Anyone tracking Ameya Precision Tools? It was massively oversubscribed during the IPO. Recetnly touched all time lows when promoter did some good buying. Hard to find much info about it.

Thank you for sharing. Margins have improved slightly and debt is reduced a bit. However, It is interesting to know why the company is not coordinating with a rating agency, based on the rating given by CRISIL, investors, lenders, and all other market participants should exercise due caution while using the rating assigned/ reviewed with the suffix ‘ISSUER NOT COOPERATING’.

Ratings are required by a company only when they need debt. The rating agencies charge a fee. I think if the company does not wish to raise debt, the advisable course of action is to save that unnecessary cost.

4 Likes

cfo is negative as the receivables are extremely high, i think they maybe trying to get new clients and it order to capture them they will be providing extra credit period (assumption), what should be tracked here is are there write offs.

debt is all short term, to fund the working capital, no idea on why the interest is so low, will deep dive soon.

so the plan would be to sweat the current assets first, as you can see how the revenues have grown without adding any new capacity, maybe more is left (maybe). also they would first want to get a bit of cash flow rather than just going further deep into debt.

all of these are assumption, thats what i am thinking, we need to give some breathing space and time to the management after they have already bettered the company so much. atleast we know they can execute.

1 Like

so just an honest question, when you know that IBC may capture/ take away market share from GCL. whats the reason for buying it. as the market will not grow now. and also as IBC is more efficient and effective>?

1 Like

Thank you, Rinku, for your input. Appreciate!

I have a few observations about this company as a part of the Thesis (It does not give buy or sell recommendations though)

- Increasing Receivables>Increasing sales - did not pass

- Miscellaneous Expenses > Volatile and high in the recent past.

- Contingent Liability is 4.23 Cr. For FY2010-11 VAT

- As per the Auditor, “according to the information and explanations given to us, following are the disputes”

-

Dispute Amount - Income-tax Act, 1961, 1944 - 1.03Cr (Amount) - dispute pending at Jurisdictional A.O Vadodara Gujarat .

-VAT- 4.23Cr (Amount) - dispute pending at VAT Tribunal, Ahmedabad.

1 Like

Appreciate your views!

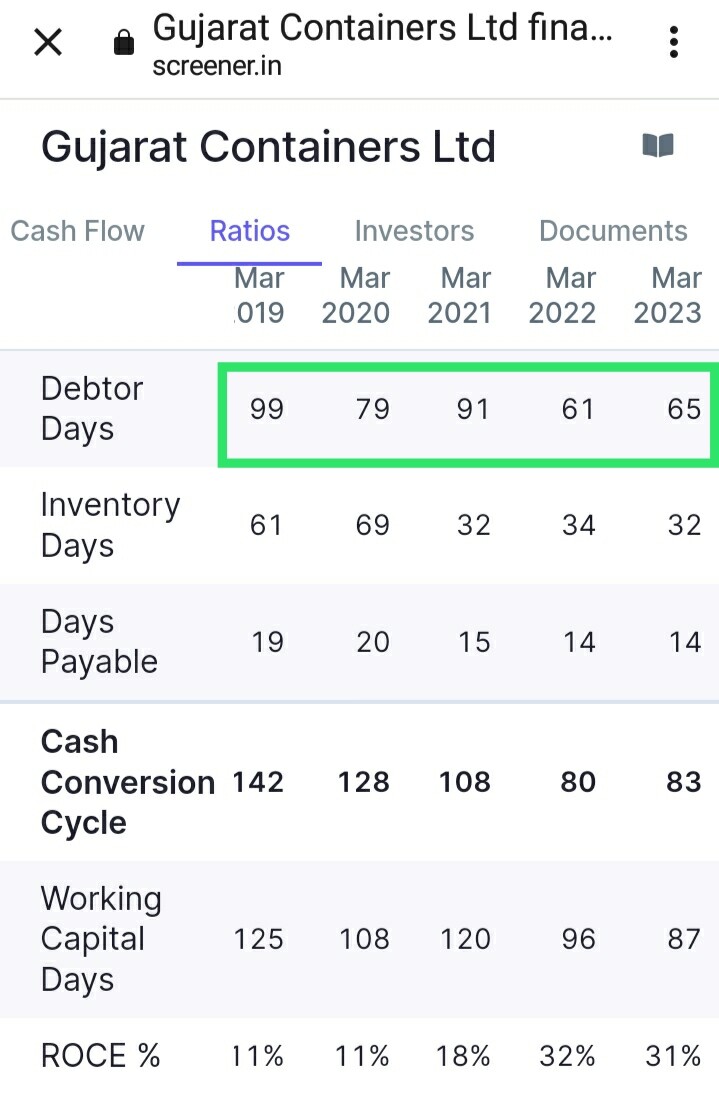

Here we can see Debtors day are continuously improving

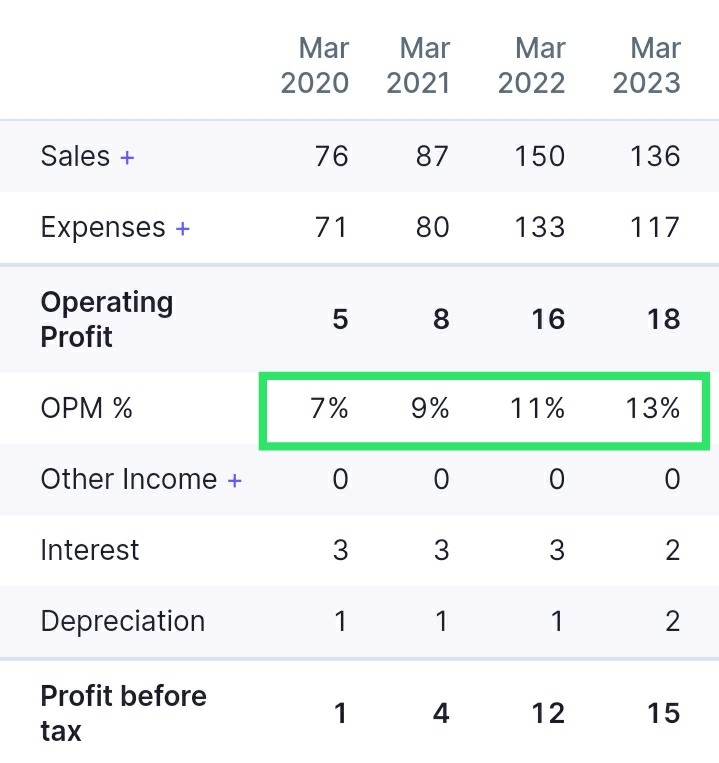

But EBITDA margin is continuously increasing

These type of contingent liabilities and disputes are common in almost all the manufacturing companies.

3 Likes

Thank you again, Rinku. About increase in margin was the first observation from my side when I looked at it.

Even if the contingent liability is below 15% of the last year’s PAT, I will still ignore but it is more than that plus zero cash flow. It does not mean that company can not do well in the future. I will personally avoid such a company but anyone who has a risk appetite can take a position with a solid exit strategy and certain allocation as a satellite portfolio. Appreciate all your view and it is always pleasure to learn from each other!

1 Like

As one of the competitor, TPL Plastec Ltd. has already commenced production of IBC in addition to BARRELS. I think, going forward, GCL may also set up IBC manufacturing unit.

So why study GCL when we know a listed player in the product which will be take over the market share.

And how do we know gcl will set up this unit, there must be some entry barrier right, if gcl is planning to enter it

Lykis promoters further sold as per today’s disclosures to exchanges. Not sure why the promoters are dumping in the open market? Any clues?

1 Like

I think there is no direct competition between GCL and TPL Plastech, as GCL currently makes only steel drums and composite drums while TPL Plastech makes only plastic drums and plastic IBC. Both steel drums and plastic drums/IBC have their own benefits and limitations. Some industry prefers steel drums and some prefer plastic drums. The demand of drums will remain for decades whether it is made from metal or plastic. TPL Plastech is specialist in making plastic drums, so it commences making plastic IBC because of increasing demand. While GCL is specialist in making steel drums, GCL can make Steel IBC, as IBC can also be made from steel.

I chose to invest in GCL because of better financial parameters in comparison to TPL Plastech like ROCE, ROE, Interest coverage ratio, Fixed assets to Turnover ratio, Stock Turnover ratio, cagr growth in sales/ net profit in last 10 year/ 5 year/3 year etc.alongwith cheap valuations.

1 Like

Did you find anything about Mitsu?

Since most of microcap counters hunt start with exchange notifications, I will use this thread to post some of the names I am tracking/buying. Viewers can do their own due diligence.

Scripname: Sparc Electrex

BSE Scripcode: 531370

Company Update on Trademark License Agreement with Hyundai Corporation Holdings Co., Ltd, Korea

7 Likes

Hi @somu0915

It would be nice if you can mention why you are tracking/buying while posting the company names

Thanks

1 Like

Most of these names will be under 100cr market cap and at this stage not much info is there and one needs to take a gut/instinct based position if one wants to.

For example, RACL geartech 5 years back was a 50Cr market cap company I invested and it had less info, only knew that it had collaboration with kubota, bmw. Today it is a 1200Cr company.

That was enough to take a small position. As time goes by, one needs to continously monitor events happening in the company.

In above example, Sparc has done good by having an exclusive trademark license agreement with Hyundai Corporation.

One needs to see how they capitalize on it, whether they can show increased revenue/profits due to this engagement.

In micro cap, its a dark tunnel with very faint light at end of tunnel, as one crosses it, the light is more visible.

24 Likes

so do you track and check financials when screening for new counters, or you just play the story. and how flexible are you in terms of these financials, also are you just betting on these counters based on these small rays of sunshine or you for something particular.

curious to know about your process

thanks

2 Likes

Any member update how come lykis huge debt paid interest low

He has bought the majority stake at 20/share and sold only ~1.5% at 120/share.

The timing of the sell is coinciding with ESM framework and his 50th Birthday celebration.

Company’s financial looks very promising the fall is fully dedicated to promoter selling.

however i checked with Company sec and the response i got is nothing off.

my sense is to hold till the Q1 numbers and then take a informed decision.

do not sell in panic , if promoter selling was not there this was best time to add.

But now its better to wait till result or let the stock settle.

4 Likes

Lykis case is quite different. Usually when there is such distress selling happens for a small cap at lower circuit, there wont be any buyers. Here 2Lakh + shares traded at LC or just around it.

Not sure why promoter keeps selling instead if he avoided that the prices would have been almost double of what it is today.

Anyone know where its facilities are located and how many employees work there?