Business in detail:

SNL is one of india’s leading needle roller bearings manufacturer. Manufactures wide range of needle roller bearings for automotive applications to serve OEMs and Aftermarket in india and overseas.

Among the very few SNL Bearings Ltd. could establish itself as one of the leading Needle Roller Bearing manufacturers mainly for automobile industries. For more than two decades it has been remained one of the leading suppliers to various big names in Automobile manufacturing like BAJAJ, LML, KINETIC ENGG.TVS, MARUTI and TATA MOTORS. Besides it manufactures some industrial bearings as well used in Textile machineries and household appliances. SNL exports its products to many of the countries across the globe.

Established in 1983 in Ranchi the capital city of Jharkhand SNL was promoted by then the Shriram group of Industries in technical collaboration with INA Germany. By virtue of being associated with INA, SNL got the opportunity to have one of the finest Technologies in the world in Needle Bearing manufacturing. SNL became associated with India’s most progressive business group in the field in the year 2000 when NRB Bearings Limited took over the management of the unit. Combination of different technologies that is simply world class SNL can rightfully boast of technologically ahead of many in the business. SNL has a capability of manufacturing it’s own special purpose machines required for Bearing manufacturing. The ability to design and develop Low cost Automation would surely be the pride of many in the business it self. This gives SNL to become the most cost-effective manufacturer of the products. SNL becomes a unique and perfect industry that manufactures its machines for its products and designs and develops all sorts of low cost automation that add to its productivity significantly. A team of very talented and innovative people inclined to develop cost effective machines and processes always working towards the customers benefit.

So indirectly its future heavily depends on NRBs growth prospects.

SNL has stable Gross profit and EBITDA margins. It couples with good working capital management (might be due to high intercompany transactions). These all leads to Positive operating cash flows (OCF) in all historical years.

As they able to generate decent OCF, They regular redeeming its 11% redeemable preference share capital. That’s lead to declining in total share capital. > Its Equity share capital has not changes from past few years.

Preference shares are hold by NRB limited. As on March 2015, only 50 lakhs remain which was 800 lakhs in the year 2011.

Appreciate your efforts for starting a new thread.

But, it would be more fruitful, if in future, our own research is also posted while starting a thread, rather than copy-paste material from the company’s website.

These efforts would never go in vain.

I had studied this company recently. The low P/E, with good ROCE & other financials had brought this up on the customised screener.

As rightly pointed out by Jinesh, SNL is a subsidiary company of NRB Bearrings. NRB has a bigger business, & is reputed brand.

What we need to find out is :

the reason why SNL was started, when product profile of both NRB & SNL are the same.

there is a majority of sales revenue to parent NRB. So, both the seller & buyer being the same., the product price & hence the margin can be managed to suit both or either of them.

The management credentials seem to be fine., as I couldn’t find anything against it on the net.

The ARs provide very little information about the future growth prospects.

All in all, it is a purely value buy., but with future growth prospects limited / unknown.

There is a need to dig more into it., to have a good understanding of the business.

@mukesh_gt : SNL was originally a Ranchi-based listed Shriram Group company, acquired by NRB in June 2001. I would guess that the reason NRB never delisted the company was that the cost of delisting was too high and cumbersome. The unanswered question is why would they not merge SNL into NRB? And if merger is the right step for NRB why have they not done so all these years. Given that analysts look at NRB on a consol basis, the minority interest in SNL is so small that it hardly moves the needle (pun intended) for NRB.

Strange that SNL has half the valuation multiple of NRB despite having significantly better RoE and margins.

Discl: Have a tracking position; given the very thin trading volumes building a meaningful position is going to be very difficult. And exiting will be even more difficult.

The reduction in the share capital is due to the payment of preference shares. The preference shares have reduced from 8 Cr in March 2011 to just Rs 50 Lacs in March 2015

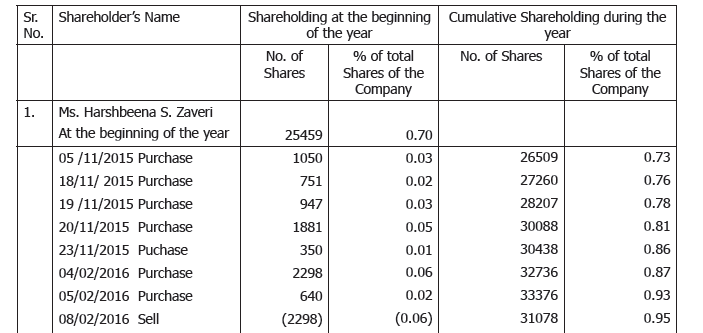

Ms Zaveri bought some shares on 4/2/16 and sold on 8/2/16. Dont think any business fundamentals changed in 4 days. Just a concern for me, since I don’t prefer promoters engaging in trading activities of their own shares.

The total Indian bearings market is estimated at Rs. 8,000-8,500 crore of which Ball bearings constitute 48% and Roller bearings constitute 52%. Needle bearings form 9-10% of the Roller bearings market. Hence ~Rs. 450 crore.

Source: Industry, Timken India QIP RHP, ICICIdirect.com Research

Board also approved payment of dividend of Rs. 5/- per Equity Shares.

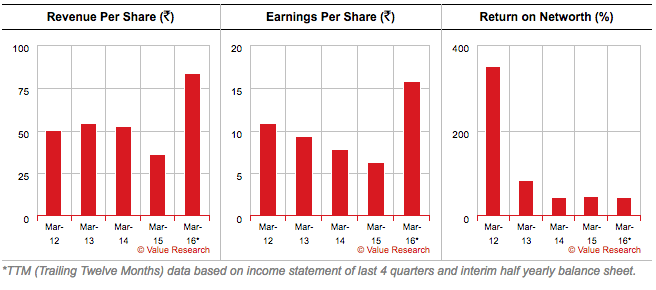

It was not a good year for auto sector, still it maintained decent rev/profit. In better time, it would post steller result. Valuation is very reasonable for this 100 cr mcap company. Stable stock to have in pf. Long way to go.