants to continue improving this.The Domestic business is a good strategic fit,and is the seed for long-term relationships with clients.Rezopia has been almost fully integrated & cross-selling benefits will start very soon.Company is seeing good traction from Australia & has added 5-6 clients.Capex will be low for next FY as well.Management is seeing good improvement in client engagements,way-to-market,etc.Aspiration/long-term goal is to be a global leader in select niches & attract the best talent.RoCE is 31%,while RoNW is 40%…expect to maintain or improve this further.Growth has been strong since the company focussed on unique seminars & presentations,enhancing its acceptance to clients.Interestingly,the company also maintains an account Dashboard,which helps them see how they fit strategically,for their client.Client concentration has reduced,in-line with co.'s expectations.Top 10 clients contribute 70% now,vs. 75% in earlier quarters.Notably,there was no de-growth for any of these,rather,the other accounts grew faster.Company remains confident about future growth.Payouts will remain healthy,even as company is constantly looking for acquisitions.

Seeing the numbers,I feel FY15 EPS should be north of 12.For Fy16,we can expect around 15.So,it is still available at 10x forward with a very good dividend yield.Mr. Reddy sounded very confident…no big promises,only delivery! Markets seem concerned about the scope for further margin expansion,as they are already quiet high.But the Domestic biz. should start contributing more to the bottomline in the coming quarters.I stay positive on the stock.

Mr. Venkatraman, CFO - Just gave a great pitch on TV, saying we’d sustain margins, and on the run-up post the interview, dumped a boatload of his shares (33% of his holdings - 30L in total) on the buying public.

“An insider is selling” is different than almost every insider is selling. I believe many of the insiders cashed in because they thought the stock was overvalued at that time. I also sold my stake around 175 after CEO sold out. Now reinvested at 137.

They are into following category of businesses - IT services (Overseas) and Products and Services (Domestic) e-Commerce (Order management, loyalty card management) Enterprise Software Products (Product configuration business?, Getting Software Products Cloud ready - cross-OS app development like iOS, Android etc.) Travel (e.g. Rail reservation systems), Rezopia is the main development centre.

Some steps taken

Entry into France

Acquisition of Rezopia (60% stake, Boosts Travel portfolio) and Xyka (Feeds into Rezopia)

Participation in various Travel and Retail events across the globe

Spend on Marketing/Branding

International business contributed 36% revenue, 81% PAT.

Domestic business contributed rest. Domestic business is a big drag from financial point of view.

International Business Growth (Revenue, PAT) - 25% and 85%. Domestic Business Growth (Revenue, PAT) - 1% and 31%.

Full Year Dividend Payment of Rs. 7/- - which is very healthy I think.

India Subsidiary named Sonata Technology Solutions (India) Limited was approved to be closed under Fast Exit Scheme. (Good thing?). Sonata Information Technology Limited is the main company into India.

Qualifications in Audit Report. Qualification 1: Non-compilance on Lease Deed (They had floor-wise lease deeds at different point and now entire building is occupied by Sonata. Single Deed is WIP). Qualification 2: Delay in filing Annual Return on Foreign Liabilities and Assets for FY14. (There were two forms that need to be filled, one being superset of other. So they filed only one thinking it was enough. 2nd form is now filed).

Most of their subsidiaries show loss on Page 27 of AR 15. Also NP numbers do not add up. Can somebody help?

Promoters hold only 32% of shares, FIIs hold about 8%.

M D Dalal (Executive Vice-Chairman) sold 1/5th of 1.25% of his stake,

Hemendra Kothari (India’s 94th Richest) increased his share from 8.61% to 10.14%,

Apart from sales by Bhupati investments, Major stake was sold by Orange Mauritius Investments Limited (4.24% to 1.72%).

CEO and CFO are external candidates and not the promoters. Most of their shares are received as a part of ESOP. I’m inclined to ignore their selling as they think of themselves as employees and not founders(Views?)

Rs. 6.5 Cr is spent on salaries of CEO/CFO/Directors/SMP/KMP, which is 5% of NP. (Reasonable?)

Thanks,

Rupesh

Disc: Invested at 145 levels, forms 3% of portfolio, looking to build conviction before further buying

Listened to management con call. Following is summary:

Domestic Product and Services

We don’t look at domestic business as a top-line market, the metric used is rather gross margins. We sign up for deals if gross margin is more.

During last quarter, gross margins went from 3.5% to 5%

Domestic business can also be seen as strategic business. E.g. if we are the largest partner in India, then we are treated very differently in the HQ. Domestic business might also enable for us to get access to technology.

We work directly with clients and want to be their value add partner. We do things like help in cloud migration.

Client Portfolio

We currently serve 40 to 50 clients, 20-25 clients are in pipeline.

Top 10 clients contribute 72% of the revenue. Top 10 clients are not same year after year, new clients enter and old ones exit.

Haven’t lost a single client so far, different clients have grown at different rates.

Off-shore pricing rate is ~25$ (per hour?). We don’t see any concerns with this rate.

We take 3 year view of the client and this year all the top 10 clients will have good business year.

Added 8 new clients this Quarter

Marketing Initiative to give seminars and focused marketing to get new clients. Attend travel summits etc. Increased spend on S&M. (Very casual answer by CEO)

Utilisation

Current utilisation is at 85% and CEO said we are over efficient (LOL).

Average annual salary hike is ~8%

Hiring is done based on visibility for next 180 days. Currently hiring is complete for next 180 days.

Finance

Hedging is done for dollar and euro on 12 rolling months quarter coverage. We are 80% hedged (?)

Hedging rates as follows: USB -> 65, GBP -> 103, Euro -> 74

Had exchange loss in Q4 of 1.2 Cr (Vs. 84L last Q)

40 Cr Rs. are pending from Indian Income Tax department

New investments might impact the margins.

Acquisitions

Acquired Rezopia to get access to travel accounts of marge client portfolio. Travel is the fastest growing e-Commerce segment (from AR)

Currently we have 300-400k$ business from 2 clients of Rezopia.

Plan is to integrate Rezopia products, build on them and create a product for larger Travel clients.

Results will take 12 to 18 months to show up.

Thanks,

Rupesh

This is based on my notes taken more than 2 weeks ago. Any mistakes are solely mine.

There’s no visible moat in the company, the only play is undervaluation with possibly good bottomline growth for 1 to 2 years. The balance sheet is strong and new acquisitions and entry into new geographies (Aus) might add to good growth.

Tax dispute with Indian authorities is matter of some concern (but not a lot due to strong BS), management (particularly CEO) sounds casual and over confident at times (Ignorable?).

Disc: Invested, not looking to hold for extra long term, might add for short term (1-2 years) on corrections

I am not sure if there is no visible moat. I’m a total layman when it comes to understanding IT companies. But I’ll still like to mention what I’ve understood so far.

sonata is more of a niche IT company and they boast to be a top quality player in their verticals.

the business is debt free, enabling them to operate at lower margins compared to competitors (or operate with higher OPM).

company claims to be an end to end service provider with acquisition of rezopia. Although, as mentioned before, it shall take more than a year and a half for the results to show up.

we need to understand if the growing number of customers is result of underpricing only or they actually are better than competitors at what they do (as they want to suggest with the awards and declarations).