I’ll say what I said to Manish ji Sorry Manish ji, I got carried away. I already apologised on the forum. Let me apologise again. Sorry.

But I stand by what I said. This company is run by loons and it deserves the PE it has atm.

I’ll say what I said to Manish ji Sorry Manish ji, I got carried away. I already apologised on the forum. Let me apologise again. Sorry.

But I stand by what I said. This company is run by loons and it deserves the PE it has atm.

This seems a major red flag. Can we have views on this from other fellow members ?

It appears that the situation should be considered alongside the July Rights issue, which was valued at Rs. 141 Crores at Rs. 275 per share. Additionally, it’s worth noting that promoters are consistently purchasing shares from the open market.

From this perspective, it seems like promoters are aiming to accumulate as many shares as possible at a lower price, using various means, including potentially questionable tactics.

While this news might not be favorable for existing shareholders, it does suggest that promoters have a high level of confidence in the future growth of the business.

Looking at historical precedents, similar occurrences in other companies have been overshadowed by sustained business performance. However, it’s essential to acknowledge that while this may impact the stock price in the short term, market outcomes are never guaranteed.

Ultimately, how one interprets this situation depends on individual perspectives and risk tolerance.

Disclosure: Invested

I have written to company for clarification. will let you know what i get

Looks like a lot of active shareholders raised the issue with the management and hence management came with a clarification.

But the important thing to note is- There is nothing in the clarification.! ![]()

As per management, Company needed funds, so they decided to give company funds at 1/10th the Market valuation and Investors should be thankful to them. I don’t understand why they even came out with such a clarification.

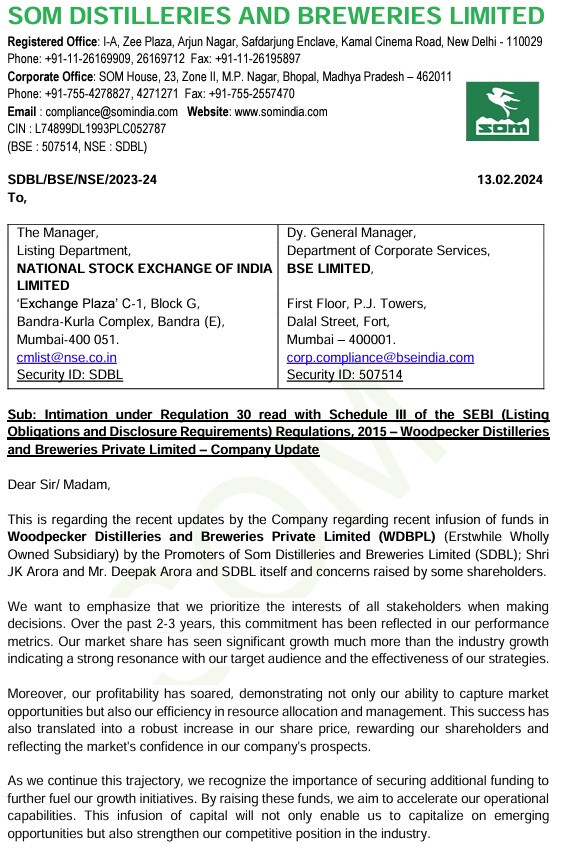

@Sanjeev_Bansal Yes it is disappointing. Because shareholders have issue with valuation of subsidiary(Woodpecker) not the infusion of funds.

Please help me understand

if it is possible to add more fund on similar or little bit higher valuation leads to decrease in earning of the main company(SDBL) and reduce main company shareholding to 50% (or even less)?

Company mentioned that it want to raise funds about 350 cr in Sept last year but it was not closed that time and again in Jan this year. Will above move be considered negative by institutional investor?

Disclosure : Invested and tracking.

Promoters’ ongoing purchases from the open market may be seen as a positive development. However, these disclosures suggest a strategy to accumulate as much stake as possible, potentially at the expense of current stakeholders’ interests.

The question arises: Is it legal to acquire such stake at any valuation without shareholders’ permission? If so, promoters could feasibly continue acquiring stake in the future, even at lower valuations, without restrictions. Does the law permit such activities openly?

Thanks @mendax2014 , this is a grown up forum. I dont mind using those words as it communicated to me cant trust the promoters so sell it. I agree when i look at it again. thank you for sharing and raising an alarm

FYI.

After the founders failed to remit Goods and Services Tax in a year, they were arrested the next year. After they were released from jail, within ten days they donated Rs 1 crore to the BJP. The same year they gave another Rs 1 crore to the BJP as a donation.

Hi guys,

Long time since I have discussed about this company

Let’s have a look at what is happening and how can we expect things going forward, Please note I am mostly discussing beer in the entire post

What is the capacity now and revenue generating potential?

New capacity addition of 6 million cases in KA would be online by March 2024. It can generate revenue of 270cr at 90% utilisation

So all in all after this capex with 85% utilisation company can do 1600cr of revenue in FY25 about 30%++ growth from 1200cr (now current run rate includes IMFL but 1600cr is pure beer)

What are the growth triggers going forward??

Lets see the events which took place last year

Market size

Then we have Kerala, Tamil nadu , Punjab, Jharkhand and Puducherry which they have entered.

So it is plain and simple they are going PAN india, entering into contract manufacturing for IMFL where they have poor utilisation and if you see whichever market they enter they become the 2nd largest player with about 20% market share. (Detailed expansion on this)

i) 2018 opened factory in OR, remove 2yrs of covid, in 3-4 yrs they have scaled to 18% market share as on june 2023

ii)2019 opened factory in KA, remove 2yrs of covid, in 2-3yrs they scaled to 20% from 3% as on may 2023

iii) In delhi without factory have about 11% market share

iv) Pan india market share from 2% in Q1FY23 to about 5.5-6% in Q3FY24 (need to verify this somehow but with the kind of growth they had look realistic)

4.The biggest trigger for growth would be when they acquire or do a greenfield in any other state, we know when they open a factory that is the time they start dominating in a particular state

OPINION - I think this year by august - september we should get some clarity on this capacity expansion, this would be one of the major triggers for re rating in my opinion and this is definitely going to happen.

Guidance, valuation and Peer comparison

This year I see them closing at 1200cr and with KA capacity and all this tie up I see 1600 cr in FY25

Management has guided for 2000 cr by FY26 this is very much achievable though slightly conservative in my view, so for the market size table above if they take 20% market share of 9.5cr cases that is almost 2cr cases and current run rate in 2cr cases + IMFL should do good and some states are not added as well + every year there is 3-5% of price hike. Looks very much achievable. Lets see

Comparison with UB

They are clearly better in each parameter, so why is there a discount? My understanding is they are not very big still and they are not a pan india brand + corporate governance issue. At 2000 cr sales they will be 30% of UB size in terms of scales and by FY26 they might even do better this depends on the factory which they would set up

Recent stake bought in subsidiary

What did they mean here?

i) Back in 2019 promoter issued them warrants for 13 lakh share at a price of 275 when the market price was 100, almost 23cr extra investment here

ii) In december 2022 they proposed to issue them 65 lakh warrants at 142 but they cancelled it stating less funds is required and we will do rights as we want shareholders to benefit , now that time this would seem like a joke

Now they have issued themselves 55 lakh shares at 275 rs, I am sure when the business back in December 2022 was about to do very good the promoter definitely understood this and could have taken stake back then, just more money was not required does not make sense, they had the opportunity to buy it at huge discount.

Now they are doing at 130rs premium almost 71cr extra

iii) We also need to judge corporate governance based on the standard of the industry, beer is an industry where a huge amount of dealing is done in cash.

My point is they have not done good but they are not complete chor

Even if you see the stake in subsidiary cannot be sold, it is like a lifelong stake and they needed money for 55cr hassan expansion. So again we should not see this event in isolation. Like we can reverse this question and ask what would we pay for a stake in the subsidiary where we won’t be able to sell the stake in open market?

IT raid

This was purely political in my view, I mean the company says in the last 18-25 yrs this has never happened . They used to pay 40% taxes before 2019 and it is a nature of the IT department to go behind where there is exponential growth, which they had.

What happens in this company in worst case scenario, i think we can still make 40%-50% kind of returns in 2yrs, pretty decent for a worst case imo

@Sanjeev_Bansal @rajpanda Sir plz share your view on it

ayush sir not able to tag you, you are also tracking this business from a long time, I would be glad if your could share your view on it

One last point promoter is buying his business left right and center, he is playing the long term game, I think he can see his business become a second largest brand in the countary in coming yrs, I think a B2C business in a industry growing at 9% which cannot be replaced by AI, available at 10times in 2yrs forward, seems to be a good opportunity

DIsc- invested, buying , can be wrong and will exit if I see some more red flags

I also request everybody if somebody can help me meet the promoter, have some wonderful questions, should benefit all of us, DM me , we can collobrate

thankyou

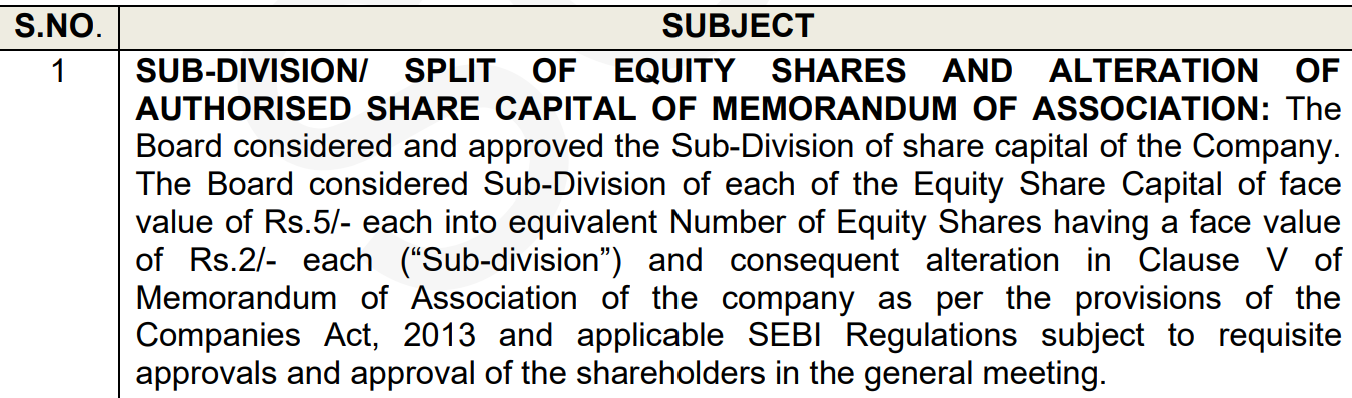

@Sanjeev_Bansal The company promoters purchased 20% of a subsidiary that earns (50% of overall earnings 30cr out of 60cr) at a pre-money valuation of 150cr i.e. 5x ! How can the minority shareholders not have a say in this? This does seem majorly unfair to the minority shareholders ! It appears this is setting the stage to merge the subsidary into the parent co at inflated valuations to further increase the shareholding of the founder (which in itself is not bad) but this is clearly at the expense of the minority shareholders. Does the dilution of shares in a material subsidary not need explicit minority holder approval?

@manhar How can you focus on the earning power of the overall company if you cannot even predict that the founder may further dilute the listed company’s share of this subsidary ? How does one get comfort they will not do this to the other subsidary? The absolute value of the public market purchases are meaningless (<50cr worth)

Welcome to the world of small and midcap investing in India ![]()

Jokes aside, I believe they need an approval from the shareholders but not sure about it. Some one from the community may throw more light on it. But I don’t think even that will pose much challenge for the promoters. We have companies like Vedanta, 50 times bigger than SDBL doing all kind of stuff and still nobody says anything.

Corporate governance is a big issue in Indian companies and given the lack of legal oversight and strong institutions (SEBI is not a strong institution), such issues are very common. >90% of the companies in this space are like this. You may take them to court but everyone knows the speed and solution in such cases. Simple solution is to stay away from such names or if still invested, be aware of what you are getting into.

@manhar the promoter has in effect purchased 10% of the company at 30cr instead of 200cr. And people are willing to look at his 2cr worth market purchase and claim that he is minority shareholder friendly. Does this not set a very bad precedent? Should they not be penalised with a very low multiple (like Lux etc?)

This is a 50k macap company doing such stuff, 100cr of unaccounted beer

My point is we need to understand what kind of industry we are analyzing and what kind of corporate governance can be expect from that industry.

Think about this way som is the largest manufacturer in MP, they are in business for the last 30yrs and they might be one of the biggest non government company to provide revenue to the state. Just think they might contribute like 5% or 10% to state government revenue.

The point is just understand how deep their roots might be and the kind of GANDAGI they are dealing in, it is a CASH industry, promoter pumping hundreds of crore in business, now we dont have to be a forensic expert to understand that this is all unaccounted sale of beer which they are pumping in the business.

Please understand if tomorrow their business stops it will effect entire MP and as they grow larger it becomes huge problem for each state loosing hundreds of crores of sales.

The only thing which I wanted to verify here is weather their number which they are reporting are true or not (atlest I should know the PE I am calculating is real) as of now I could get decent evidence and waiting for some more.

No straight answer to this, one I would ask in concall as to why they did this and second if they do it again I would increase my margin of safety.

Like right now I am comfortable buying them when they are below 20PE and sell close to 40PE, if they again to such stuff I would buy them below 15PE or so. The reason I am intrested in this business becasue the product is great and the business is real.

I think you did not read my post completely let me put it again

Plus thier share holding is up by 16% in last 2.5yrs so I did not get the 2cr point

Guys I am actively seeking the guidance of seniors, my money is at stake in this company and I dont want to loose it, hence I am actively looking for some example if anybody can share where business was REAL but they had serious CG issue and business was very strong fundamentally. I want to read more of such business and see what happned with them

Just to give an example cmpanies like Manpasand Beverages Ltd did not have CG issues but were FRAUD and companies like Caplin Point Laboratories Ltd did have CG issues

Markets are sentimental, there was no reason for it to fall 45% from its high and there is no reason for it to recover 40% form its low now (promoter was a chor know from a long time it is only that people realized that again recently)

The moment there is some development on their latest factory capex market will again forget and I would expit close to 40times pe

DIsc- I can be wrong and would like to accept my mistake in case I am wrong and draw my lessons, vice versa

some good news

thankyou

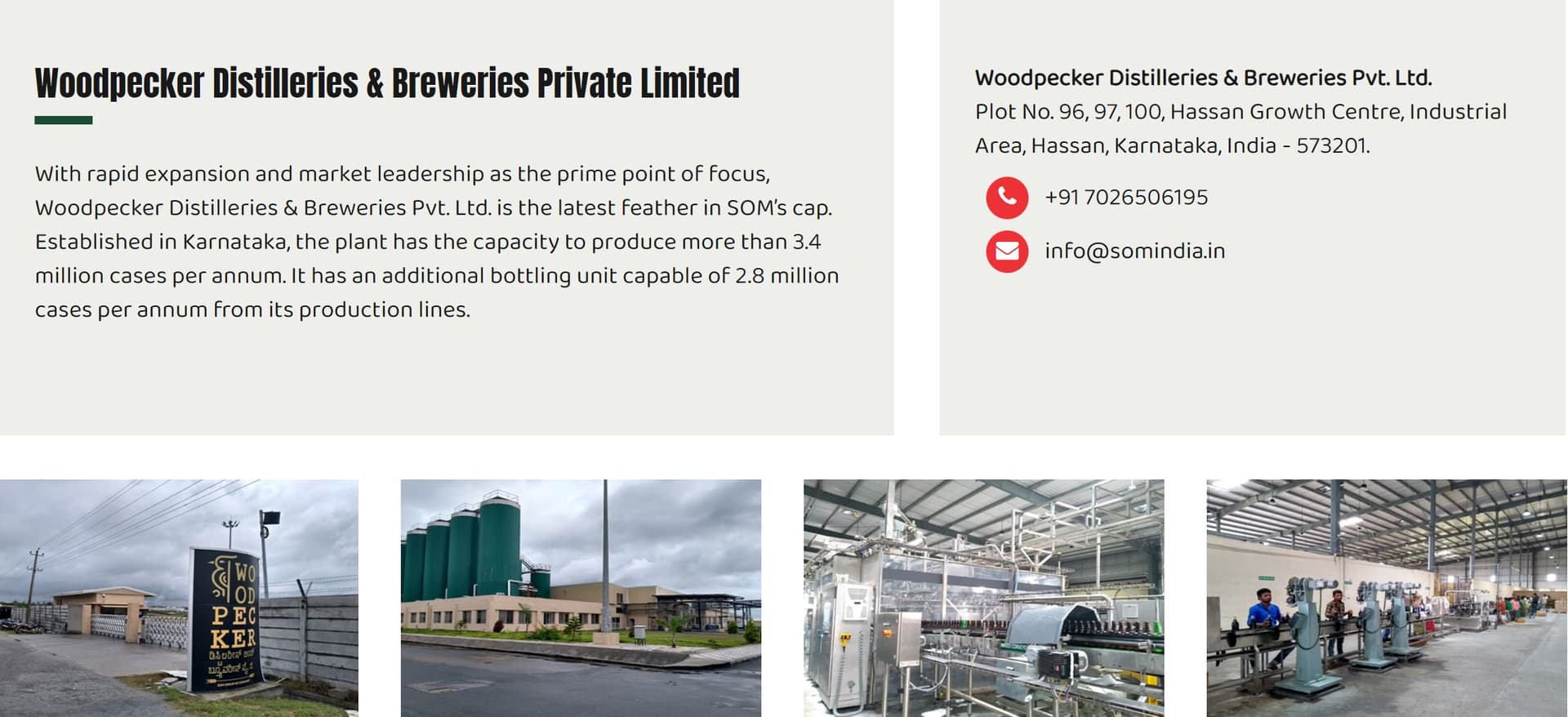

I happened to visit their Hassan plant around a year ago which manufactures Woodpecker Beer predominately, and a few exchanged words with the employees confirmed the demand to me. They were operating 24/7 trying to fulfill orders above their capacity. I think the situation has been the same ever since reason why they are also seen doing capacity expansion.

Edit -

This was the one

I don’t know if you have mentioned this before in the thread, but what is your return expectancy here? CMP is 25% below the ATH. Are you looking for a multibagger here or do you want to hold for longer term, thinking of compounding?

From your posts alone, it seems there are some issues with the company. The participation from institutions, FII or DII is <1%. No MF holding here, but they hold United Spirits, United Breweries, Radico Khaitan (I have not checked others). Retail has 64% holding here.

If your had bought a lower price, as a value bet, then I guess it is fine, if not, if your purchase price is close to CMP, or if you had bought at a higher price, and are thinking of increasing position, then it can be risky. Price can double from here within 1 year, due to capacity expansion, or for any other business changes, I don’t know.

Senior and experienced investors usually stay away from such businesses, one reason being, there are many opportunities available in the market, they can dedicate their time and efforts to such businesses and increase their chance of being rewarded. As you are young, you have every right and affordability to learn and experience any which way possible. So this can be a case study for you, irrespective of the outcome.

Not invested, know nothing about the business, nothing to add quantitatively, just posting some qualitative observations and some thoughts.

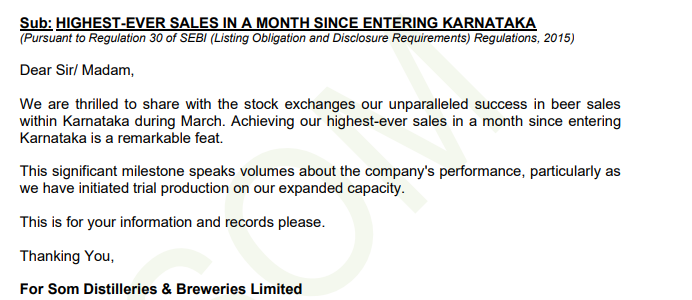

Commercial production of the increased capacity at their Karnataka plant has begun.

140 lakh cases from the previous 90 lakh cases.

Of course the company has done a nice job. of course promoters have done nice things in the past. but @manhar the promoter has just purchased 10% of the company at 30cr instead of 200cr. Which fund manager will back this company? I also was thinking of buying this company but is corporate governance optional? But i guess different people have different thresholds.