it is crazy. It has run up from Rs 30 to Rs 80 within 6 weeks. But OFS at 16% discount to market price is not a good news for retail investors.

The promoters perhaps have realised that the current price Rs 80 is not worth it. It is a lesson for all of us that we should be cautious in chasing such high flying stocks , where promoter holding is very high

As per Norms , promoters can not have more than 75% stake and promoters wound like to take this opportunity in off loading. Govt hungry for money …needs money to spend.

Anyway, Order win gives future earning visibility… So, if you are long term investor , we need not worry. Fundamentally, Renewable stocks are going to be on demand due to thrust on renewable energy. Though these stocks carry PSU tag, but these PSU’s are leading from front by huge capex plan on Renewable energy.

Discl: bought Rs @33 and I may be biased.

It is not a buy or sell recommendation. please apply due diligence before buying

Yesterday’s OFS for Non-retail portion saw High demand for this stock from the MF’s and HNI’s. Today, it is open for retail investors. But now the price is fallen very near to the floor price and one can buy from open market aswell if one is interested to buy rather than buying from OFS.

MF’s seem to be entering in a big way in to PSU stocks especially Defence , railway , & renewable - could be good for long term retail investors , since MF SIP’s gradually could be an enabler for rise in shre price over a period of time.

However , retail investors should be cautious about OFS for stocks with high promoter holding. though for long term investors , it may be a temporary blip since most of these companies have clear earning visibility for next 4-5-6-7 years , though you may not see a sequential growth QOQ , because of long tenure for execution of the orders and the only key risk is timely execution of orders apart from change in Govt policy which may affect minority share holders interest

OFS of PSU’s is a strategic divestment plan by the Govt and there are still 21 PSU’s with promoter stake more than 75% and it is difficult to predict which PSU is next on pipeline for OFS. They just declare in the evening and next day is the OFS.

Discl: Not a sell buy recommendation I have investments in above named PSU’s and hence may be biased. Pl do your own assessment

Om…what are the news in SJVN story ?..

are they into solar EPC also , do they have their own solar plant?

how much is total installed capacity of SJVN ?..sorry if i am asking for repeat details and are already mentioned on this thread, the installed capacity may be different then in the past !

If they are into anything related to solar, to my understanding sjvn still has lots of steam left !

D-Tracking, Plan to invest.

The Company successfully bagged 100 MW Solar Project @ ₹2.54/Unit on Build Own and

Operate basis through a tariff based competitive bidding process of GUVNL Phase XXISJVN Green Energy Limited (“SGEL”) at a tentative cost of ₹550 crores.

Current Hydro + Solar Capacity: 59,87 MW.

Anticipated 12,000 MW by 2026 and company wants to acheive 25,000 MW by 2030 & 50,000 MW installed capacity by 2040 as per management. (Take it with large pinch of Himalyan Salt

Most of new capacity is solar. They are not into EPC or Solar Manufacturing.

Company is developer and operator of Solar Power Plant selling energy thorugh PPA and direct contracts.

Currently over-extended i beleive but long term should compound well.

They are mostly into renewables now… one of their major Thermal plant is Buxar. Apart from this, I dont think they have any major Thermal.

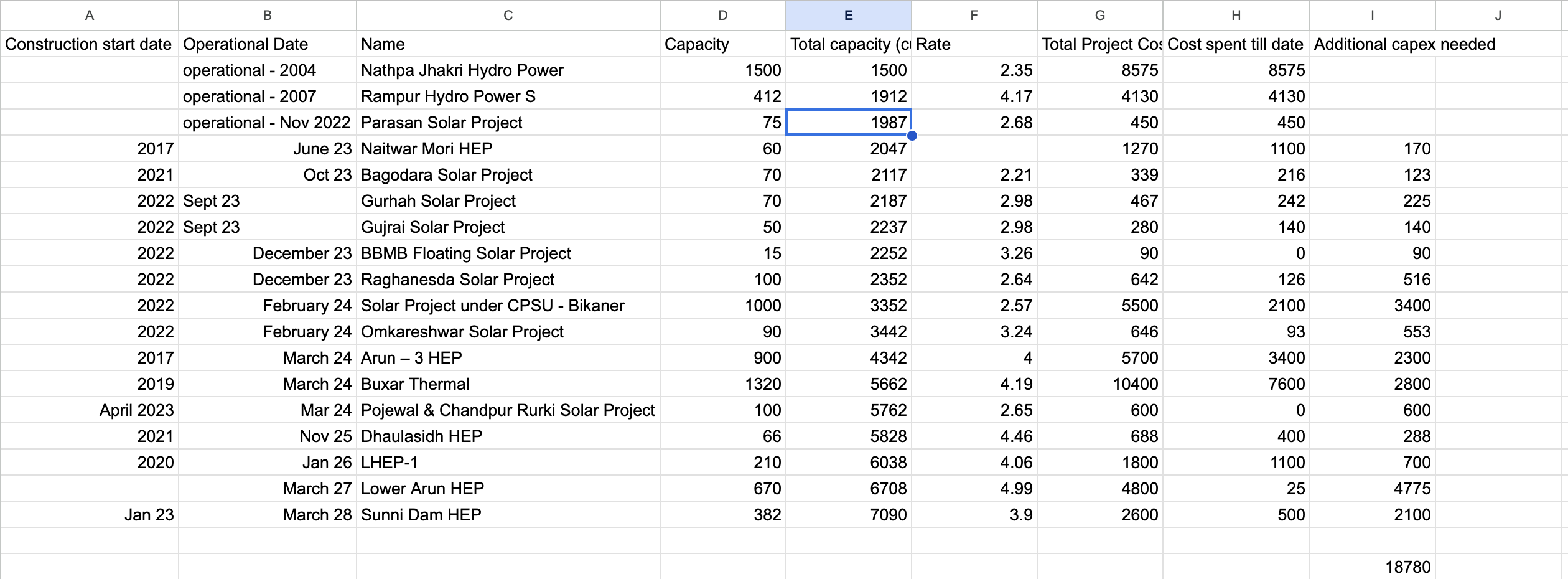

When I researched on SJVN in June 2023, they had installed capacity of about 2000 MW and had visible pipeline of 7000 MW capacity (image attached for my analysis until June 2023). At that point of time, they had vision to 20x their installed capacity by 2030 or so.

In last 6-8 months, they have got orders of atleast 4000 - 5000 MW, so now projections are at 12000 MW operational capacity by 2026-27.

They aim to increase their installed Capacity to 25 MW by 2030. Which will be more than 12x of their current capacity

SJVN has been designated as Renewal Energy Implementation Agency by Government of India. Through REIA SJVN collects the demand from the states / discoms and then for the renewal

energy, they invite bids from the developers. These developers build RE project, then the

PPOs are signed between these developers and the discoms of the states. And the SJVN will

get INR0.07 paisa per unit for this energy which we would be supplied to these discoms. There are 4 REIA in India at the moment.

All this growth will certainly bring in risks along:

Some project size are way too small, so too many projects to manage - Current capacity if 2000 MW with 5-6 projects. 6x increase in capacity is being achieved with about 50 projects.

Financial viability of small projects - small projects may be low margin

Huge capex needed for power projects would mean a very high debt and Interest payout, which may erode some profit margins.

What I am expected - With 12x capacity, revenues are expected to be 10-12x and Net Profits may increase 6-7x due to interest outgo in initial years + REIA opportunity would also bring in 2-2.5K profits over 4-6 years. REIA is a new thing for SJVN, not sure how it will play out.

My average buying price is 66, I am expecting a min of 6x from my invested price by 2030

Thanx LaryWink …Members have already indicated some numbers, though order book numbers keep increasing day by day.

Wanted to add that SJVN was basically a Hydro power producer.

But now since Hydro power is no longer preferred as it is inefficient way of producing power at a river by constructing a dam. The concept of hydropower has been snatched away to form Hydro pump storage system synched with Solar and Wind energy. So both NHPC and SJVN have both stopped constructing traditional hydro power stations. Both these companies are now bidding for Solar , wind , roof top solar.

Future looks bright , but past /present not so bright. However, bulging orde book gives future earning visibility.So execution is the key which is expected to reflect in financial performance in future.

Discl : Invested @33 level from the time the Green hydrogen thread was initiated. Recently booked some profit to get back my capital and still holding a major chunk.

Not a buy or sell recommendation. please make your own assessment before investing. Stock has run up quite a bit in anticipation of future performance. PSU’s have it’s own pros and cons

Can someone help me understand what this budgetary allocation actually means? Is it some form of grant that these companies get that they don’t have to pay back? How does this work?

I read in May 2019 concall that SJVN had installed capacity of 2015 MW. It planned to increase it to 5000 MW by 2023. However, as per the latest concall, its installed capacity is 2227 MW only which is very slight increase to its 2019 capacity. In the last concall also, ambitious targets (25000 MW by 2030) have been given.

Could someone please try to reconcile such staggering variance between ambitious goals and actual growth?

it’s evident that there has been a shift in the approach of company towards renewable energy expansion since 2023.

The landscape has evolved significantly with a stronger governmental emphasis on renewable energy installation and a concerted effort by companies to pursue aggressive bidding strategies, resulting in the procurement of substantial orders. These factors have catalyzed a more focused trajectory towards achieving the envisioned 2030 goals, as evidenced by the company’s proactive stance in securing contracts.

While the variance between the initial targets and the current installed capacity may seem significant, it’s essential to acknowledge the dynamic nature of the renewable energy sector and the recalibration of strategies in response to evolving market dynamics and regulatory frameworks.

Does anyone has calculated - For these much ambitious plan, how much debt they have to take? & What will be the D/E ratio ?

What is average time between project start & actual revenue generation in Solar & other renewable plants where they are getting orders? (I assume that for Solar, it will be very less than their traditional Hydro project - Where they have to construct dam & so on…)

Just to get idea, how bad initially their balance sheet will look like before completion of these projects. Also need to factored in project delays & cost over run etc.

SJVN’s ambitious expansion plans raise questions about debt levels and balance sheet health. Here’s a balanced analysis considering utilizing existing reserves:

Utilizing reserves:

While utilizing the ₹10,000 crore reserves could certainly reduce debt dependence, it wouldn’t be prudent to deplete them entirely. Reserves provide a safety net for unforeseen circumstances and future growth opportunities.

A strategic approach would be to use a portion of the reserves for equity contribution while leveraging debt responsibly.

Debt management:

SJVN already has significant debt, and exceeding their risk appetite could jeopardize financial stability.

Maintaining a healthy debt-to-equity (D/E) ratio is crucial. Current projections estimate a significant increase in debt, potentially impacting the D/E ratio.

Diversifying funding sources through green bonds, infrastructure investment trusts, and strategic partnerships could ease debt dependence.

Project timelines and impact:

Solar projects generally have shorter gestation periods (12-18 months) compared to hydro projects (5-10 years). This faster revenue generation can improve cash flow and mitigate debt burden quicker.

However, initial balance sheet impact during construction remains unavoidable, even with shorter solar project timelines.

Project delays and cost overruns further aggravate financial stress. SJVN needs robust project management and contingency plans to minimize such risks.

Overall:

Striking a balance between growth aspirations and prudent financial management is essential for SJVN’s long-term success.

Utilizing reserves strategically, diversifying funding sources, and mitigating project risks are key strategies to navigate ambitious expansion while maintaining financial health.

Additional factors to consider:

Government support: SJVN being a government-owned company might enjoy certain financial advantages and support.

Renewable energy push: The government’s focus on renewables could provide favorable financing options and regulations for SJVN’s green projects.