I guess, hopefully, there will be an uptick of orders from these OEMs to catch up with production lost during the strike.

Disc - Invested

I guess, hopefully, there will be an uptick of orders from these OEMs to catch up with production lost during the strike.

Disc - Invested

In my opinion main hurdle in the price movement is valuations, This 70 PE multiples for 25-30% growth company is already at a premium rate, until and unless there is some sharp jump in the Top & bottom line there may not be much movement.

The acquisition of Novelic (54%) may add some value. The segment is niche and the target company is profitable.

Disc: not invested.

Stance: Invested

There should be a movement in topline and bottom line in next 1-2 years. Their revenues are linked to how BEV and ICE automotive industry are performing. In the current high interest scenario across the world, people are skeptical to take loans to buy vehicles. But when the interest rate cuts start globally, the sales will start increasing sharply.

Of course, there might be some lags in the timeline. But generally, auto sector and infrastructure sectors are beneficiaries of rate cuts. This is my hypothesis on the stock.

Only concern with sona comstar is - it should not go syngene way. All good stories and build up. No delivery. Share price keeps underperforming heavily.

As per concall and Media interviews of management revenues in FY25 & FY26 could shoot-up significantly as more number of products are coming under serial production.

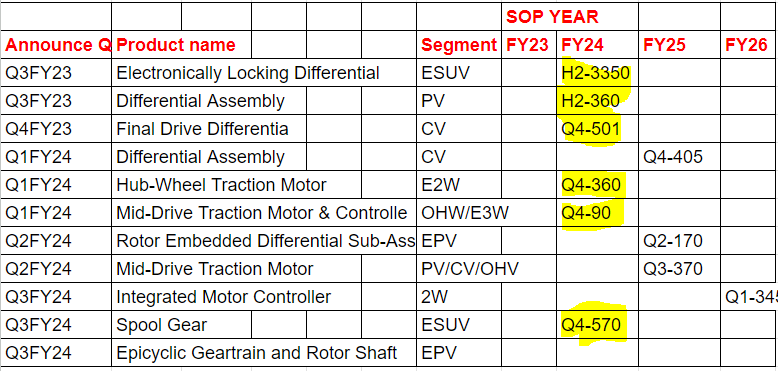

I have tracked few product names of Serial production starting in Q4 & H2FY24 order value is ~5000 Cr

5000 cr is very big number , can you post some of the product names to know more about those.

Hi, on the Tesla front, anything most current? Sorry if i missed some note on this already.

I hope this will help, Numerical number beside Quarter show that start of serial production. it will take few months to ramp up the production of particular product but i am not sure about the duration of the cycle

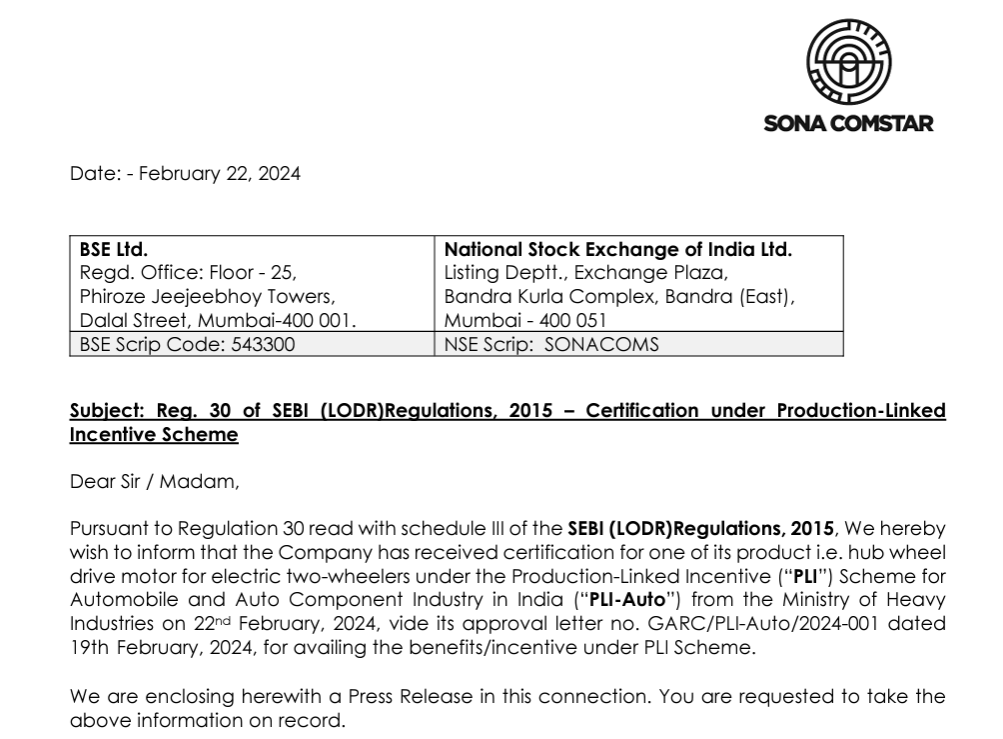

PLI application for 1 product is approved, as per management all EV related products they are making are eligible for PLI.

19000 Cr of EV order book is there, imagine the amount of PLI benifits they would receive. This being factored now.

We can have some insights of these PLI benefits exact calculations in the concall

Q3FY2024:

Highest ever EBITDA and Net Profit

Order Book of 24,000 Cr (79% is EV)

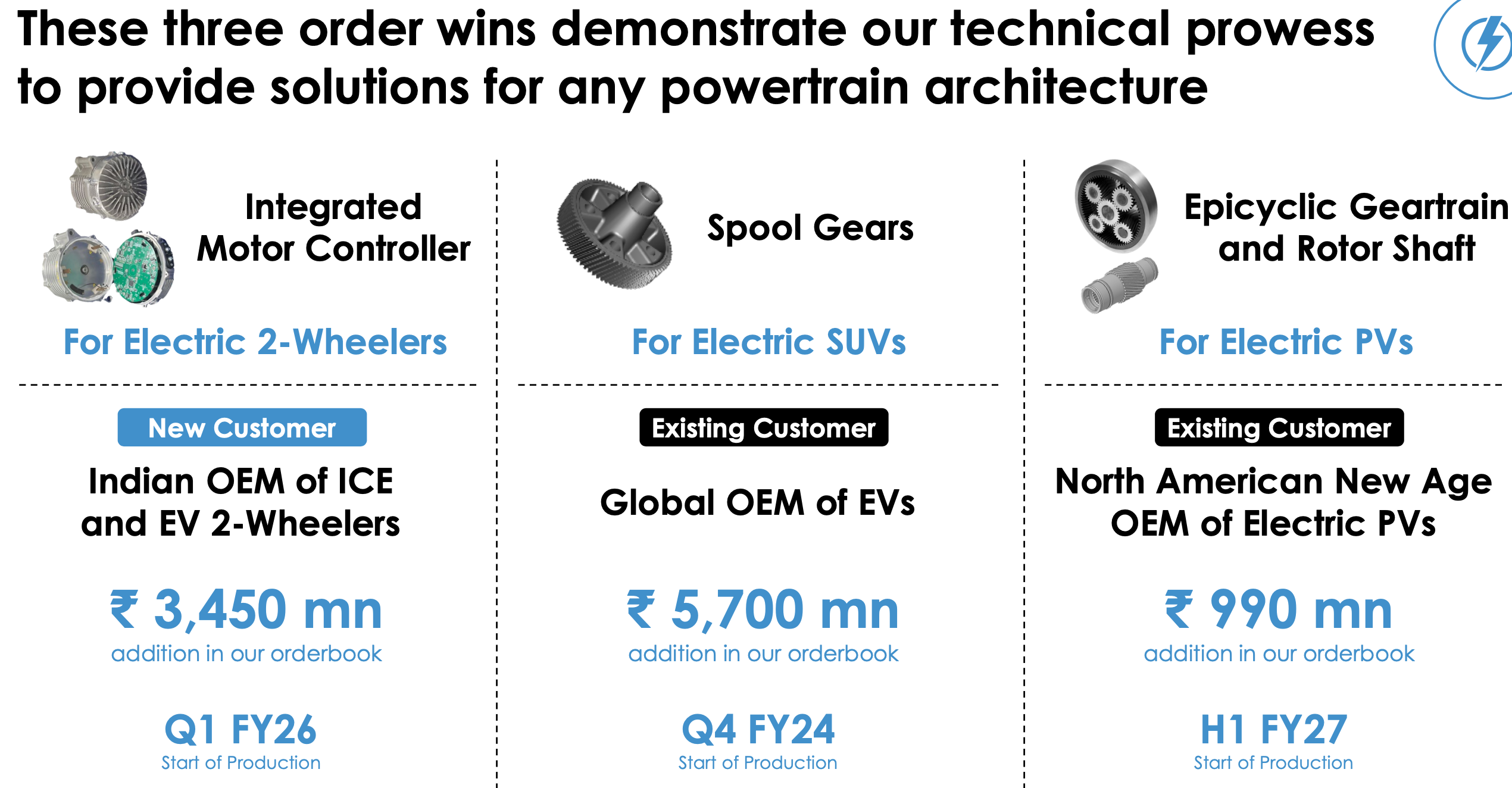

Added 5 new EV Programs and 2 new EV customers.

Now have 53 EV programs across 30 unique customers.

The Company faced the following challenges

In 2023, the company has increased its global market share in both differential gears and starter motors.

“We are certain that electrification will continue to drive strong growth for us non the immediate, in the medium as well as the long term”.

Outlook on india

Disclosure: Invested

I am still waiting for it to rock :D. The results for the fourth quarter were impressive but it still dwindled today. The valuations are still expensive though. Even with the net profit growth for FY 23-24, PEG is almost 3 at current PE.

I believe PEG is 2.75 if you consider the valuation at consolidated basis. Nonetheless it is still on the higher side. Assuming the growth momentum of 25% for the next 5-6years (quite possible) the high valuation is ok.

Sona BLW has also setup a merger and acquisition committee, some news could be expected in months/years to come.

Not to mention, the management ethos is what I really like about this company. Maybe I will not make quick gains in this counter but i can comfortably park my investment here for a excellent long term wealth creation. Company should compound at of 20-25% for the next 5-7 years easily, considering the earning visibility.

As everyone knows the fact that valuation is high and still FII’s own 33% and DII’s own 29% (both highest in recent times) with retail only with 8.5%. This shows that everyone is positive and waiting for the price to expand. Looks like it’ll be range of 585-700 for some time.

Disc - Invested and ready to hold for many years to come.

Waiting for the transcript to come (don’t have the patience to go through the recording). Technically its at an important juncture nearing 200 daily EMA.

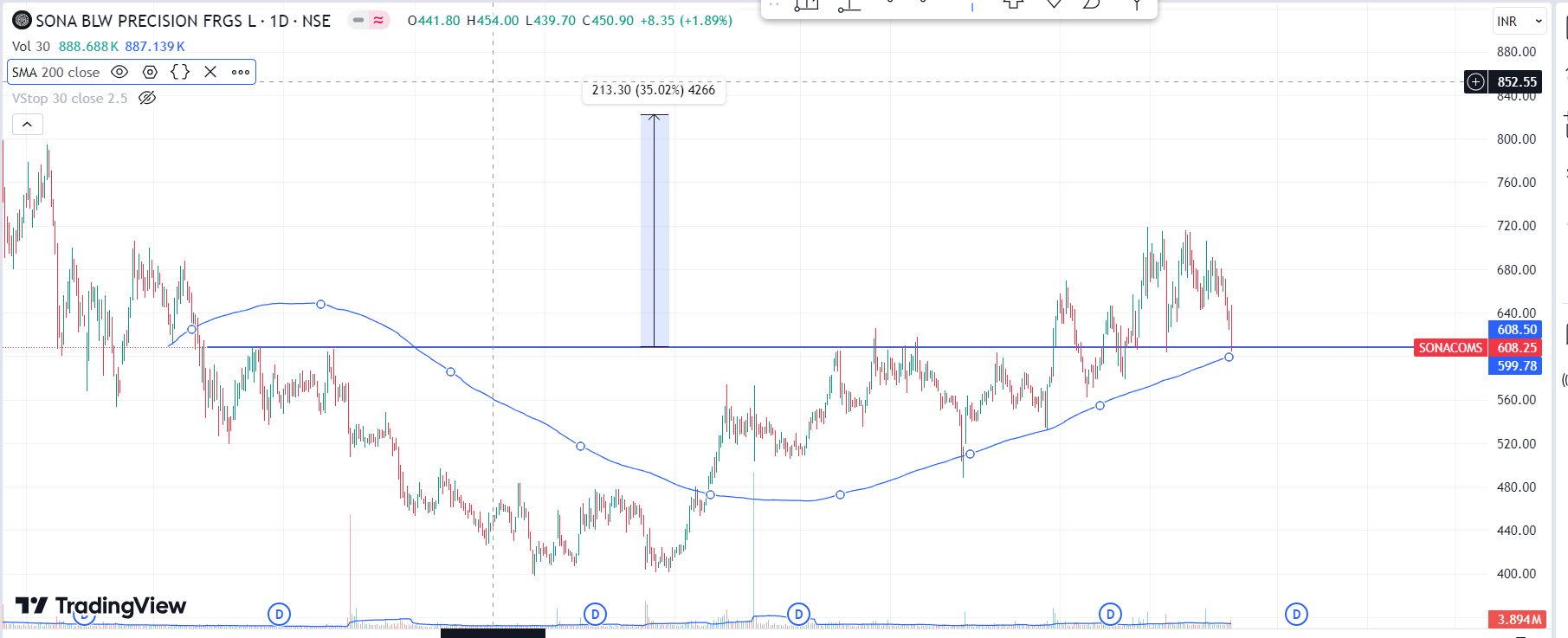

I think the downside risk is not too much (I may be wrong which I often am) but the upside at this level will be time consuming - so an opportunity cost where on the other end broader market is doing well.

Disc: No position. In a dilemma whether to start building core position or wait for it to setup technically.

Hi Pankaj,

My 2 cents,

Since Dec 2022 the price has moved (today’s CMP) barely 22-24%. On the contrary, FII holding rose 11% to 33% whereas Dll holding from 24% to 28% and Retail reduced from 11% to 8.5%.

IMO there’s no significant supply at this level (unless any sharp downwards movement in broader market).

I’m ready to buy some more.

Yes I also think the downside is not much. The same may be true for demand as well. I would see how the stock reacts at this level and maybe do a pilot buy.

I intend to deploy 10-15% capital in this company but I don’t want that capital to be idle. If it slides further it will be difficult to hold for me. If it consolidates then I’m losing opportunities.

So I need to see how it reacts here. If it shows further signs of accumulation I get in and size it otherwise will review.

Anyhow this is my thought for now, if something interests me in this concall my view may change.

Here the dilemma is what typical Technofunda investor faces - technically I have better setups in the market but fundamentally I like this company and biased.

Anyhow will be a good learning experience for me ![]()