Solar Industries confirms receipt of order for 3 variants of Pinaka missile from Armenia !

https://idrw.org/armenia-ordered-3-variants-of-pinaka-mbrl-from-india/

https://idrw.org/armenia-ordered-3-variants-of-pinaka-mbrl-from-india/

Solar Industries revises their annual revenue growth guidance for FY 2022-23 from 30% to around 50%.

Cyber attack on servers, not sure about the authenticity of report but the website is down from last saturday.

Surprising thing is, the ICICI Securities have made the recommendation after the said cyber attack. Even the share price is not much affected.

or are they finding exit route by recommending ![]() and they are not talking about any impact of cyber attack… it is these situations which make individual investors dilemma on whether to buy or not…solar was never a cheap stock… its still not now also … P/B of 17 … and 52 week range: 2000 - 4500 …

and they are not talking about any impact of cyber attack… it is these situations which make individual investors dilemma on whether to buy or not…solar was never a cheap stock… its still not now also … P/B of 17 … and 52 week range: 2000 - 4500 …

Solar Industry is one company Indian defence can’t live without.

We have to see what the effects of the cyber attack going to be.

Since i could not get more update on this attack … i reached out to the IR , and go a prompt response

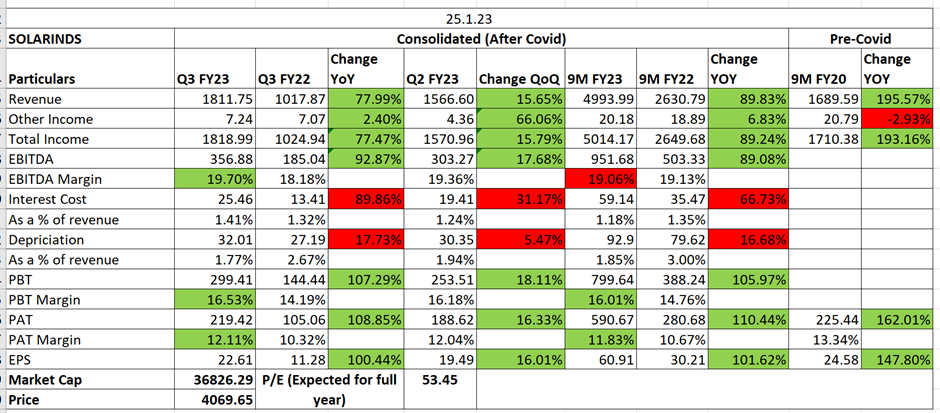

| - | Explosives contribute 48% of the revenue and exports contribute 40% of the revenue. |

|---|---|

| - | Explosives segment by volume saw a 17% YOY growth in Q3 & 13% YOY growth in 9M. |

| - | Explosives segment by price saw a 46% YOY growth in Q3 & 63% YOY growth in 9M. |

| - | Explosives segment by value saw a 71% YOY growth in Q3 & 85% YOY growth in 9M. |

| - | Initiating systems saw a 32% YOY growth in Q3 and 33% YOY growth in 9M. |

| - | Most of the sales comes from Coal India (CIL) (17%). Exports are around 40%. Defence sector takes up about 6% of the sales. Housing & Infra segment contributes 17% to sales. Non-CIL customers from coal segment are showing demand. Overseas subsidiaries are also seeing increased demand. |

| - | Order book is at 3389 crores. Defence sector is 817 crores & 2572 is from Coal India and Singareni Coal. |

| - | Market share of 30% in India. |

| - | In exports of Industrial explosives and initiating systems, 70% share is of Solar Inds |

| - | Exports to about 55 countries and recently expanded its manufacturing base to African countries. |

| - | Gross margins have reduced due to high input costs. Explosives realizations were also quite flattish. |

| - | The company has increased its revenue growth guidance to 65%+ for FY23E (previous guidance was 45-50% growth). |

| - | Volume Growth guidance is 15-17%. In exports, volume growth will be seen around 15-20%. |

| - | EBITDA margins expected to be 18-20%. PAT margins around 11%. |

| - | Domestic explosive realizations will remain flattish and will pick up after 2 quarters. |

| - | Exports revenue is expected to increase and EBITDA margins will be between 18-21%. |

| - | The company expects the next contract from Coal India by October 2023 and from Singareni Coal by April 2024. Till then, existing contracts in hand will be executed |

| - | Space Applications of their products is also in the testing phase. |

| - | Capex for the next two years is also expected to be |

| - | Commercial production at Australia facility is expected to start by Q1FY24. Indonesian unit is already started partially and is expected to start fully by Q1FY24 |

The stock seems to be consolidating. Any update on the fallout of the leak?

Economic Explosives Ltd wholly owned subsidiary of Solar Industries India Ltd has signed a contract on 20th April 2023, for supply of Loitering Munition with Ministry of Defense, Government of India.

This is a first of its kind Loitering Munition made by an Indian Company. It demonstrates our ability & agility in absorbing new technologies to develop products for the future. The contract is for value of Rs.212 Crs to be delivered within a period of 1 Year.

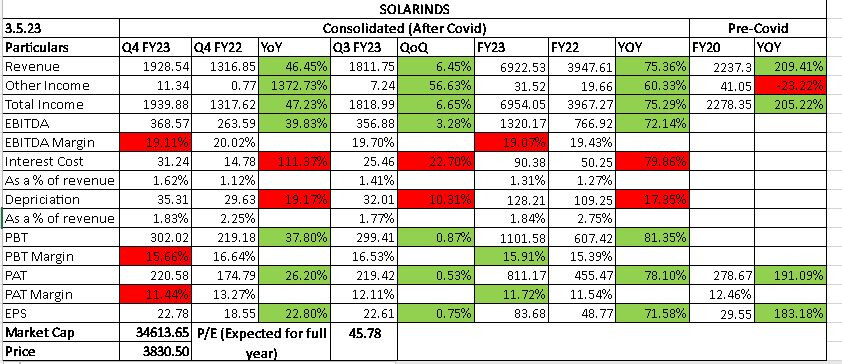

FY 2022-23 was an exceptional year, Amonium Nitrate prices had reached historical high of EUR 850 /MT… as against average price of around EUR 200-250 for last 10years. Company has also advised in its current concal that there will be volume growth of around 15% in the current FY , however topline growth will be flat.

The current valuations in my opinion seems to be reasonably high looking to flat growth and hence the share price is expected to remain stagnant for next 9 to 12 months.

Disclosure : Exited my position and will review entry after 9 to 12 months.

Based on past performance and future data point experts please suggest is this a good entry point for investment for 3 to 5 years thanks in advance for your inputs .

There is always a good entry point depends on individual risk appetite and investment strategy .

Following Makes it lucrative : 1) Solar industries announced that it has successfully demonstrated its prototypes of Weaponized Drones (Hexacopter) and Loitering Munitions and become the first Indian firm to do so.

2) Solar Industries is a world leader in packaged explosives and accessories.

It is developing an array of drones for ammunition delivery to bring a new capability to Indian armed forces.

It has one of the largest production facilities for HMX & its compositions in the world. So far India was dependent on imports of these products but , these items are now being exported to many countries including the USA, Europe & Israel.

Compounded Sales Growth

10 Years: 21%

5 Years: 29%

3 Years: 46%

TTM: 75%

Compounded Profit Growth

10 Years: 20%

5 Years: 28%

3 Years: 41%

TTM: 71%

Return on Equity

10 Years: 24%

5 Years: 25%

3 Years: 27%

Last Year: 33%

Valuation is on the bit higher side. But you will have to pay for the business in this sector who has strong Moat.

The stock has multiplied by almost 75 times. Way more to go .

Disc : Invested and Biased

Brokerages expect revenue of 7687 cr. in FY24 and 9269 cr. in FY25. EPS expected is 97.3 and 123.7 for the respective years.