GNG Electronics: The Scarcity Play in an AI-Driven World

25/01/2026

1. Overview

GNG Electronics has positioned itself as a significant player in the global circular economy, specifically within the Information and Communication Technology (ICT) refurbishment sector. The company creates value by procuring used laptops, desktops, and other ICT devices, refurbishing them to “enterprise-grade” standards, and selling them across 38+ countries.

Key Investment Thesis:

-

Scalability in a Niche: They operate in a fragmented market but have established an industrial-scale operation (5 facilities, ~1,200 employees) that is hard to replicate.

-

AI & Tech Tailwinds: Management is aggressively positioning the company to benefit from the “AI adoption wave” by supplying affordable, high-performance hardware required for AI processing.

-

ESG Alignment: The business model is inherently ESG-compliant, appealing to global corporations with strict sustainability mandates.

2. Company Profile & Business Model

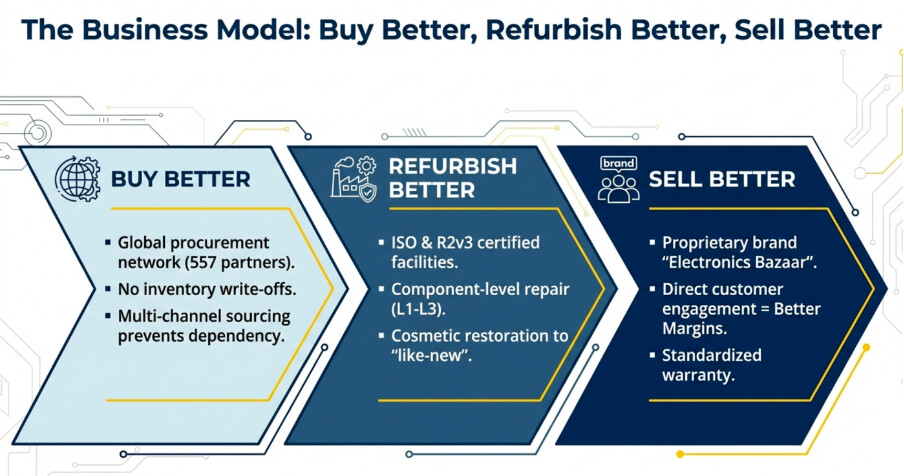

GNG Electronics follows a “repair-over-replacement” philosophy, positioning itself at the intersection of affordable technology and environmental sustainability.

-

Integrated Value Chain: The company manages the entire lifecycle of refurbished ICT devices, including global sourcing, specialized L1-L3 refurbishment (including motherboard and LCD repairs), multi-channel sales, and after-sales support with 1–3 year warranties.

-

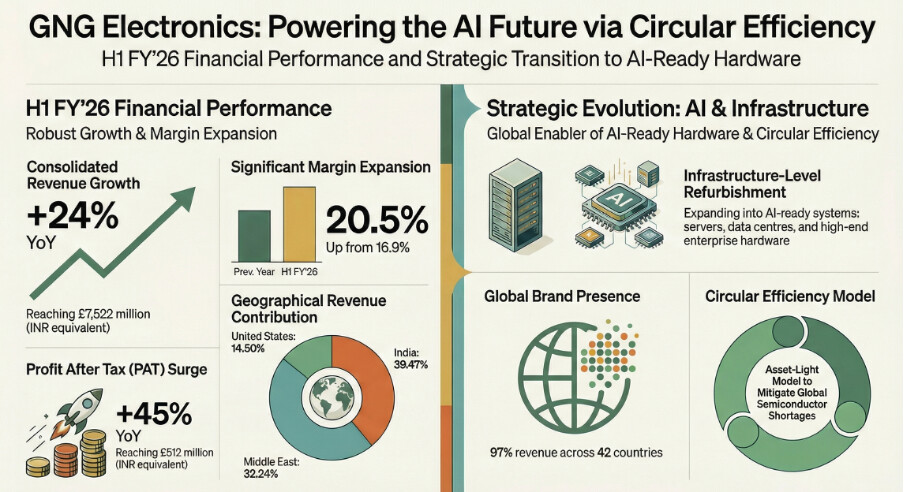

Brand Dominance: The “Electronics Bazaar” brand contributes 97% of total revenue, backed by strong online visibility and a network of 4,154 touchpoints globally.

-

Strategic Partnerships: GNG is a Microsoft Authorized Refurbisher and a certified partner for HP and Lenovo. It serves as a critical IT asset disposal (ITAD) partner for major corporates, including India’s second-largest software company.

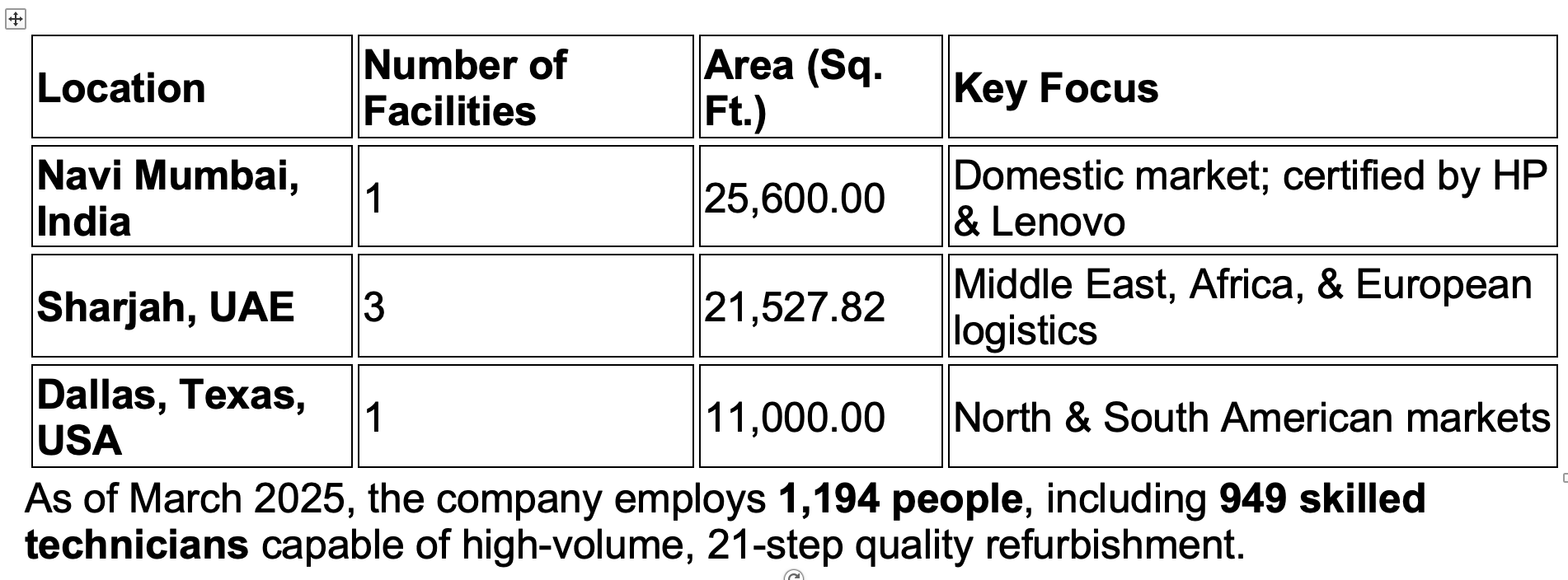

3. Operational Infrastructure

The company’s global footprint allows it to mitigate regional risks and access approximately 70% of global GDP.

4. Financial Performance Analysis

GNG Electronics has demonstrated robust top-line and bottom-line growth in the first half of FY26, driven by expanding margins and geographic reach.

Revenue Growth

-

Q2 FY26 Revenue: ₹439.9 Cr, up 24.7% YoY and 41% QoQ.

-

Drivers: The growth is attributed to higher throughput, strong institutional demand, and expansion in international markets, particularly the Middle East and the US.

-

Seasonality: The sharp sequential jump from Q1 (₹312 Cr) to Q2 (₹440 Cr) suggests strong momentum or seasonality favouring the second quarte

-

Profitability & Margins

-

Gross Margins: Expanded significantly to 20.5% in H1 FY26 from 16.9% in H1 FY25. This indicates better sourcing capabilities or a shift to higher-value products (like AI-ready laptops).

-

EBITDA Margins: Stood at 10.9% for H1 FY26, an improvement of ~47 basis points YoY. Management attributes this to operating leverage—revenue growing faster than fixed costs.

-

PAT Growth: Profit After Tax grew 45% YoY in H1, with margins improving to 6.8%. The company is successfully converting top-line growth into bottom-line returns, aided by a relatively asset-light model.

5. Working Capital Analysis

This is the most critical area for an investor to monitor, as the refurbishment business is working-capital intensive.

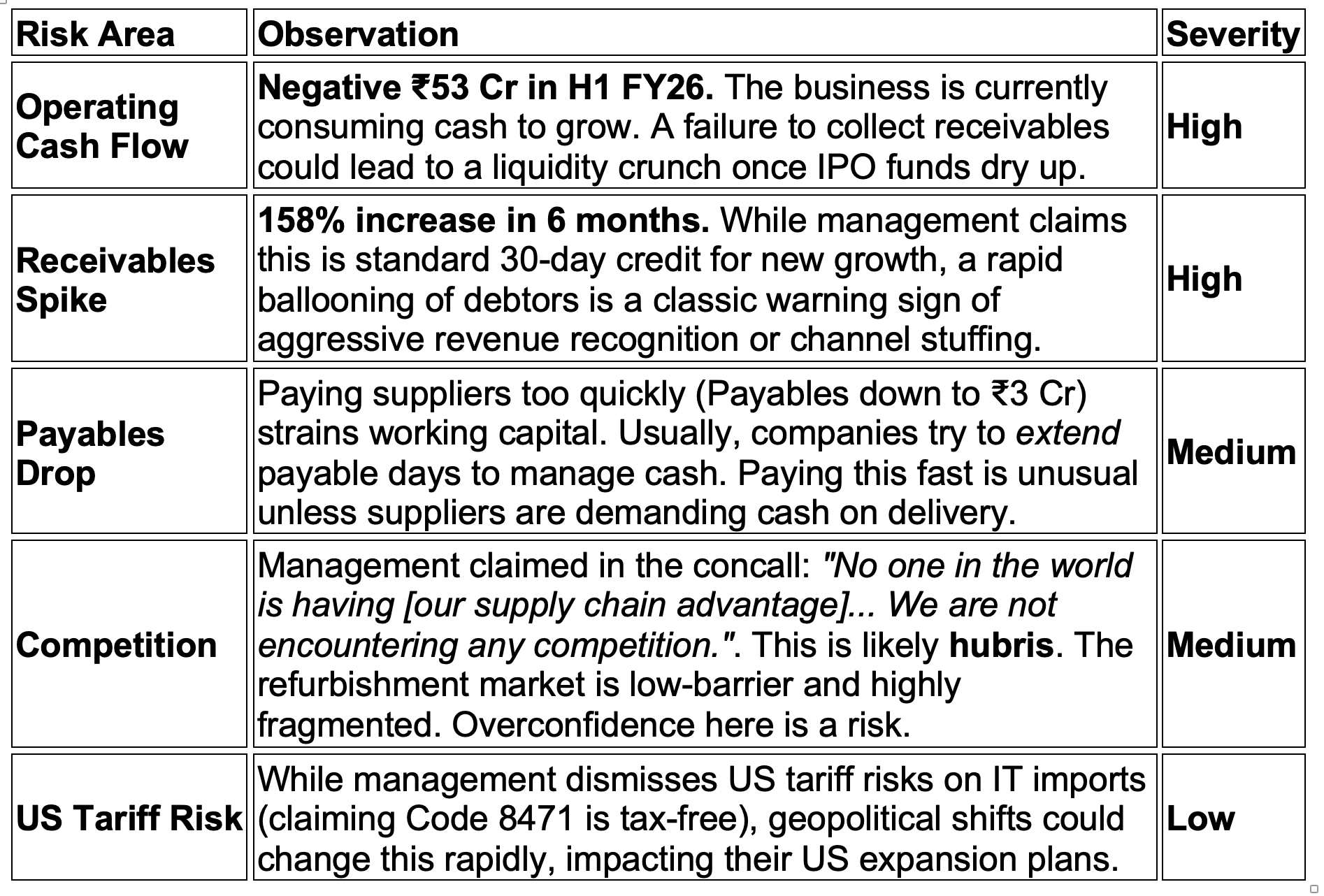

A. Trade Receivables (Red flag?)

There has been a sharp increase in trade receivables, which requires close monitoring.

-

The Jump: Receivables increased from ₹67.6 Cr in March 2025 to ₹174.8 Cr in September 2025. This is a ~158% increase in just six months, while revenue grew by ~24%.

-

Management Explanation: In the Q2 concall, the CFO explained that they need to support channel partners with credit to penetrate new markets. They claim the credit period is standard (30-35 days) and have “no history of bad debts”.

-

Investor View: The growth in receivables is outpacing revenue growth. If receivables are ₹175 Cr on Q2 revenue of ₹440 Cr, the Days Sales Outstanding (DSO) is roughly 36 days, which aligns with management’s claim. However, the absolute rise locks up significant cash.

B. Inventory Management

-

Current Levels: Inventory stands at ₹414.7 Cr (Sept '25), down slightly from ₹486.6 Cr (Mar '25).

-

Quality of Inventory: Management explicitly stated in the Q2 concall that they hold no inventory older than one year. This reduces the risk of obsolescence, which is a major risk in the tech hardware sector.

-

Turnover: The reduction in inventory despite rising sales indicates improved inventory turnover and efficiency in the “procure-refurbish-sell” cycle.

C. Trade Payables

-

Sharp Decrease: Trade payables dropped drastically from ₹26.7 Cr (Mar '25) to just ₹3.1 Cr (Sept '25).

-

Implication: The company is paying its suppliers much faster. While this builds trust with suppliers (crucial for sourcing high-quality used devices), it puts further strain on operating cash flow.

Working Capital Conclusion: The company is currently “funding” growth by offering credit to customers and paying suppliers quickly. This is a cash-intensive strategy.

6. Cash Flow Analysis

The Cash Flow Statement reveals a divergence between reported profits (PAT) and actual cash generated from operations.

A. Operating Cash Flow (OCF) - NEGATIVE

-

Reported OCF: For H1 FY26, the Net Cash Flow generated from/(used in) operating activities was negative ₹(53.1) Cr.

-

Reason: Despite a Profit Before Tax of ₹58.6 Cr, the cash was consumed by:

-

Inventories: ₹71.8 Cr released (positive).

-

Receivables: ₹(107) Cr outflow (increase in debtors).

-

Payables: ₹(45) Cr outflow (decrease in creditors).

-

-

Investor Note: The company is burning cash at the operating level to fuel growth. This is sustainable only as long as they have access to external capital (equity/debt).

B. Investing Cash Flow

-

Net Cash Used: ₹(98.5) Cr.

-

Major Outflow: Primarily driven by an “Investment in Subsidiary” or similar financial assets (₹100 Cr outflow noted in standalone cash flow), likely related to expanding global operations or managing liquidity. CapEx on property/plant remains low (asset-light model).

C. Financing Cash Flow

-

Net Cash Generated: ₹307.3 Cr.

-

IPO Impact: The massive inflow came from the IPO proceeds (~₹400 Cr).

-

Debt Repayment: The company used IPO funds to repay significant long-term and short-term borrowings, reducing the debt burden.

Liquidity Position: Thanks to the IPO, the company ended Sept '25 with a healthy cash balance of ₹156.6 Cr. However, this cash buffer relies on financing activities, not operational cash generation.

7. Future Prospects & Growth Strategy

Management outlined a clear roadmap for future growth in their presentations and conference call.

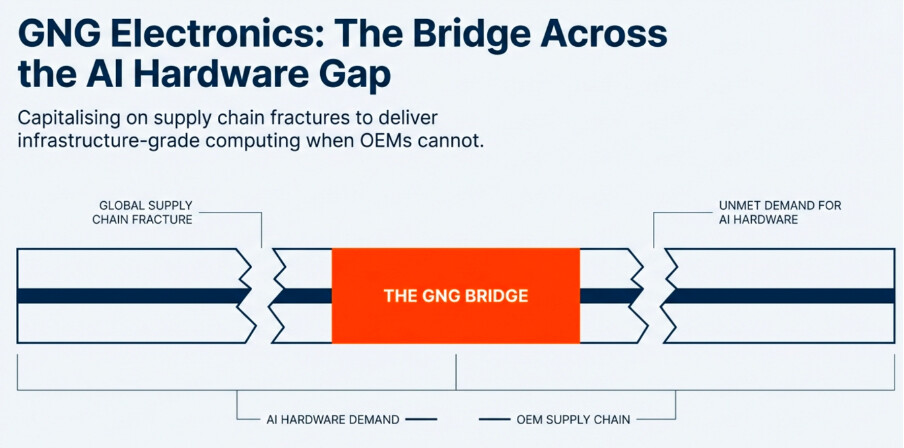

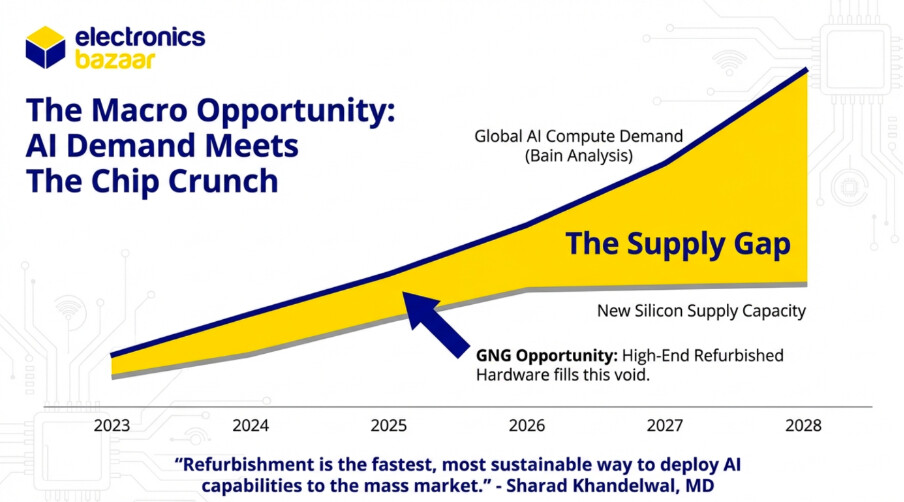

A. The “AI” Tail wind

-

Strategy: Management is heavily marketing the need for “AI-ready” hardware. They argue that the AI boom creates a shortage of new chips, pushing enterprises to buy high-end refurbished laptops that can handle AI workloads at a lower cost.

-

Potential: If they can position refurbished devices as viable alternatives for edge-AI computing, this opens a premium market segment.

B. Geographic Expansion

-

New Markets: Operations have expanded to Dallas, Texas (USA) and increased capacity in Sharjah (UAE). They are targeting sales in 42 countries.

-

Direct-to-Consumer (Brand Building): They are shifting focus to their own brand “Electronics Bazaar” rather than just being a backend refurbisher. This is intended to capture higher margins and customer loyalty.

C. ESG & Circular Economy

-

Regulatory Support: Governments (like France and Ireland) are mandating that a % of IT procurement must be refurbished.

-

Corporate Targets: GNG enables large corporations to meet their sustainability goals (Scope 3 emissions) by disposing of old IT assets responsibly and buying refurbished units.

-

Governance: Led by Managing Director Sharad Khandelwal (29 years of ICT experience) and a board including former Dell executive Amit Midha, who has 4.25% holding in the company.

-

D. Guidance

- Targets: Management has guided for 20-25% top-line growth for FY26 and a 75 bps margin improvement. They maintained this guidance in the Q2 call, citing a conservative approach.

8. Red Flags & Risk Assessment

One must weigh the growth potential against these specific risks identified in the documents.

-

9. Conclusion

GNG Electronics is a high-growth company in a “sunshine sector” (Circular Economy/Refurbishment). The reported P&L numbers are excellent, showing strong demand and improving margins. The IPO has successfully deleveraged the balance sheet and provided a cash buffer.

However, the quality of earnings is currently low due to poor cash conversion. The divergence between PAT (Profit) and OCF (Operating Cash Flow) is the primary concern. The growth is being funded by an expanding working capital cycle (higher receivables, lower payables).

Probable Scenarios:

-

Bull Case: If the receivables are collected on time (turning into cash in Q3/Q4) and the AI/ESG thesis plays out, the stock could see significant upside as margins expand and OCF turns positive.

-

Bear Case: If the receivables turn out to be sticky or bad debts, the company will burn through its IPO cash quickly. The negative OCF is sustainable only for a short period.

One should monitor Cash Flow from Operations and Receivable Days closely in the next results. Positive OCF is the confirmation signal needed for a long-term investment.

================================================================

Management Commentary from Q2 Concall transcript:

-

First full quarter as a listed company; management framed the business as evolving “from being a fast-growing refurbisher to become a technology enabler” positioned at the intersection of AI-driven compute demand + supply constraints + circular economy.

-

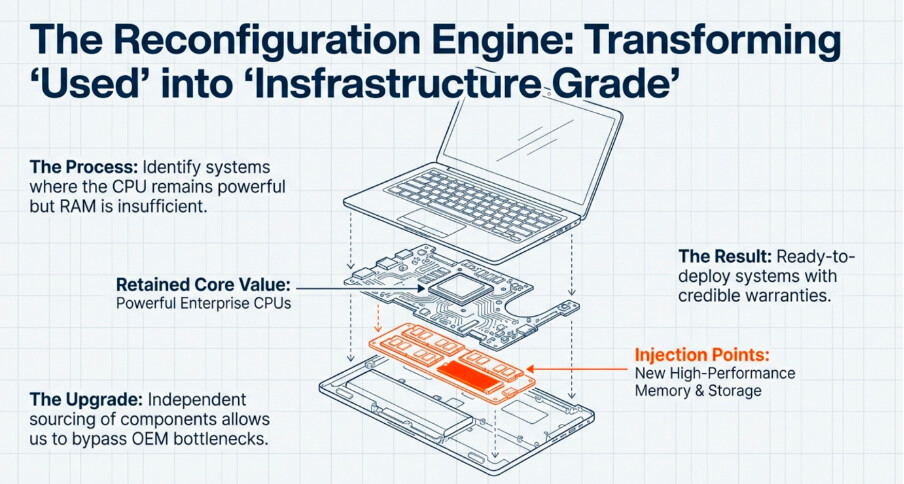

Strategic expansion beyond laptops into “infrastructure level refurbishment”(servers, storage, high-end desktops) to address AI-driven enterprise workloads—explicitly called a “natural progression” and a key new vector.

-

Material deleveraging post-IPO and expected H2 interest savings, but continued reliance on working-capital debt as the model scales.

Cost commentary (why EBITDA didn’t expand as much as gross margin):

-

Management attributed EBITDA leverage being partly absorbed by front-loaded investments: “a lot of investments… in terms of talent and people,” headcount up meaningfully (details below).

-

Other expenses up due to “logistics cost, marketing and travel and hiring costs,” including hiring across Middle East, U.S., and India.

Volumes and mix:

-

H1 units: ~302,000.

-

Revenue mix: ~80% laptops / 20% other devices (value), shifting from 75/25 in the prior comparable period—implying higher laptop contribution and realization.

-

Unit mix: 72% laptops / 28% other.

Average selling price (ASP) improvement:

-

India laptop ASP: ~Rs. 26,800 (from ~Rs. 25,800).

-

International laptop ASP: ~Rs. 28,500(from ~Rs. 27,500).

-

Non-laptop ASPs also up “~2% to 3%” overall.

Capacity:

-

Current global refurbishment capacity stated as “north of 120,000 units a month.”

-

Management indicated the mix is moving toward enterprise-grade systems needing “more space because of enterprise-grade computers and servers.”

Industry and demand outlook: AI + supply constraints + circular economy:

AI-led compute demand

-

Management repeatedly asserted AI is driving a cycle toward high-end processors/memory/SSD, describing laptops as “the engines of AI productivity.”

-

Demand tailwind articulated as a need for “AI-ready systems at a fraction of original cost” with credible warranty.

Supply constraints

- Cited “global semiconductor shortages… AI chip crunch” and argued their refurbishment model can deliver performance “without depending on new chip production cycles.”

New, newsworthy strategic initiative: infrastructure-level refurbishment + footprint expansion:

-

-

Clear strategic escalation: “beginning of our entry into infrastructure level refurbishment… deliver AI-ready computing systems, server storages, and high-end desktops… for global enterprises.”

-

Facility/space actions: management said it has “preemptively secured long-term spaces across India (Mumbai), UAE, and the United States” intended as “high-capacity refurbishment and testing centers” including “servers, data centers, hardware.”

-

Capex framing: described as aligned to an “asset-light model,” “not requiring heavy Capex.”

IPO Details:

================================================================Compiled Notes from here & there, No Buy/Sell Recommendation

================================================================

-