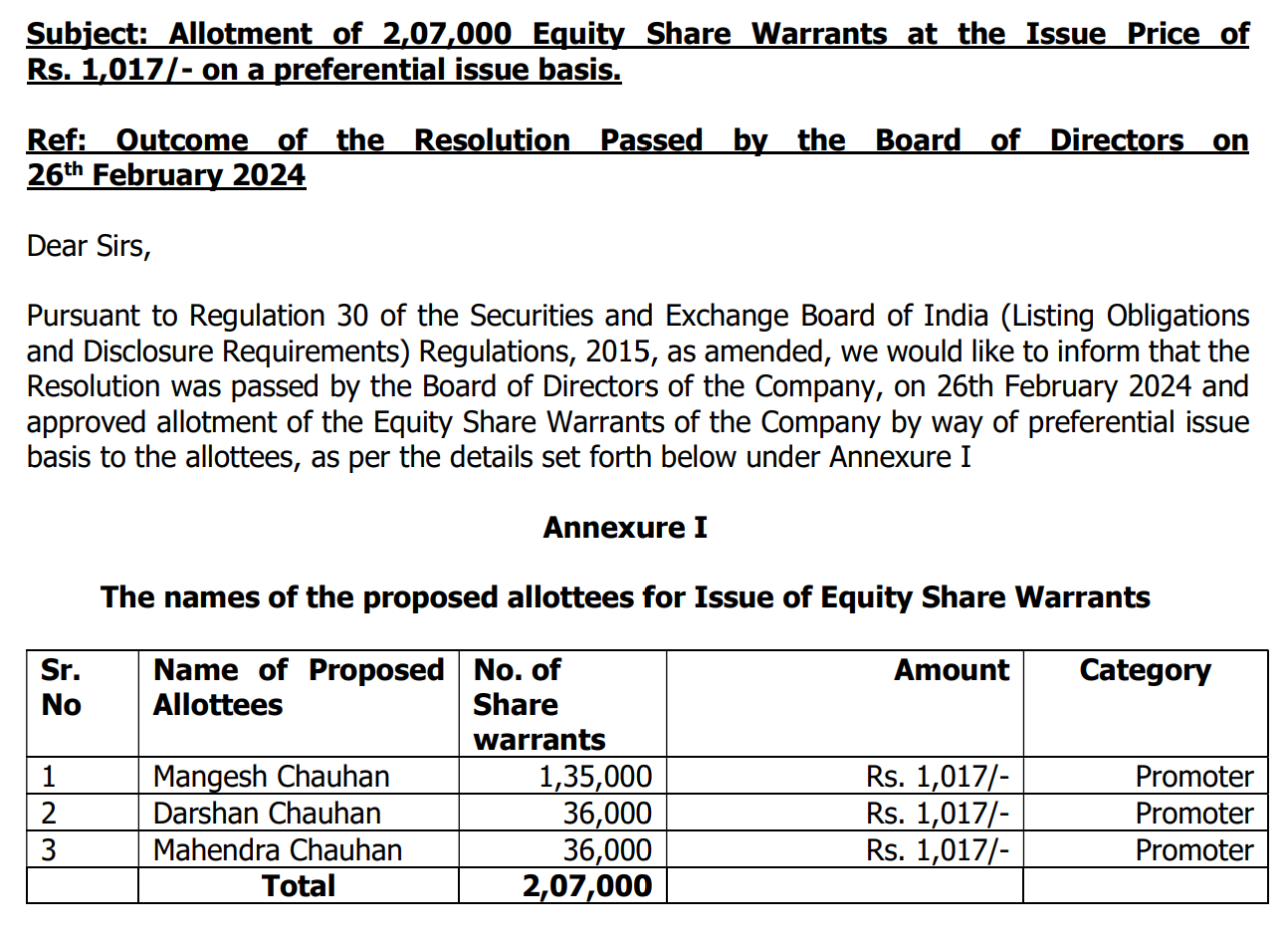

Promoters to be issued 2,07,000 Warrants convertible into Equity Shares on a preferential basis at a Price of Rs 1017 per Warrant.

44359456-1ce5-4c0f-b223-024b28c2fb86.pdf (317.3 KB)

Promoters to be issued 2,07,000 Warrants convertible into Equity Shares on a preferential basis at a Price of Rs 1017 per Warrant.

44359456-1ce5-4c0f-b223-024b28c2fb86.pdf (317.3 KB)

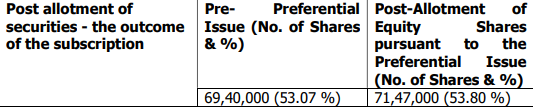

unable to understand this ,promoters issued 1.5% extra shares (2/132.8)but stake only increased by 0.61% ? Can anyone explain?

1.5% on total basis, only promoter stake increased by .61%, check below table of promoter stake pre and post issue.

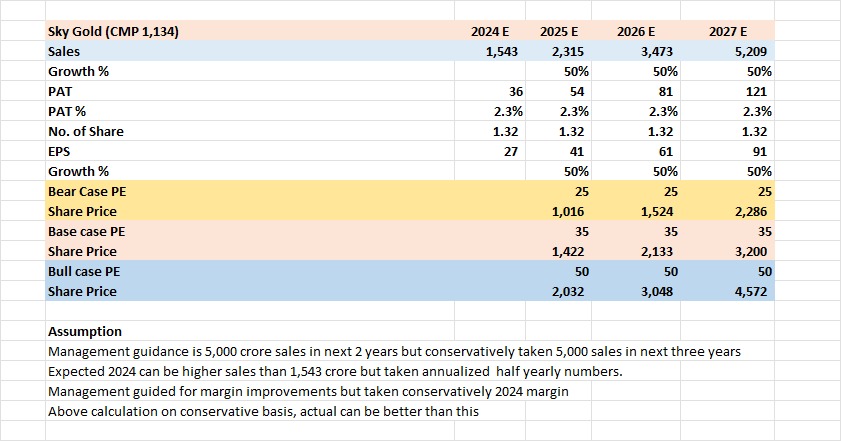

Next 12 month expectations of 3000cr rev and after that 5000cr rev expectations

Current export revenue 3% ,targeting this to be 30% of revenue , also export is a higher margin business

Current pat margins at 2.5%-3% ,targeting this to be around 3.5%-4%.

Pref shares currently to be used for working capital , debt repayment can be easily done after few years.

Cost of debt at 9%, will be reduced to 3% soon.

Wc cycle from 60 to 45 days expected soon.

Roe targeting to be 25%-30% from 20%.

Superb Q3FY24 results.

-Sales up 72% YoY.

-EBITDA up 48% YoY.

-PAT up 40% YoY.

-EPS growth of 15% YoY.

EPS growth lower than PAT growth due to issue of new shares in Q3FY24.

Management Commentry on Results:

New facility has become operational in August 2023 which has a capacity of producing 750 - 800 kg per month and currently have achieved 60% capacity utilization.

Intend to grow revenue at 30% CAGR for upcoming years.

Want to expand product portfolio - doubling from current 3000 offerings to about 7000 per month by introducing new metals such as white gold, platinum and studded jewellery as well as foraying in new segments like mangalsutra, chains, antique bridal jewelleries etc.

Want to expand footprint beyond the domestic market to have meaningful export contribution from markets of SEA, MEA and USA.

Plan to double headcount of our inhouse design team from 100 to ~200-250.

The company also plans to add around 30,000 moulds every year. Moulds are used in the casting process of manufacturing jewellery.

In my view, their 30% growth guidance is for topline and not the bottom line. With operating leverage and operational efficiency steps, margin should grow at a faster pace.

One blip wrt earlier guidance - Earlier they were talking of 5k cr revenue in FY26 and now in FY27. Realistically it may happen in FY28 (with 30% CAGR).

Disclaimer: Invested

Thanks for correcting me.

I went through the concall. The guidance is to reach 5000cr revenue by 2027 so that implies a CAGR of 41% or so. Apart from this PAT margins will expand on top of it. Triggers are reduced gold losses via ERP implementation, switching new customers to higher margin designs after first order, constant fixed costs.

They will also switch the current 160 cr loan which is around 9% to gold loan at 4.5%. This would have negligibe effect I think, because they also plan to increase the loan amount to 240 crs or so.

Overall I agree that 40% cagr target is ambititous and execution is important. Stock has a lot of upside left if they walk the talk.

Another preferential issue at ~1000.

Surprising, in the recent concall they indicated that any further preferential allotment would not be required anytime soon.

This is the not new one. It’s all ready noticed on 16 jan and approved on 8 Feb at price of 1017.

Oh is that so? The filing came yesterday. In that case, the concall is consistent with no more dilutions. Thanks for pointing this out.

Company looks good fundamentally with a strong growth trajectory. Need to see if management walks the talk and meets the guidance of 5000 Cr revenue with 3% margin by FY27 or not. Considering the working capital requirement for 5000 Cr revenue will weight down on the margins by increasing the interest cost or we will see equity dilution

But the preferential issue done at a significant discount to the share price at that time is concerning and then another preferential warrants issue within a month (although close to the current price this time) raises some doubts on the company.

Disc: Tracking position

This is the old one or a completely new one?

It is a completely new issue, I guess you are talking about the one which closed on 7th December and that was at a price of 425/share.

This is a good article that explains the Promoter warrants issue risks - Stock Warrants to Promoters: How to Analyse - Dr Vijay Malik

We can read it considering the recent promoter warrants issued by Sky gold when they clearly had other ways of funding the working capital and only 25% of capital will be received in the books immediately and for rest 75% promoters will have 18 months.

Not a buy or sell recommendation. Disc: Bought in the last 30 days

Here is my thesis

Thesis

About the business

Sky gold is a B2B business that manufactures designs for jewellery retailers like Malabar, Kalyan etc.It is a proxy to the gold jewellery and is mainly catering to the domestic market, however they are in talks to produce for retailers in Malaysia and some gulf countries as well.

Revenue growth

The company produced around 250-300 kgs per month of gold jewellery before the factory, but they have recently moved to a much bigger facility which should produce around 700-800 kgs per month. The company, according to the guidance of the promoters, should reach 5000 crores by FY26, which basically means the business starts functioning at full capacity.

Honestly, I found that number too stretched, however found data point where organised manufacturing only has a 15% market share, which is quite less compared to organised retail and hence this will need to catch up to the organised market share of the retail jewellers. Yet, i did not want to aggressive and have used a 35% growth from FY25( 35% seems big but knowing the story and plans in place by the company, it might just happen)

Ebitda

Since it’s down the value chain, we can’t expect them to have Operating margins of retail businesses we have studied. Due to the fact that they are expanding almost 4x, The company believes a 5%+ margin is possible. However, due to the nature of the business and the fact that competition is only going to get tougher, I am assuming a 4.5% margin which is what they have been doing for the past few quarters

Depreciation and Interest costs

The capex required isn’t much and hence depreciation too won’t be very significant. The interest costs should rise, however not as much as the revenue growth because of a number of measures regarding their contracts with customers, starting the use of Gold metal loan, reducing working capital days and not holding gold bullion inventory by just taking them from customers.

Possible antithesis

• Concentrated customers: top 10 make 70% of their revenue and hence any potential loss of customers could be a big blow. However, they are very close to signing Tanishq and hence it could be negated

• The business has a negative CFO at the moment, however it is mainly due to the working capital pressure which came from the aggressive growth, the promoters said that they should be cash flow positive due to the transition being complete and the measures being taken to reduce working capital. However, I would still wanna observe and see how this aspect turns out.

• The data found is extremely limited, and hence the corporate governance could be questionable.

• Valuations: Even though the growth promised is really good, I would want to wait for at least a 10%-15% correction to increase the margin of Safety.( we got this correction in the recent fall)

Why do you say so? Can you explain more?