Company Analysis

S J Logistics- premier international logistics service provider, provides the services including freight forwarding, transportation, warehousing, Non-Vessel Operating Common Carrier & customs clearance.

TTMPE- 28

Market Cap-500

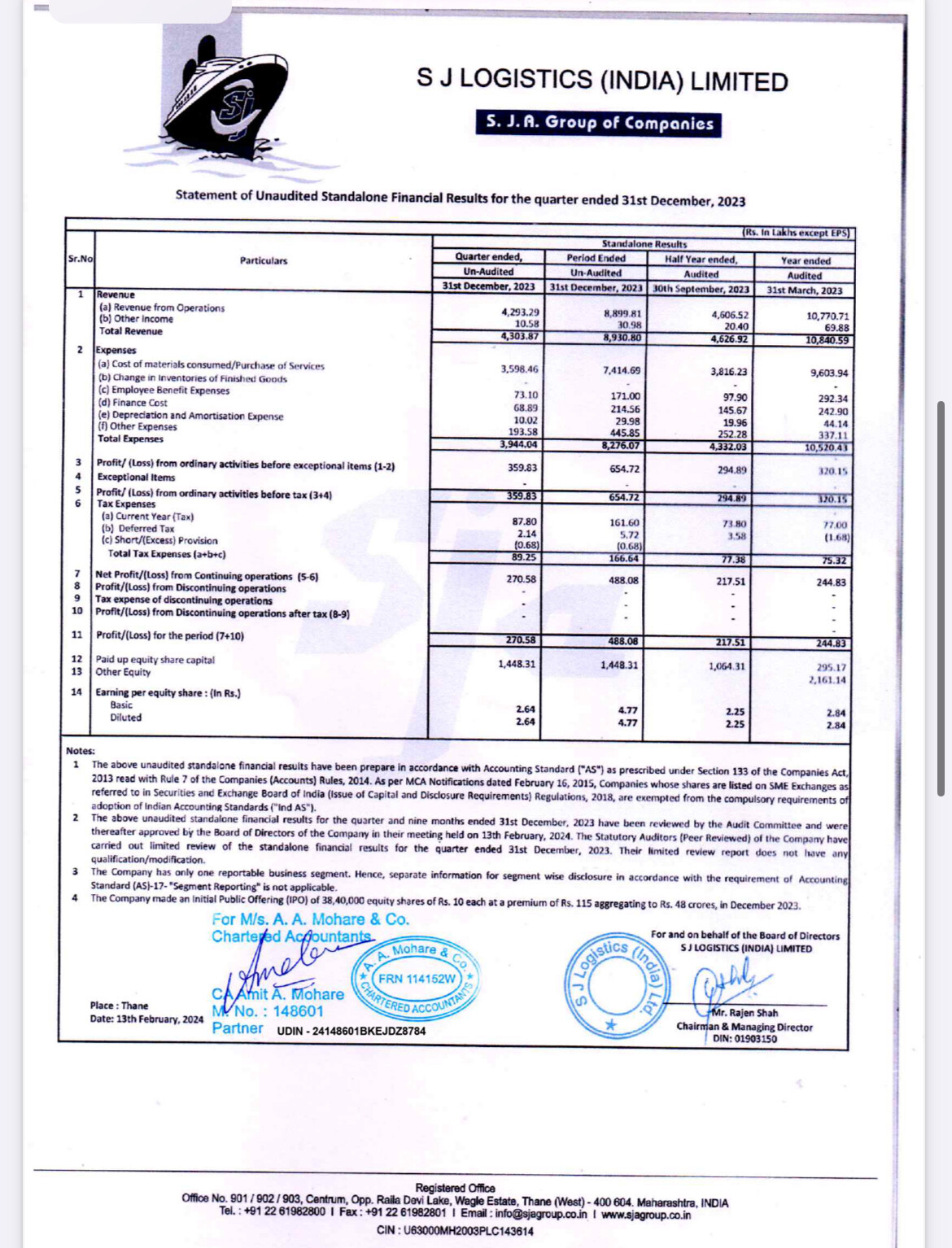

TTM PAT=7.6/4 (march23) + 9.3 (Sept)+ 6.2 (Dec) =17.4

TTM PE- 500/17.4 = 28.8

Services Offered-

FCL Shipping

Project Cargo

Warehousing

Non-Vessel Operating Common Carrier

Inland Transportation

Door Delivery

Customs House Agent (Across borders)

Air Freight

LCL (less than a container load and describes sea shipping for cargo loads not large)

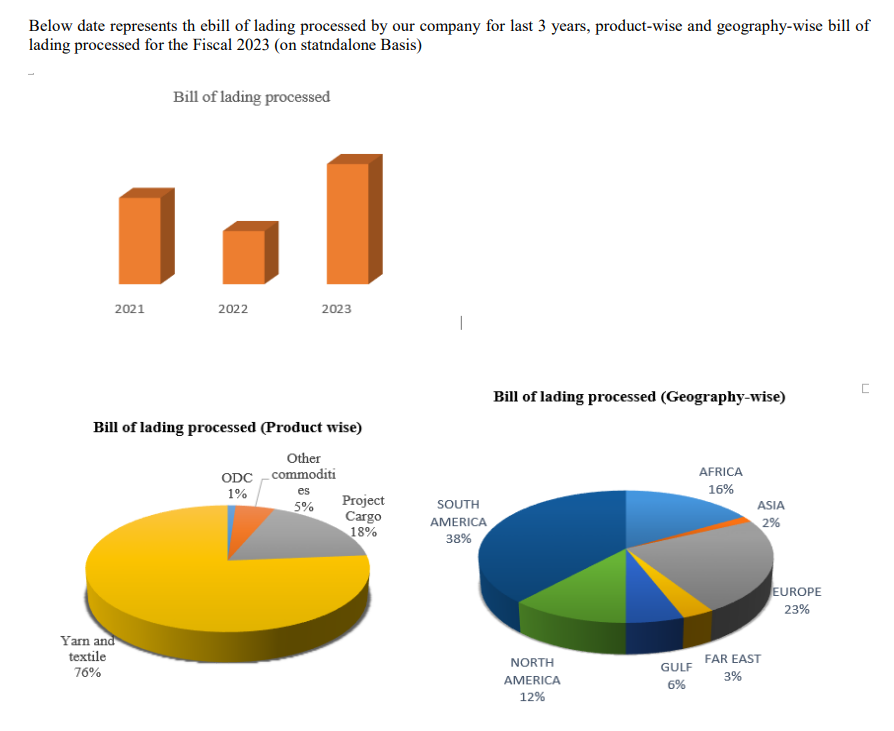

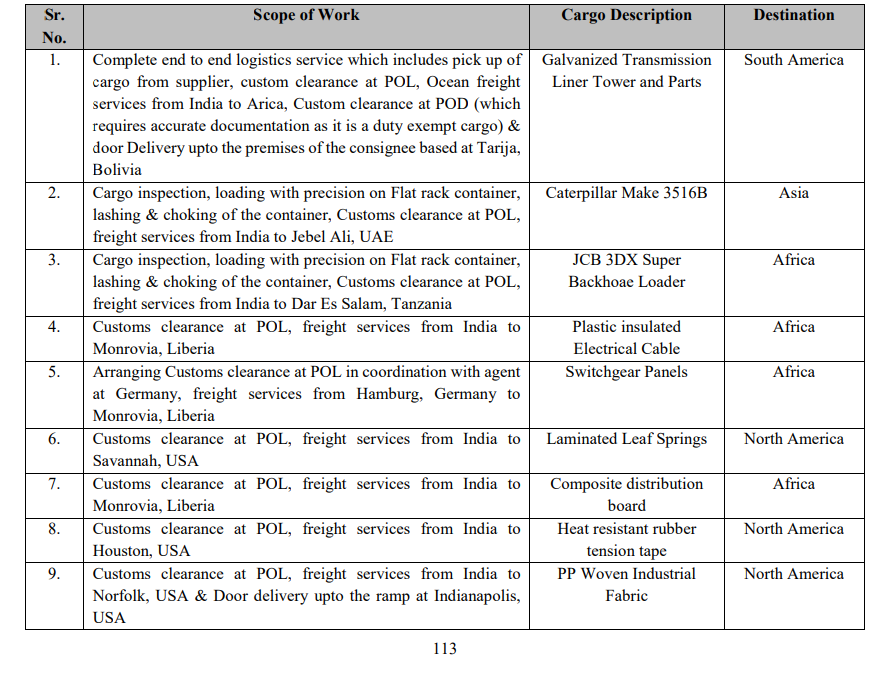

Major Focus on Project Cargo-The project cargos they have transported majorly includes earth moving equipment, transmission towers, ODC & break-bulk cargo and also undertake ODC (Over Dimension Cargo) which is out-gauge cargo that requires special handling, low bed trailer transportation

Red Sea Issue already brings up the container prices, its good for them.

Major Clients-

Skipper- (Solid growth in numbers, FYI)

SW Solar

Areva T&D

Transrail

Sterlite and etc

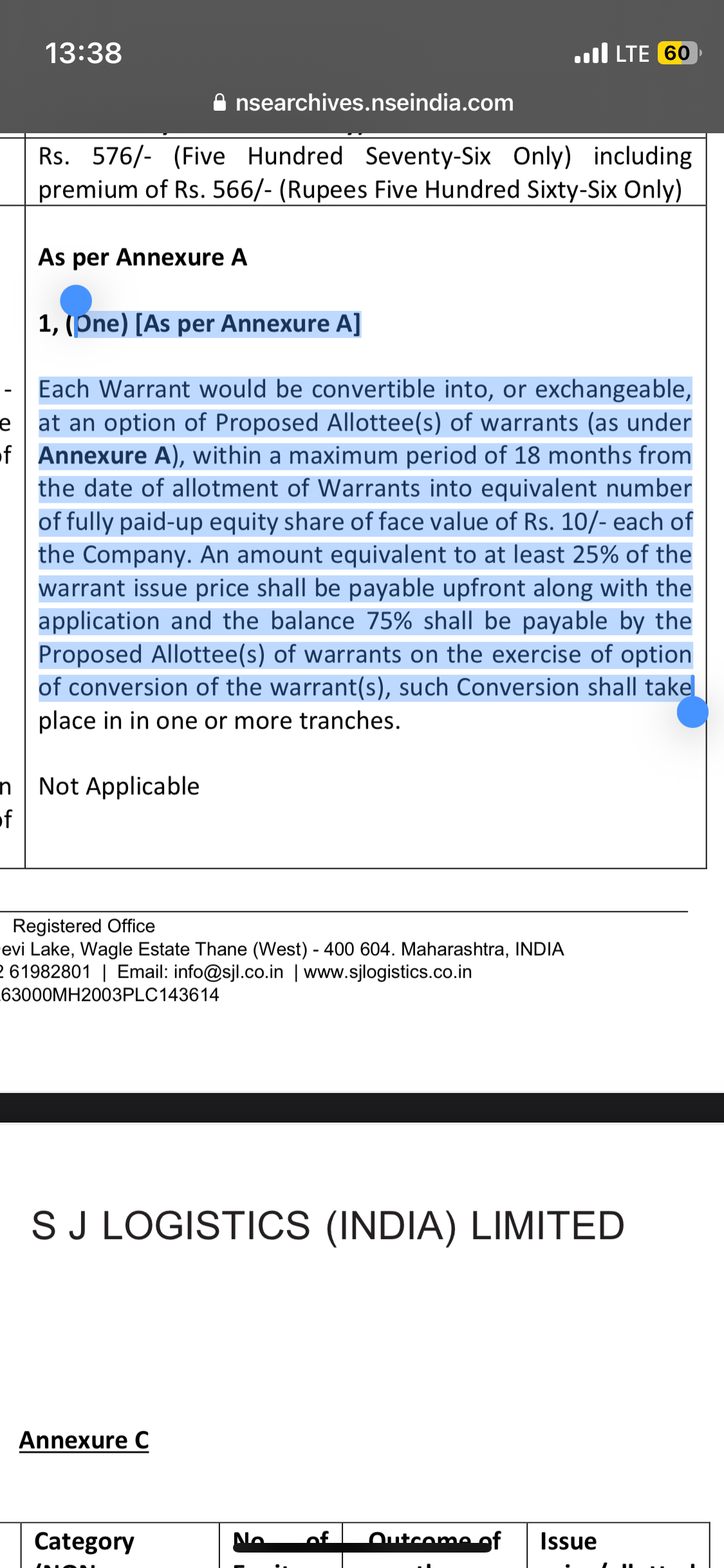

Company does repayment of loan amount and looking for expansion plans.

Recent Results- Solid Numbers are posted as 1 year PAT is achieved in 1 quarter…

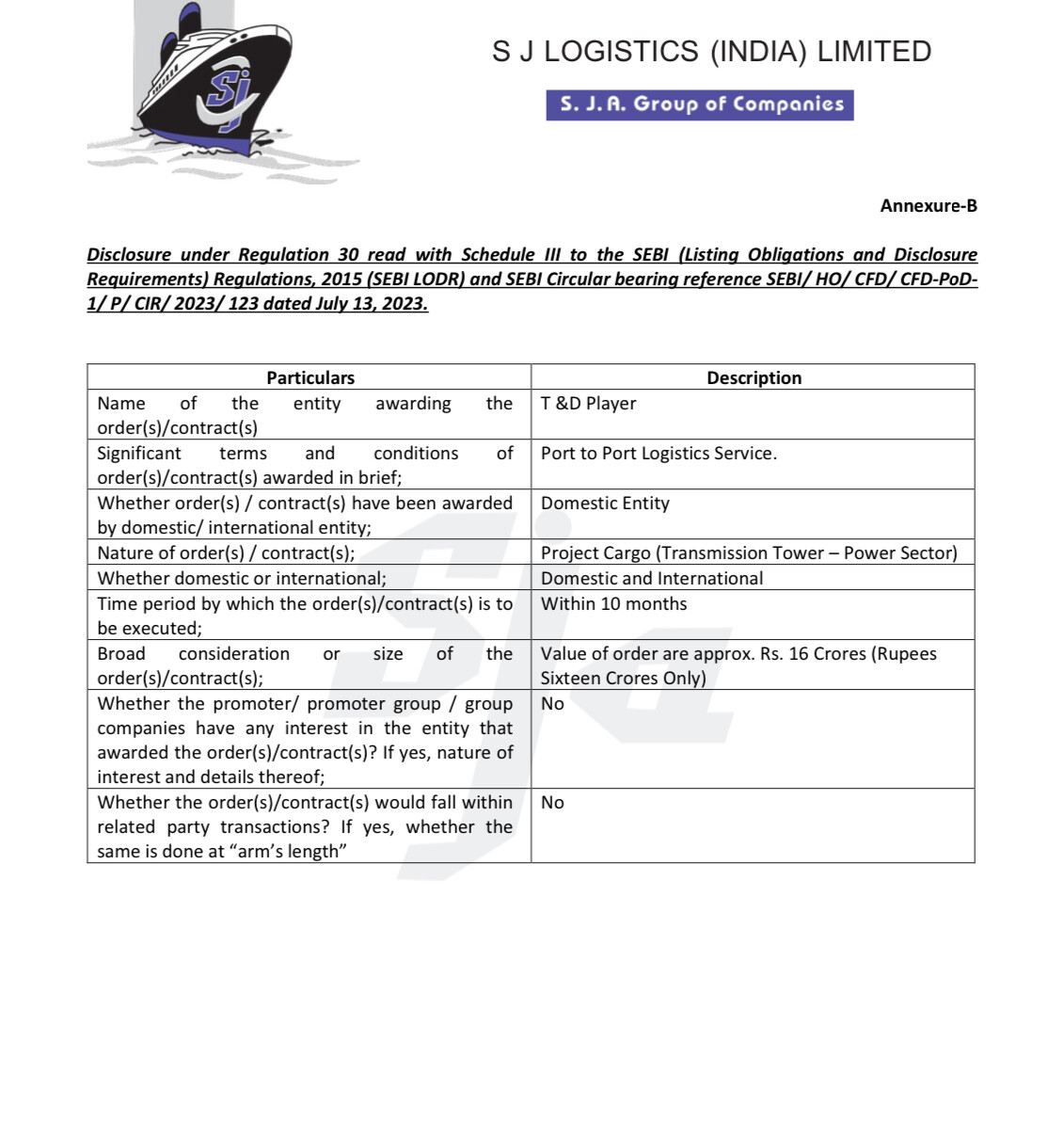

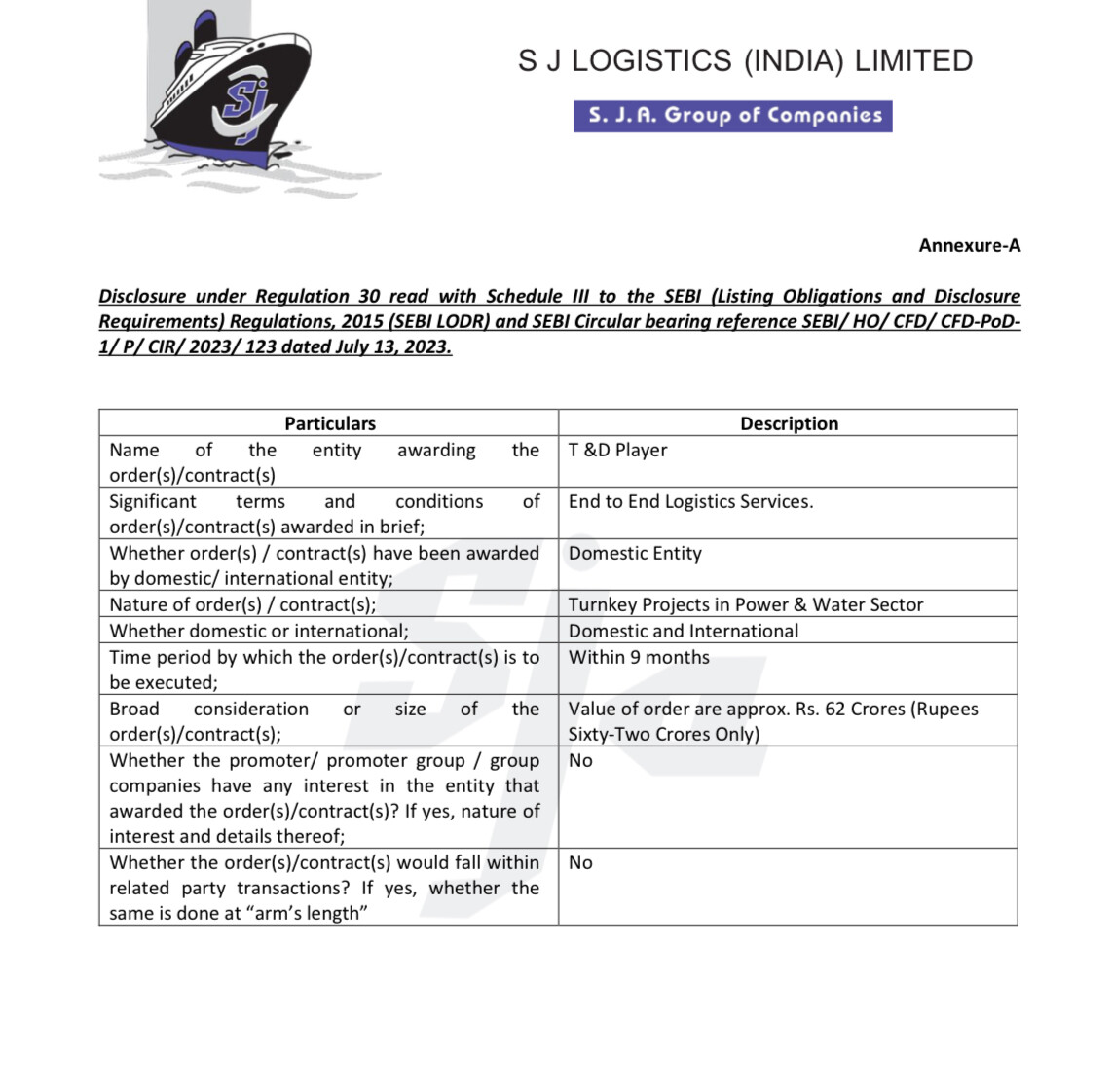

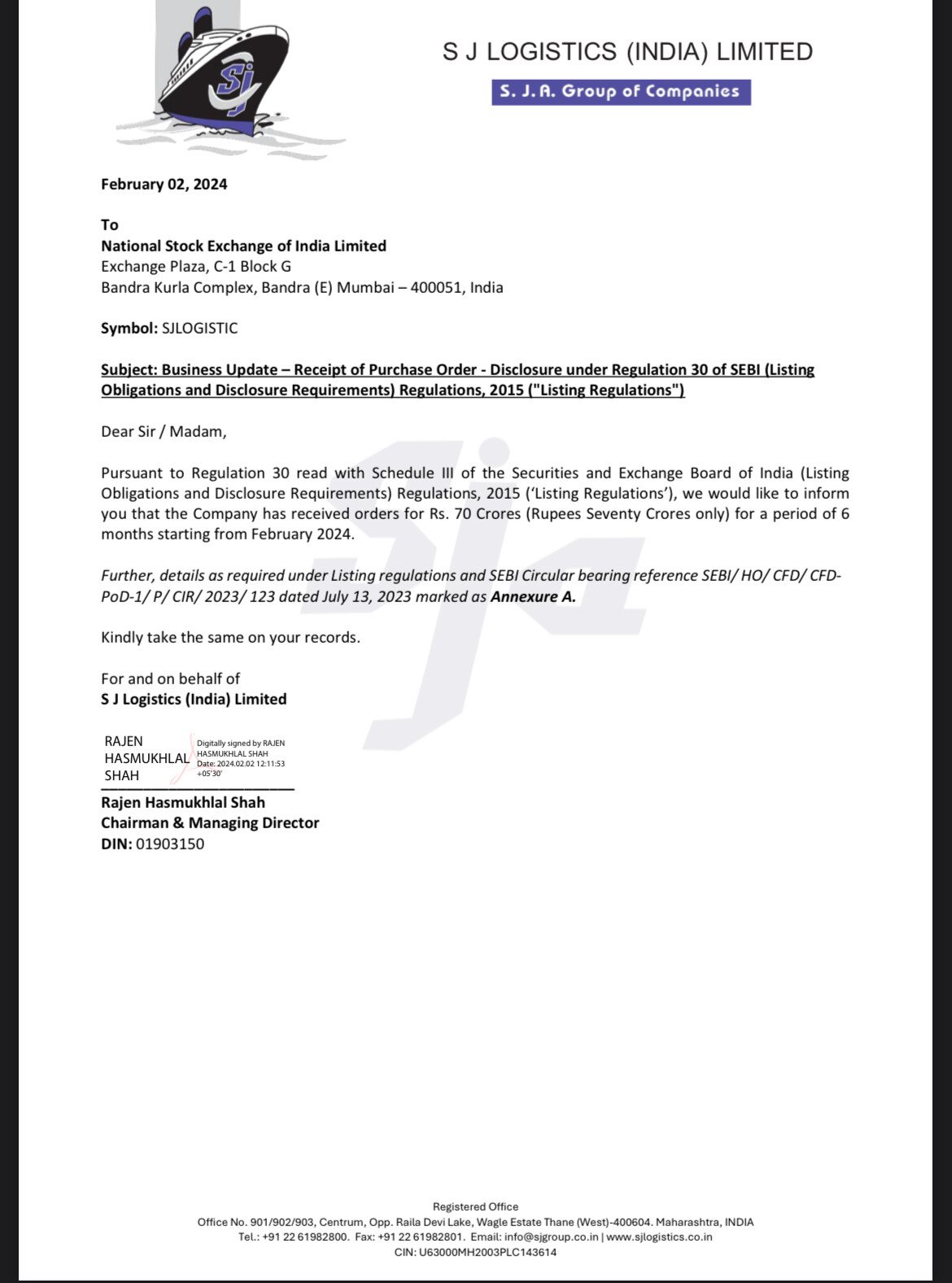

Recently got order worth 70 cr

Key Risk Factors—

Breakdown, mishaps or accidents could result in a loss or slowdown in operations

They don’t have Custom House Agent license.

Their logistic and freight business is largely dependent on export of yarn and yarn commodities

DYDD, Study at your own in depth.