Solara Active Pharma Sciences Earnings Call for Q4FY21

Business

- Dip in gross margins is mainly due to fluctuations in sales mix between regulated and non regulated markets, since business is expanding into non regulated markets this has impacted the gross margins, this is going to improve in future

- High Receivables - This is again due to non regulated markets contribution (sales increase on QoQ is due to this 30% sales from North America + Canada, rest is from non regulated markets) , in these markets the credit terms are slightly stretched compared to regulated ones

- Dip in Ibuprofen prices are protected by long term contracts

- Raw material fluctuations are not going to affect much due to the processes and cost efficiencies in place in the form of better procurement processes in place

- Favipiravir and one more COVID drugs are going come on to the market soon (Aurore has more of these kind of drugs )

- New Product Launches in Q2 Q3 - (Market opportunity size could be 10s of crores, too early to give exact number, multiple discussions with customers, capacity is fully booked for the entire year, good margin products )

- Current capacity utilization is about Mid to late 80% (Excluding Vizag)

- 35-36% raw material is imported out of which 29% is from China (it used to be 32% )

Management

- Hired a consulting firm to help to identify synergies after the merger

- Focus on backward integration

- Finding ways to get the approvals by using remote audits (this is already happening in the industry )

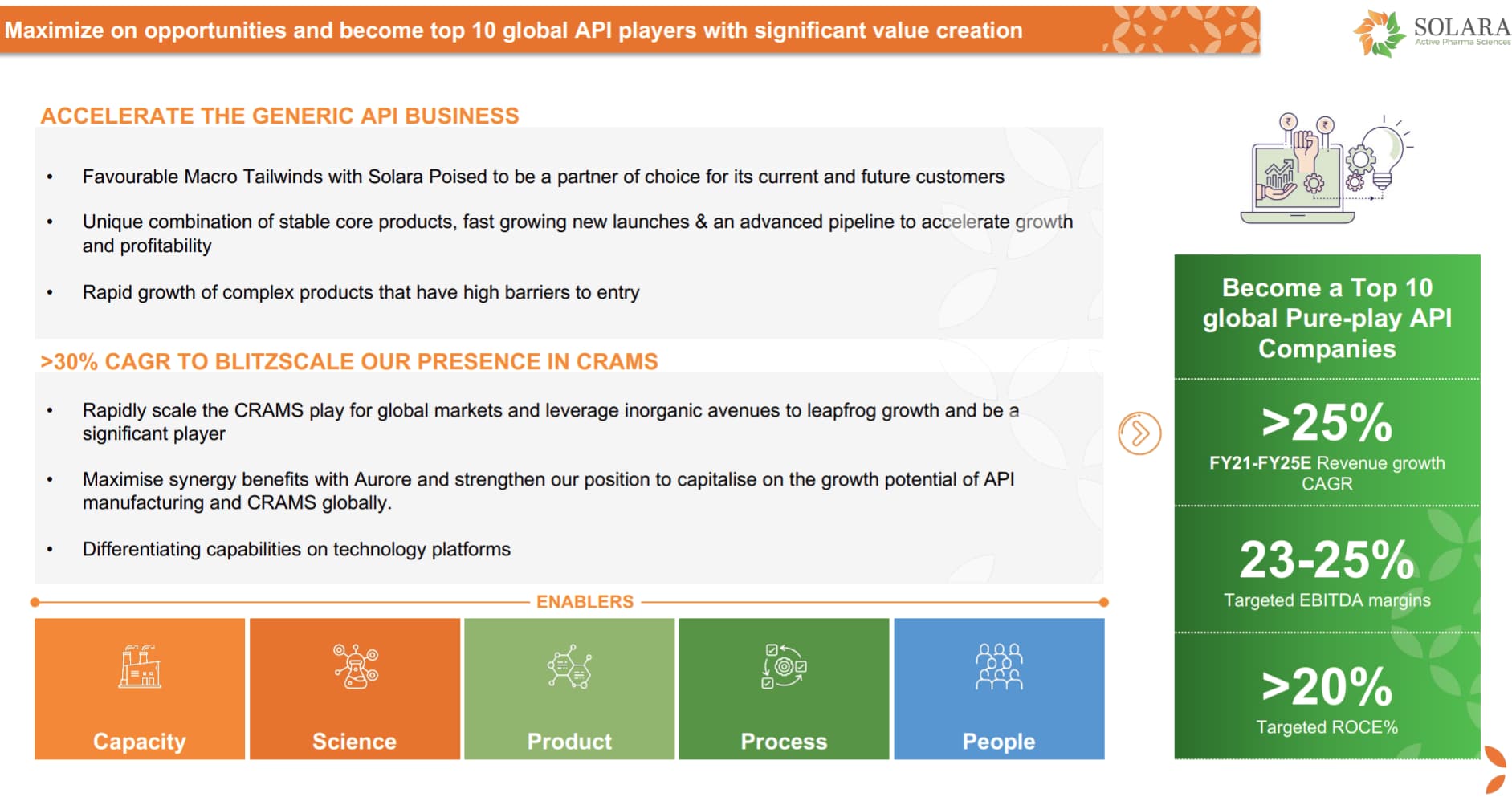

- Management didn’t give any guidance on the growth, this is mainly due to the ongoing merger with Aurore, soon after the merger they are going to give detailed update

- Order is full and Vizag plant is running its 2/3 of capacity, this is mostly going to cater to non regulated market and it is a multi purpose plant (Total IBU capacity 3,600 tons in Vizag all of this is going to less regulated markets at the moment, currently there is no approval from FDA at the moment , soon this approval comes then the product can be sold to regulated market)

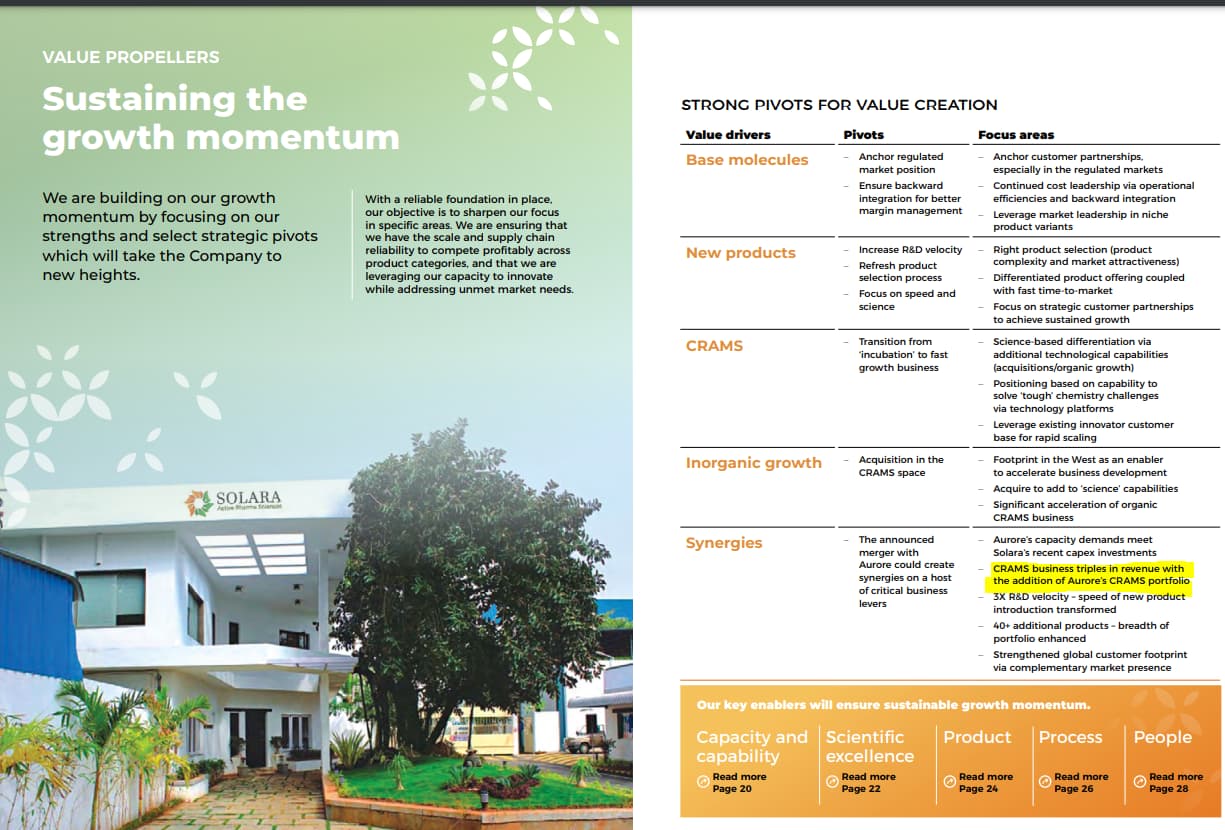

- CRAMS is picking up (Added 4 customers , Revenue + cost synergies + R & D - Aurore merger synergies ), made breakthrough in Japan, Korea, Singapore

- Also thinking of additional capex , will give more clarity after the integration with Aurore

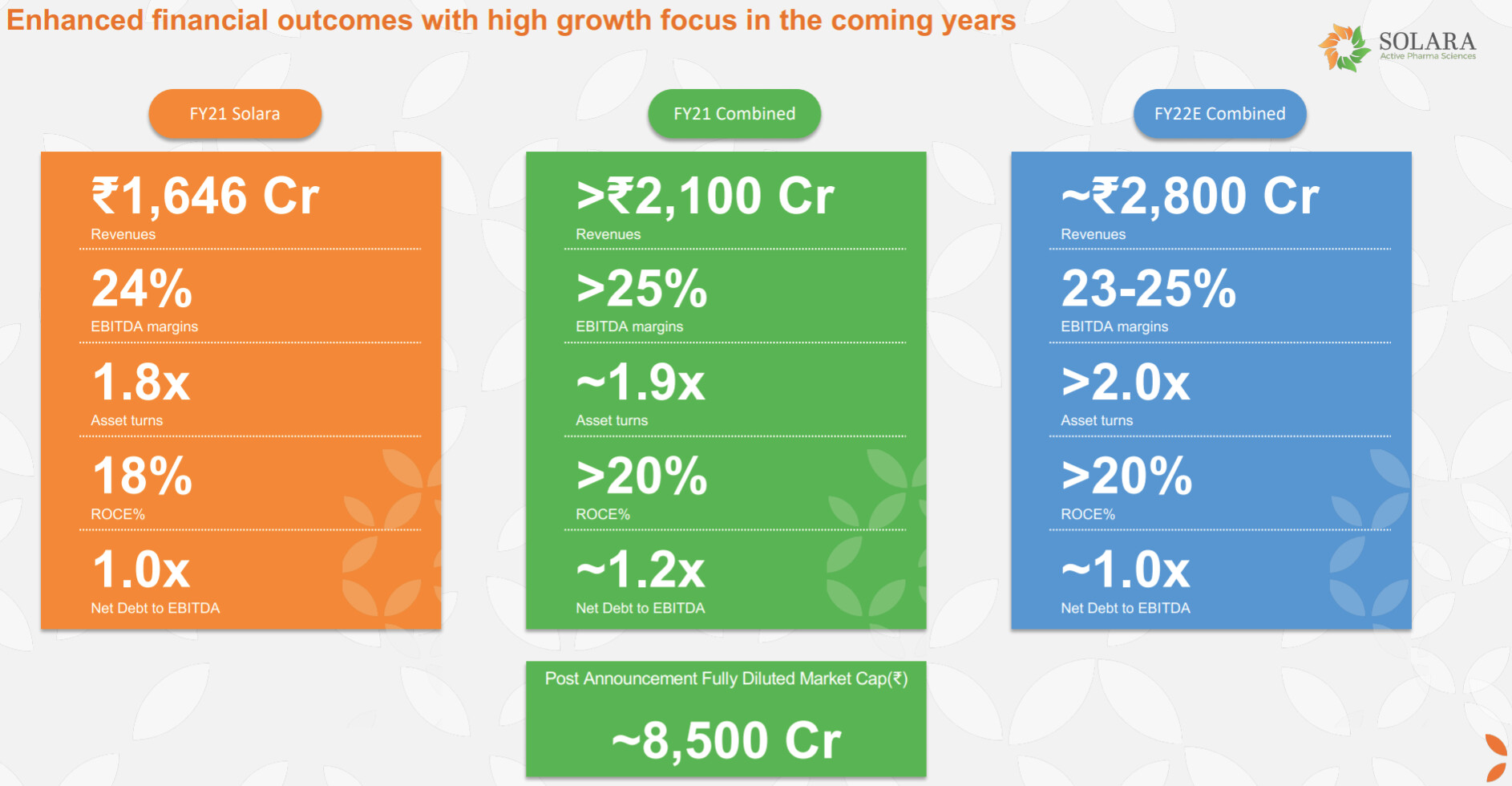

- Financial ratios are going to improve once the Aurore merger is completed

- Europe is slowed down mainly due to more focus on covid related products by the clients, expecting things to come back to normal soon

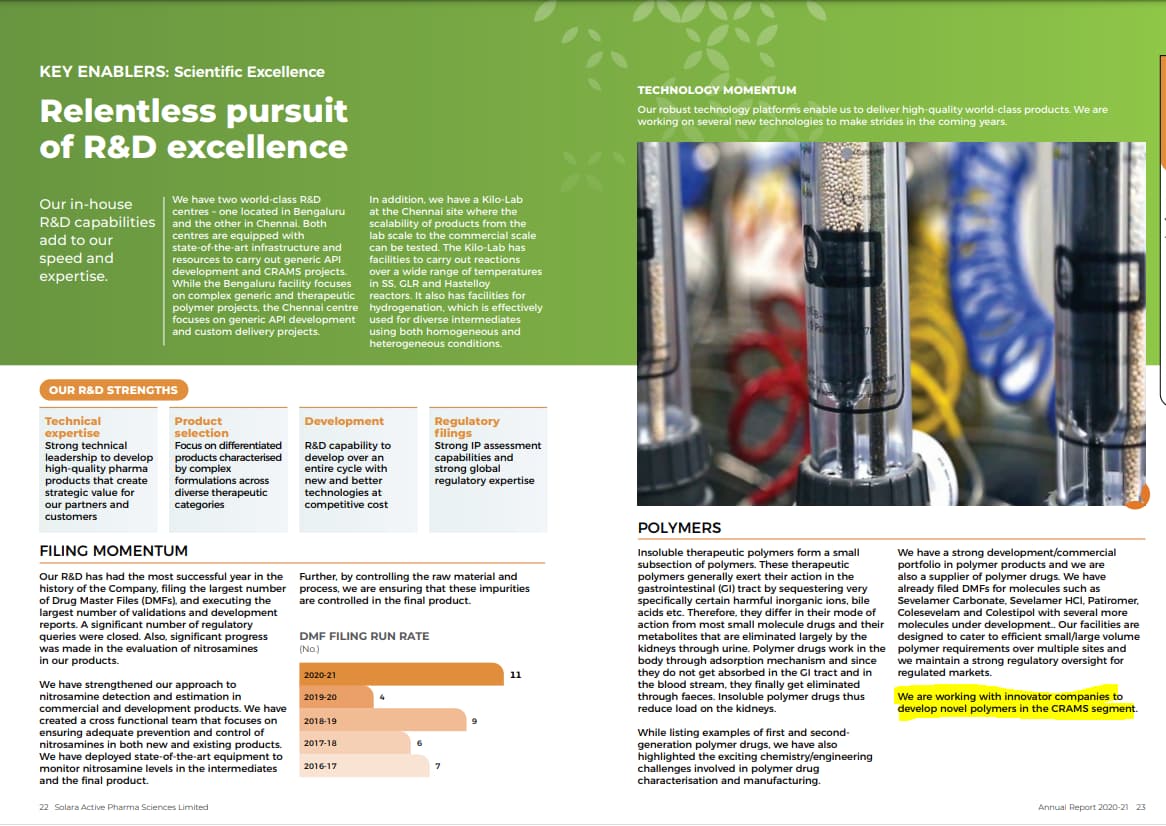

- Remain Invested in Technology Platforms - for example Bio Catalysis, Flow Chemistry , Fermentations , Complex Generics (Help us to offer higher margin products , we are working on these lines )

- CAPEX - 250 cr - Growth capex, we will give more details post synergy (Land available in mysore and vizag so we have to decide where the demand etc… )